3D IC Market Insights

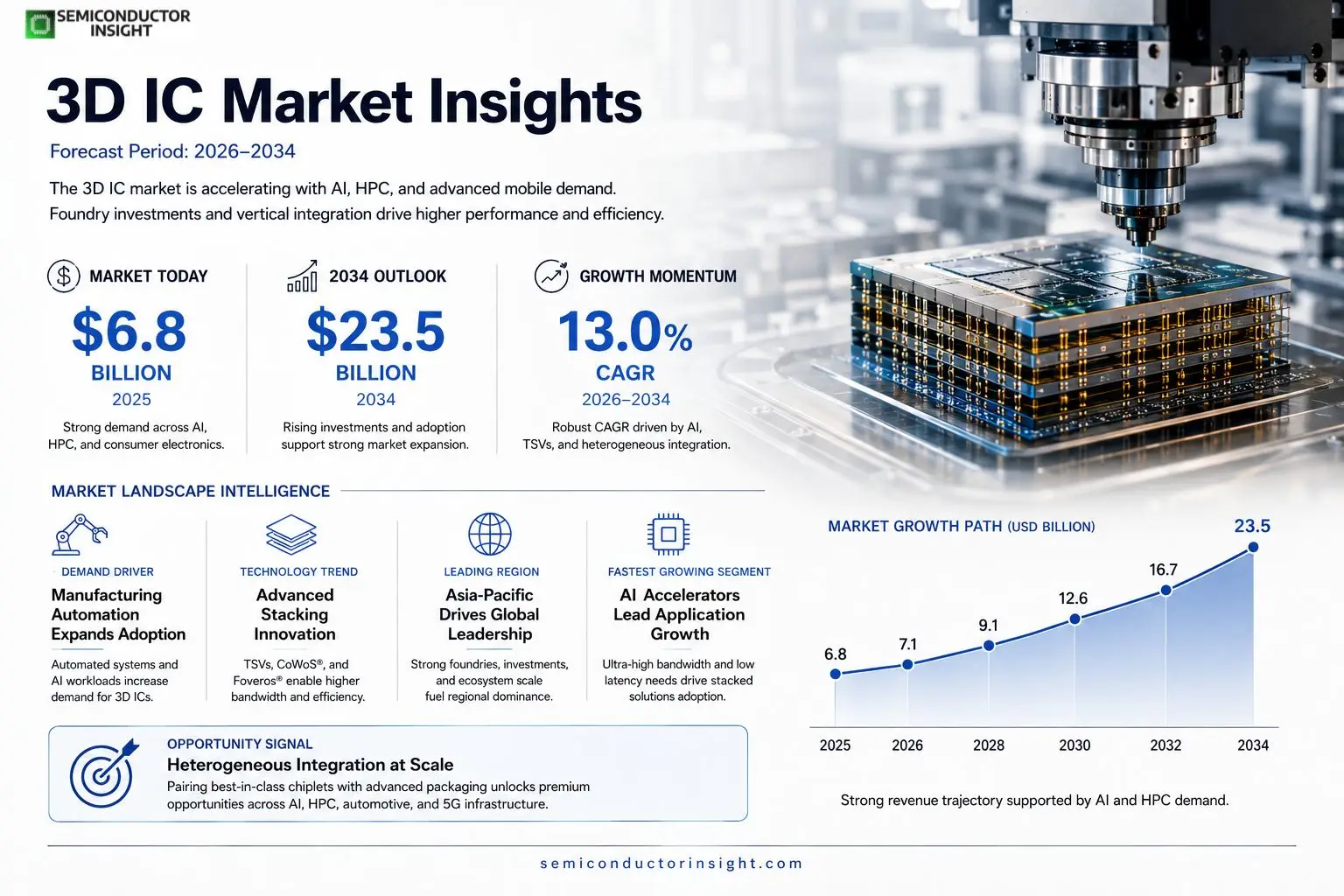

3D IC market size was valued at USD 6.8 billion in 2025. The market is projected to grow from USD 7.1 billion in 2026 to USD 23.5 billion by 2034, exhibiting a CAGR of 13.0% during the forecast period.

