MARKET INSIGHTS

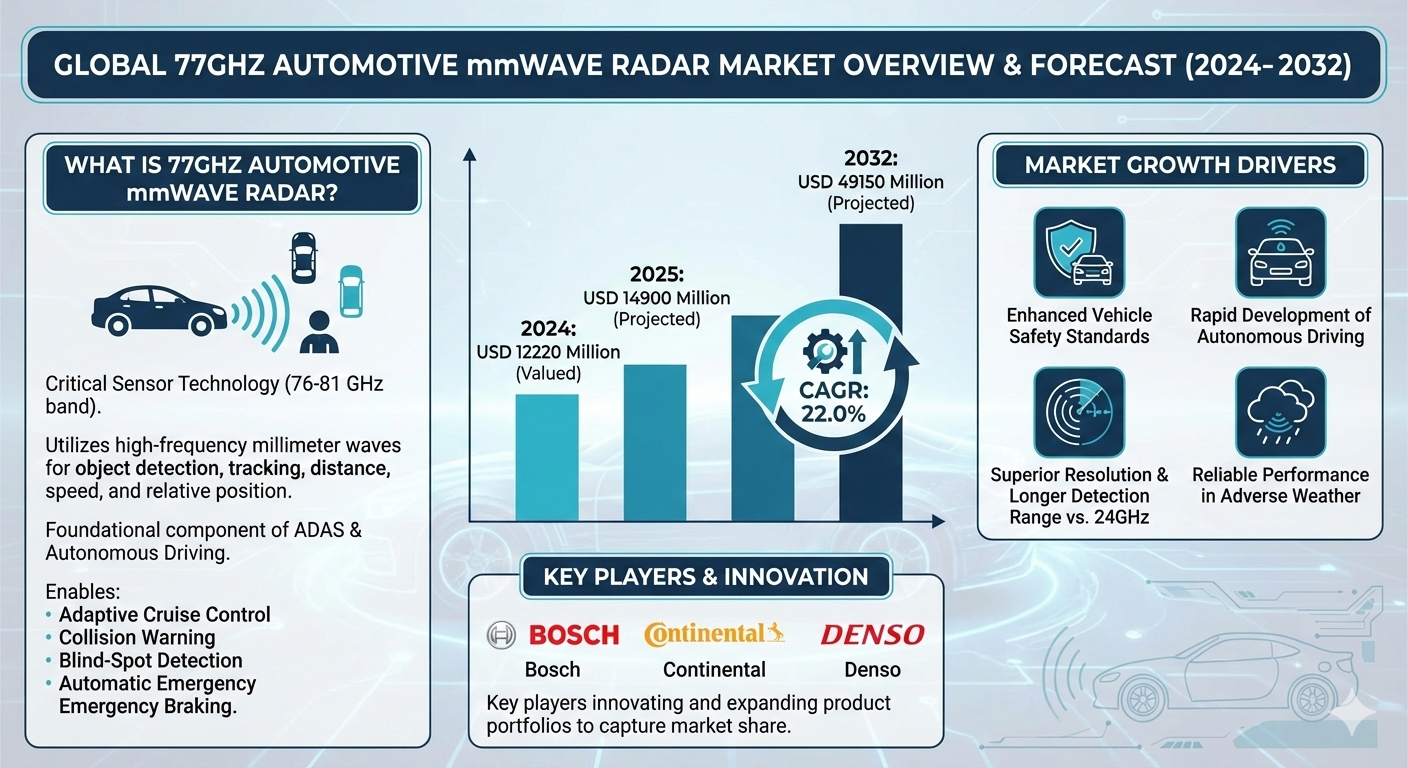

The global 77GHz Automotive mmWave Radar Market was valued at 12220 million in 2024 and is projected to reach US$ 49150 million by 2032, at a CAGR of 22.0% during the forecast period.

77GHz automotive millimeter-wave radar is a critical sensor technology designed for vehicles, operating within the 76-81 GHz frequency band. It utilizes high-frequency millimeter waves to detect and track objects in the vehicle’s vicinity, providing precise data on distance, speed, and relative position. This technology is a foundational component of Advanced Driver-Assistance Systems (ADAS) and autonomous driving, enabling essential safety features such as adaptive cruise control, collision warning, blind-spot detection, and automatic emergency braking.

