MARKET INSIGHTS

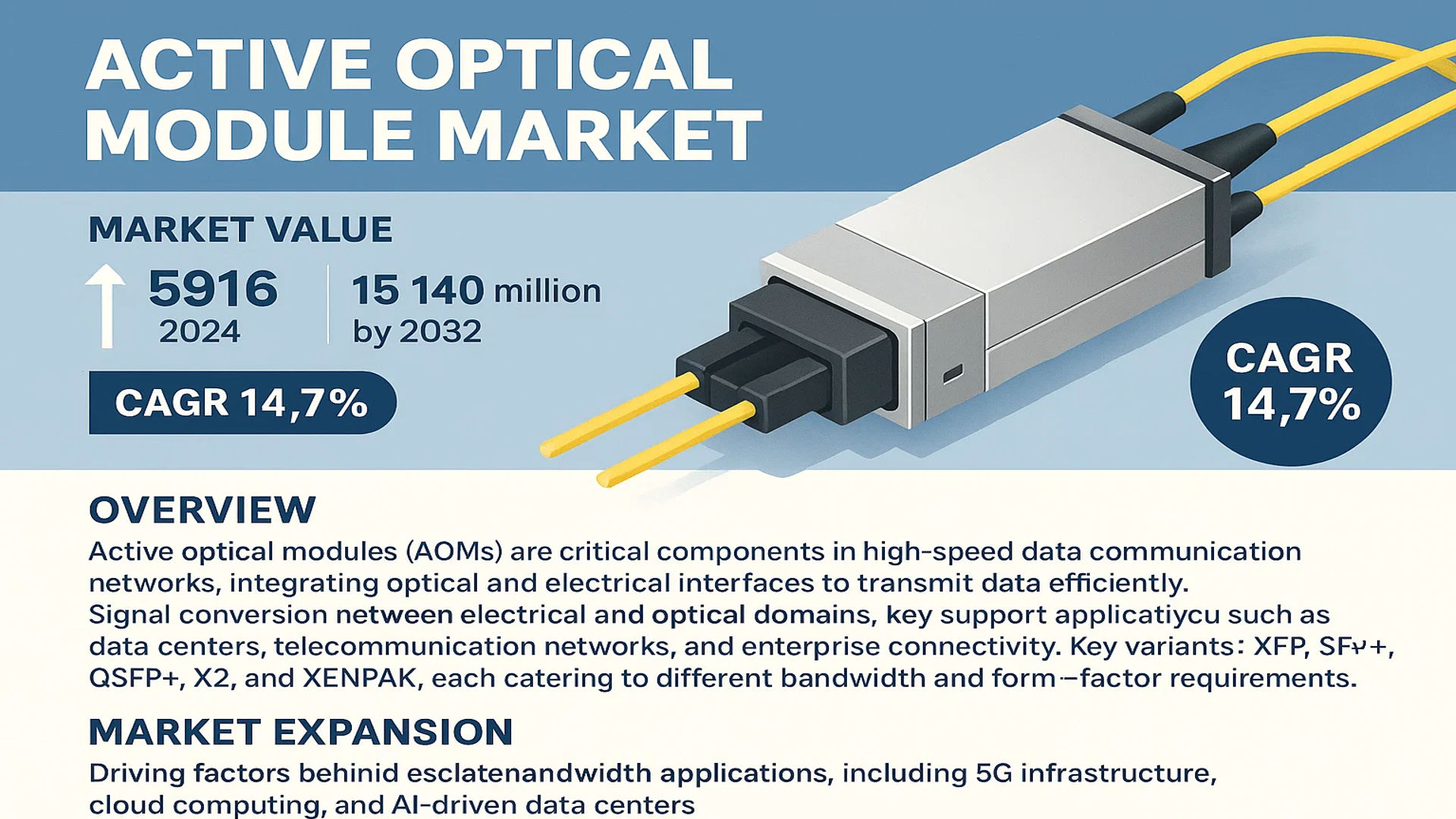

The global Active Optical Module Market was valued at 5916 million in 2024 and is projected to reach US$ 15140 million by 2032, at a CAGR of 14.7% during the forecast period.

