MARKET INSIGHTS

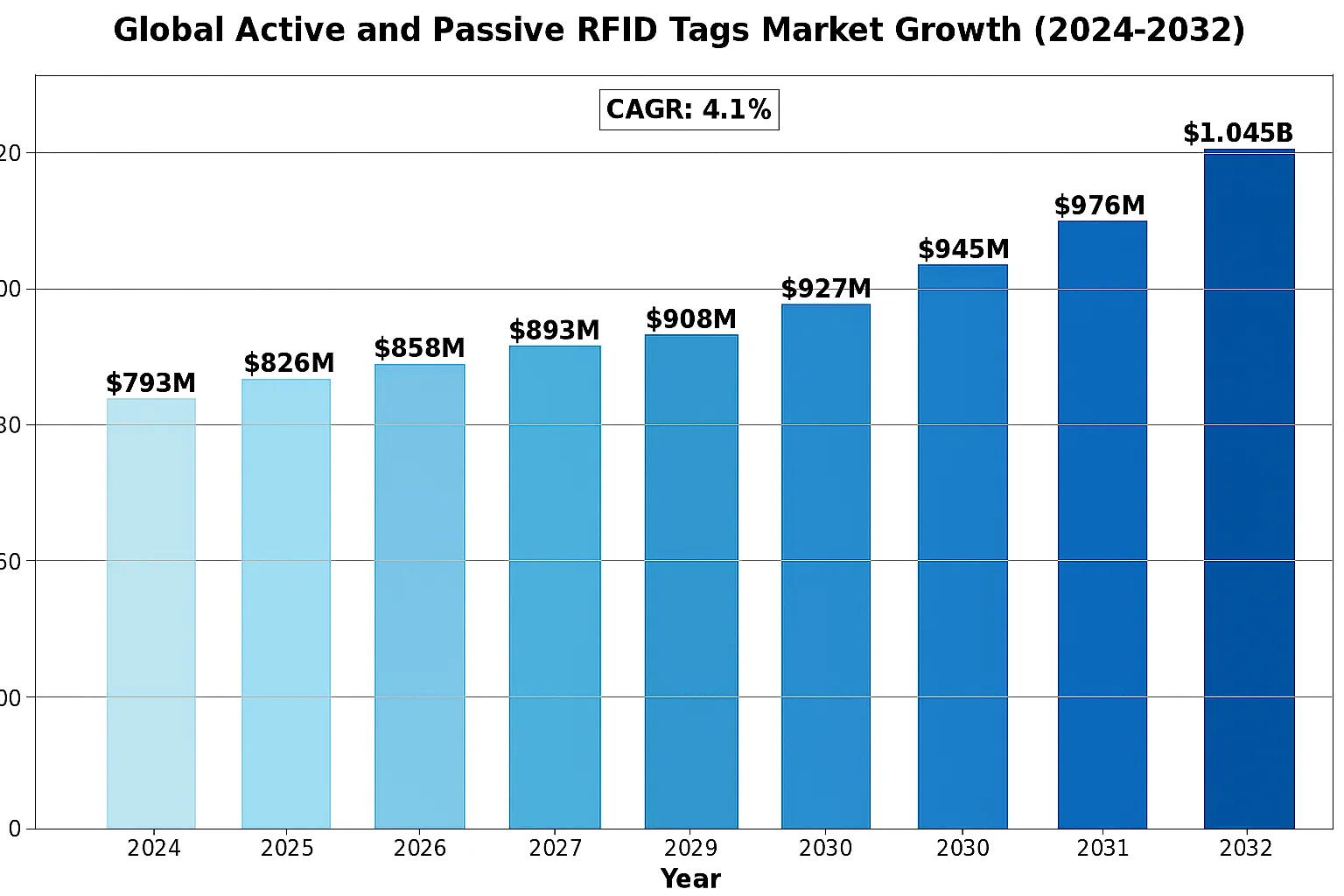

The global Active and Passive RFID Tags Market was valued at 793 million in 2024 and is projected to reach US$ 1045 million by 2032, at a CAGR of 4.1% during the forecast period.

Active and passive RFID tags are key components in radio frequency identification systems. Active RFID tags are battery-powered devices that continuously transmit signals, enabling real-time tracking with extended read ranges – ideal for logistics and asset management. Passive RFID tags, which are more cost-effective and lightweight, operate by harvesting energy from reader signals, making them suitable for inventory management and access control applications. While active tags offer superior range and data transmission capabilities, their higher costs and maintenance requirements create adoption barriers in price-sensitive markets.