Three‑dimensional integrated circuits (3D ICs) are semiconductor devices that vertically stack multiple active layers (dies) interconnected through micro‑bumps or through‑silicon vias (TSVs). This architecture shortens interconnect length, improves signal integrity, and enables heterogeneous integration of logic, memory, and analog functions within a compact footprint.The market is experiencing rapid expansion because AI accelerators, high‑performance computing (HPC) servers, and advanced mobile platforms demand higher bandwidth and lower power consumption than traditional planar chips can provide.

Furthermore, ongoing investments by leading foundries such as TSMC, Intel, and Samsung Electronics, together with specialized packaging firms like ASE Group, are accelerating volume production of technologies such as CoWoS®, Foveros®, and X‑Band interposers.

Recent milestones,including TSMC’s Q1‑2024 launch of full‑scale N7+ CoWoS® services,underscore the momentum behind stacked solutions.

While cost considerations remain a challenge for low‑margin applications,

the convergence of AI workloads and edge computing continues to drive adoption across data centers and consumer electronics.

MARKET DRIVERS

Increasing Demand for Miniaturized Electronics

The rapid growth of smartphones, wearables, and IoT devices is pushing manufacturers to pack more functionality into smaller footprints. **3D IC Market** players are benefiting from this trend as vertical integration enables higher transistor density without enlarging the die area. Recent forecasts indicate that device form‑factor reduction alone could add over $2 billion to market revenue by 2027.

Advancements in Through‑Silicon Via (TSV) Technology

Improvements in TSV reliability and pitch have lowered defect rates, making 3D stacking economically viable for high‑performance computing. **Industry surveys** show that up to 45 % of leading semiconductor firms have incorporated TSV‑based designs into their roadmaps, driving a CAGR of roughly 12 % for the segment.

➤ 3D IC Market is being propelled forward by the convergence of heterogeneous integration and advanced packaging.

Beyond performance, cost efficiencies are emerging as yield optimization and shared substrate usage reduce material waste. Analysts expect these savings to translate into an additional $1.5 billion of profit margin expansion for top tier vendors by 2030.

MARKET CHALLENGES

Complexity of Manufacturing Processes

Building multi‑die stacks demands precise alignment, high‑temperature bonding, and stringent contamination control. The intricate workflow increases cycle time, and any deviation can lead to costly rework. Companies report that defect‑related losses can erode up to 8 % of projected revenue.

Other Challenges

High Capital Expenditure

Establishing dedicated 3D stacking lines requires investments exceeding $500 million, a barrier for medium‑size players. This capital intensity slows market entry and concentrates production among a few large fabs.Moreover, the limited availability of robust design‑for‑manufacturing (DFM) guidelines hampers rapid prototyping, extending time‑to‑market for new products.

MARKET RESTRAINTS

Limited Availability of Skilled Workforce

The specialized knowledge required for 3D integration,covering wafer‑level bonding, thermal analysis, and reliability testing,is scarce. Surveys indicate that only 30 % of engineering teams feel fully equipped to handle advanced stacking projects.Design‑tool maturity also lags behind traditional planar flows, forcing many designers to rely on custom scripts and manual verification steps, which further inflates development costs.Thermal management remains a technical restraint; as dies are stacked, heat dissipation paths become constrained, necessitating innovative cooling solutions that are still under commercial development.

MARKET OPPORTUNITIES

Emerging Applications in AI and Edge Computing

AI accelerators demand ultra‑high bandwidth and low latency, qualities inherent to 3D stacking. Integrating memory directly onto logic dies reduces data movement, delivering performance gains of up to 3× compared with conventional packages.Automotive electronics, especially advanced driver‑assistance systems (ADAS), are adopting 3D ICs to meet stringent size, weight, and power (SWaP) requirements while maintaining reliability under harsh conditions.Finally, the rollout of 5G infrastructure creates a need for compact, high‑throughput modules. 3D IC solutions enable antenna‑in‑package designs that can support the massive MIMO configurations essential for next‑generation networks.

