MARKET INSIGHTS

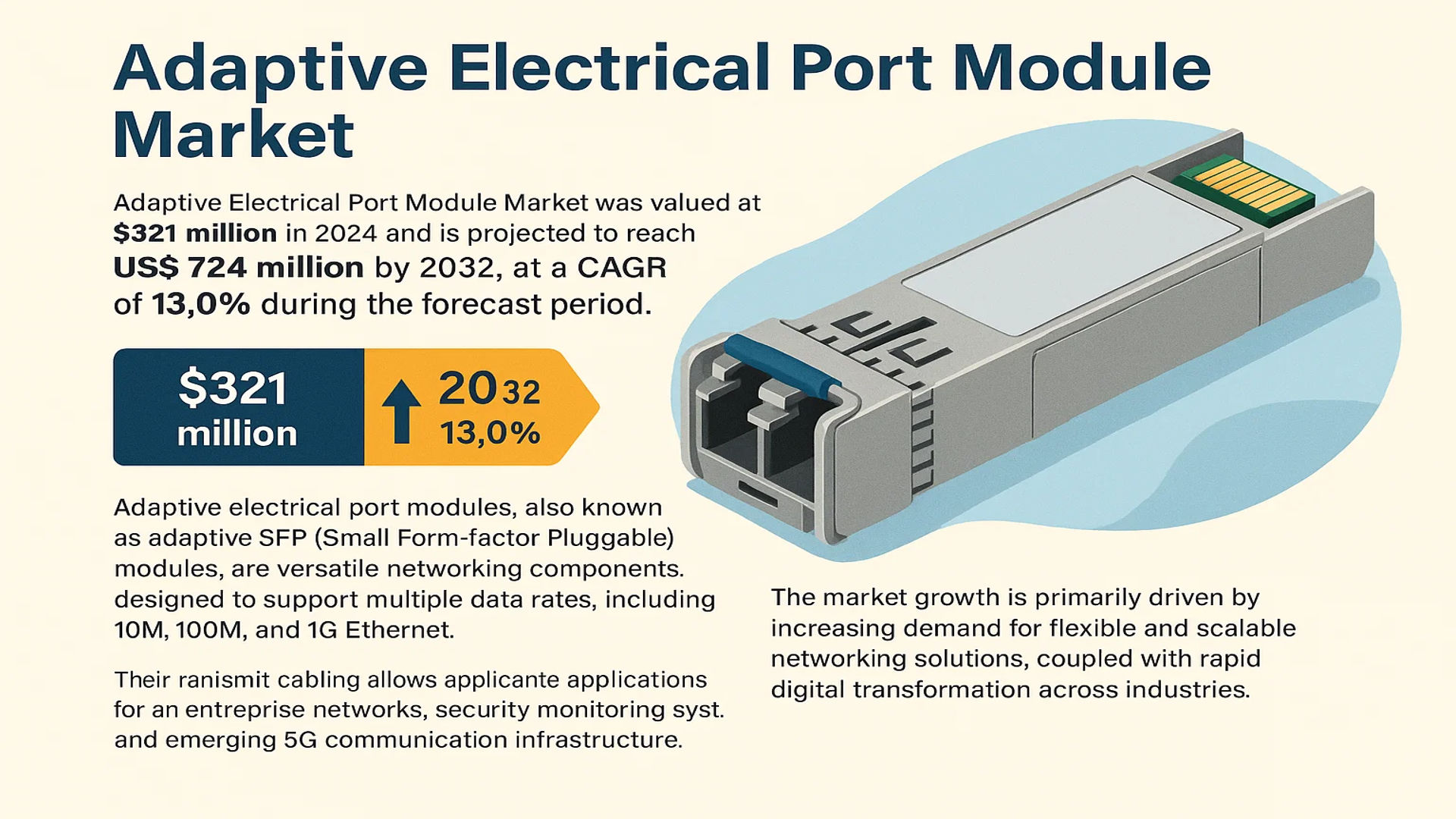

The global Adaptive Electrical Port Module Market was valued at 321 million in 2024 and is projected to reach US$ 724 million by 2032, at a CAGR of 13.0% during the forecast period.

Adaptive electrical port modules, also known as adaptive SFP (Small Form-factor Pluggable) modules, are versatile networking components designed to support multiple data rates, including 10M, 100M, and 1G Ethernet. These modules enable seamless connectivity across diverse network environments, from basic home networks to high-performance data centers. Their compatibility with twisted-pair cabling allows transmission distances of up to 100 meters, making them ideal for applications in enterprise networks, security monitoring systems, and emerging 5G communication infrastructure.