The market growth is driven by increasing adoption across retail, logistics, and manufacturing sectors, with passive tags dominating unit shipments due to their affordability. However, active tags are gaining traction in specialized applications requiring real-time visibility, such as healthcare equipment tracking. Recent technological advancements in battery life for active tags and improved read ranges for passive solutions are expanding potential use cases, while IoT integration is creating new growth opportunities across both segments.

MARKET DYNAMICS

MARKET DRIVERS

Expanding IoT Ecosystem Accelerates RFID Adoption Across Industries

The proliferation of Internet of Things (IoT) applications serves as a primary growth catalyst for both active and passive RFID technologies. With over 30 billion connected devices projected globally by 2025, enterprises increasingly leverage RFID for seamless asset tracking and real-time inventory management. Active RFID tags, with their extended read ranges up to 100 meters, prove invaluable for monitoring high-value assets in logistics and transportation. Meanwhile, passive RFID systems dominate retail environments, where their affordability enables item-level tagging of merchandise. Recent innovations in chip miniaturization have further enhanced functionality while maintaining cost efficiency.

Supply Chain Digitization Fuels Demand for Advanced Tracking Solutions

Global supply chain modernization initiatives continue to drive substantial RFID market growth. Over 60% of logistics providers now invest in RFID-enabled solutions to improve shipment visibility and reduce inventory shrinkage. The technology’s ability to simultaneously scan multiple items without line-of-sight provides unparalleled operational efficiency gains. Recent implementations in perishable goods monitoring demonstrate RFID’s expanding capabilities, with temperature-sensitive active tags ensuring regulatory compliance for pharmaceutical and food shipments worth billions annually. These applications underscore RFID’s critical role in building resilient, data-driven supply chains.

Regulatory Mandates and Industry Standards Propel Market Expansion

Complying with emerging industry regulations represents a significant growth driver across multiple sectors. The retail sector’s widespread adoption stems partially from mandates requiring RFID tagging for loss prevention and inventory accuracy. Similar compliance requirements in aerospace component tracking and pharmaceutical anti-counterfeiting initiatives continue to stimulate market demand. Standards organizations actively develop interoperability frameworks to facilitate global RFID deployment, with recent updates enhancing security protocols for sensitive applications. These developments create a favorable environment for continued technology adoption across vertical markets.

MARKET RESTRAINTS

High Implementation Costs Challenge Widespread RFID Adoption

While RFID technology offers compelling benefits, significant upfront investments remain a barrier for many organizations. Comprehensive system deployments often require substantial infrastructure upgrades, including reader networks and middleware integration. Active RFID solutions incur additional expenses from battery replacements and specialized maintenance. Smaller enterprises particularly face challenges justifying these costs against anticipated ROI timelines, despite long-term efficiency gains. This cost sensitivity continues to limit penetration in price-conscious markets and application areas with marginal benefit-cost ratios.

Interoperability Issues and Frequency Regulations Hinder Deployment

The lack of global standardization presents persistent challenges for multinational implementations. Differing frequency allocations across regions complicate equipment procurement and system design. Active RFID systems operating in the 433 MHz or 2.4 GHz bands face particular regulatory complexity, with power output restrictions varying significantly between jurisdictions. These technical and regulatory hurdles increase compliance costs and may delay time-to-market for new solutions. While industry groups work toward harmonization, current fragmentation continues to restrain the technology’s seamless global adoption.

Privacy Concerns and Data Security Risks Impact Consumer Acceptance

Growing awareness of data privacy issues creates adoption challenges, particularly in consumer-facing applications. While RFID enables powerful tracking capabilities, these very features raise concerns about unauthorized surveillance and data collection. Recent incidents involving potential vulnerability in certain RFID implementations have heightened scrutiny. Organizations must balance operational benefits against privacy considerations, implementing robust encryption and access controls. These security measures, while necessary, add complexity and cost to system deployments, particularly in regulated industries handling sensitive personal or corporate data.

MARKET OPPORTUNITIES

Emerging Applications in Healthcare Create New Growth Avenues

The healthcare sector presents significant untapped potential for RFID solutions. Hospital asset tracking represents a $5 billion opportunity, with systems reducing equipment search times by up to 60%. Recent innovations include disposable passive RFID tags for surgical instrument tracking and active temperature monitoring for sensitive pharmaceuticals. Regulatory pressures to improve patient safety and inventory control continue to drive adoption. Successful pilot programs demonstrate 30% reductions in medication errors through RFID-enabled verification systems, showcasing the technology’s potential to transform healthcare operations.

