MARKET INSIGHTS

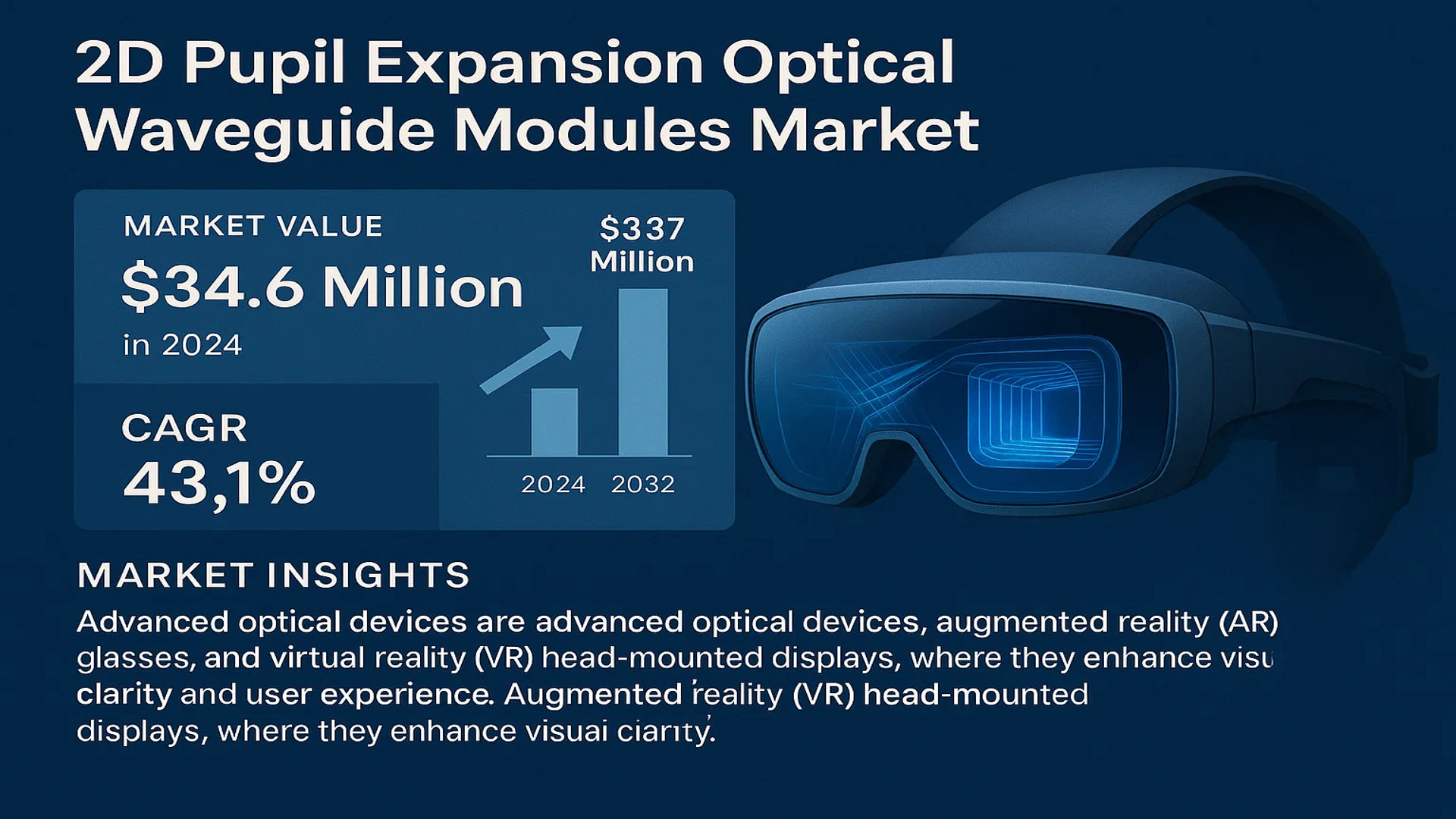

The global 2D Pupil Expansion Optical Waveguide Modules Market was valued at 34.6 million in 2024 and is projected to reach US$ 337 million by 2032, at a CAGR of 43.1% during the forecast period.