The market growth is primarily driven by increasing demand for flexible and scalable networking solutions, coupled with rapid digital transformation across industries. While North America currently dominates the market due to early technology adoption, Asia-Pacific is expected to witness the highest growth rate because of expanding IT infrastructure investments. Key players such as Cisco, Hewlett Packard Enterprise, and Huawei are actively innovating to capture market share through advanced multi-rate compatibility features and improved power efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Speed Network Connectivity to Propel Market Expansion

The exponential growth in data traffic, driven by cloud computing, IoT proliferation, and 5G adoption, is creating unprecedented demand for high-speed network infrastructure. Adaptive electrical port modules have become critical enablers in this landscape, providing the flexibility to support multiple data rates (10M/100M/1000BASE) while maintaining backward compatibility with existing infrastructure. The global IP traffic is projected to grow at a compound annual rate exceeding 25%, with enterprise data centers accounting for nearly 30% of this demand. This surge directly correlates with increased adoption of adaptive SFP modules that can dynamically adjust to varying bandwidth requirements without requiring hardware changes.

Data Center Modernization Initiatives Accelerating Deployment

Major hyperscalers and colocation providers are actively replacing legacy infrastructure with adaptive port solutions to optimize operational efficiency. The transition from fixed-rate ports to adaptive modules allows data centers to achieve 40-50% better port utilization while reducing capital expenditures. Telecommunications operators are similarly adopting these modules to future-proof their access networks, particularly as the global installed base of 10G-capable devices surpassed 200 million units in 2024. Recent product innovations, such as Cisco’s programmable SFP-E modules supporting auto-negotiation between 1G and 10G speeds, demonstrate how manufacturers are addressing evolving market needs.

Enterprise Digital Transformation Fueling SME Adoption

Small and medium enterprises undergoing digital transformation represent a growing market segment, with adoption rates increasing by approximately 18% year-over-year. The plug-and-play nature of adaptive electrical port modules eliminates the need for specialized IT expertise during deployment, making them particularly attractive for resource-constrained organizations. Furthermore, the modules’ 100-meter transmission capability over standard twisted-pair wiring provides cost-effective solutions for office network upgrades without requiring cable plant modifications. As hybrid work models become permanent, enterprises are prioritizing network flexibility – a key value proposition driving the modules’ 35% share in the corporate LAN segment.

MARKET RESTRAINTS

Higher Initial Costs Compared to Fixed-Rate Modules Constrain Price-Sensitive Markets

While offering superior flexibility, adaptive electrical port modules typically carry a 20-30% price premium over their fixed-rate counterparts. This cost differential presents a significant adoption barrier in developing regions and budget-conscious verticals, where network infrastructure investments are closely scrutinized. Manufacturing complexities associated with supporting multiple protocols and auto-negotiation capabilities contribute to the higher bill of materials, with active electronic components accounting for nearly 60% of total production costs. The pricing pressure is particularly acute in the SME segment, where procurement decisions frequently prioritize immediate cost savings over long-term operational benefits.

Interoperability Challenges with Legacy Infrastructure

Despite standards compliance claims, field deployments reveal persistent interoperability issues between adaptive modules and older network equipment. Approximately 15% of installations require manual configuration overrides or firmware updates to establish stable link negotiation, increasing deployment complexity and support costs. The situation is exacerbated in multi-vendor environments, where subtle implementation differences in auto-negotiation protocols can disrupt service provisioning. Network administrators frequently report higher mean-time-to-repair incidents involving adaptive modules compared to fixed-rate alternatives, creating hesitancy among risk-averse enterprises.

MARKET OPPORTUNITIES

Edge Computing Deployments Creating New Growth Vectors

The rapid expansion of edge computing infrastructure presents a substantial opportunity, with projections indicating 75% of enterprise data will be processed at the edge by 2030. Adaptive electrical port modules are uniquely positioned to serve these decentralized deployments, offering the dual advantages of high-density connectivity and future-proof scalability. Manufacturers are developing ruggedized variants capable of operating in harsh industrial environments while maintaining the full range of speed adaptation capabilities. Recent trials in smart factory applications have demonstrated 40% reductions in cabling complexity when using adaptive modules for machine-to-machine communication networks.

5G Backhaul Modernization Projects Driving Carrier Investments

Telecommunication providers are allocating significant portions of their 5G capital expenditures to backhaul network upgrades, with adaptive port modules emerging as preferred solutions for flexible capacity provisioning. The ability to seamlessly transition between 1G and 10G connections allows operators to optimize backhaul economics while accommodating unpredictable traffic growth patterns. Several tier-1 carriers have standardized on adaptive modules for their small cell deployments, recognizing the technology’s ability to reduce spare part inventories and simplify field operations. This trend is expected to accelerate as 5G densification requirements intensify, potentially creating a $120 million annual opportunity by 2027.

