MARKET INSIGHTS

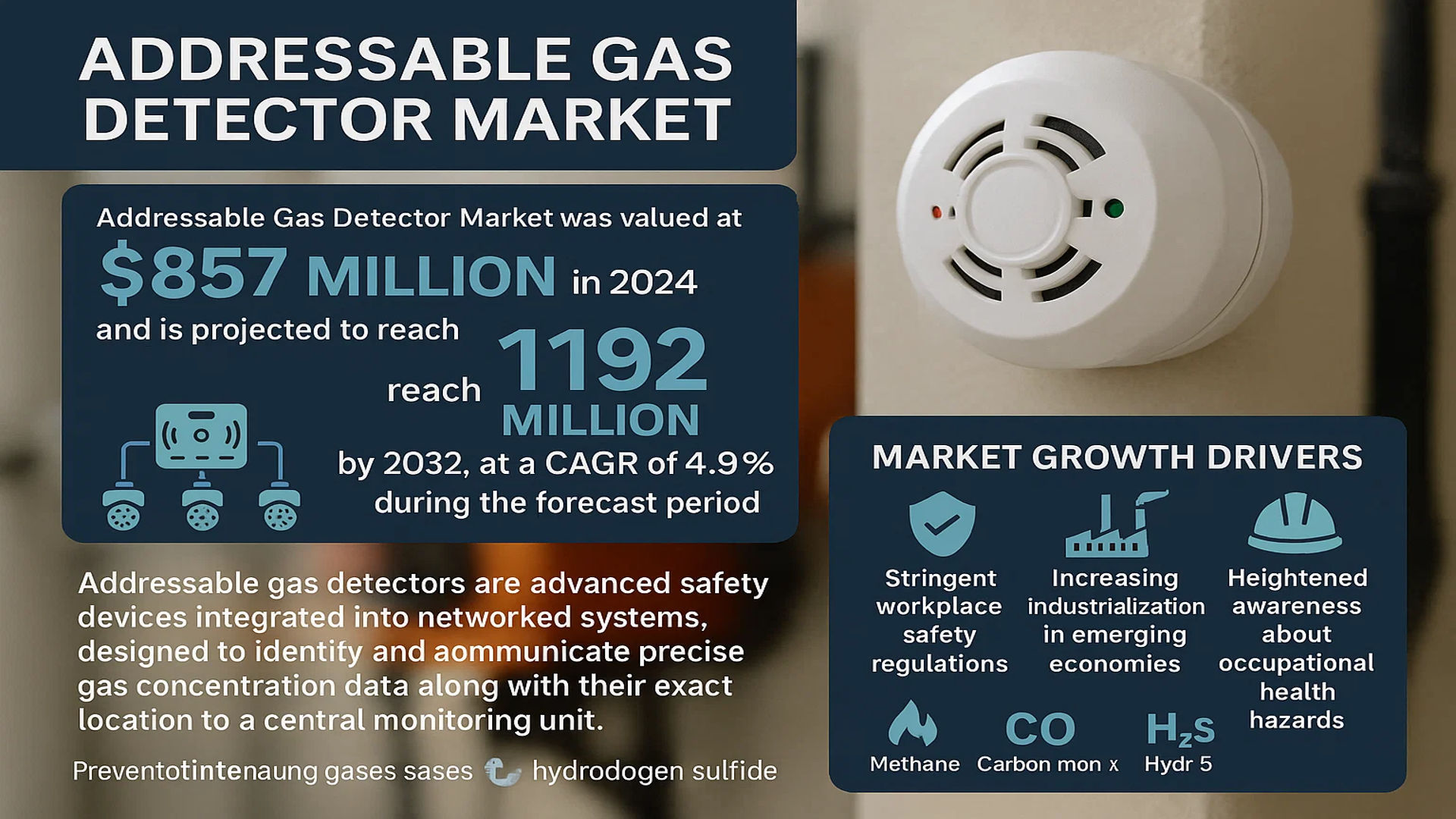

The global Addressable Gas Detector Market was valued at 857 million in 2024 and is projected to reach US$ 1192 million by 2032, at a CAGR of 4.9% during the forecast period.