3D IC Market Trends

AI‑Driven Demand for Stacked Silicon

Artificial‑intelligence accelerators and high‑performance computing workloads are reshaping semiconductor design priorities. By stacking active dies, designers achieve markedly shorter interconnect paths, reduced signal loss, and higher bandwidth per pin. This architectural advantage directly addresses the power‑efficiency constraints of modern data‑center processors and edge AI chips, creating a decisive shift toward vertically integrated solutions across both server and consumer segments.

Other Trends

Foundry Investments Accelerate Volume Production

Leading foundries such as TSMC, Intel, and Samsung have expanded capacity for advanced TSV and micro‑bump processes. Recent announcements include full‑scale services for N7+ CoWoS® and the introduction of new X‑Band interposers, signaling a move from pilot runs to regular high‑volume manufacturing. Packaging specialists like ASE Group are concurrently scaling their advanced fan‑out and interposer capabilities, reinforcing a supply chain that can meet the escalating demand for stacked silicon.

Cost Management and Heterogeneous Integration

While the performance upside is compelling, cost remains a critical barrier for price‑sensitive applications. Design teams are therefore emphasizing heterogeneous integration, pairing high‑end logic dies with lower‑cost memory or analog blocks on a single stack to amortize the expense of advanced packaging. This approach enables incremental adoption, allowing manufacturers to target premium segments first before extending the technology to broader markets.Overall, the trajectory of 3D IC Market reflects a convergence of AI workload intensity, robust foundry investment, and pragmatic cost strategies. The ecosystem’s ability to deliver scalable, power‑efficient solutions through vertical stacking is set to reinforce its role as a cornerstone of next‑generation semiconductor platforms.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive Dynamics in the 3D IC Market

3D IC Market is currently dominated by a few vertically integrated foundries that command the majority of volume production. TSMC leverages its CoWoS® platform to deliver high‑bandwidth interposers for AI accelerators, while Intel’s Foveros® technology enables heterogeneous stacking of logic and memory within its Xeon and Core families. Samsung Electronics complements these capabilities with X‑Band interposers and advanced TSV processes, securing a strong foothold in both mobile and high‑performance computing segments. Collectively, these three leaders shape pricing, roadmap timing, and ecosystem standards, creating a tiered structure where Tier‑1 fabs supply the bulk of high‑value chips and downstream packaging specialists add the final integration steps.Beyond the Tier‑1 giants, a growing cohort of specialized packaging and fabless companies adds depth to the competitive landscape. ASE Group, Amkor Technology, and JCET provide advanced packaging services that make 3D stacking economically viable for mid‑range customers. Foundries and STMicroelectronics pursue niche TSV lines for automotive and industrial applications. Meanwhile, NXP Semiconductors, Infineon Technologies, Sony Semiconductor Solutions, Qualcomm, and Broadcom focus on integrating 3D ICs into sensor modules, RF front‑ends, and communication silicon, driving diversification across the value chain. These players collectively expand market reach, foster innovation, and mitigate the cost barriers that can limit broader adoption of stacked architectures.