MARKET CHALLENGES

Thermal Management Complications in High-Density Installations

The increased power requirements of adaptive electrical port modules, typically 15-20% higher than fixed-rate equivalents, create thermal challenges in high-density switching environments. Data center operators report that adaptive modules contribute disproportionately to hot-spot formation in fully populated chassis, sometimes requiring under-provisioning of ports to maintain acceptable operating temperatures. These thermal constraints become particularly problematic in edge computing deployments where cooling infrastructure may be limited. Manufacturers are responding with improved heatsink designs and dynamic power adjustment features, but the fundamental physics limitations continue to challenge form factor miniaturization trends.

Fiber Optic Alternatives Eroding Cost-Performance Advantage

The declining costs of optical transceivers, particularly in the 10G segment, are reducing the economic advantage of copper-based adaptive modules in medium-range applications. While twisted-pair solutions maintain dominance in last-mile deployments, fiber alternatives now offer competitive total-cost-of-ownership for runs exceeding 30 meters in enterprise environments. The situation is compounded by technical limitations – adaptive electrical modules cannot support emerging 25G/40G standards, forcing organizations to consider fiber for future upgrade paths. This competitive pressure has intensified pricing wars in the 1G/10G segment, squeezing manufacturer margins despite growing unit volumes.

ADAPTIVE ELECTRICAL PORT MODULE MARKET TRENDS

Increasing Data Center Investments Drive Market Growth

The global adaptive electrical port module market is witnessing robust growth due to the rapid expansion of data centers worldwide. With enterprises increasingly adopting cloud computing and hyperscale infrastructure, the demand for efficient networking solutions like adaptive electrical port modules has surged. These modules offer multi-rate support (10/100/1000BASE) and extend transmission distances up to 100 meters, making them ideal for high-density data center environments. In 2024, investments in data center infrastructure exceeded $250 billion globally, further accelerating market adoption. Additionally, the rising popularity of edge computing has created new opportunities for adaptive modules in distributed network architectures.

Other Trends

5G Network Deployments Fuel Demand

The ongoing rollout of 5G networks across major economies is significantly boosting the adaptive electrical port module market. As telecom operators upgrade their backhaul and fronthaul networks to support higher bandwidth requirements, these modules provide the necessary flexibility for multi-gigabit connectivity. Countries leading 5G adoption, such as the U.S., China, and South Korea, are seeing particularly strong demand. With over 1.5 billion 5G subscriptions projected by 2025, network equipment manufacturers are increasingly incorporating adaptive port modules into their switching and routing solutions.

Enterprise Network Modernization Initiatives

Modernizing legacy enterprise networks represents another key driver for adaptive electrical port module adoption. Businesses across sectors are upgrading their networking infrastructure to support digital transformation initiatives, with particular emphasis on SMEs implementing cost-effective yet future-proof solutions. The ability of these modules to operate across three different Ethernet speeds (100M, 1G, and 10G) makes them highly versatile for evolving network requirements. This flexibility has proven particularly valuable in hybrid work environments where network loads fluctuate significantly throughout the day. Recent surveys indicate that over 60% of enterprises plan to upgrade their network hardware within the next two years.

COMPETITIVE LANDSCAPE

Key Industry Players

Network Giants Drive Innovation in Adaptive Electrical Port Module Market

The global adaptive electrical port module market features a dynamic competitive landscape, characterized by strong penetration from established networking equipment providers alongside aggressive growth from specialized manufacturers. Cisco Systems leads the market with an estimated 22% revenue share in 2024, leveraging its comprehensive portfolio of adaptive SFP modules and deep integration capabilities across enterprise and data center environments.

While Hewlett Packard Enterprise (HPE) and Juniper Networks maintain significant shares through their advanced networking solutions, Chinese manufacturers like Huawei and ZTE are gaining traction in APAC markets. This regional growth is propelled by increasing 5G deployments and smart infrastructure investments across China and Southeast Asia.

The market sees continuous innovation as players introduce modules supporting higher data rates and improved power efficiency. Recent developments include Intel’s launch of energy-optimized adaptive modules for edge computing applications, while startups like Ruijie Networks are carving niches in SME network segments with cost-competitive solutions.

Strategic partnerships between component manufacturers and end-users are reshaping the competitive dynamics. For instance, Finisar’s collaboration with major cloud service providers has significantly strengthened its position in the data center segment, which accounted for 38% of total module deployments last year.

List of Key Adaptive Electrical Port Module Manufacturers

- Cisco Systems, Inc. (U.S.)

- Hewlett Packard Enterprise (U.S.)

- Juniper Networks (U.S.)

- Huawei Technologies Co., Ltd. (China)

- H3C Technologies (China)

- ZTE Corporation (China)

- NETGEAR (U.S.)

- Ruijie Networks (China)

- Intel Corporation (U.S.)

