Advanced packaging chip last-level cache SRAM macro Market Insights

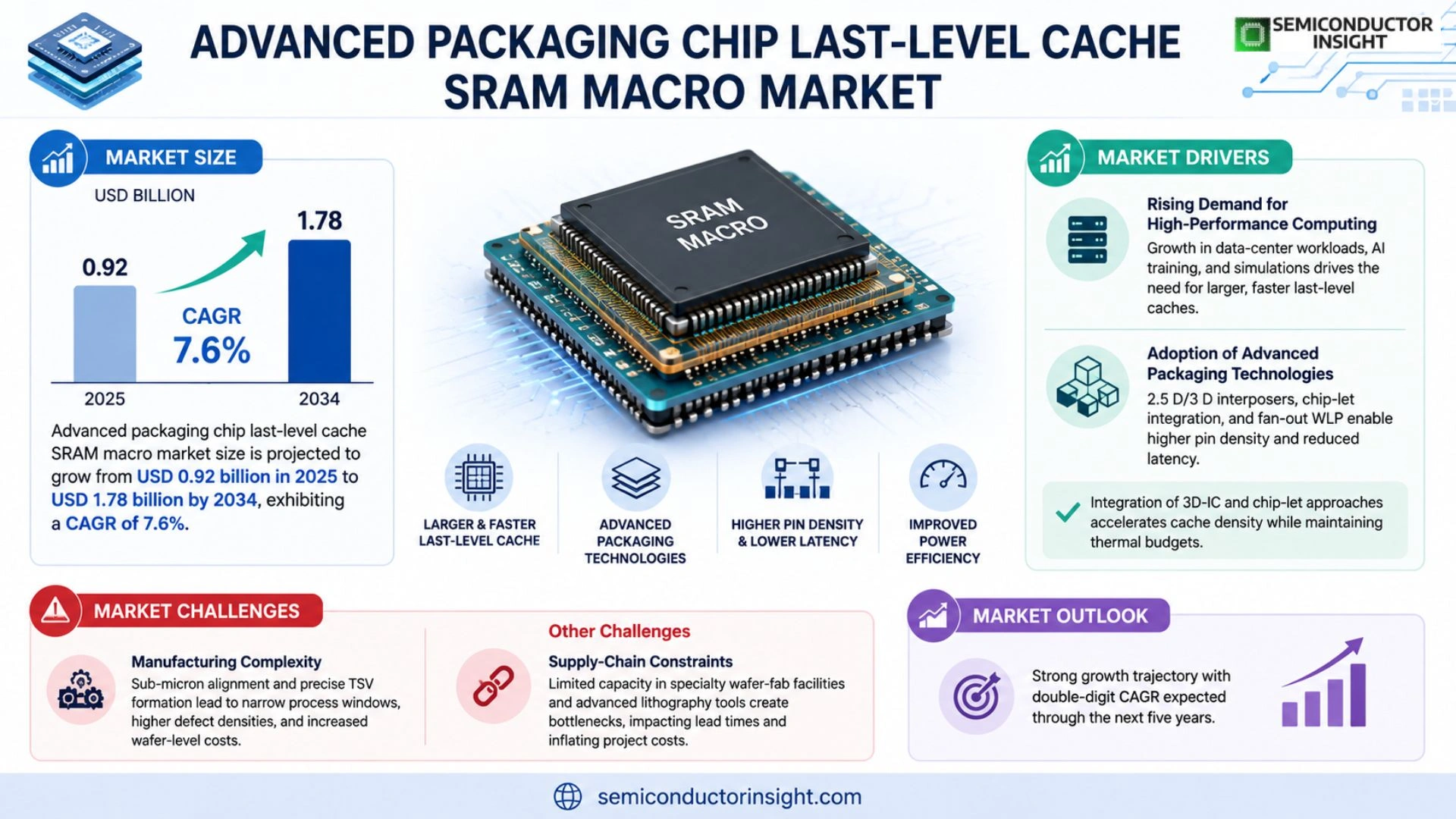

Global Advanced packaging chip last-level cache SRAM macro market size is projected to grow from USD 0.92 billion in 2025 to USD 1.78 billion by 2034, exhibiting a CAGR of 7.6% during the forecast period.

Advanced packaging chip last-level cache (LLC) SRAM macros are high‑density static random‑access memory blocks integrated within multi‑die stack packages to serve as the final caching tier for processors and accelerators. These macros deliver low latency access (<10 ns), high bandwidth (>200 GB/s), and power efficiency essential for AI inference, high‑performance computing, and edge devices.