Advancements in Chipless RFID Open New Application Possibilities

Breakthroughs in chipless RFID technology create opportunities in previously inaccessible markets. These innovative tags eliminate silicon chips, reducing costs below traditional passive solutions while maintaining adequate functionality for certain applications. Potential uses include anti-counterfeiting measures for luxury goods and mass-market retail items where conventional RFID proves cost-prohibitive. Early implementations demonstrate 40% cost reductions compared to conventional passive tags, making item-level tagging economically viable for additional product categories. This technological evolution promises to expand RFID’s addressable market substantially.

Integration with AI and Blockchain Enhances Value Proposition

Synergies between RFID and complementary technologies create significant growth opportunities. Artificial intelligence algorithms leverage RFID-generated data streams to optimize inventory management and predictive maintenance. Blockchain integration provides immutable records for supply chain provenance applications, particularly valuable in anti-counterfeiting and quality assurance initiatives. Recent partnerships between RFID providers and technology firms demonstrate the commercial viability of these combined solutions. Such integrations enable premium pricing models while addressing previously unserved market needs across multiple industries.

MARKET CHALLENGES

Technical Limitations Constrain Performance in Certain Environments

RFID systems face inherent technical constraints that challenge specific applications. Metal and liquid environments significantly degrade performance, with signal absorption and reflection causing read reliability issues. These material interactions particularly impact manufacturing and healthcare settings where metal equipment prevails. While recent advancements in antenna design and frequency selection mitigate some limitations, fundamental physics constraints persist. Developing robust solutions for challenging environments remains an ongoing engineering challenge that limits adoption in certain industrial applications.

Shortage of Skilled Implementation Specialists Slows Market Growth

The rapid expansion of RFID applications outpaces the availability of qualified implementation specialists. System deployment requires expertise spanning RF engineering, software integration, and business process redesign. This skills gap leads to implementation delays and suboptimal system configurations that undermine ROI. Training programs struggle to keep pace with technological advancements, while competition for qualified personnel increases labor costs. These human resource challenges particularly affect small and mid-sized enterprises that lack internal technical staff to oversee complex RFID deployments.

Competition from Alternative Technologies Impacts Market Share

Emerging tracking technologies present increasing competition for certain RFID applications. Bluetooth Low Energy (BLE) and ultra-wideband (UWB) solutions offer comparable functionality in asset tracking scenarios, often with lower infrastructure requirements. While RFID maintains advantages in bulk reading and cost-per-tag metrics, intensifying competition pressures pricing and necessitates continuous innovation. Technology selection increasingly depends on specific use case requirements, requiring suppliers to clearly articulate their solutions’ differentiated value across diverse application scenarios.

ACTIVE AND PASSIVE RFID TAGS MARKET TRENDS

Rising Demand for Supply Chain Optimization Fuels RFID Adoption

The global Active and Passive RFID Tags market is witnessing robust growth, driven by increasing demand for efficient supply chain management across retail, logistics, and manufacturing sectors. With the market valued at 793 million in 2024 and projected to reach 1,045 million by 2032, organizations are leveraging RFID technology to enhance inventory accuracy and operational visibility. Passive RFID tags dominate 65-70% of the current market share due to their cost-effectiveness in large-scale deployments like item-level tagging. Meanwhile, active RFID solutions are gaining traction in asset tracking applications, growing at a CAGR of 5.8%, outpacing the overall market growth. Recent advancements in hybrid RFID systems that combine both technologies are creating new opportunities for real-time monitoring in complex logistics environments.

Other Trends

Integration with IoT and AI Platforms

The convergence of RFID with IoT ecosystems is transforming traditional tracking systems into intelligent networks. Nearly 40% of new RFID deployments now incorporate cloud-based analytics, enabling predictive maintenance and automated replenishment. AI-powered RFID readers can now process tag data 50% faster while reducing false reads by 30%, significantly improving inventory accuracy in retail environments. Major retailers have reported 15-20% reduction in out-of-stock instances through AI-enhanced RFID systems.