- Pulian International (Taiwan)

Segment Analysis:

By Type

SDR SDRAM Dominates the Market Due to High Compatibility with Multiple Network Configurations

The market is segmented based on type into:

- SDR SDRAM

- Subtypes: PC100, PC133, and others

- DDR SDRAM

- Subtypes: DDR1, DDR2, DDR3, and others

- Others

By Application

Data Center Segment Leads Due to Increasing Demand for High-Speed Network Solutions

The market is segmented based on application into:

- Data Center

- SMEs Network

- Security Monitoring

- 5G Communication

By Transmission Rate

10G Ethernet Segment Holds Strong Position to Support Next-Gen Network Demands

The market is segmented based on transmission rate into:

- 100M Ethernet

- 1G Ethernet

- 10G Ethernet

Regional Analysis: Adaptive Electrical Port Module Market

Asia-Pacific

The Asia-Pacific region dominates the Adaptive Electrical Port Module market, accounting for over 40% of global demand in 2024. This leadership position stems from rapid digital transformation across China, Japan, and India, coupled with massive investments in 5G infrastructure. China’s “Digital China 2025” initiative has accelerated deployment in data centers and telecommunications, creating strong demand for high-speed adaptive modules. While cost sensitivity remains a factor, the region shows increasing preference for DDR SDRAM modules due to their performance advantages. Local manufacturers like Huawei, ZTE, and Ruijie compete effectively with global players through aggressive pricing and domestic supply chain advantages.

North America

North America represents the second-largest market, characterized by technological sophistication and early adoption of advanced networking solutions. The U.S. leads in data center deployments, with hyperscale operators driving demand for 10G-capable adaptive modules. Recent FCC policies promoting broadband expansion are further stimulating market growth. Enterprise network upgrades and increasing investment in IoT infrastructure contribute to steady demand. Major players like Cisco and Juniper Networks maintain strong positions through continuous product innovation and partnerships with cloud service providers. The region shows particular strength in application segments like 5G communication and security monitoring systems.

Europe

Europe’s market growth is propelled by stringent data regulations and emphasis on network security, particularly in Germany and the U.K. The region shows strong uptake in enterprise and SME network applications, with growing demand for modules supporting Power over Ethernet (PoE) capabilities. EU cybersecurity certification requirements have influenced product development, with manufacturers introducing more secure authentication features in their modules. While market growth is steadier than Asia-Pacific, Western European nations demonstrate higher willingness to pay for premium, reliability-tested products. The upcoming wave of industrial IoT deployments is expected to create new opportunities across manufacturing hubs.

South America

South America presents emerging opportunities, particularly in Brazil’s growing data center market and Argentina’s telecom sector. Market adoption faces challenges including import dependency and currency volatility, which affect pricing stability. However, increasing mobile broadband penetration and government digitalization programs are driving demand in the SME network segment. Local players face intense competition from Chinese manufacturers offering cost-competitive solutions. The market shows preference for basic SDR SDRAM modules due to budget constraints, though this is gradually shifting as network requirements become more sophisticated.

Middle East & Africa

This region exhibits the fastest growth rate (projected CAGR of 15.2% 2024-2032), albeit from a smaller base. Gulf nations like UAE and Saudi Arabia lead in smart city deployments, requiring advanced adaptive modules for their infrastructure. Africa’s growth is constrained by limited last-mile connectivity but shows promise in mobile money and banking applications. The market remains price-sensitive, with Chinese brands dominating the entry-level segment. Significant potential exists in security monitoring applications as governments invest in surveillance infrastructure, though political and economic instability in some areas creates uneven growth patterns across the region.

Report Scope

This market research report provides a comprehensive analysis of the Global Adaptive Electrical Port Module market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 321 million in 2024 and is projected to reach USD 724 million by 2032, growing at a CAGR of 13.0%.

- Segmentation Analysis: Detailed breakdown by product type (SDR SDRAM, DDR SDRAM) and application (Data Center, SMEs Network, Security Monitoring, 5G Communication) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including Cisco, Hewlett Packard Enterprise, Juniper Networks, Huawei, and H3C, covering their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in adaptive SFP modules, integration with 5G networks, and evolving industry standards for multi-rate support.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing data center deployments and 5G infrastructure development, along with challenges like supply chain constraints.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving network infrastructure ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Adaptive Electrical Port Module Market?

->Adaptive Electrical Port Module Market was valued at 321 million in 2024 and is projected to reach US$ 724 million by 2032, at a CAGR of 13.0% during the forecast period.

Which key companies operate in Global Adaptive Electrical Port Module Market?

-> Key players include Cisco, Hewlett Packard Enterprise, Juniper Networks, Huawei, H3C, Netgear, ZTE, and Intel, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-speed network connectivity, data center expansion, and 5G network deployments.

Which region dominates the market?

-> Asia-Pacific shows the highest growth potential, while North America currently leads in market share.

What are the emerging trends?

-> Emerging trends include multi-rate adaptive modules, energy-efficient designs, and integration with AI-powered network management systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...