MARKET INSIGHTS

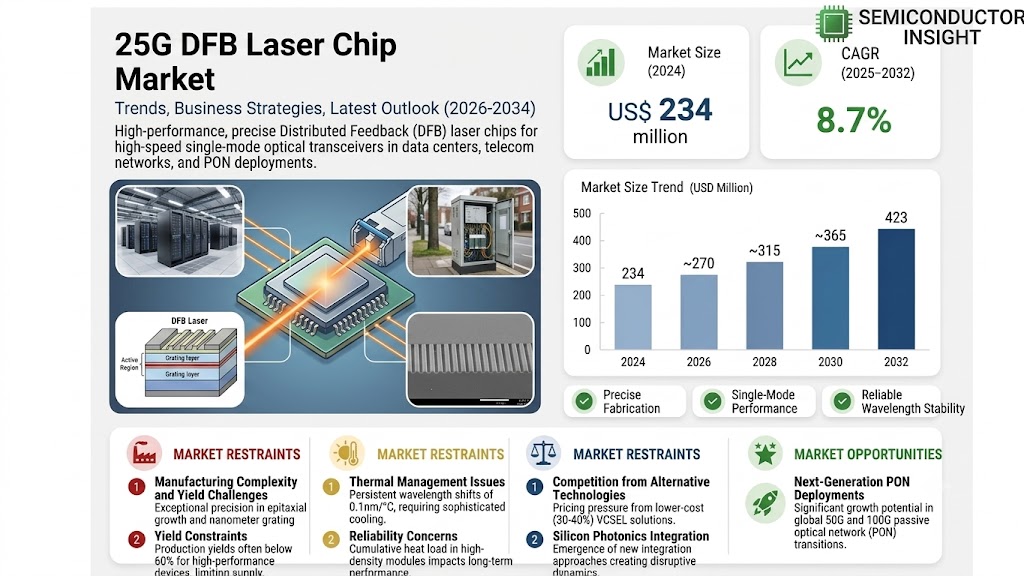

The global 25G DFB Laser Chip Market size was valued at US$ 234 million in 2024 and is projected to reach US$ 423 million by 2032, at a CAGR of 8.7% during the forecast period 2025-2032. This growth aligns with broader semiconductor industry trends, which saw the global market reach USD 579 billion in 2022 and is expected to grow to USD 790 billion by 2029 at 6% CAGR.

25G DFB (Distributed Feedback) Laser Chips are semiconductor devices that generate coherent optical signals at 25 gigabits per second, primarily used in high-speed data transmission applications. These chips feature a built-in Bragg grating structure that enables single-mode operation with narrow spectral width, making them ideal for 5G fronthaul networks and data center interconnects. Key variants include LWDM, CWDM, and MWDM configurations tailored for different wavelength division multiplexing applications.

The market is being propelled by the global rollout of 5G networks, which requires high-performance optical components for fronthaul and midhaul connections. Data center expansion is another major driver, with hyperscale operators deploying 25G optical transceivers for server connectivity. While demand is strong, supply chain challenges for semiconductor materials and geopolitical factors affecting the photonics industry present temporary headwinds. Leading players like Lumentum and II-VI Incorporated are investing in production capacity expansions to meet growing demand, particularly in Asia-Pacific markets where 5G deployment is most aggressive.

MARKET DYNAMICS

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth in 5G Infrastructure Deployment Accelerating Demand

The global rollout of 5G networks is creating unprecedented demand for 25G DFB laser chips, which serve as critical components in optical communication systems. With over 300 commercial 5G networks deployed worldwide as of 2024, telecom operators are heavily investing in fronthaul and backhaul infrastructure requiring high-speed optical transceivers. The transition from 10G to 25G solutions is accelerating due to 5G’s need for lower latency and higher bandwidth, with data rates projected to exceed 100G in coming years. This technological migration is forcing network equipment providers to adopt advanced optical components that can support next-generation architectures while maintaining cost efficiency.

Surge in Hyperscale Data Center Expansion Fueling Adoption

Hyperscale data centers are driving significant demand for 25G DFB laser chips to support their massive interconnect requirements. With cloud computing workloads growing at over 20% annually, major providers are deploying optical links that leverage these components for high-density, energy-efficient interconnects. The transition from 10G to 25G interfaces is particularly evident in leaf-spine architectures where these laser chips enable cost-effective scaling of data center fabrics. Furthermore, the rise of AI and machine learning applications is creating additional demand for high-speed optical interconnects capable of supporting distributed computing workflows across server clusters.