The market is experiencing robust growth driven by the global push for enhanced vehicle safety standards and the rapid development of autonomous driving technologies. The superior resolution and longer detection range of 77GHz radar, compared to older 24GHz systems, make it indispensable for modern automotive applications. Its ability to perform reliably in adverse weather conditions, where optical sensors like cameras may fail, further solidifies its role. Key industry players, including Bosch, Continental, and Denso, are continuously innovating and expanding their product portfolios to capture market share, fueling further expansion and technological advancement.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Advanced Driver Assistance Systems to Accelerate Market Growth

The global automotive industry is witnessing unprecedented integration of Advanced Driver Assistance Systems (ADAS) across vehicle segments, driving substantial demand for 77GHz mmWave radar technology. This frequency band has become the industry standard for critical safety applications due to its superior resolution and detection capabilities compared to lower frequency alternatives. Regulatory mandates across multiple regions requiring enhanced vehicle safety features have accelerated adoption rates, with over 65% of new vehicles in developed markets now equipped with some form of ADAS functionality. The 77GHz radar’s ability to provide precise object detection, velocity measurement, and angular positioning makes it indispensable for features like autonomous emergency braking, adaptive cruise control, and blind spot detection. Market analysis indicates that vehicles equipped with comprehensive ADAS packages demonstrate up to 40% reduction in collision rates, creating strong consumer and regulatory push for wider implementation.

Advancements in Autonomous Driving Technology to Fuel Market Expansion

The progression toward higher levels of vehicle automation represents a fundamental growth driver for 77GHz radar technology. As automakers target Level 3 and Level 4 autonomy, sensor redundancy and reliability become paramount requirements. The 77GHz radar’s all-weather operational capability provides critical advantages over optical sensors, particularly in adverse conditions where cameras and LiDAR face performance limitations. Recent technological breakthroughs have enhanced resolution to sub-degree accuracy while maintaining detection ranges exceeding 250 meters, enabling sophisticated path prediction and object classification algorithms. The automotive industry’s collective investment in autonomous driving technology exceeds $100 billion annually, with radar systems representing approximately 15-20% of total sensor suite investments. This substantial financial commitment underscores the strategic importance of 77GHz technology in achieving viable autonomous driving solutions.

Increasing Vehicle Safety Regulations and NCAP Ratings to Drive Implementation

Global regulatory frameworks and consumer safety rating programs continue to raise the bar for vehicle safety standards, creating mandatory adoption pathways for 77GHz radar systems. New Car Assessment Programs (NCAP) across North America, Europe, and Asia-Pacific have progressively incorporated advanced safety features into their rating criteria, with top safety ratings now requiring comprehensive ADAS implementations. Regulatory bodies have established performance standards for collision avoidance systems that effectively mandate radar-based solutions for achieving compliance. The European Union’s General Safety Regulation, implemented in 2022, requires all new vehicles to include intelligent speed assistance and advanced emergency braking systems, creating immediate demand for radar sensors. Similar regulations in the United States and China have accelerated OEM adoption timelines, with penetration rates in new vehicles expected to exceed 85% by 2028 across major automotive markets.

MARKET CHALLENGES

High System Integration Costs and Complexity to Hinder Widespread Adoption

While technological capabilities continue to advance, the integration of 77GHz radar systems presents significant cost and complexity challenges for automotive manufacturers. The current system cost remains substantially higher than traditional automotive components, with complete radar modules ranging between $150-400 per unit depending on performance specifications. This cost structure creates particular challenges for entry-level and mid-market vehicle segments where price sensitivity is most pronounced. Beyond component costs, integration requires sophisticated calibration processes, electromagnetic compatibility management, and complex software integration with vehicle control systems. The development cycle for new radar-integrated vehicles typically extends 12-18 months longer than conventional models due to validation requirements and regulatory compliance testing. These factors collectively create adoption barriers, particularly for manufacturers operating in highly competitive market segments with narrow profit margins.

