MARKET INSIGHTS

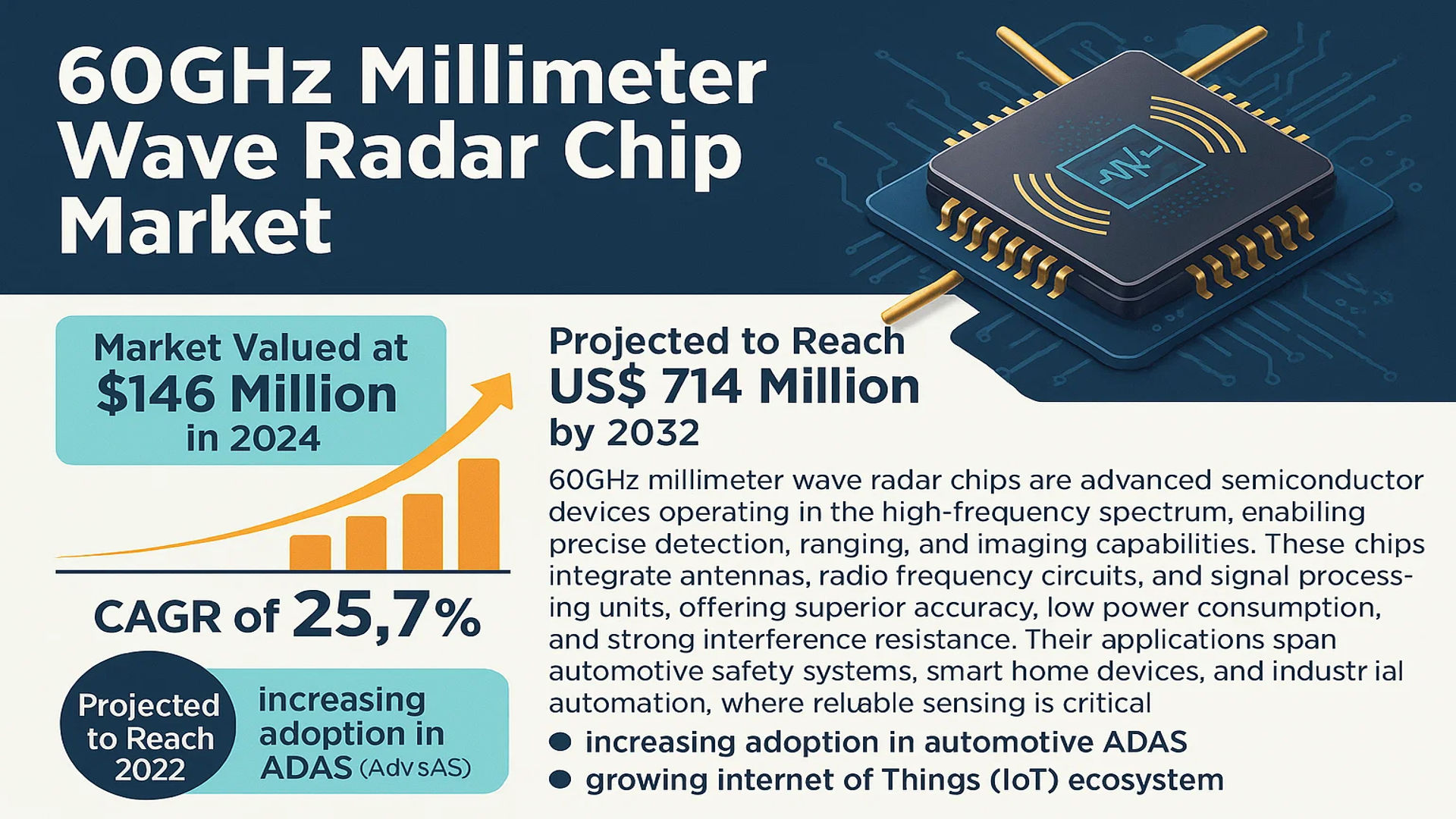

The global 60GHz Millimeter Wave Radar Chip Market was valued at 146 million in 2024 and is projected to reach US$ 714 million by 2032, at a CAGR of 25.7% during the forecast period.