The market is experiencing rapid growth due to escalating demand for heterogeneous integration, rising adoption of AI workloads that require larger on‑chip caches, and continued investment in wafer‑level fan‑out (WLP) and interposer technologies. Furthermore, industry leaders such as TSMC, Samsung Electronics, Intel Corp., ASE Group, and Amkor Technology are expanding their advanced packaging portfolios and forging collaborations to accelerate LLC SRAM macro deployment across data‑center processors and automotive SoCs.

MARKET DRIVERS

Rising Demand for High‑Performance Computing

Advanced packaging chip last-level cache SRAM macro Market is being propelled by exponential growth in data‑center workloads, AI training, and scientific simulations. Enterprises are investing in CPUs and GPUs that require larger, faster last‑level caches to sustain throughput, creating a clear need for more sophisticated SRAM macro solutions.

Adoption of Advanced Packaging Technologies

Technologies such as 2.5 D/3 D interposers, chip‑let integration, and fan‑out wafer‑level packaging are enabling higher pin density and reduced signal latency. These advances directly benefit last‑level cache SRAM macro designs, allowing manufacturers to meet the power‑efficiency targets of modern processors.

➤ Integration of 3D‑IC and chip‑let approaches accelerates cache density while maintaining thermal budgets.

Overall, the convergence of performance‑critical workloads and cutting‑edge packaging methods is establishing a strong growth trajectory for the market, with industry analysts forecasting double‑digit CAGR through the next five years.

MARKET CHALLENGES

Manufacturing Complexity

Producing high‑density SRAM macros within advanced packages demands sub‑micron alignment and precise TSV formation. The associated process windows are narrow, leading to higher defect densities and increased wafer‑level cost, which can deter mid‑range adopters.

Other Challenges

Supply‑Chain Constraints

Limited capacity in specialty wafer‑fab facilities and the need for advanced lithography tools create bottlenecks. This constraint pressures lead times and can inflate pricing for early‑stage projects.

MARKET RESTRAINTS

Design Validation Overheads

Validating signal integrity and thermal performance of last‑level cache SRAM macro within heterogeneous stacks requires extensive simulation and silicon‑prototype testing. The time and cost associated with these validation cycles act as a restraint, especially for startups lacking deep ASIC design expertise.

MARKET OPPORTUNITIES

Emerging Applications in Edge AI

Edge devices are increasingly executing AI inference locally to reduce latency and bandwidth usage. This shift creates an opportunity for compact, power‑efficient SRAM macros that can be integrated using advanced packaging to meet the stringent size and performance requirements of edge processors.

Advanced packaging chip last-level cache SRAM macro Market Trends

Rapid Growth Fueled by AI‑Intensive Workloads and Heterogeneous Integration

Advanced packaging chip last-level cache SRAM macro Market is witnessing a marked expansion as designers seek higher compute density and lower latency for AI inference and high‑performance computing. In 2025 the market was valued at roughly USD 0.92 billion and is projected to reach about USD 1.78 billion by 2034, reflecting strong demand for LLC SRAM macros that can deliver over 200 GB/s bandwidth while maintaining power efficiency. Key drivers include the rise of heterogeneous integration, the scaling of wafer‑level fan‑out and interposer technologies, and the need for larger on‑chip caches to support emerging edge and data‑center processors.

Other Trends

Technology Adoption and Design Advances

Advanced packaging solutions such as chip‑on‑wafer, fan‑out panel, and embedded interposers are becoming mainstream, enabling LLC SRAM macros to be co‑located with logic dies in multi‑die stack configurations. This architectural shift shortens data paths, reduces signal loss, and improves energy per operation, which is critical for AI accelerators. Foundries and assembly houses are also standardizing design‑for‑test and reliability methodologies to accelerate time‑to‑market, while simulation tools are increasingly integrating thermal and mechanical analysis for dense stack designs.