Other Challenges

Spectrum Allocation and Regulatory Compliance Issues

The 77GHz band operates within a strictly regulated portion of the electromagnetic spectrum, requiring manufacturers to navigate complex international regulatory frameworks. Different regions maintain varying technical requirements for transmission power, bandwidth utilization, and interference mitigation, creating compliance challenges for global vehicle platforms. Recent spectrum reallocations for 5G telecommunications have created potential interference concerns, requiring advanced filtering techniques and frequency coordination measures. The certification process for new radar systems typically involves multi-year validation cycles across different regulatory jurisdictions, delaying market entry and increasing development costs.

Technical Limitations in Object Discrimination and Resolution

Despite significant advancements, 77GHz radar systems still face challenges in precise object classification and discrimination compared to multi-sensor approaches. The technology demonstrates limitations in distinguishing between multiple closely spaced objects and accurately identifying specific object types in complex traffic scenarios. These limitations become particularly relevant in urban environments where pedestrians, cyclists, and vehicles operate in close proximity. Current systems require sophisticated signal processing algorithms and sensor fusion approaches to achieve the reliability standards required for autonomous driving applications, adding computational complexity and development costs.

MARKET RESTRAINTS

Supply Chain Constraints and Semiconductor Shortages to Limit Market Growth

The 77GHz radar market faces significant constraints from ongoing global semiconductor shortages and specialized component supply chain limitations. These systems require highly specialized integrated circuits manufactured using advanced semiconductor processes that have limited global production capacity. The automotive industry’s transition toward electrification and digitalization has created unprecedented demand for automotive-grade semiconductors, with lead times for certain critical components extending beyond 52 weeks. This supply-demand imbalance has forced automakers to delay vehicle production and reduce optional equipment availability, directly impacting radar system implementation rates. The situation is further complicated by geopolitical factors affecting semiconductor manufacturing and export controls, creating uncertainty in long-term component availability and pricing stability.

Technical Standardization and Interoperability Issues to Restrain Market Development

The absence of comprehensive technical standards and interoperability frameworks presents significant restraints to market growth. While the 77GHz frequency band has achieved broad regulatory acceptance, implementation approaches vary considerably between manufacturers regarding waveform design, signal processing methodologies, and data interface protocols. This lack of standardization creates compatibility challenges for vehicle platforms that incorporate radar systems from multiple suppliers and complicates aftermarket repair and calibration processes. The industry’s fragmented approach to sensor fusion architectures further exacerbates interoperability issues, as different manufacturers employ proprietary algorithms and data structures that limit cross-platform compatibility. These technical disparities increase development costs, extend validation timelines, and create barriers to widespread technology adoption across the automotive ecosystem.

Consumer Acceptance and Privacy Concerns to Impact Adoption Rates

Market growth faces restraints from consumer acceptance issues and privacy concerns surrounding continuous monitoring and data collection capabilities. While safety benefits are well-established, some consumer segments express reservations about pervasive sensor systems that continuously monitor the vehicle environment. Privacy advocacy groups have raised concerns about data collection practices and potential misuse of environmental information gathered by radar systems. These concerns have prompted regulatory reviews in several jurisdictions regarding data privacy frameworks for automotive sensors. Additionally, insurance implications and liability questions surrounding automated systems create consumer hesitation, particularly in regions with complex legal frameworks governing automotive accidents and system failures. These factors collectively influence purchasing decisions and may slow adoption rates in certain market segments.

MARKET OPPORTUNITIES

Emerging Applications in Commercial Vehicles and Fleet Management to Create New Growth Avenues

The commercial vehicle segment presents substantial growth opportunities for 77GHz radar technology, particularly in fleet management and logistics applications. Commercial fleet operators are increasingly adopting advanced safety systems to reduce accident rates, lower insurance costs, and improve operational efficiency. Radar-based systems offer particular advantages for large vehicles with significant blind spots and complex maneuvering requirements. The technology enables advanced features like trailer alignment monitoring, loading dock assistance, and pedestrian detection around stationary vehicles. Market analysis indicates that commercial vehicle adoption rates for advanced radar systems could reach 70% by 2030, representing a addressable market exceeding 15 million units annually. This segment demonstrates less price sensitivity than consumer vehicles and faster adoption cycles due to clear return-on-investment calculations from safety improvements and operational efficiencies.