Advancements in DWDM Technology Creating New Applications

The development of dense wavelength division multiplexing (DWDM) systems utilizing 25G DFB laser chips is opening new market opportunities. Recent technological breakthroughs have enabled channel spacing reductions below 100GHz, allowing more wavelengths to be packed into existing fiber infrastructure. This is particularly valuable for metro and long-haul applications where operators need to maximize fiber utilization. The integration of tunable DFB lasers is further enhancing network flexibility, enabling dynamic wavelength allocation and reducing inventory requirements for service providers. These innovations are extending the applicability of 25G solutions beyond traditional datacom into telecom transport networks.

MARKET RESTRAINTS

Manufacturing Complexity and Yield Challenges Limiting Supply

The production of 25G DFB laser chips faces significant technical hurdles that constrain market expansion. These components require exceptionally precise fabrication processes, with typical production yields for high-performance devices often below 60% for new production lines. The epitaxial growth of semiconductor layers demands nanometer-scale precision to achieve the required performance characteristics, making the manufacturing process both capital-intensive and technologically challenging. Furthermore, wafer-level testing and binning processes add to production costs, particularly for wavelength-specific applications where tight parameter controls are essential.

Thermal Management Issues Impacting Performance Reliability

Thermal sensitivity poses a persistent challenge for 25G DFB laser chip adoption in harsh operating environments. These devices typically experience wavelength shifts of 0.1nm/°C, requiring sophisticated temperature control mechanisms in final modules. In high-density applications such as data center interconnects, the cumulative heat load from multiple transceivers can push thermal management systems to their limits. This not only increases system complexity but also raises concerns about long-term reliability, particularly in outdoor deployments where ambient temperature variations are significant. These thermal considerations are forcing design compromises that sometimes limit performance parameters or increase form factor requirements.

Competition from Alternative Technologies Creating Pricing Pressure

The emergence of viable alternative technologies is constraining pricing power in the 25G DFB laser chip market. Vertical-cavity surface-emitting lasers (VCSELs) have made significant performance strides, achieving data rates up to 50G per channel in some configurations. While DFB lasers maintain advantages in single-mode applications, the cost differential versus VCSEL solutions (typically 30-40% lower) is forcing DFB chip manufacturers to aggressively reduce prices. Additionally, silicon photonics integration approaches are creating new competitive dynamics that could potentially disrupt traditional III-V semiconductor laser markets in certain applications.

MARKET OPPORTUNITIES

Next-Generation PON Deployments Offering Significant Growth Potential

The global transition to 50G and 100G passive optical networks (PON) is creating substantial opportunities for 25G DFB laser chip suppliers. Major telecom operators have begun trialing next-generation PON architectures that utilize multiple 25G wavelengths to achieve higher aggregate capacities. This evolution requires DFB lasers with exceptional linearity and low noise characteristics to support the analog nature of PON transmission. With fiber-to-the-home penetration approaching 60% in some markets, the upgrade cycle for existing GPON networks represents a multi-billion dollar opportunity that will drive demand for high-performance optical components through the next decade.

Emerging Co-Packaged Optics Applications Creating New Design Wins

The development of co-packaged optics architectures is opening new application spaces for 25G DFB laser chips. Leading cloud providers are actively exploring optical I/O solutions that move photonics closer to processing elements, with some prototype systems demonstrating power reductions exceeding 30% compared to traditional pluggable transceivers. These implementations often utilize arrays of 25G lasers integrated directly with switching ASICs, demanding unprecedented levels of miniaturization and thermal efficiency. The transition to co-packaging requires tight collaboration between laser chip suppliers and semiconductor manufacturers, creating opportunities for companies that can deliver customized solutions meeting exacting performance specifications.

Automotive LiDAR Applications Presenting Diversification Potential

The rapidly evolving automotive LiDAR market is emerging as an unexpected but promising opportunity for 25G DFB laser technology. While most current systems use pulsed lasers for time-of-flight measurements, frequency-modulated continuous-wave (FMCW) LiDAR approaches are gaining traction due to their superior velocity measurement capabilities. These systems often utilize DFB lasers operating in the 1550nm window, requiring similar performance characteristics as telecom-grade devices but with additional emphasis on linearity and frequency stability. With autonomous vehicle development accelerating, this niche application could become a significant market segment for specialized 25G DFB laser products.