2D Pupil Expansion Optical Waveguide Modules are advanced optical devices consisting of multiple waveguide units arranged in a two-dimensional array to achieve efficient pupil expansion of optical signals. These modules leverage waveguide technology to provide superior energy utilization, high-quality display performance, and robust environmental adaptability. They are increasingly being adopted in augmented reality (AR) glasses and virtual reality (VR) head-mounted displays, where they enhance visual clarity and user experience.

The market is experiencing significant growth due to rising demand for AR/VR applications in consumer electronics and industrial sectors. The U.S. market is estimated to account for approximately 35% of global revenue in 2024, while China is emerging as a fast-growing market due to increasing local manufacturing capabilities. Key players such as Lumus, Optinvent, and Shanghai Lipai Optical Crystal Technology are driving innovation through strategic partnerships and product enhancements, further accelerating market expansion. The resin-based waveguide segment is expected to show strong growth, supported by its cost-effectiveness and manufacturing scalability.

MARKET DRIVERS

Rapid Expansion of AR/VR Technologies Accelerates Market Adoption

The global AR/VR market growth is serving as a key catalyst for 2D pupil expansion waveguide modules, with headset shipments projected to exceed 50 million units annually by 2025. As display resolutions improve and form factors shrink, waveguide technology has emerged as the preferred optical solution for next-generation wearable devices. The technology’s ability to provide wide field-of-view (typically 40°-60°) while maintaining compact dimensions gives it significant advantages over traditional optical systems. Major tech companies have invested over $10 billion in AR/VR development since 2020, with waveguide displays becoming a focal point of this investment.

Growing Military and Industrial Applications Fuel Market Demand

Beyond consumer electronics, defense sectors across North America and Asia-Pacific are driving adoption of waveguide-based Head-Mounted Displays (HMDs) for training and operational applications. The U.S. military alone has allocated more than $1.2 billion for AR-based systems in its 2024 budget, with waveguide technology being specified for multiple next-generation projects. Industrial applications are also growing at a 38% CAGR as manufacturers implement augmented reality for maintenance, assembly, and quality control processes where the waveguide’s durability and optical clarity provide operational advantages.

Technological Advancements in Waveguide Manufacturing Enhance Viability

Recent breakthroughs in nanoimprint lithography and glass molding techniques have reduced waveguide production costs by approximately 40% since 2022 while improving optical performance. The shift from traditional photolithography to these mass production methods enables manufacturers to achieve yields above 85%, making the technology commercially viable for consumer applications. Leading suppliers have demonstrated waveguide modules with optical efficiencies exceeding 2500 nits/lumen, a critical threshold for daylight-readable AR displays.

MARKET RESTRAINTS

High Manufacturing Complexity Limits Production Scalability

Despite advancements, waveguide manufacturing remains technically challenging due to the precision required for micro-optical structures typically measuring between 300-500nm. Current production methods often require specialized cleanroom facilities with sub-micron alignment capabilities, creating capital expenditure barriers exceeding $50 million for new fabrication lines. Yield rates for complex multi-layer waveguide designs remain below 60% at most facilities, significantly impacting unit economics at scale.

Other Constraints

Material Limitations

Available optical polymer and high-index glass materials still exhibit tradeoffs between refractive index (typically 1.5-1.7), thermal stability, and optical losses. Current materials demonstrate approximately 15% light loss per waveguide layer, limiting the practical number of expansion stages and ultimately restricting field-of-view.

Thermal Management Challenges

Waveguide modules in active AR systems generate localized heating exceeding 60°C during continuous operation. This thermal load can induce birefringence changes in optical materials, degrading image quality and necessitating complex thermal compensation designs that add cost and weight.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impact Critical Component Availability

The waveguide ecosystem relies on specialized materials and components from concentrated supply bases, with over 70% of high-index glass production originating from three suppliers globally. Recent geopolitical tensions have exposed vulnerabilities in this supply chain, with lead times for certain optical substrates extending beyond 12 months. Alternative materials development remains constrained by intellectual property barriers, as over 1,200 active patents cover core waveguide technologies.

