MARKET INSIGHTS

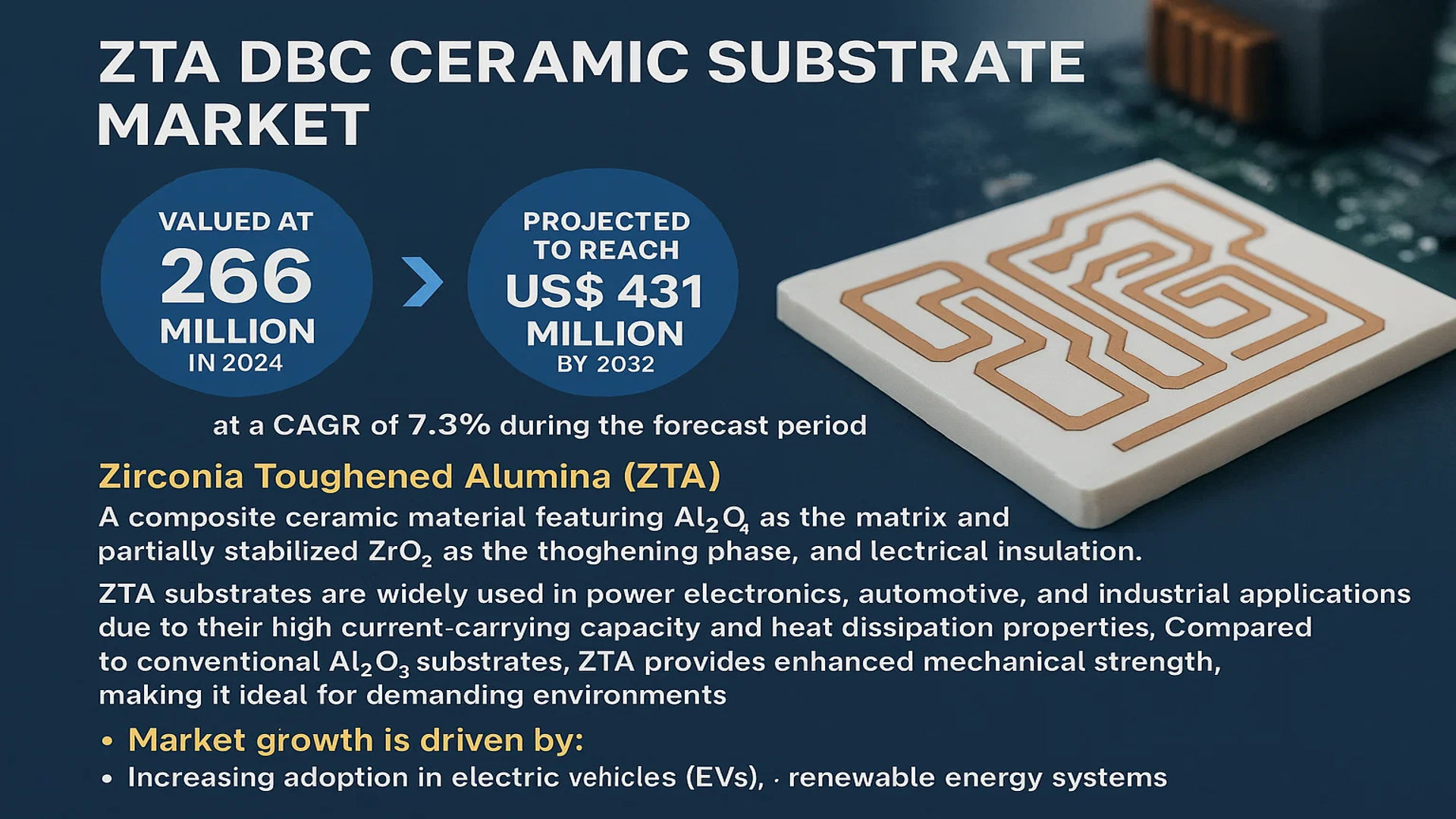

The global ZTA DBC Ceramic Substrate Market was valued at 266 million in 2024 and is projected to reach US$ 431 million by 2032, at a CAGR of 7.3% during the forecast period.

Zirconia Toughened Alumina (ZTA) is a composite ceramic material featuring Al2O3 as the matrix and partially stabilized ZrO2 as the toughening phase, offering superior strength, thermal shock resistance, and electrical insulation. ZTA substrates are widely used in power electronics, automotive, and industrial applications due to their high current-carrying capacity and heat dissipation properties. Compared to conventional Al2O3 substrates, ZTA provides enhanced mechanical strength, making it ideal for demanding environments.

The market growth is driven by increasing adoption in electric vehicles (EVs), renewable energy systems, and aerospace applications. Furthermore, technological advancements in semiconductor packaging and rising demand for efficient thermal management solutions are accelerating market expansion. Leading manufacturers such as Rogers Corporation, Heraeus Electronics, and NGK Electronics Devices dominate the market, collectively holding over 80% of the global share. Strategic collaborations and R&D investments are key factors shaping the competitive landscape.