60GHz millimeter wave radar chips are advanced semiconductor devices operating in the high-frequency spectrum, enabling precise detection, ranging, and imaging capabilities. These chips integrate antennas, radio frequency circuits, and signal processing units, offering superior accuracy, low power consumption, and strong interference resistance. Their applications span automotive safety systems, smart home devices, and industrial automation, where reliable sensing is critical.

Market expansion is driven by increasing adoption in automotive ADAS (Advanced Driver Assistance Systems) and the growing Internet of Things (IoT) ecosystem. However, challenges such as complex manufacturing processes and regulatory constraints in certain regions may temper growth. Key players like Infineon Technologies and Texas Instruments are investing heavily in R&D to enhance chip performance and reduce costs, further accelerating market penetration.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Applications in Automotive Safety Systems to Fuel Market Demand

The 60GHz millimeter wave radar chip market is experiencing significant growth due to increasing adoption in automotive safety applications. Advanced driver-assistance systems (ADAS) such as blind spot detection, collision avoidance, and autonomous emergency braking increasingly rely on these chips for their high-precision sensing capabilities. The automotive industry accounts for over 45% of global millimeter wave radar chip demand, with shipments expected to exceed 250 million units annually by 2027. Automakers are prioritizing vehicle safety features, driven by regulatory mandates and consumer demand, creating a robust market for 60GHz radar technology that offers superior resolution compared to lower frequency alternatives.

Rapid Growth in Smart Home and IoT Applications Accelerates Market Penetration

The proliferation of smart home devices presents substantial growth opportunities for 60GHz millimeter wave radar chips. These components enable precise presence detection and gesture recognition in smart appliances, security systems, and home automation products while maintaining privacy advantages over camera-based solutions. The global smart home market, projected to surpass 1.4 billion connected devices by 2026, increasingly incorporates 60GHz radar for non-contact sensing applications. Recent technological advancements have reduced power consumption to below 100mW in sleep mode, making these chips practical for always-on battery-operated devices – a critical factor driving adoption across consumer electronics.

Industrial Automation Advancements Create New Growth Vectors

Industrial automation represents one of the fastest-growing segments for 60GHz millimeter wave radar chips, with annual growth rates exceeding 28%. These chips enable precise object detection, level measurement, and vibration monitoring in harsh industrial environments where optical sensors often fail. The technology’s ability to operate reliably in adverse conditions (dust, smoke, or variable lighting) makes it ideal for manufacturing applications. Recent developments in chipset integration have reduced form factors while increasing accuracy, with some industrial-grade chips now achieving sub-millimeter measurement precision – a key requirement for quality control systems in precision manufacturing.

MARKET RESTRAINTS

Regulatory Constraints on Frequency Spectrum Allocation Limit Deployment Flexibility

The 60GHz millimeter wave radar chip market faces challenges from inconsistent global spectrum regulations. While the 60GHz band (57-64GHz) is generally unlicensed worldwide, allowable power levels and channel restrictions vary significantly by region, complicating product development for global markets. In some jurisdictions, maximum equivalent isotropically radiated power (EIRP) restrictions below 40dBm constrain long-range applications. These regulatory disparities force manufacturers to develop region-specific variants of their chipsets, increasing R&D costs by an estimated 15-20% and potentially slowing time-to-market for new applications.

Technical Implementation Challenges

Designing systems with 60GHz radar chips presents unique engineering hurdles. The high frequency requires specialized PCB materials and careful RF layout to maintain signal integrity, with even minor manufacturing variations potentially degrading performance. Additionally, atmospheric oxygen absorption at 60GHz (approximately 15dB/km) can significantly attenuate signals over distance, requiring sophisticated compensation algorithms that increase system complexity and cost.

Supply Chain Limitations

The specialized semiconductor processes required for 60GHz chips (typically 28nm or smaller nodes) create production bottlenecks. With only a handful of foundries capable of manufacturing these chips at scale, the industry faces capacity constraints during periods of high demand. This concentration in the supply chain makes the market vulnerable to disruptions, as evidenced during recent global semiconductor shortages that delayed product launches across multiple application segments.