Addressable gas detectors are advanced safety devices integrated into networked systems, designed to identify and communicate precise gas concentration data along with their exact location to a central monitoring unit. These systems play a critical role in industrial safety by enabling real-time detection of hazardous gases such as methane, carbon monoxide, and hydrogen sulfide, thereby preventing potential accidents and ensuring regulatory compliance.

The market growth is driven by stringent workplace safety regulations, increasing industrialization in emerging economies, and heightened awareness about occupational health hazards. However, high installation costs and the need for skilled personnel pose challenges. Leading manufacturers like Honeywell, Drager, and MSA are investing in IoT-enabled smart detectors, which is expected to create new growth opportunities in the coming years.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Industrial Safety Regulations to Propel Market Expansion

The global addressable gas detector market is experiencing robust growth driven by increasingly stringent workplace safety regulations across industries. Governments worldwide have intensified compliance requirements for occupational exposure limits to hazardous gases, mandating real-time monitoring systems in high-risk environments. In the oil and gas sector alone, which accounts for over 35% of detector deployments, updated OSHA and other international standards now require networked detection systems capable of pinpointing gas leak locations instantly. This regulatory push has created a $280 million annual compliance-driven demand, particularly in North America and Europe where enforcement is most rigorous.

Growing Industrial Automation to Accelerate Market Adoption

Industry 4.0 transformation across manufacturing sectors is creating significant demand for intelligent gas detection systems that integrate with plant-wide automation networks. Addressable detectors now form critical components of smart factory ecosystems, with their data being incorporated into predictive maintenance algorithms and centralized safety dashboards. The manufacturing sector’s adoption has grown at 6.2% annually as facilities upgrade from standalone detectors to networked solutions that provide location-specific alerts through SCADA integration. Recent advancements in industrial IoT protocols have enabled seamless connectivity between gas detectors and plant control systems, further driving replacement demand.

Expanding Oil Exploration Activities to Boost Demand

The resurgence of offshore oil exploration and shale gas production is generating substantial demand for robust gas detection infrastructure. With over 150 new offshore platforms scheduled for deployment in the next five years and shale gas production projected to increase by 18% globally, the need for advanced detection systems that can operate in harsh environments while providing precise location data has become critical. Oilfield operators are increasingly specifying addressable systems that can withstand extreme conditions while maintaining accuracy, with the sector accounting for 28% of new system installations last year.

MARKET RESTRAINTS

High Initial Costs to Impede Small Enterprise Adoption

While addressable gas detector systems offer superior safety features, their significant upfront investment remains a key market constraint. Complete networked solutions can cost 40-60% more than conventional detectors, creating adoption challenges for small and medium enterprises. The average price point for industrial-grade addressable systems ranges from $3,500-$7,000 per sensing point, with full facility deployments often exceeding $100,000. These capital requirements have limited penetration in developing markets and small-scale operations where budget constraints outweigh safety considerations, particularly in the food processing and light manufacturing sectors.

Technical Limitations in Extreme Conditions Restrict Applications

Addressable systems face performance challenges in certain industrial environments that limit their applicability. High-temperature operations above 60°C can degrade sensor accuracy, while corrosive atmospheres in chemical plants reduce equipment lifespan. Humidity levels exceeding 95% have been shown to produce false positives in some catalytic bead sensors, creating operational disruptions. These technical constraints have slowed adoption in sectors like metal processing and pulp manufacturing where environmental conditions often exceed standard detector specifications, forcing continued reliance on traditional solutions.

MARKET CHALLENGES

Shortage of Skilled Installation Technicians Creates Deployment Bottlenecks

The specialized nature of addressable system installation and calibration has created a workforce gap that threatens market growth. Certified technicians capable of properly configuring networked detectors and validating system-wide performance remain scarce, with industry estimates suggesting a 35% deficit in qualified personnel. This skills shortage has led to project delays averaging 8-12 weeks in some regions, particularly for complex multi-zone installations where proper commissioning is critical. The challenge is compounded by the rapid technological evolution of detection systems, requiring continuous technician retraining.