Competitive Landscape and Strategic Partnerships

Major players such as TSMC, Samsung Electronics, Intel Corp., ASE Group, and Amkor Technology are expanding their advanced packaging portfolios and entering joint development agreements to accelerate deployment of LLC SRAM macro solutions. These collaborations focus on scaling production capacities, sharing IP for cache controller integration, and co‑optimizing supply chains for automotive and industrial IoT segments. As the ecosystem matures, a competitive emphasis on yield improvement and cost‑effective back‑end processes is expected to shape the market’s next phase of growth.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Packaging Chip LLC SRAM Macro Competitive Landscape

Advanced packaging chip last‑level cache (LLC) SRAM macro market is dominated by a small group of integrated‑device manufacturers that combine leading‑edge wafer‑level fan‑out (WLP), interposer and 2.5‑D/3‑D stacking capabilities. TSMC leverages its extensive CoWoS ecosystem to supply high‑density LLC SRAM blocks for hyperscale data‑center CPUs, while Samsung Electronics integrates its own memory IP with advanced fan‑out packaging to achieve sub‑50 ps latency. Intel Corp. capitalizes on in‑house packaging R&D to embed SRAM macros within its Xeon and Alder Lake platforms, creating a vertically integrated supply chain. ASE Group and Amkor Technology function as pure‑play advanced‑packaging service providers, offering turnkey solutions that enable fabless designers to access LLC SRAM without building proprietary fabs. Together these leaders shape a market structure where design‑wins are closely tied to packaging differentiation and the ability to deliver 200 GB/s bandwidth at low power.

Beyond the tier‑one tier, a broader set of niche players contributes specialized capabilities that enrich the ecosystem. GlobalFoundries focuses on mixed‑signal integration, delivering customized LLC SRAM for automotive SoCs. STMicroelectronics and NXP Semiconductors supply automotive‑grade memory blocks paired with robust packaging for safety‑critical applications. Micron Technology and SK Hynix provide high‑density SRAM IP that is packaged by third‑party assemblers to reach emerging AI edge markets. JCET Group and Powertech Technology (PTI) excel in advanced flip‑chip interconnects, while TSMC’s partner ecosystem includes TowerJazz and X‑Fab for specialty process nodes. These companies collectively broaden the competitive landscape, ensuring a diversified supply base for next‑generation high‑performance computing and AI inference workloads.

List of Key Advanced Packaging Chip LLC SRAM Macro Companies Profiled

- TSMC

- Samsung Electronics

- Intel Corp.

- ASE Group

- Amkor Technology

- GlobalFoundries

- STMicroelectronics

- NXP Semiconductors

- Micron Technology

- SK Hynix

- JCET Group

- Powertech Technology (PTI)

- TowerJazz

- X‑Fab

- Renesas Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

High‑density SRAM is emerging as the dominant type because it satisfies the pressing need for larger on‑chip caches in AI accelerators and high‑performance computing. It enables designers to pack more bits per unit area, supporting heterogeneous integration trends. ● Offers ultra‑low access latency essential for real‑time inference. ● Provides power‑efficiency benefits that align with edge‑device constraints. ● Integrates seamlessly with wafer‑level fan‑out and interposer platforms, accelerating time‑to‑market for advanced processors. |

| By Application |

|

Data‑center processors lead the application landscape as enterprises demand higher throughput for AI training and inference workloads. ● The need for rapid data movement pushes designers toward LLC SRAM that can sustain multi‑hundred gigabyte‑per‑second bandwidth. ● Energy‑constrained data‑center designs benefit from the power‑saving attributes of advanced packaging SRAM. ● Automotive SoCs follow closely, driven by autonomous‑driving compute that relies on fast, reliable cache hierarchies. |

| By End User |

|

Chip manufacturers dominate the end‑user segment, leveraging advanced packaging to differentiate next‑generation products. ● They prioritize design‑for‑manufacturability to reduce cycle times for AI‑centric silicon. ● Collaborative ecosystems with packaging specialists (e.g., TSMC, Intel) enhance technology transfer and reduce risk. ● System integrators appreciate the modularity of LLC SRAM macros for building heterogeneous compute stacks. |

| By Integration Technology |

|

Interposer‑based stacking is gaining traction because it offers the highest bandwidth path between compute cores and LLC SRAM. ● Provides a highly controlled electrical environment that minimizes signal‑integrity challenges. ● Aligns with the industry push toward heterogeneous integration, enabling co‑fabrication of logic and memory. ● Supports higher thermal budgets, which is crucial for high‑performance AI accelerators. |

| By End Market |

|

Artificial Intelligence drives the strongest demand for advanced LLC SRAM because AI models require rapid access to large working sets. ● The push for on‑device inference amplifies the need for compact, power‑efficient cache blocks. ● HPC workloads benefit from deterministic latency offered by tightly integrated SRAM macros. ● Automotive adoption is propelled by safety‑critical compute that cannot tolerate cache misses. |

Regional Analysis: Asia-Pacific

The Asia-Pacific region boasts a well-established and sophisticated manufacturing ecosystem for semiconductors. Countries like Taiwan and South Korea are global leaders in front-end and back-end processing, providing a strong foundation for advanced packaging chip last-level cache SRAM macro Market growth. Continuous investments in state-of-the-art fabrication facilities are enhancing the region’s manufacturing capabilities.