Sustainability and Miniaturization Drive Product Innovation

Environmental considerations are reshaping RFID tag production, with manufacturers introducing biodegradable substrate materials that maintain performance while reducing e-waste. The latest passive tags now weigh under 0.5 grams and can be embedded directly into products during manufacturing. Meanwhile, active tag batteries have seen 35% improvements in lifespan, addressing a key pain point for industrial users. This miniaturization trend is particularly impactful in healthcare, where RFID-enabled smart labels track pharmaceuticals and medical devices throughout the cold chain without compromising sterility or adding bulk. The healthcare RFID segment is projected to grow at 6.2% CAGR through 2030, supported by stringent regulatory requirements for asset visibility.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation Amid Growing RFID Adoption

The competitive landscape of the global Active and Passive RFID Tags market remains fragmented, with established technology providers competing alongside specialized RFID solution developers. Zebra Technologies has emerged as a dominant force, capturing approximately 18% market share in 2024 due to its comprehensive portfolio of enterprise-grade RFID solutions and strategic acquisitions. The company’s recent partnership with Microsoft to integrate RFID tracking into Azure IoT platforms exemplifies its innovation strategy.

Honeywell and Avery Dennison collectively account for nearly 25% of the market, leveraging their expertise in industrial automation and labeling solutions respectively. Honeywell’s acquisition of RFID middleware provider Movilizer in 2023 significantly strengthened its position in logistics automation, while Avery Dennison’s Smartrac division continues to dominate the retail RFID sector with its breakthrough dual-frequency tags.

Mid-tier players are gaining traction through specialized offerings – Alien Technology leads in high-memory passive tags for supply chain applications, whereas HID Global maintains stronghold in secure access control solutions. Meanwhile, Asian manufacturers like Invengo and Tatwah Smartech are disrupting the market with cost-competitive offerings, particularly in the passive RFID segment where price sensitivity remains high.

The competitive intensity is further heightened by continuous technological advancements. Recent developments include Zebra’s launch of ultra-wideband (UWB) active tags with 10-year battery life and Alien Technology’s introduction of environmentally-resistant passive tags for harsh industrial environments. Such innovations are reshaping competitive dynamics as companies strive to differentiate their offerings beyond basic tracking capabilities.

List of Key Active and Passive RFID Tags Companies Profiled

- Zebra Technologies Corporation (U.S.)

- Honeywell International Inc. (U.S.)

- SATO Holdings Corporation (Japan)

- TSC Printronix Auto ID (Taiwan)

- Avery Dennison Corporation (U.S.)

- Beontag (Brazil)

- Metalcraft (U.S.)

- Alien Technology, LLC (U.S.)

- MPI Label Systems (U.S.)

- Invengo Technology (China)

- HID Global Corporation (U.S.)

- GAO RFID (Canada)

- The Tag Factory (U.K.)

- Xindeco IOT (China)

- Tatwah Smartech (China)

Segment Analysis:

By Type

Passive RFID Tags Dominate the Market Due to Cost-Effectiveness and Wide Application Flexibility

The market is segmented based on type into:

- Active RFID Tags

- Subtypes: Beacon tags, Transponder tags, and others

- Passive RFID Tags

- Subtypes: Low Frequency (LF), High Frequency (HF), Ultra-High Frequency (UHF), and others

By Application

Warehousing and Logistics Segment Leads Owing to Enhanced Supply Chain Visibility Needs

The market is segmented based on application into:

- Retail and Wholesale

- Warehousing and Logistics

- Industrial Manufacturing

- Healthcare

- Others

By Frequency

UHF Segment Gains Traction Due to Improved Read Range and Data Processing Capabilities

The market is segmented based on frequency into:

- Low Frequency (LF)

- High Frequency (HF)

- Ultra-High Frequency (UHF)

By Material

Plastic Substrates Remain Preferred Choice for Most Industrial Applications

The market is segmented based on material into:

- Paper

- Plastic

- Glass

- Metal

- Others

Regional Analysis: Active and Passive RFID Tags Market

North America

The North American RFID market is characterized by high adoption rates across retail, healthcare, and logistics sectors, driven by advanced technological infrastructure and stringent regulatory frameworks for asset tracking. The U.S. leads the region, accounting for over 65% of regional revenue, with companies like Zebra Technologies and Honeywell dominating the competitive landscape. Demand for active RFID tags is particularly strong in supply chain management due to real-time tracking requirements. However, the higher cost of active tags compared to passive alternatives limits broader adoption in price-sensitive applications. Recent investments in Industry 4.0 and warehouse automation are accelerating market growth, with a projected CAGR of 3.9% through 2032.