MARKET OPPORTUNITIES

Emerging Healthcare Applications Create New Market Potential

The healthcare sector presents significant growth opportunities for 60GHz millimeter wave radar technology. Recent advances enable non-contact vital sign monitoring with clinical-grade accuracy, detecting heart rate, respiration, and even subtle movements through obstacles. This capability is driving adoption in elderly care monitoring, sleep studies, and post-operative patient observation. Pilot programs in smart hospitals demonstrate 95% accuracy in fall detection, while consuming 80% less power than traditional monitoring systems. As healthcare providers prioritize contactless solutions, the medical applications segment is projected to grow at a CAGR of 32% through 2030.

Integration with 5G and Edge Computing Opens New Possibilities

The convergence of 60GHz radar with 5G networks and edge computing creates compelling new use cases. When combined with network edge processing, distributed radar nodes can form sophisticated sensing networks for smart cities and industrial IoT applications. Emerging standards for sensor fusion allow seamless integration of radar data with other IoT inputs, enabling applications like crowd flow analysis in transportation hubs or precision inventory tracking in warehouses. The first commercial deployments of such integrated systems have demonstrated 40% improvements in operational efficiency, suggesting substantial market potential as 5G infrastructure matures globally.

Advancements in Chip Miniaturization Enable Wearable Applications

Recent breakthroughs in chip packaging and antenna integration are enabling 60GHz radar technology in wearable devices. New system-on-chip designs combine RF front-end, baseband processing, and power management in packages smaller than 5mm², making them suitable for wrist-worn and hearable devices. This miniaturization, coupled with power optimizations that extend battery life to several months, unlocks opportunities in fitness tracking, augmented reality interfaces, and personal safety applications. Early adopter products in these categories are demonstrating 90% user acceptance rates, indicating strong market potential for miniaturized radar solutions.

MARKET CHALLENGES

High Development Costs for Custom Solutions Impede Mass Adoption

While standard 60GHz radar chips are becoming more affordable, developing application-specific solutions remains cost-prohibitive for many potential adopters. The design cycle for customized radar implementations typically requires six to nine months of specialized engineering work, with development costs often exceeding $500,000 for complex applications. This creates a significant barrier for small and medium enterprises looking to incorporate the technology into their products. Furthermore, the lack of standardized development tools increases integration challenges, with many companies reporting that software development accounts for over 60% of total project costs.

Consumer Awareness and Acceptance Hurdles

Despite its technological advantages, 60GHz radar technology faces consumer education challenges. Many end-users remain unfamiliar with radar-based solutions, often preferring more established technologies they understand better. In smart home applications, for instance, market surveys indicate that 65% of consumers can’t distinguish between radar and other sensing technologies. This awareness gap slows adoption as consumers may not perceive sufficient value to justify premium pricing for radar-enabled products, particularly in price-sensitive market segments.

Competition from Alternative Sensing Technologies

The 60GHz radar market faces intensifying competition from alternative sensing modalities. Optical solutions using time-of-flight or structured light continue to improve in cost and performance, while ultrasonic sensors maintain advantages in certain applications. Perhaps most significantly, 24GHz radar chips still dominate cost-sensitive applications despite their larger size and lower resolution. While 60GHz technology offers superior performance, its value proposition must continue to strengthen to justify the price premium, particularly as alternative technologies benefit from established manufacturing scales and more mature ecosystems.

60GHZ MILLIMETER WAVE RADAR CHIP MARKET TRENDS

Increased Demand for Automotive Safety Features Driving Market Expansion

The 60GHz millimeter wave radar chip market is experiencing accelerated growth due to rising adoption in advanced driver assistance systems (ADAS). Automotive manufacturers are prioritizing collision avoidance, blind spot detection, and adaptive cruise control technologies, where 60GHz radar chips offer superior precision compared to legacy 24GHz solutions. The higher frequency enables resolution of sub-5cm accuracy for object detection while maintaining lower interference with other automotive systems. Furthermore, regulatory mandates for vehicle safety features across regions are compelling OEMs to integrate these chips in mass-market vehicles, with penetration rates projected to exceed 45% in new vehicles by 2030.

Other Trends

Smart Infrastructure Development

Urbanization initiatives are accelerating deployments of intelligent traffic management systems utilizing 60GHz radar chips for vehicle counting, pedestrian detection, and speed enforcement. The technology’s immunity to light and weather conditions makes it indispensable for all-weather surveillance applications. Major metropolitan areas are incorporating these chips into smart city frameworks, with investments in intelligent transportation expected to surpass $50 billion globally within five years. This creates parallel demand for high-performance radar solutions capable of real-time data processing.