Other Challenges

Standardization Deficits

The absence of industry-wide performance metrics and testing protocols creates integration challenges for OEMs. Currently, there are over 15 competing waveguide architectures in development, each with unique optical interfaces and performance characteristics that complicate system design.

Talent Shortages

Specialized optical engineers with waveguide expertise remain scarce, with industry estimates suggesting a global shortage exceeding 2,000 qualified professionals. Educational programs have been slow to adapt, with fewer than 20 universities worldwide offering dedicated coursework in diffractive optics.

MARKET OPPORTUNITIES

Emerging Automotive HUD Applications Present New Growth Frontier

The automotive Heads-Up Display (HUD) market represents a significant expansion opportunity, with waveguide-based augmented reality HUDs expected to capture over 30% of the premium vehicle segment by 2027. These systems require advanced pupil expansion techniques to achieve the large eyebox demanded by automotive applications. Recent demonstrations have shown waveguide AR-HUDs capable of 15° field-of-view with 10m virtual image distance, meeting critical automotive safety requirements.

Medical Imaging and Surgical Navigation Open New Verticals

Healthcare applications are emerging as high-value opportunities, with waveguide displays enabling novel augmented reality solutions for surgical navigation and medical training. The technology’s ability to superimpose high-resolution 3D imagery directly in the surgeon’s field of view has demonstrated measurable improvements in procedure accuracy. Early clinical studies show AR-guided surgeries can reduce operation times by 18-22% while decreasing complication rates, driving adoption in neurosurgery and orthopedic applications.

Advancements in Metaverse Technologies Create Complementary Demand

As metaverse platforms evolve beyond traditional VR, hybrid AR/VR systems utilizing waveguide optics are gaining traction. These transitional devices require the compact form factor and high transparency of waveguide displays to blend digital content with real-world environments seamlessly. Industry projections indicate the metaverse hardware market could require over 5 million waveguide display units annually by 2026 as next-generation mixed reality headsets enter mass production.

2D PUPIL EXPANSION OPTICAL WAVEGUIDE MODULES MARKET TRENDS

Rising Demand for AR/VR Devices Driving Market Growth

The global 2D Pupil Expansion Optical Waveguide Modules Market is experiencing significant growth due to increasing adoption in augmented reality (AR) and virtual reality (VR) applications. With AR headsets projected to reach 30 million units by 2025, manufacturers are heavily investing in waveguide technology to enable lightweight, high-resolution displays. Major tech companies have already incorporated waveguide-based displays in their latest mixed reality devices, pushing the market toward a projected valuation of $337 million by 2032. The technology’s ability to expand the exit pupil while minimizing optical aberrations makes it ideal for next-generation wearables.

Other Trends

Material Innovations in Waveguide Manufacturing

Material science breakthroughs are enabling thinner, more durable waveguide modules with improved optical clarity. While glass waveguides currently dominate with over 65% market share, advanced resin composites are gaining traction due to their flexibility and cost-effectiveness. Recent developments in nano-imprinting lithography have further enhanced resin waveguide performance, closing the optical quality gap with traditional glass solutions. This diversification of material options allows manufacturers to optimize modules for different applications, from consumer electronics to medical devices.

Technological Advancements in Optical Design

The market is witnessing rapid innovation in geometric phase optics and holographic waveguide technologies, significantly improving light efficiency and field-of-view capabilities. Recent product launches demonstrate Field-of-View (FoV) improvements from 30° to over 50°, meeting the demands of increasingly sophisticated AR applications. The integration of diffractive optical elements with traditional refractive designs has emerged as a key approach to balancing performance with manufacturing scalability. Furthermore, AI-assisted optical simulations are reducing development cycles by 40-60%, accelerating time-to-market for new waveguide solutions.