Technological Innovations in Radar Chipset Design to Enable Cost Reduction and Performance Enhancement

Breakthroughs in semiconductor technology and integrated circuit design are creating opportunities for significant cost reduction and performance improvement in 77GHz radar systems. The development of system-on-chip solutions that integrate multiple radar functions into single silicon packages has reduced component counts by over 40% while improving reliability and manufacturing scalability. Advanced semiconductor processes using silicon-germanium and gallium-nitride technologies are enabling higher output power and improved signal-to-noise ratios, enhancing detection range and accuracy. These technological advancements are driving cost reductions exceeding 15% annually while simultaneously improving performance specifications. The emergence of software-defined radar architectures further enhances flexibility and future-proofing capabilities, allowing performance upgrades through software updates rather than hardware replacements.

Expansion into Non-Traditional Automotive Applications to Diversify Market Opportunities

Beyond conventional automotive applications, 77GHz radar technology is finding new opportunities in adjacent markets including infrastructure monitoring, industrial automation, and smart city applications. Traffic management systems are adopting radar technology for vehicle counting, speed enforcement, and intersection monitoring with advantages over traditional methods in adverse weather conditions. Industrial applications include machinery protection systems, automated guided vehicle navigation, and perimeter security implementations. The technology’s ability to operate reliably in challenging environmental conditions makes it suitable for these diverse applications, creating additional revenue streams for manufacturers and reducing dependence on automotive market cycles. These emerging applications could represent over 20% of total market volume by 2030, providing diversification benefits and growth stability for industry participants.

77GHZ AUTOMOTIVE MMWAVE RADAR MARKET TRENDS

Integration with Autonomous Driving Systems to Emerge as a Dominant Trend

The proliferation of autonomous driving systems is fundamentally reshaping the 77GHz automotive mmWave radar market. As vehicles progress through the levels of automation, from Level 2 (partial automation) to Level 4 (high automation), the demand for robust, reliable, and high-resolution sensor suites intensifies. The 77GHz radar is a cornerstone of this ecosystem, prized for its exceptional long-range object detection capabilities and resilience in adverse weather conditions where optical sensors falter. This trend is directly fueled by global regulatory pushes for enhanced vehicle safety; for instance, the European New Car Assessment Programme (Euro NCAP) has incorporated Advanced Driver-Assistance Systems (ADAS) testing into its safety ratings, making features like Autonomous Emergency Braking (AEB) and adaptive cruise control nearly standard in new models. Consequently, automakers are integrating multiple 77GHz radar units per vehicle, moving beyond a single front-facing radar to include corner and rear radars for a 360-degree sensing cocoon, a key enabler for higher levels of autonomy.

Other Trends

Miniaturization and Cost Reduction

A significant and ongoing trend is the relentless drive toward miniaturization and cost reduction of 77GHz radar modules. Early systems were relatively bulky and expensive, limiting their adoption to premium vehicle segments. However, advancements in semiconductor technology, particularly in Silicon-Germanium (SiGe) and CMOS-based RF integrated circuits, have enabled the development of highly compact, single-chip radar solutions. This technological evolution drastically reduces the physical footprint, power consumption, and, most importantly, the bill of materials. As production volumes scale to meet soaring demand, economies of scale are further driving down costs. This is crucial for democratizing safety technologies, allowing them to penetrate mid-range and eventually economy vehicle segments, thereby expanding the total addressable market significantly. This trend is vital for achieving the projected market growth, making advanced safety features accessible to a broader consumer base.