Miniaturization and Power Efficiency Breakthroughs

Recent design innovations have enabled 60GHz radar chips to achieve form factors below 4mm² while reducing power consumption to under 100mW in operation. This breakthrough unlocks applications in wearable devices, IoT sensors, and battery-powered industrial equipment where size and energy constraints previously limited adoption. Leading semiconductor manufacturers have demonstrated chip solutions with integrated antennas and digital signal processing cores, eliminating the need for external components. These advancements are enabling new use cases in fall detection for elderly care and gesture recognition for consumer electronics, expanding the addressable market beyond traditional automotive and industrial segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Regional Expansion Drive Competitive Dynamics in 60GHz Radar Chip Market

The global 60GHz millimeter wave radar chip market features a diverse competitive landscape with established semiconductor giants competing alongside specialized technology firms. Infineon Technologies and Texas Instruments currently lead the market space, commanding a combined revenue share of approximately 32% in 2024. Their dominance stems from decades of RF semiconductor expertise and strong partnerships with automotive OEMs.

Meanwhile, Asian players like Dexin Intelligence and Zhenghe Microchip are rapidly gaining traction, particularly in China’s booming smart home and industrial automation sectors. These regional specialists benefit from government support for domestic semiconductor production and tailored solutions for local market needs.

Recent developments show European firms such as Imec and Acconeer making strategic moves through academic collaborations and miniaturization breakthroughs. In June 2024, Imec announced a new 60GHz radar chip with 40% lower power consumption – a critical advancement for battery-powered IoT applications.

The competitive intensity is further heightened by emerging applications in healthcare and transportation. Companies are now focusing on developing application-specific chips rather than generic solutions, with Socionext and AKM recently introducing chips optimized for fall detection and crowd monitoring respectively.

List of Key 60GHz Millimeter Wave Radar Chip Companies

- Infineon Technologies (Germany)

- Texas Instruments (U.S.)

- Imec (Belgium)

- Dexin Intelligence (China)

- Acconeer (Sweden)

- Space Microelectronics (China)

- Zhenghe Microchip (China)

- Socionext (Japan)

- Catland (U.S.)

- Skerelli (South Korea)

- Anda (Taiwan)

- AKM (Japan)

Segment Analysis:

By Type

Distance Measurement Chip Segment Leads Due to Increasing Demand in Autonomous Vehicle Applications

The market is segmented based on type into:

- Distance Measurement Chip

- Subtypes: Short-range, Medium-range, Long-range

- Speed Measurement Chip

- Angle Measurement Chip

- Other

- Subtypes: Multi-function chips, Specialty chips

By Application

Automotive Sector Dominates the Market Due to Rising Adoption of ADAS Technologies

The market is segmented based on application into:

- Automotive

- Subtypes: Passenger vehicles, Commercial vehicles

- Transportation

- Industrial Automation

- Healthcare

- Other

- Subtypes: Consumer electronics, Smart home devices

By End User

OEMs Account for Significant Market Share Due to Direct Integration Requirements

The market is segmented based on end user into:

- Original Equipment Manufacturers (OEMs)

- Aftermarket Suppliers

- System Integrators

- Research Institutions

By Technology

MIMO Technology Gains Traction Due to Superior Detection Capabilities

The market is segmented based on technology into:

- Multiple Input Multiple Output (MIMO)

- Single Input Single Output (SISO)

- Phased Array

- Others

- Subtypes: Frequency-modulated continuous wave (FMCW), Ultra-wideband (UWB)

Regional Analysis: 60GHz Millimeter Wave Radar Chip Market

Asia-Pacific

As the leading region in the 60GHz millimeter wave radar chip market, Asia-Pacific is projected to maintain dominance, driven primarily by China’s rapidly expanding automotive and industrial automation sectors. The region accounted for over 45% of the global market share in 2024, with expected annual growth exceeding 28% through 2032. China’s strong semiconductor manufacturing ecosystem and government initiatives such as the “Made in China 2025” strategy are accelerating innovation in radar technologies. Japan and South Korea are also making significant advances in ADAS (Advanced Driver Assistance Systems) applications. However, cost pressures and intellectual property challenges create competitive hurdles for local manufacturers against global leaders.