Expansion into Industrial and Medical Applications

While consumer electronics remain the dominant application, accounting for approximately 58% of 2024 revenues, industrial and medical sectors are emerging as high-growth areas. In medical applications, waveguide modules enable advanced surgical navigation systems with heads-up displays, while industrial implementations facilitate hands-free maintenance and repair procedures. The sector’s growth is further supported by increasing adoption in defense and aerospace, where ruggedized waveguide displays enhance situational awareness in challenging environments.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Competition in the 2D Pupil Expansion Waveguide Market

The global 2D Pupil Expansion Optical Waveguide Modules market exhibits a fragmented yet competitive landscape, characterized by both established optical technology providers and emerging specialized manufacturers. Lumus has emerged as a dominant force in AR/VR waveguide technology, leveraging its proprietary reflective waveguide designs that capture approximately 25% of the high-end AR smart glasses market as of 2024. Their success stems from strategic partnerships with major tech companies and continuous refinement of their light-guide optical element (LOE) technology.

Meanwhile, Optinvent has gained significant traction through its circular polarized light waveguide solutions, particularly in industrial AR applications. The company’s patented technology has enabled them to secure contracts with several Fortune 500 manufacturers, demonstrating the growing industrial demand for waveguide-based displays. Their multi-layer optical waveguide architecture achieves over 85% light efficiency, a key differentiator in this performance-driven market.

Chinese manufacturers like Shanghai Lipai Optical Crystal Technology and Beijing Nai Dejia Display Technology are rapidly expanding their market presence through aggressive pricing strategies and government-supported R&D initiatives. Combined, these companies now account for nearly 40% of Asia-Pacific shipments, benefiting from strong domestic demand and expanding overseas distribution networks.

The competitive intensity is further heightened by vertical integration strategies. Companies such as LINGXI have begun producing both waveguides and complementary optical components in-house, reducing dependency on suppliers and improving margins. This trend suggests the market is evolving toward more consolidated supply chains, with leading players aiming to control multiple stages of the value chain.

Looking forward, the competitive dynamics will likely shift as key patents expire and manufacturing processes mature. Multiple companies are investing in nanoimprint lithography techniques that promise to reduce production costs by up to 60% for volume manufacturing. This technological evolution may reshape the competitive hierarchy within the next 3-5 years.

List of Key 2D Pupil Expansion Waveguide Companies Profiled

- Lumus (Israel)

- Optinvent (France)

- Shanghai Lipai Optical Crystal Technology (China)

- Lohn Optics (Germany)

- LINGXI (China)

- Gudong Technology (China)

- OPTIX (South Korea)

- Beijing Nai Dejia Display Technology (China)

Segment Analysis:

By Type

Resin Segment Leads the Market Due to Its Lightweight and Cost-Effective Properties in AR/VR Applications

The market is segmented based on material type into:

- Resin

- Glass

By Application

Consumer Electronics Segment Dominates with Increasing Adoption in AR/VR Headsets and Smart Glasses

The market is segmented based on application into:

- Consumer Electronics

- Industrial Manufacturing

- Advanced Medical

- Others

By Technology

Waveguide Array Technology Holds Significant Potential for Future Growth

The market is segmented based on technology into:

- Diffractive Waveguide

- Reflective Waveguide

- Holographic Waveguide

- Waveguide Array

By End-User

Commercial Sector Accounts for Major Share Due to Expanding AR Retail Applications

The market is segmented based on end-user into:

- Commercial

- Industrial

- Healthcare

- Military & Defense

Regional Analysis: 2D Pupil Expansion Optical Waveguide Modules Market

Asia-Pacific

The Asia-Pacific region leads the 2D Pupil Expansion Optical Waveguide Modules market, driven primarily by China’s dominance in AR/VR technology manufacturing and adoption. With major manufacturers like Shanghai Lipai Optical Crystal Technology and Gudong Technology headquartered here, the region benefits from strong R&D investments and government support for next-gen display technologies. China alone is projected to account for over 40% of global production by 2032. Japan and South Korea contribute specialized glass waveguide manufacturing expertise, while Southeast Asia provides cost-effective manufacturing hubs. The consumer electronics sector, particularly AR smart glasses, accounts for 65% of regional demand, with industrial and medical applications growing at 30% CAGR.