List of Key 3D IC Companies Profiled

- TSMC

- Intel

- Samsung Electronics

- ASE Group

- Amkor Technology

- JCET Group

- Foundries

- STMicroelectronics

- NXP Semiconductors

- Infineon Technologies

- Sony Semiconductor Solutions

- Qualcomm

- Broadcom

- Micron Technology

- Marvell Technology Group

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

TSV‑Based Stacking drives the market because it enables high‑density vertical interconnectivity, reduces signal loss, and supports heterogeneous integration of logic and memory.

|

| By Application |

|

AI Accelerators emerge as the leading application due to demanding bandwidth, low latency, and power‑efficiency needs.

|

| By End User |

|

Data Center Operators prioritize 3D ICs for the ability to sustain exponential growth in compute workloads while managing power budgets.

|

| By Integration Technology |

|

Chiplet Integration is gaining traction because it offers modularity and faster time‑to‑market.

|

| By Market Drivers |

|

Performance Demand underpins 3D IC Market as designers seek to break bandwidth bottlenecks inherent in planar architectures.

|

Regional Analysis: Asia-Pacific

Asia-Pacific

China’s substantial investments in its domestic semiconductor industry are driving significant growth in 3D IC Market. The government’s focus on self-sufficiency and technological independence is fostering innovation and attracting players to establish manufacturing and research facilities. The demand for 3D ICs in applications such as AI, high-performance computing, and automotive electronics is particularly strong.

Taiwan remains a leader in semiconductor manufacturing and design, holding a significant share in 3D IC Market. Its established ecosystem of leading foundries and fabless companies provides a strong foundation for innovation and production. The region’s expertise in advanced packaging technologies is a key driver of growth in 3D IC Market.

South Korea is another major player in 3D IC Market, with strong capabilities in memory chips, logic circuits, and advanced packaging. The country’s investments in research and development are focused on developing next-generation 3D IC technologies for applications in mobile devices, data centers, and automotive electronics.

Japan possesses a rich history in semiconductor innovation and continues to play a significant role in 3D IC Market. Its strengths lie in advanced packaging technologies, high-performance logic circuits, and automotive electronics applications. Collaboration between industry, academia, and government is driving the development of cutting-edge 3D IC solutions.

North America

North America represents a stable and mature market for 3D ICs, with significant demand from the aerospace, defense, and automotive sectors. The region is witnessing increased adoption of 3D ICs in high-performance computing and data centers. Key players are focusing on developing advanced packaging technologies and heterogeneous integration solutions. The focus is on specialized applications requiring high reliability and performance.

Europe

Europe’s 3D IC market is gradually gaining traction, driven by growing demand from the automotive and industrial sectors. Investments in research and development are focusing on energy-efficient 3D ICs for applications in electric vehicles and smart manufacturing. Collaborative initiatives between European companies and research institutions are fostering innovation in 3D IC technologies.

South America

South America represents a relatively nascent market for 3D ICs, with potential growth driven by the expanding telecommunications and industrial sectors. The adoption of 3D ICs is expected to increase with the growth of IoT and 5G connectivity. Government initiatives aimed at promoting technological development are creating a favorable environment for 3D IC Market.

Middle East & Africa

The Middle East & Africa region presents a growing opportunity for 3D IC Market, driven by increasing investments in infrastructure development and the expansion of the telecommunications sector. The adoption of 3D ICs in automotive, industrial, and consumer electronics applications is expected to drive market growth. The region’s focus on smart city initiatives is also creating demand for advanced 3D IC solutions.

Report Scope

This market research report provides a comprehensive analysis of the 3D IC Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of 3D IC Market?

-> 3D IC Market was valued at USD 6.8 billion in 2025 and is expected to reach USD 23.5 billion by 2034.

Which key companies operate in 3D IC Market?

-> Key players include TSMC, Intel, Samsung Electronics, ASE Group, among others.

What are the key growth drivers?

-> Key growth drivers include AI accelerators, high‑performance computing (HPC) servers, advanced mobile platforms, and the convergence of AI workloads with edge computing.

Which region dominates the market?

-> The reference does not specify a single dominant region; growth is driven ly with significant activity in regions hosting major foundries such as Asia‑Pacific.

What are the emerging trends?

-> Emerging trends include advanced stacking technologies like CoWoS®, Foveros®, X‑Band interposers, and broader adoption of through‑silicon vias (TSVs) for heterogeneous integration.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...