North America

With major technology firms and automotive OEMs driving innovation, North America represents the second-largest market. The U.S. holds over 80% of regional revenue, supported by military R&D investments and private-sector collaborations addressing autonomous vehicle challenges. FCC regulatory approvals for higher-frequency applications have enabled rapid commercialization, with applications expanding into smart infrastructure and healthcare monitoring. Key players like Texas Instruments and Infineon Technologies are strengthening their 60GHz portfolios through specialized chipsets with enhanced power efficiency. High research costs and stringent certification processes, however, limit small-scale market entrants.

Europe

Europe’s focus on automotive safety standards (Euro NCAP) and Industry 4.0 adoption fuels steady demand for 60GHz radar chips. Germany leads with applications in industrial automation and premium vehicle manufacturing, supported by academic-industry partnerships in millimeter-wave research. The EU’s regulatory framework promotes spectrum harmonization, though complex compliance requirements slow time-to-market for new products. Manufacturers are prioritizing miniaturization and multi-function chips to address space constraints in smart factory equipment. Despite these advances, reliance on imported raw materials keeps production costs higher compared to Asian counterparts.

Middle East & Africa

This emerging market shows concentrated growth in UAE and Saudi Arabia, where smart city projects incorporate 60GHz radar for traffic management and security. While presently accounting for less than 5% of global sales, the region offers long-term potential with increasing foreign investments in tech infrastructure. Local players face technological gaps, relying heavily on imports from Europe and Asia. Governments are initiating R&D incentives to foster domestic semiconductor capabilities, though progress remains gradual due to limited specialized workforce and testing facilities.

South America

Brazil and Argentina are piloting industrial and automotive applications, but economic instability hinders large-scale adoption. Most demand comes from aftermarket vehicle safety systems, with price sensitivity favoring low-cost Asian imports over premium solutions. Some progress is evident in mining and agriculture automation, where radar chips enable equipment monitoring. Lack of local manufacturing and inconsistent regulatory policies continue to restrain market expansion, though trade agreements may improve technology access in coming years.

Report Scope

This market research report provides a comprehensive analysis of the Global 60GHz Millimeter Wave Radar Chip market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 146 million in 2024 and is projected to reach USD 714 million by 2032, growing at a CAGR of 25.7%.

- Segmentation Analysis: Detailed breakdown by product type (Distance Measurement Chip, Speed Measurement Chip, Angle Measurement Chip, Others), application (Automotive, Transportation, Industrial Automation, Healthcare, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis. Asia-Pacific dominates due to high adoption in automotive and industrial sectors.

- Competitive Landscape: Profiles of leading market participants, including Infineon Technologies, Texas Instruments, Imec, Acconeer, and Socionext, covering their product portfolios, R&D investments, and strategic partnerships.

- Technology Trends & Innovation: Assessment of AI/ML integration, miniaturization trends, advanced signal processing techniques, and evolving industry standards like IEEE 802.11ad.

- Market Drivers & Restraints: Analysis of factors such as autonomous vehicle adoption and smart city initiatives versus challenges like high development costs and regulatory hurdles.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, system integrators, OEMs, and investors regarding supply chain optimization and emerging opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified secondary data from regulatory bodies, company filings, and trade associations to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Global 60GHz Millimeter Wave Radar Chip Market?

-> 60GHz Millimeter Wave Radar Chip Market was valued at 146 million in 2024 and is projected to reach US$ 714 million by 2032, at a CAGR of 25.7% during the forecast period.

Which key companies operate in this market?

-> Key players include Infineon Technologies, Texas Instruments, Imec, Acconeer, Socionext, Dexin Intelligence, and AKM, among others.

What are the primary growth drivers?

-> Major drivers include rising ADAS adoption (projected 60% penetration in new vehicles by 2030), industrial automation growth (8.9% CAGR), and increasing smart home installations (2.5 billion devices expected by 2026).

Which application segment dominates?

-> Automotive applications accounted for 42% market share in 2024, followed by industrial automation at 28%.

What are the emerging technological trends?

-> Key trends include chipset miniaturization (below 5nm nodes), AI-powered signal processing, and multi-sensor fusion technologies enhancing detection accuracy beyond 200 meters.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...