False Alarm Management Remains Persistent Operational Challenge

False positive readings continue to undermine confidence in addressable systems despite technological advancements. Industrial environments with fluctuating air compositions or high particulate levels experience alarm rates up to 15% higher than laboratory conditions, leading to operational disruptions. The food processing sector reports particular challenges with vapor interference triggering unnecessary shutdowns. While machine learning algorithms show promise in reducing false alerts, their implementation remains limited to only 12% of installed systems due to computational requirements and validation concerns.

MARKET OPPORTUNITIES

Emerging Economies Present Significant Growth Potential

Developing nations represent the most substantial untapped market for addressable gas detectors as industrial safety standards evolve. Countries like India and Brazil have shown 22% annual growth in safety system investments as their manufacturing bases expand and regulatory frameworks mature. The ASEAN region alone is projected to add over 50,000 new detector nodes annually as petrochemical complexes and energy infrastructure projects multiply. Localized production and financing models are making these systems more accessible, with regional manufacturers capturing 40% of the market through cost-optimized solutions.

Smart City Development Creates New Application Areas

Urban infrastructure projects are opening new deployment scenarios for addressable gas detection technology. Municipal gas distribution networks are increasingly incorporating networked detectors into their IoT platforms, with 120 major cities worldwide now piloting smart leak detection grids. Underground parking facilities and wastewater treatment plants represent additional growth frontiers, with these applications growing at 18% annually. The convergence of public safety requirements and smart infrastructure investments is expected to create a $220 million opportunity for networked gas detection by 2027.

AI Integration to Unlock Predictive Capabilities

Artificial intelligence is poised to transform addressable systems from reactive tools to predictive safety assets. Advanced analytics applied to detector networks can now identify patterns preceding gas release events, enabling preventative maintenance. Early adopters in the chemical sector have reported 30% reductions in unplanned downtime through these predictive capabilities. The integration of weather data and process variables further enhances detection accuracy, with next-generation systems expected to achieve 98% reliability in distinguishing actual threats from environmental noise.

ADDRESSABLE GAS DETECTOR MARKET TRENDS

Increasing Industrial Safety Regulations to Boost Market Growth

The global addressable gas detector market is witnessing significant growth due to stricter workplace safety regulations across industries. Governments and regulatory bodies are mandating the installation of advanced gas detection systems to prevent accidents in high-risk environments like oil & gas facilities, chemical plants, and mining operations. The U.S. Occupational Safety and Health Administration (OSHA) and the European Union’s ATEX directives have set stringent guidelines, compelling companies to adopt reliable detection solutions. As a result, the market is projected to grow at a CAGR of 4.9%, reaching $1.19 billion by 2032 from $857 million in 2024. The oil & gas sector, particularly in North America and the Middle East, has been a major driver of this demand.

Other Trends

Integration of IoT and Wireless Technologies

The integration of Internet of Things (IoT) capabilities in gas detection systems is reshaping the market landscape. Modern addressable gas detectors now feature real-time wireless connectivity, cloud-based monitoring, and predictive analytics to enhance safety management. These smart detectors provide remote access to critical gas concentration data, enabling faster response times during emergencies. The adoption of WirelessHART and LoRaWAN protocols has further improved system reliability in large industrial facilities. China’s manufacturing sector, in particular, has shown rapid adoption of these connected safety solutions, contributing to regional market expansion.

Growing Demand in Emerging Economies

Developing nations are demonstrating increased demand for addressable gas detectors due to rapid industrialization and infrastructure development. Countries like India, Brazil, and Indonesia are investing heavily in petrochemical plants, power generation facilities, and water treatment centers that require robust gas monitoring systems. The Asia-Pacific region is expected to register the highest growth rate of 6-7% annually, driven by China’s dominant position in manufacturing and India’s expanding oil refinery capacity. Meanwhile, Middle Eastern countries continue to prioritize safety upgrades in their massive hydrocarbon processing facilities, creating sustained demand for advanced detection technologies.