Active optical modules (AOMs) are critical components in high-speed data communication networks, integrating optical and electrical interfaces to transmit data efficiently. These modules facilitate signal conversion between electrical and optical domains, supporting applications such as data centers, telecommunication networks, and enterprise connectivity. Key variants include XFP, SFP+, QSFP+, X2, and XENPAK, each catering to different bandwidth and form factor requirements.

The market expansion is driven by escalating demand for high-bandwidth applications, including 5G infrastructure, cloud computing, and AI-driven data centers. However, challenges such as high manufacturing costs and technical complexities in thermal management persist. Leading players like Hisilicon, Amphenol, and Eoptolink dominate the competitive landscape, with the top five companies holding a significant revenue share in 2024. Recent advancements in silicon photonics and coherent optics are further propelling innovation, ensuring long-term market sustainability.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth in Data Center Deployments to Drive Active Optical Module Demand

The staggering expansion of hyperscale data centers globally is creating unprecedented demand for high-speed optical connectivity solutions. With data traffic projected to grow at a compound annual rate of over 25% through 2030, data center operators are increasingly adopting active optical modules (AOMs) to support 400G and 800G Ethernet standards. These modules enable higher bandwidth density while reducing power consumption – a critical factor as energy costs continue rising. Recent technological breakthroughs in silicon photonics have further enhanced AOM performance, making them indispensable for modern data center architectures.

5G Network Rollouts Accelerating Adoption of High-Speed Optical Solutions

The global transition to 5G networks represents a fundamental driver for the AOM market, requiring substantial upgrades to fronthaul and backhaul infrastructure. Mobile operators worldwide are investing heavily in fiber-based solutions to support the low-latency, high-bandwidth requirements of 5G services. Active optical modules play a pivotal role in these deployments, with the front-haul segment alone expected to account for over 30% of total market demand by 2026. The integration of AOMs in small cell deployments and centralized radio access networks (C-RAN) is proving particularly transformative for mobile network architectures.

Furthermore, government initiatives accelerating digital infrastructure development are providing additional momentum:

➤ Multiple national broadband plans now mandate fiber-optic backbones, creating sustained demand for high-performance optical modules in telecommunications applications.

The combination of private sector investment and public infrastructure programs is creating a robust growth environment for AOM manufacturers across both developed and emerging markets.

Emergence of AI and Machine Learning Workloads Fueling Advanced Optical Needs

Artificial intelligence and machine learning applications are driving revolutionary changes in data center architectures, particularly in interconnect requirements between GPUs and accelerators. The bandwidth demands of AI clusters – often requiring petabits per second of internal connectivity – are pushing AOM technology to new performance thresholds. Leading cloud providers are now deploying optical modules capable of 1.6Tbps speeds to support distributed AI training workloads, creating a premium segment within the market. This trend is expected to intensify as AI model complexity continues growing exponentially, with neural networks doubling in size approximately every 3-6 months.

MARKET RESTRAINTS

Supply Chain Vulnerabilities and Component Shortages Constraining Market Growth

The active optical module industry faces significant challenges from ongoing supply chain disruptions, particularly for critical photonic components. The concentrated nature of semiconductor manufacturing has created bottlenecks, with lead times for certain optoelectronic chips extending beyond 52 weeks in some cases. These constraints are exacerbated by the complex multi-country supply chains typical in AOM production, where a single module might incorporate components from a dozen different specialized suppliers. While capacity expansions are underway, the capital-intensive nature of photonics fabrication means supply-demand imbalances may persist through 2025.

High Development Costs Creating Barriers for Market Entrants

The significant R&D expenditures required for next-generation AOM development present another key market restraint. Designing optical modules for 800G and beyond often requires investments exceeding $50 million per product family, creating substantial barriers for smaller players. Additionally, the rapid pace of technology obsolescence in this sector means manufacturers must continually reinvest in new designs to remain competitive. This dynamic favors established players with deep financial resources, potentially limiting innovation from emerging competitors and consolidating market share among a handful of dominant suppliers.