Governments across Asia-Pacific are actively promoting semiconductor innovation and manufacturing through substantial financial support and strategic policies. These initiatives aim to reduce reliance on foreign suppliers and foster domestic talent development in advanced packaging technologies. Tax incentives and research grants are attracting investments in R&D and production facilities.

The Asia-Pacific semiconductor market is home to numerous key players involved in the development and production of advanced packaging chip last-level cache SRAM macro Market solutions. These include established integrated device manufacturers (IDMs), fabless design houses, and contract manufacturing organizations (CMOs) located throughout the region. Strategic collaborations and partnerships are common among these players to drive innovation and expand market reach.

The demand for advanced packaging chip last-level cache SRAM macro Market is being driven by the increasing adoption of advanced technologies in various applications, including high-performance computing, artificial intelligence, and 5G communication. The growth of the automotive industry, with its increasing reliance on electronic control units (ECUs), is also contributing to the demand for these sophisticated SRAM solutions.

North America

The North American market for advanced packaging chip last-level cache SRAM macro Market is characterized by a strong focus on innovation and high-performance applications, particularly within the data center and aerospace & defense sectors. While representing a mature market, ongoing research and development efforts are geared towards enhancing the efficiency and reliability of advanced packaging solutions. Significant investments are being made in advanced manufacturing capabilities and collaborations between academic institutions and industry players. The market is driven by demand for high-bandwidth memory and low-latency SRAM in cutting-edge computing systems.

Europe

Europe’s advanced packaging chip last-level cache SRAM macro Market is experiencing steady growth, driven by the increasing demand for sophisticated electronics in automotive, industrial automation, and consumer electronics. Government initiatives aimed at fostering semiconductor manufacturing within the region are gaining momentum. Key players are focusing on developing energy-efficient and high-reliability SRAM solutions for demanding applications. Collaboration within the European Union is facilitating research and development efforts and promoting a more cohesive semiconductor ecosystem.

South America

The South American market for advanced packaging chip last-level cache SRAM macro Market is relatively nascent but exhibits significant growth potential. The expanding telecommunications infrastructure and increasing adoption of digital technologies are driving demand for advanced semiconductors. The automotive sector is also contributing to market growth, particularly with the adoption of connected and autonomous vehicle technologies. While the market is currently smaller compared to other regions, it presents a promising long-term opportunity for advanced packaging providers.

Middle East & Africa

The Middle East & Africa region represents a growing market for advanced packaging chip last-level cache SRAM macro Market, spurred by increasing investments in infrastructure development, digital transformation, and the expansion of the automotive industry. The demand for advanced semiconductors is expected to rise significantly in the coming years, driven by the growth of smart cities, industrial automation, and 5G deployments. Government initiatives promoting technological advancement are also contributing to market growth.

Report Scope

This market research report provides a comprehensive analysis of the Advanced packaging chip last-level cache SRAM macro Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Advanced packaging chip last-level cache SRAM macro Market?

-> Advanced packaging chip last-level cache SRAM macro Market was valued at USD 0.92 billion in 2025 and is expected to reach USD 1.78 billion by 2034.

Which key companies operate in Advanced packaging chip last-level cache SRAM macro Market?

-> Key players include TSMC, Samsung Electronics, Intel Corp., ASE Group, and Amkor Technology, among others.

What are the key growth drivers?

-> Key growth drivers include escalating demand for heterogeneous integration, increasing AI workloads that require larger on‑chip caches, and continued investment in wafer‑level fan‑out (WLP) and interposer technologies.

Which region dominates the market?

-> The reference does not specify a dominant region for this market.

What are the emerging trends?

-> Emerging trends include advancements in AI inference applications, broader adoption of wafer‑level fan‑out and interposer solutions, and expanding advanced‑packaging portfolios by leading semiconductor manufacturers.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...