Technological Advancements in Sensor Capabilities

Recent innovations in multi-gas detection and infrared sensor technology are expanding application possibilities for addressable systems. Manufacturers are developing detectors capable of simultaneously monitoring multiple hazardous gases with greater accuracy and lower maintenance requirements. The introduction of laser-based detection methods has improved performance in challenging environments with extreme temperatures or high humidity. These technological enhancements are particularly valuable for the food & beverage industry, where precise gas monitoring during packaging and storage processes is essential for quality control and regulatory compliance.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Product Innovation & Market Expansion Drive Competition

The global addressable gas detector market features a mix of multinational corporations and regional players competing through technological differentiation and safety compliance expertise. Industry leader Honeywell International Inc. dominates with over 15% market share, leveraging its connected safety solutions across oil & gas, chemicals, and manufacturing sectors. Their Sensepoint XLC series, launched in 2023, introduced wireless mesh networking capabilities that significantly enhanced installation flexibility in hazardous areas.

German firm Drägerwerk AG maintains strong positioning in Europe through its Polytron® 8900 series, which incorporates AI-driven predictive maintenance features. Meanwhile, MSA Safety Incorporated has gained traction in North America’s mining sector with its intrinsically safe designs, capturing approximately 12% of regional sales.

Japanese manufacturer Riken Keiki Co., Ltd. leads Asia-Pacific adoption through compact form factors optimized for confined spaces, while Industrial Scientific Corporation continues to expand its iNet® cloud platform globally, demonstrating 18% year-over-year growth in connected device subscriptions.

Market dynamics show:

- Top 5 players control ~45% of 2024 revenue

- 25% of new product launches in 2023-24 focused on IoT integration

- Strategic acquisitions increasing, with 7 major M&A deals since 2022

List of Key Addressable Gas Detector Manufacturers

- Honeywell International Inc. (U.S.)

- Drägerwerk AG & Co. KGaA (Germany)

- MSA Safety Incorporated (U.S.)

- Riken Keiki Co., Ltd. (Japan)

- Industrial Scientific Corporation (U.S.)

- 3M Company (U.S.)

- New Cosmos Electric Co., Ltd. (Japan)

- Shenzhen ExSAF Electronics Co. (China)

- United Technologies Corporation (U.S.)

- Johnson Controls International (Ireland)

Recent competitive developments include Emerson’s 2024 acquisition of portable gas detection specialist Trolex, while smaller players like Chengdu Action Electronics are gaining share in developing markets through cost-optimized solutions. The market remains innovation-driven, with most competitors allocating 8-12% of revenues to R&D for advanced detection algorithms and communication protocols.

Segment Analysis:

By Type

Wall Mounted Segment Leads Due to Its Widespread Industrial Adoption

The market is segmented based on type into:

- Wall Mounted

- Hand Held

- Others

By Application

Oil and Gas Sector Dominates with Highest Safety Requirement

The market is segmented based on application into:

- Oil and Gas

- Mining

- Manufacturing Industry

- Food and Beverage

- Others

By Technology

Infrared Technology Gains Traction for Combustible Gas Detection

The market is segmented based on technology into:

- Electrochemical

- Infrared

- Catalytic

- Metal Oxide Semiconductor (MOS)

By Connectivity

Wired Addressable Systems Maintain Strong Market Position

The market is segmented based on connectivity into:

- Wired

- Wireless

Regional Analysis: Addressable Gas Detector Market

North America

North America leads the global Addressable Gas Detector market, driven by stringent workplace safety regulations and advanced industrial infrastructure. The U.S. Occupational Safety and Health Administration (OSHA) mandates strict gas monitoring compliance, particularly in oil & gas and chemical sectors. With the region accounting for over 30% of global market revenue, major players like Honeywell and MSA dominate with technologically advanced solutions. Recent investments in smart manufacturing and IIoT integration are accelerating demand for networked gas detection systems. However, high product costs and saturation in mature markets slightly restrain growth compared to emerging regions.