The combination of technical complexity and financial requirements has created a challenging environment:

➤ Recent industry analysis suggests development cycles for new AOM products have extended by 30-40% compared to pre-pandemic timelines due to increased design complexity and testing requirements.

These factors are slowing the overall pace of innovation while increasing the cost structure across the value chain.

MARKET CHALLENGES

Power Consumption and Thermal Management Issues in High-Density Deployments

As data rates continue climbing to 800G and 1.6T, active optical modules face escalating thermal management challenges. Power densities in modern switch racks now exceed 40kW in many deployments, with optical modules contributing significantly to the thermal load. This creates difficult engineering tradeoffs between performance, power efficiency, and reliability – particularly in hyperscale environments where equipment operates continuously at peak capacity. Module manufacturers are investing heavily in advanced cooling solutions and lower-power designs, but fundamental physics limitations make this an ongoing battle as speeds increase.

Additional Technical Challenges

Signal Integrity at Higher Frequencies

Maintaining signal integrity becomes increasingly difficult as data rates push into terabit territories, requiring more sophisticated DSP techniques and higher-quality optical components. This adds both cost and complexity to module designs.

Interoperability Concerns

The proliferation of proprietary implementations among different switch vendors creates interoperability challenges, forcing module makers to maintain multiple product variants and increasing inventory complexity.

MARKET OPPORTUNITIES

Co-Packaged Optics Emergence Creating New Product Development Pathways

The transition toward co-packaged optics (CPO) architectures represents one of the most significant opportunities in the optical components market. By integrating optical engines directly with switch ASICs, CPO solutions promise substantial power savings and density improvements for next-generation data centers. Early implementations suggest potential power reductions of 30-50% compared to discrete pluggable modules, making this technology particularly attractive for sustainability-focused cloud operators. While technical hurdles remain, lead customers are already working closely with suppliers on pilot deployments, with commercial availability expected to ramp significantly after 2025.

Edge Computing Expansion Driving Demand for Ruggedized Optical Solutions

The rapid growth of edge computing infrastructure is creating new opportunities for specialized AOM products designed for harsh environments. Unlike temperature-controlled data centers, edge locations often confront wide thermal variations, vibration, and limited maintenance access – demanding more robust optical solutions. Module suppliers developing products specifically for these challenging deployments can command premium pricing while establishing early positions in a market segment projected to grow at nearly 30% annually through 2030. This includes applications in industrial settings, telecom edge nodes, and outdoor wireless infrastructure.

Technological convergence is creating additional avenues for innovation:

➤ Emerging silicon photonics platforms are enabling new levels of integration between optical and electronic components, potentially revolutionizing module form factors and performance characteristics in coming years.

Companies successfully navigating these transitions will be well-positioned to capitalize on the next phase of optical networking evolution.

ACTIVE OPTICAL MODULE MARKET TRENDS

5G Network Expansion Driving Demand for High-Speed Optical Modules

The global rollout of 5G networks is significantly increasing the adoption of active optical modules (AOMs) due to their ability to handle high-speed data transmission with low latency. These modules play a crucial role in enabling fiber-optic communication infrastructures that support 5G backhaul and fronthaul networks. With major telecom operators investing heavily in next-generation network deployments, the market for AOMs is expected to grow at a CAGR of 14.7%, reaching $15.14 billion by 2032. The RF-over-fiber (RFoF) technology used in 5G small cells further amplifies the demand for advanced AOMs capable of supporting ultra-high frequencies.

Other Trends

Data Center Modernization

Increasing data traffic from cloud computing and AI workloads is compelling data center operators to upgrade their infrastructure with high-capacity AOMs. The shift toward 400G and 800G optical transceivers is accelerating, with hyperscale data centers being early adopters. In 2024, the QSFP+ and SFP+ segments collectively accounted for over 60% of the market share, while emerging demand for co-packaged optics (CPO) technology is reshaping future deployment strategies. This transition is driven by the need for energy-efficient solutions that reduce power consumption per bit of data transmitted.