North America

North America remains the innovation hub for waveguide technologies, with California-based Lumus securing multiple patents for pupil expansion architectures. The U.S. Department of Defense has allocated $150 million for waveguide-based heads-up displays, driving specialized military applications. Silicon Valley’s AR startups and tech giants are collaborating with module manufacturers to develop consumer-grade AR glasses, fueling 50% year-on-year demand growth since 2022. Canada’s OPTIX has emerged as a leader in resin-based waveguide modules, capturing 15% of the North American professional AR headset market. Regulatory focus on optical safety standards creates both challenges and quality benchmarks for manufacturers.

Europe

Europe demonstrates steady growth in waveguide adoption, particularly for industrial AR applications in Germany’s manufacturing sector and medical imaging in Scandinavia. The EU’s Horizon Europe program has funded 28 research projects involving waveguide optics since 2021, fostering academic-commercial partnerships. France’s Optinvent holds key patents for compact waveguide designs used in aviation HUDs. While the market grows at 38% CAGR, higher production costs compared to Asian manufacturers limit mass-market penetration. Regulatory requirements under CE marking ensure waveguide products meet stringent optical performance standards, creating a quality-conscious but slower-moving market.

South America

South America represents an emerging market where lower-cost Chinese waveguide modules dominate, accounting for 80% of imports. Brazil shows potential as a future manufacturing base, with tax incentives attracting foreign waveguide technology investment. However, limited local R&D capabilities and infrastructure challenges constrain market growth to 18-20% annually. Medical applications show strongest growth as hospitals adopt AR-assisted surgical systems. Economic volatility creates irregular demand patterns, making the region a secondary priority for major manufacturers.

Middle East & Africa

The MEA region shows niche demand concentrated in oil/gas and defense sectors, where waveguide-based monitoring systems are gaining traction. UAE’s technology free zones have attracted waveguide module distributors serving the Arabian Gulf markets. Israel’s Lumus maintains technology partnerships with local military contractors. While overall adoption remains low, the high-value application segments support premium pricing. Infrastructure limitations and low local manufacturing capacity mean the region will likely remain an import-dependent market through 2030.

Report Scope

This market research report provides a comprehensive analysis of the Global 2D Pupil Expansion Optical Waveguide Modules Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 34.6 million in 2024 and is projected to reach USD 337 million by 2032, growing at a CAGR of 43.1%.

- Segmentation Analysis: Detailed breakdown by product type (Resin, Glass), application (Consumer Electronics, Industrial Manufacturing, Advanced Medical, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key markets, with Asia-Pacific expected to exhibit the highest growth.

- Competitive Landscape: Profiles of leading market participants, including Lumus, Optinvent, Shanghai Lipai Optical Crystal Technology, Lohn Optics, and LINGXI, covering their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in augmented reality (AR) and virtual reality (VR) applications, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth, such as rising demand for AR/VR devices, along with challenges like high production costs and supply chain constraints.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 2D Pupil Expansion Optical Waveguide Modules Market?

->2D Pupil Expansion Optical Waveguide Modules Market was valued at 34.6 million in 2024 and is projected to reach US$ 337 million by 2032, at a CAGR of 43.1% during the forecast period.

Which key companies operate in Global 2D Pupil Expansion Optical Waveguide Modules Market?

-> Key players include Lumus, Optinvent, Shanghai Lipai Optical Crystal Technology, Lohn Optics, LINGXI, Gudong Technology, OPTIX, and Beijing Nai Dejia Display Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for AR/VR devices, advancements in waveguide technology, and increasing adoption in consumer electronics and industrial applications.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by China’s expanding AR/VR industry, while North America remains a key market due to technological advancements.

What are the emerging trends?

-> Emerging trends include miniaturization of waveguide modules, integration with AI-powered devices, and increasing focus on lightweight and durable materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...