Sensor Fusion and AI-Powered Signal Processing

The evolution towards sensor fusion represents a critical trend, moving beyond the capabilities of any single sensor type. While the 77GHz radar excels in measuring distance and velocity and performing well in poor weather, it lacks the high-definition spatial awareness of LiDAR or the rich contextual data provided by cameras. The market trend is therefore shifting towards the sophisticated integration of these sensors. The 77GHz radar’s role in this fused system is often to provide a highly reliable baseline of object list data—confirming the presence, range, and radial speed of targets identified by other sensors. Furthermore, the application of Artificial Intelligence (AI) and machine learning algorithms to raw radar signal processing is a groundbreaking development. These advanced algorithms can dramatically improve object classification, distinguishing between a pedestrian, a cyclist, and a stationary pole with far greater accuracy than traditional methods. This enhances the overall decision-making capability of the ADAS or autonomous driving system, reducing false positives and increasing overall safety and reliability.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Alliances and Technological Innovation Drive Market Leadership

The global competitive landscape for the 77GHz Automotive mmWave Radar market is characterized by a mix of established automotive suppliers and emerging technology specialists. The market structure is moderately consolidated, with the top five players collectively holding a significant portion of the market share. This concentration is driven by high R&D costs, complex manufacturing processes, and the need for strong relationships with automotive OEMs.

Robert Bosch GmbH and Continental AG are recognized as market leaders, primarily due to their extensive product portfolios, longstanding relationships with global automakers, and substantial investment in research and development. Both companies have pioneered advancements in radar technology, particularly in enhancing object resolution and environmental robustness. Their global production footprint ensures reliable supply to major automotive manufacturing regions worldwide.

Denso Corporation and Valeo SA also command considerable market presence. Their growth is largely attributed to focused innovation in compact radar design and cost-effective solutions tailored for high-volume vehicle platforms. These companies have been particularly successful in the Asian and European markets, where regulatory push for advanced safety features is strongest.

Furthermore, growth strategies among these key players increasingly involve strategic partnerships with semiconductor companies and software firms to enhance system-on-chip capabilities and AI-driven signal processing. Recent mergers and acquisitions have also been observed, aimed at vertical integration and securing technological patents.

Meanwhile, companies like Aptiv PLC and ZF Friedrichshafen AG are strengthening their positions through targeted investments in next-generation radar systems capable of supporting higher levels of autonomy. Their focus on developing scalable architectures allows them to serve both premium and mass-market segments effectively.

List of Key Companies Profiled in the 77GHz Automotive mmWave Radar Market

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- Denso Corporation (Japan)

- HELLA GmbH & Co. KGaA (Germany)

- Veoneer, Inc. (Sweden)

- Valeo SA (France)

- Aptiv PLC (Ireland)

- ZF Friedrichshafen AG (Germany)

- WHST (China)

- Hitachi Astemo, Ltd. (Japan)

- Nidec Elesys Corporation (Japan)

- Cheng-Tech (China)

- Chuhang Tech (China)

- HUAYU Automotive Systems Co., Ltd. (China)

- Desay SV Automotive Co., Ltd. (China)

Segment Analysis:

By Type

Long-Range mmWave Radar Segment Dominates Due to Critical Role in Adaptive Cruise Control and Autonomous Highway Driving

The market is segmented based on type into:

- Short-range mmWave Radar

- Medium-range mmWave Radar

- Long-range mmWave Radar

By Application

Passenger Vehicle Segment Leads Due to High Adoption of ADAS Features and Stringent Safety Regulations

The market is segmented based on application into:

- Passenger Vehicle

- Commercial Vehicle

By Function

Adaptive Cruise Control Represents the Largest Functional Segment Owing to its Standardization in Mid to High-End Vehicles

The market is segmented based on function into:

- Adaptive Cruise Control (ACC)

- Automatic Emergency Braking (AEB)

- Blind Spot Detection (BSD)

- Forward Collision Warning (FCW)

- Others

By Vehicle Autonomy Level

Level 2 and Level 2+ Vehicles Represent the Primary Market Due to Current Commercial Deployment and Consumer Readiness

The market is segmented based on vehicle autonomy level into:

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

Regional Analysis: 77GHz Automotive mmWave Radar Market

Asia-Pacific

The Asia-Pacific region dominates the global 77GHz automotive mmWave radar market, accounting for over 45% of total volume consumption as of 2024. This leadership position is driven by massive automotive production in China, Japan, and South Korea, coupled with aggressive government mandates for advanced driver-assistance systems (ADAS). China’s New Car Assessment Program (C-NCAP) has significantly raised safety standards, requiring more vehicles to incorporate collision avoidance technologies. Japan’s automotive giants including Toyota, Honda, and Nissan are rapidly integrating 77GHz radar across their model ranges to maintain competitive advantage. South Korea’s strong electronics ecosystem supports local production of radar components. While cost sensitivity remains a factor, the region’s scale of manufacturing is driving down costs faster than other markets, making 77GHz radar increasingly accessible in mid-range vehicle segments.