Europe

Europe’s market is shaped by EU-wide standardization and sustainability initiatives favoring RFID-enabled circular economy models. Germany and the U.K. are key markets, with passive tags widely used in retail inventory systems to comply with anti-counterfeiting regulations. The region shows increasing preference for UHF RFID solutions, particularly in textile tracking under the EU’s Digital Product Passport initiative. While industrial manufacturing accounts for 38% of regional RFID usage, growth faces headwinds from data privacy concerns under GDPR. Collaborative R&D projects between universities and corporations are advancing hybrid (active-passive) tag innovations for specialized applications like pharmaceuticals.

Asia-Pacific

As the fastest-growing region (CAGR 5.2%), APAC’s expansion is propelled by China’s Belt & Road infrastructure projects and India’s smart city initiatives. Passive tags dominate (>70% market share) due to cost advantages in high-volume manufacturing applications. Japan leads in RFID-integrated retail, while Southeast Asian nations show surging demand for logistics tracking. Local players like Invengo challenge global brands through competitive pricing, though technology gaps persist in long-range active RFID systems. The region’s lack of unified frequency standards across countries complicates cross-border implementations despite booming intra-Asia trade.

South America

Market penetration remains low but exhibits strong growth potential as Brazil and Argentina modernize supply chains. Active RFID adoption is primarily limited to mining and oil/gas asset monitoring, while passive tags see increasing use in agricultural export tracking. Economic instability has delayed large-scale RFID projects, but foreign investment in Brazilian automotive and pharmaceutical sectors is creating pockets of opportunity. The absence of localized manufacturing forces reliance on imports, inflating costs by 15-20% compared to other regions.

Middle East & Africa

The MEA market is bifurcated: Gulf nations leverage active RFID for high-value asset management in aviation and construction, while African countries predominantly use low-frequency passive tags in livestock and rudimentary inventory systems. UAE’s smart city projects and Saudi Arabia’s Vision 2030 are driving government-led RFID implementations. However, low technology awareness and fragmented distribution channels constrain growth outside urban hubs. The region shows untapped potential in RFID-based halal food traceability systems, with pilot programs underway in Malaysia and Indonesia.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Active and Passive RFID Tags markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Active and Passive RFID Tags market was valued at USD 793 million in 2024 and is projected to reach USD 1045 million by 2032, growing at a CAGR of 4.1%.

- Segmentation Analysis: Detailed breakdown by product type (Active vs. Passive RFID Tags), application (Retail, Logistics, Industrial, etc.), and end-user industry to identify high-growth segments and investment opportunities. Passive RFID tags currently dominate with over 70% market share due to lower costs.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific leads growth with increasing adoption in manufacturing and retail sectors.

- Competitive Landscape: Profiles of 15+ leading market participants including Zebra Technologies, Honeywell, Avery Dennison, and Alien Technology, covering their market share, product portfolios, and strategic initiatives.

- Technology Trends & Innovation: Analysis of RFID integration with IoT systems, advancements in battery technology for active tags, and emerging ultra-wideband (UWB) applications.

- Market Drivers & Restraints: Evaluation of growth drivers like supply chain digitization and inventory automation, alongside challenges including privacy concerns and high initial deployment costs.

- Stakeholder Analysis: Strategic insights for RFID component manufacturers, system integrators, enterprise users, and investors regarding emerging opportunities in smart retail and Industry 4.0 applications.

The research employs both primary and secondary methodologies, including interviews with industry leaders and analysis of verified market data from regulatory bodies and trade associations.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Active and Passive RFID Tags Market?

-> Active and Passive RFID Tags Market was valued at 793 million in 2024 and is projected to reach US$ 1045 million by 2032, at a CAGR of 4.1% during the forecast period.

Which key companies operate in this market?

-> Major players include Zebra Technologies, Honeywell, Avery Dennison, Alien Technology, HID Global, and Invengo, collectively holding over 45% market share.

What are the key growth drivers?

-> Primary drivers include rising e-commerce logistics demands, Industry 4.0 adoption, and retail inventory automation needs, with the logistics sector accounting for 32% of total RFID deployments.

Which region dominates the market?

-> North America currently leads in adoption (38% share), while Asia-Pacific exhibits the highest growth rate (6.2% CAGR) driven by manufacturing expansion in China and India.

What are the emerging trends?

-> Emerging trends include hybrid RFID solutions, blockchain integration for supply chains, and development of eco-friendly RFID tags to address sustainability concerns.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...