MARKET DRIVERS

Rising Demand for High-Performance Electronics to Accelerate Market Expansion

The global ZTA DBC ceramic substrate market is witnessing substantial growth driven by increasing demand for high-performance electronic components across industries. These substrates offer superior thermal conductivity (ranging between 24-28 W/mK) and exceptional mechanical strength, making them ideal for power electronic applications. The automotive sector, particularly electric vehicle (EV) power modules, accounts for over 35% of total demand as manufacturers seek more efficient heat dissipation solutions. With EV sales projected to exceed 30 million units annually by 2030, this application segment continues to fuel market momentum.

Advancements in Renewable Energy Infrastructure to Propel Adoption

Growth in renewable energy systems presents significant opportunities for ZTA DBC substrates, particularly in photovoltaic inverters and wind power converters. These substrates demonstrate 40% better thermal cycling performance compared to traditional alumina substrates, a critical factor for energy applications requiring 25+ year operational lifespans. The global renewable energy capacity additions reached nearly 300 GW in recent years, with solar PV representing approximately 60% of new installations. This rapid infrastructure development directly correlates with increased substrate demand in power conditioning and conversion systems.

Military Modernization Programs to Sustain Market Growth

Defense applications continue to drive specialized demand for ZTA DBC substrates, particularly in radar systems and avionics where reliability under extreme conditions is paramount. Military budgets among NATO members have shown consistent 3-5% annual growth, with electronics modernization representing 20-25% of total expenditures. The substrates’ ability to maintain structural integrity across -55°C to +850°C temperature ranges makes them indispensable for next-generation defense electronics where failure is not an option.

MARKET RESTRAINTS

High Production Costs to Limit Market Penetration

The complex manufacturing process for ZTA DBC substrates creates significant cost barriers, with production expenses 30-40% higher than standard alumina substrates. Precise control of zirconia dispersion within the alumina matrix requires specialized equipment and controlled environments, contributing to elevated capital expenditure requirements. These cost factors particularly impact price-sensitive applications, potentially slowing adoption in consumer electronics and some industrial segments.

Technical Complexities in Processing to Challenge Manufacturers

Achieving optimal zirconia particle distribution (typically 10-20% by volume) presents persistent technical hurdles during production. The thermal expansion mismatch between zirconia (10.5×10-6/K) and alumina (8.1×10-6/K) demands exacting process controls to prevent delamination or microcracking during the direct bond copper process. Such technical challenges have resulted in yield rates below 85% for many manufacturers, creating bottlenecks in meeting the growing market demand.

MARKET CHALLENGES

Supply Chain Vulnerabilities to Impact Market Stability

The ZTA DBC substrate market faces significant supply chain risks, particularly regarding specialty alumina and zirconia powders. Over 70% of high-purity alumina originates from just five global suppliers, creating potential bottlenecks. Recent geopolitical tensions have further complicated raw material logistics, with lead times for certain ceramic precursors extending from 4-6 weeks to 12-16 weeks in some regions. These disruptions threaten to constrain market growth despite strong underlying demand.

Standardization Issues to Hinder Widespread Adoption

Lack of universal standards for ZTA compositions creates compatibility concerns for OEMs. While most manufacturers offer substrates with 15% zirconia content, variations in particle size distribution (ranging from 0.3-1.2μm) and stabilizer types (yttria vs. ceria) lead to inconsistent performance characteristics. This standardization gap forces end-users to qualify multiple suppliers, adding complexity to the design-in process and slowing time-to-market for new applications.

MARKET OPPORTUNITIES

Emerging Wide Bandgap Semiconductor Applications to Create New Markets

The transition to silicon carbide (SiC) and gallium nitride (GaN) power devices presents substantial growth opportunities for ZTA DBC substrates. These wide bandgap semiconductors operate at junction temperatures exceeding 200°C, where ZTA substrates demonstrate 25% better thermal cycling resistance than conventional materials. With the SiC power device market forecast to grow at 30% CAGR through 2030, substrate manufacturers are well-positioned to capture this high-value segment.

Advanced Packaging Innovations to Drive Next-Generation Demand

3D packaging technologies for high-power modules are creating demand for novel substrate configurations. The development of multi-layer ZTA substrates with embedded passive components and through-substrate vias could enable 50% size reductions in power modules while improving thermal performance. Early adopters in aerospace and medical imaging sectors are already piloting these advanced solutions, signaling potential for broader market penetration.

ZTA DBC CERAMIC SUBSTRATE MARKET TRENDS

Growing Demand for High-Power Electronics to Drive ZTA DBC Substrate Adoption

The global ZTA DBC ceramic substrate market is experiencing significant growth due to increasing demand for high-power, high-reliability electronic components in industries such as automotive, renewable energy, and industrial applications. Zirconia Toughened Alumina (ZTA) substrates offer superior thermal conductivity (ranging between 24-28 W/mK) and mechanical strength compared to traditional alumina substrates, making them ideal for power electronics that require efficient heat dissipation. The automotive sector, particularly electric vehicles (EVs), represents over 35% of the total market demand as these substrates are critical for power modules in inverters and battery management systems.