Europe

Europe represents the second-largest market for 77GHz automotive mmWave radar, characterized by stringent safety regulations and high consumer adoption of premium vehicles. The EU’s General Safety Regulation (GSR2), which mandates advanced safety features including autonomous emergency braking (AEB) for all new vehicles from 2022 onward, has been a primary market driver. European automotive suppliers including Bosch, Continental, and ZF have established strong technological leadership in radar systems, with several introducing fourth-generation 77GHz radars with improved resolution and object classification capabilities. The region’s focus extends beyond compliance to developing sophisticated sensor fusion systems that combine radar with cameras and LiDAR for higher levels of automation. Germany remains the technological hub, with substantial R&D investments in radar signal processing and artificial intelligence for object recognition.

North America

North America’s market growth is propelled by consumer demand for safety features and regulatory initiatives from the National Highway Traffic Safety Administration (NHTSA). The region shows particularly strong adoption in premium and larger vehicle segments, including pickup trucks and SUVs, where 77GHz radar enables features like adaptive cruise control and blind-spot detection. The United States represents the largest sub-market, with significant investments in autonomous vehicle development influencing radar technology requirements. However, the market faces challenges from competing sensor technologies and cost pressures in entry-level vehicle segments. Recent developments include the integration of radar with vehicle-to-everything (V2X) communication systems, creating more comprehensive safety networks.

South America

The South American market for 77GHz automotive mmWave radar is emerging but faces significant growth constraints. Economic volatility and currency fluctuations make advanced safety systems challenging to implement in cost-sensitive markets. Brazil and Argentina represent the primary markets, though adoption remains largely limited to premium imported vehicles and locally manufactured high-end models. The region lacks comprehensive regulatory mandates for ADAS implementation, which slows widespread adoption. However, increasing awareness of vehicle safety and gradual economic stabilization are creating opportunities for market growth. Local assembly of vehicles with pre-installed radar systems is becoming more common, particularly from European and Asian manufacturers expanding their presence in the region.

Middle East & Africa

This region represents the smallest but growing market for 77GHz automotive mmWave radar. Development is uneven, with wealthier Gulf Cooperation Council (GCC) countries showing stronger adoption due to higher disposable income and preference for luxury vehicles. The United Arab Emirates and Saudi Arabia are leading markets where premium vehicle sales incorporate advanced safety systems. In contrast, most African markets face significant economic barriers to adoption, with radar systems primarily featured in imported luxury vehicles. The region’s extreme environmental conditions, including dust storms and high temperatures, create both challenges and opportunities for radar manufacturers to develop ruggedized systems. Long-term growth potential exists as economic development increases and regional safety standards evolve.

Report Scope

This market research report provides a comprehensive analysis of the global and regional 77GHz Automotive mmWave Radar markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 77GHz Automotive mmWave Radar Market?

-> 77GHz Automotive mmWave Radar Market was valued at 12220 million in 2024 and is projected to reach US$ 49150 million by 2032, at a CAGR of 22.0% during the forecast period.

Which key companies operate in Global 77GHz Automotive mmWave Radar Market?

-> Key players include Bosch, Continental, Denso, Hella, Veoneer, Valeo, Aptiv, and ZF, among others.

What are the key growth drivers?

-> Key growth drivers include increasing ADAS adoption, government safety regulations, and autonomous vehicle development.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe and North America remain dominant markets.

What are the emerging trends?

-> Emerging trends include 4D imaging radar, sensor fusion integration, and cost reduction through semiconductor innovation.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...