25G DFB LASER CHIP MARKET TRENDS

5G Infrastructure Expansion Driving Demand for High-Speed Optical Components

The rapid global rollout of 5G networks continues to be the primary growth driver for 25G DFB (Distributed Feedback) laser chips. These chips serve as critical components in optical modules for fronthaul and midhaul 5G networks, enabling high-speed data transmission with low latency. Recent data shows that 5G network deployments increased by over 35% year-over-year in 2023, with China, North America, and Europe leading adoption. Network operators require reliable 25G DFB chips to meet the increasing bandwidth demands of 5G applications while maintaining signal integrity over longer distances. Furthermore, integration with small cell deployments and cloud-RAN architectures has created new opportunities for component suppliers.

Other Trends

Data Center Optical Interconnect Evolution

The evolution of hyperscale data center architectures toward higher-speed interconnects continues to stimulate demand for 25G DFB laser chips. Modern data centers now prioritize energy-efficient optical transceivers capable of handling increasing workloads from AI/ML applications and cloud computing. The transition from 100G to 400G Ethernet standards has created sustained demand for 25G-based solutions, as they serve as building blocks for higher-speed optical modules. Research indicates that data center optical component spending grew by approximately 14% in the past year, with 25G DFB chips remaining fundamental for both short-reach and long-reach applications.

Technological Advancements in Laser Production

Manufacturers are focusing on improving production yields and power efficiency of 25G DFB lasers to address industry requirements. Recent developments include the adoption of advanced epitaxial growth techniques and wafer-level testing methodologies to enhance consistency and reduce costs. The industry is also seeing increased investment in indium phosphide (InP) based laser production, which offers superior performance characteristics for high-speed applications. While 25G technology remains a workhorse for current deployments, research into next-generation solutions continues to push the boundaries of modulation efficiency and thermal stability.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define Market Leadership in 25G DFB Laser Chips

The global 25G DFB Laser Chip market is characterized by intense competition among established semiconductor players and specialized optoelectronics manufacturers. The landscape remains semi-consolidated, with top players collectively holding approximately 60-65% market share in 2024, while emerging regional competitors continue to gain traction through cost-competitive solutions. Lumentum Holdings and II-VI Incorporated (now Coherent Corp) currently lead the sector, leveraging their vertically integrated manufacturing capabilities and strong R&D pipelines for high-speed optical components.

Recent industry analysis shows that Chinese manufacturers like Yuanjie Semiconductor Technology and Wuhan Mind Semiconductor are rapidly closing the technology gap, having captured nearly 30% of the Asia-Pacific market through aggressive pricing strategies and government-supported semiconductor initiatives. This regional competition is forcing global players to accelerate innovation cycles while maintaining stringent quality standards required for telecom infrastructure deployments.

Market leaders are actively pursuing three key strategies to maintain dominance: 1) Development of next-generation LWDM and MWDM chips for 5G fronthaul networks 2) Strategic partnerships with datacenter operators for customized solutions 3) Expansion of production capacity in Southeast Asia to mitigate geopolitical risks. These initiatives come as the industry anticipates 40% growth in demand for 25G DFB chips from hyperscale data centers between 2024-2027.

Notably, Sumitomo Electric Industries has strengthened its market position through the acquisition of several optical component startups, while Broadcom continues to dominate the high-performance segment through its advanced packaging technologies. Smaller players like Ningbo ORI CHIP are finding success by focusing on niche applications in industrial fiber sensing and medical laser systems.

List of Key 25G DFB Laser Chip Companies Profiled

- Lumentum Holdings Inc. (U.S.)

- II-VI Incorporated (Coherent Corp) (U.S.)

- Sumitomo Electric Industries (Japan)

- Broadcom Inc. (U.S.)

- Yuanjie Semiconductor Technology (China)

- Wuhan Mind Semiconductor (China)

- Wuhan Eliteoptronics (China)

- Henan Shijia Photons (China)

- SANAN Optoelectronics (China)

- Ningbo ORI CHIP (China)

- GLSUN (China)

- MACOM Technology Solutions (U.S.)

- LuxNet Corp (Taiwan)

Segment Analysis:

By Type

LWDM DFB Laser Chip Dominates Due to High Efficiency in 5G and Data Centers

The market is segmented based on type into:

- LWDM DFB Laser Chip

- CWDM DFB Laser Chip

- MWDM DFB Laser Chip

By Application

5G Communication Network Segment Leads Owing to Global Infrastructure Expansion

The market is segmented based on application into:

- 5G Communication Network

- Data Center

By Wavelength

1310nm Wavelength Holds Major Share Due to Optimal Performance in Fiber Optic Communication

The market is segmented based on wavelength into:

- 1310nm

- 1550nm

- Others

By End User

Telecom Operators Drive Demand for High-Speed Data Transmission Solutions

The market is segmented based on end user into:

- Telecom Operators

- Cloud Service Providers

- Enterprises

Regional Analysis: 25G DFB Laser Chip Market

North America

The North American 25G DFB laser chip market is characterized by high technological adoption and significant investments in 5G infrastructure. The U.S. leads in deploying 5G networks, with telecom giants investing heavily in fiber-optic backhaul networks to support high-speed data transmission. Major players like Lumentum and II-VI Incorporated dominate the supply chain, leveraging their expertise in semiconductor lasers. While the market is mature, demand remains strong due to growing data center expansion and cloud computing needs—key drivers for 25G DFB laser chips. Regulatory support for open RAN (Radio Access Network) architectures is further accelerating adoption, though supply chain constraints and trade restrictions on advanced semiconductors pose challenges.

Europe

Europe’s 25G DFB laser chip market is driven by 5G rollouts and increasing data center investments, particularly in Germany, France, and the U.K. The EU’s Digital Compass initiative, aimed at achieving 100% 5G coverage by 2030, is a significant growth catalyst. Telecom operators like Vodafone and Deutsche Telekom are expanding their optical networks, fueling demand for high-performance laser chips. However, dependency on imports from Asian suppliers remains a bottleneck. Local manufacturers are ramping up production but still lag behind China and the U.S. in terms of technological self-sufficiency. Sustainability concerns and carbon-neutral manufacturing mandates are pushing European suppliers toward eco-friendly semiconductor fabrication.

Asia-Pacific

The largest and fastest-growing market for 25G DFB laser chips, Asia-Pacific, is propelled by China’s aggressive 5G deployment and India’s expanding telecom sector. China holds over 60% of global fiber-optic network capacity, with domestic players like Yuanjie Semiconductor and Wuhan Mind Semiconductor leading production. Japan and South Korea contribute through precision manufacturing and optical communication innovations. Cost competitiveness and high-volume production capabilities make this region a hub for DFB laser chip exports, though supply chain vulnerabilities persist due to geopolitical tensions. Rising demand from Southeast Asian data center markets further drives growth.

South America

A nascent but promising market, South America is gradually adopting 25G DFB laser technology due to limited 5G penetration and budget constraints. Brazil and Argentina are the primary markets, with government-led telecom projects slowly integrating optical components. However, economic instability and limited local semiconductor manufacturing hinder large-scale adoption. The region largely depends on imports from the U.S. and China, though growing data center investments by global tech firms suggest future potential.

Middle East & Africa

The market here is emerging but fragmented, with Gulf nations like UAE and Saudi Arabia leading due to smart city initiatives and 5G pilot projects. African adoption lags, though undersea cable expansions and fiber-to-the-home (FTTH) projects are creating demand. The lack of local semiconductor production forces reliance on imports, and high deployment costs deter widespread adoption. Still, partnerships with global telecom providers are accelerating infrastructure development, offering long-term opportunities for 25G DFB laser chip suppliers.

Report Scope

This market research report provides a comprehensive analysis of the Global 25G DFB Laser Chip market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global 25G DFB Laser Chip market was valued at US$ 234 million in 2024 and is projected to reach US$ 423 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (LWDM, CWDM, MWDM DFB Laser Chips) and application (5G Communication Network, Data Center) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific currently dominates the market with China as a key manufacturing hub.

- Competitive Landscape: Profiles of leading market participants including Sumitomo Electric Industries, Lumentum, and II-VI Incorporated, covering their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in semiconductor laser fabrication, integration with 5G networks, and evolving industry standards for optical communication.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as 5G deployment and data center expansion, along with challenges like supply chain constraints and regulatory issues.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in optical communication technologies.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global 25G DFB Laser Chip Market?

-> 25G DFB Laser Chip Market size was valued at US$ 234 million in 2024 and is projected to reach US$ 423 million by 2032, at a CAGR of 8.7% during the forecast period 2025-2032.

Which key companies operate in Global 25G DFB Laser Chip Market?

-> Key players include Sumitomo Electric Industries, Lumentum, II-VI Incorporated, Broadcom, and Macom, among others.

What are the key growth drivers?

-> Key growth drivers include 5G network deployment, data center expansion, and increasing demand for high-speed optical communication.

Which region dominates the market?

-> Asia-Pacific is the dominant market, with China leading in both production and consumption of 25G DFB Laser Chips.

What are the emerging trends?

-> Emerging trends include development of higher efficiency chips, integration with AI-driven networks, and advancements in semiconductor materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...