Technological Advancements in Optical Networking

Innovations in silicon photonics and pluggable optics are enabling manufacturers to develop compact, high-performance AOMs at competitive price points. Recent breakthroughs include 800G DR8 modules that support terabit-scale connectivity while maintaining backward compatibility with existing infrastructure. Leading players like Hilink Technology and Amphenol are investing heavily in R&D to improve thermal management and signal integrity. These advancements are particularly crucial for emerging applications in edge computing and AI-driven network optimization, where low-latency data transfer is paramount. However, supply chain challenges for semiconductor components continue to pose constraints on production scalability.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Forge Ahead with Innovations to Secure Market Dominance

The global active optical module market exhibits a semi-consolidated competitive structure, with a mix of established multinational corporations and emerging regional players vying for market share. Daiichiseiko and Hisense Broadband currently lead the market, owing to their comprehensive product portfolios spanning multiple form factors including XFP, SFP+, and QSFP+ modules. These companies benefit from vertical integration capabilities and strong distribution networks across key regions.

Silicon Line and Accelink have emerged as significant challengers, particularly in the Asia-Pacific region where demand for high-speed data transmission continues to surge. Their competitive advantage stems from cost-effective production capabilities and rapid adoption of emerging technologies like 400G optical modules.

The market has witnessed increased strategic movements in 2024, with key players focusing on R&D investments to develop energy-efficient modules and improved thermal management solutions. This technological arms race is particularly evident in data center applications, where power consumption remains a critical concern for operators.

Meanwhile, Amphenol and Eoptolink are expanding their market presence through strategic collaborations with network equipment manufacturers. Their approach combines technical expertise with scalable manufacturing, allowing them to cater to both hyperscale data center operators and telecommunications service providers.

List of Key Active Optical Module Manufacturers

- Daiichiseiko (Japan)

- Silicon Line (Germany)

- Hisilicon (China)

- Hisense Broadband (China)

- Accelink Technologies Co., Ltd. (China)

- Eoptolink Technology Inc. (China)

- Amphenol Corporation (U.S.)

- Hilink Technology (China)

- Gearlink (China)

- T&S Communication (China)

- GrenTech (China)

The industry’s competitive intensity continues to rise as companies pursue technological differentiation through advanced modulation techniques and improved signal integrity. While Chinese manufacturers dominate volume production, their American and European counterparts maintain leadership in specialized high-performance modules for mission-critical applications.

Active Optical Module Market

By Type

QSFP+ Segment Leads Due to High-Density Data Transmission in Data Centers

The market is segmented based on type into:

- XFP

- SFP+

- QSFP+

- X2

- XENPAK

- Others

By Application

Optical Fiber Communication Dominates Due to Rising Demand for High-Speed Network Infrastructure

The market is segmented based on application into:

- Optical Fiber Communication

- Bandwidth

- Others

By End-User

Telecommunications Sector Accounts for Major Share Due to 5G Deployment Requirements

The market is segmented based on end-user into:

- Telecommunications

- Data Centers

- Enterprise Networks

- Consumer Electronics

By Technology

Wavelength Division Multiplexing Gains Traction for Enhanced Bandwidth Utilization

The market is segmented based on technology into:

- Wavelength Division Multiplexing (WDM)

- Coherent Optical Communication

- Short-Reach Communication

Regional Analysis: Active Optical Module Market

Asia-Pacific

The Asia-Pacific region dominates the Active Optical Module market, driven by massive demand from China, Japan, and India. China, in particular, is the largest consumer and producer, with its telecommunications and data center sectors expanding rapidly due to government-led initiatives like “Digital China” and 5G network deployments. The region benefits from a robust supply chain ecosystem, including key players such as Hisilicon and Accelink, which contribute significantly to global production. While cost competitiveness remains a key advantage, the push for higher-speed modules, such as QSFP+ and SFP+, is accelerating market growth. Rising data traffic from urbanization and digital transformation initiatives further fuels adoption.