Asia-Pacific

The Asia-Pacific region exhibits the highest growth potential, projected to grow at 5.8% CAGR through 2032. China’s booming industrial sector and India’s expanding oil refineries drive substantial demand. Local manufacturers like Riken Keiki compete with global brands through cost-effective solutions, though quality concerns persist in price-sensitive markets. Japan’s technological leadership in sensor development complements Southeast Asia’s increasing focus on workplace safety standards. The region’s dominance in manufacturing ensures sustained demand, particularly for wall-mounted detectors in factory environments.

Europe

Europe maintains a strong position with its emphasis on industrial safety and environmental protection. The ATEX directive governs explosive atmosphere equipment standards, creating steady demand for certified addressable detectors. Germany and the UK lead adoption in chemical and pharmaceutical sectors, while Nordic countries prioritize innovative wireless solutions. The region shows increasing preference for multi-gas detectors with cloud connectivity, though slower industrial growth compared to Asia tempers market expansion. Recent EU initiatives on hydrogen energy infrastructure present new opportunities for specialized gas detection systems.

Middle East & Africa

The Middle East’s thriving oil & gas industry sustains demand for robust gas detection solutions, particularly in Saudi Arabia and the UAE. Addressable systems gain traction in large refinery complexes for centralized monitoring. Africa shows nascent growth, with South Africa leading adoption in mining operations. While underdeveloped industrial safety regulations limit market potential, increasing foreign investments in energy projects and gradual infrastructure development signal long-term opportunities. High-temperature resistant detectors see particular demand in the region’s harsh operating environments.

South America

South America’s market progresses steadily, with Brazil and Argentina as key consumers in their growing oil and mining sectors. Economic volatility and currency fluctuations impact capital investments in safety equipment, favoring mid-range solutions over premium products. Local manufacturers compete through affordable alternatives, though reliability concerns persist. Recent offshore oil discoveries and expanding LNG facilities present growth avenues. The region shows gradual shift from basic detectors to addressable systems as industrial automation increases.

Report Scope

This market research report provides a comprehensive analysis of the global Addressable Gas Detector market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Addressable Gas Detector market was valued at USD 857 million in 2024 and is projected to reach USD 1,192 million by 2032, growing at a CAGR of 4.9%.

- Segmentation Analysis: Detailed breakdown by product type (Wall Mounted, Hand Held, Others), application (Oil & Gas, Mining, Manufacturing, Food & Beverage), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants including Honeywell, Drager, MSA, Riken Keiki, and Industrial Scientific, covering their product portfolios, R&D focus, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies including IoT integration, AI-powered detection systems, and wireless connectivity in gas detection solutions.

- Market Drivers & Restraints: Evaluation of factors such as stringent safety regulations, industrial automation trends, and high installation costs impacting market growth.

- Stakeholder Analysis: Strategic insights for gas detector manufacturers, system integrators, industrial end-users, and regulatory bodies regarding market opportunities.

The report employs both primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Addressable Gas Detector Market?

-> Addressable Gas Detector Market was valued at 857 million in 2024 and is projected to reach US$ 1192 million by 2032, at a CAGR of 4.9% during the forecast period.

Which key companies operate in Global Addressable Gas Detector Market?

-> Key players include Honeywell, Drager, MSA, Riken Keiki, Industrial Scientific, 3M, and Johnson Controls, among others.

What are the key growth drivers?

-> Key growth drivers include increasing industrial safety regulations, growing adoption in oil & gas sector, and technological advancements in gas detection systems.

Which region dominates the market?

-> North America holds significant market share, while Asia-Pacific is expected to witness the fastest growth during the forecast period.

What are the emerging trends?

-> Emerging trends include integration of wireless technologies, development of multi-gas detectors, and increasing adoption of smart industrial safety solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...