North America

North America is a high-growth market, propelled by the United States’ advanced IT infrastructure and data center investments. The demand for high-speed optical modules, particularly in hyperscale data centers and cloud computing, is surging. Innovations in fiber-optic communication standards and increasing bandwidth requirements from enterprises contribute to market expansion. Leading companies like Amphenol and Silicon Line are actively developing energy-efficient and compact AOM solutions to meet regulatory and environmental standards. Despite strong demand, supply chain constraints and fluctuating component costs present challenges.

Europe

Europe’s market is characterized by stringent quality norms and a focus on sustainable, high-performance optical modules. Countries like Germany and the U.K. lead in fiber-optic adoption, backed by government funding for broadband expansion and smart city projects. The EU’s emphasis on reducing carbon footprints encourages manufacturers to develop low-power consumption modules. However, dependency on imports for critical components and slower infrastructure upgrades compared to Asia-Pacific limit faster market penetration. Companies are investing in R&D to enhance compatibility with next-gen network architectures.

South America

The market in South America is at a nascent stage but holds potential due to gradual digitalization efforts, particularly in Brazil and Argentina. Telecom operators are upgrading networks to support increasing internet penetration, which drives demand for cost-effective optical modules. However, economic instability and limited local manufacturing result in reliance on imports, affecting pricing and delivery timelines. While the market is still emerging, investments in data centers and broadband projects signal long-term opportunities.

Middle East & Africa

The Middle East & Africa region shows steady growth, with countries like Saudi Arabia and the UAE investing in smart infrastructure and 5G rollouts. Data localization policies and expanding IT hubs in Dubai and Riyadh are boosting demand for high-speed optical modules. However, infrastructure limitations in many African nations hinder widespread adoption. Market development is also constrained by funding gaps and a lack of local expertise, though partnerships with global suppliers are gradually addressing these challenges.

Report Scope

This market research report provides a comprehensive analysis of the global Active Optical Module market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Active Optical Module market was valued at USD 5,916 million in 2024 and is projected to reach USD 15,140 million by 2032, growing at a CAGR of 14.7%.

- Segmentation Analysis: Detailed breakdown by product type (XFP, SFP+, QSFP+, X2, XENPAK, Others), application (Optical Fiber Communication, Bandwidth, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for key markets including the U.S., China, Japan, Germany, and others.

- Competitive Landscape: Profiles of leading market participants including Daiichiseiko, Silicon Line, Hisilicon, Hisense Broadband, Accelink, Eoptolink, Amphenol, and others, covering their market share, product portfolios, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging optical communication technologies, integration with 5G networks, and advancements in high-speed data transmission modules.

- Market Drivers & Restraints: Evaluation of factors including growing data center demand, 5G network deployment, and bandwidth requirements versus supply chain constraints and high development costs.

- Stakeholder Analysis: Strategic insights for component manufacturers, telecom operators, data center operators, and investors regarding market opportunities and challenges.

The research methodology combines primary interviews with industry experts and analysis of verified market data from multiple authoritative sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Active Optical Module Market?

-> Active Optical Module Market was valued at 5916 million in 2024 and is projected to reach US$ 15140 million by 2032, at a CAGR of 14.7% during the forecast period.

Which key companies operate in Global Active Optical Module Market?

-> Key players include Daiichiseiko, Silicon Line, Hisilicon, Hisense Broadband, Accelink, Eoptolink, Amphenol, Hilink Technology, Gearlink, and T&S Communication.

What are the key growth drivers?

-> Key growth drivers include rising data center investments, 5G network expansion, increasing bandwidth requirements, and cloud computing adoption.

Which region dominates the market?

-> Asia-Pacific dominates the market, driven by China’s rapid telecom infrastructure development, while North America remains a significant market due to advanced data center infrastructure.

What are the emerging trends?

-> Emerging trends include development of 800G modules, silicon photonics integration, and demand for energy-efficient optical solutions in data centers and telecom networks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...