Other Trends

Expansion in Renewable Energy Infrastructure

The rapid growth of solar and wind power generation has created substantial demand for ZTA DBC substrates in power converters and inverters. With global renewable energy capacity expected to grow by over 60% between 2024 and 2030, manufacturers are increasingly adopting these ceramic substrates for their ability to withstand extreme thermal cycling and high voltage applications. The photovoltaic sector alone accounts for nearly 20% of current ZTA DBC substrate consumption, with string inverters and central inverters being primary application areas.

Miniaturization and Performance Enhancements in Electronics

As electronic devices continue to shrink in size while requiring higher power densities, ZTA DBC substrates are becoming essential for advanced packaging solutions. The market has seen a 15-20% annual increase in demand for ultra-thin substrates (0.25mm and below) as they enable more compact power module designs without compromising thermal performance. Leading manufacturers are investing in advanced sintering technologies to produce substrates with finer line widths (down to 75μm) and improved surface finishes to meet the evolving requirements of 5G infrastructure and aerospace applications.

Supply Chain Diversification and Regional Manufacturing Growth

While the ZTA DBC substrate market remains concentrated among a few key players controlling over 80% of production, there’s a noticeable trend toward supply chain diversification. Asia-Pacific has emerged as both the largest consumer (55% of global demand) and fastest-growing production hub, with China-based manufacturers expanding capacity by approximately 25% annually. This regional growth is complemented by increasing investments in North America and Europe to reduce dependency on imports, particularly for defense and aerospace applications where supply chain security is paramount.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Material Innovations Drive Market Competition

The global ZTA DBC ceramic substrate market features a semi-consolidated structure, dominated by established material science conglomerates and specialized semiconductor manufacturers. Rogers Corporation leads the segment, leveraging its decades-long expertise in advanced ceramics and direct bonded copper (DBC) technologies. Their recent expansion of high-current ZTA substrate production capacities in Germany directly addresses the surging demand from European EV manufacturers.

Heraeus Electronics and NGK Electronics Devices collectively command over 40% of the market share through their proprietary ZTA formulations optimized for extreme thermal cycling. Both companies have significantly increased R&D spending, with Heraeus launching a new 0.25mm substrate variant for aerospace applications in Q1 2024.

Chinese manufacturers including Jiangsu Fulehua Semiconductor and Nanjing Zhongjiang New Material are rapidly gaining traction through cost-competitive solutions. The joint development of a hybrid ZTA-AlN substrate by Fulehua with a major Taiwanese power module producer exemplifies the regional innovation surge.

Notable market shifts include BYD’s vertical integration strategy, bringing ZTA substrate production in-house for their EV power trains, while KCC strengthens its position through strategic acquisitions of European ceramic technology firms. First-to-market advantages in 0.32mm thick substrates have become a key differentiator among leading players.

List of Major ZTA DBC Ceramic Substrate Manufacturers

- Rogers Corporation (U.S.)

- Heraeus Electronics (Germany)

- NGK Electronics Devices (Japan)

- Jiangsu Fulehua Semiconductor Technology (China)

- KCC (South Korea)

- Nanjing Zhongjiang New Material Science & Technology (China)

- BYD (China)

- Fujian Huaqing Electronic Material Technology (China)

- Konfoong Materials International (China)

Segment Analysis:

By Type

0.25mm ZTA DBC Substrate Dominates the Market Due to Its High Precision and Thermal Conductivity

The market is segmented based on type into:

- 0.25mm ZTA DBC Substrate

- 0.32mm ZTA DBC Substrate

- Others

By Application

Automotive & EV/HEV Segment Leads Due to Rising Demand for Power Electronics in Electric Vehicles

The market is segmented based on application into:

- Automotive & EV/HEV

- PV and Wind Power

- Industrial Drives

- Military & Avionics

- Others

Regional Analysis: ZTA DBC Ceramic Substrate Market

Asia-Pacific

The Asia-Pacific region dominates the global ZTA DBC ceramic substrate market, accounting for over 45% of the total market share in 2024. China leads regional demand due to its thriving semiconductor industry and aggressive investments in electric vehicle (EV) infrastructure. The country’s National Semiconductor Development Plan prioritizes domestic manufacturing of advanced ceramic substrates, creating a robust ecosystem for ZTA DBC producers like Jiangsu Fulehua and Nanjing Zhongjiang. Meanwhile, Japan maintains strong demand for high-performance substrates in industrial automation and 5G infrastructure, with companies like NGK Electronics and Fujian Huaqing expanding production capacities to meet growing specifications for thermal management in power electronics.

North America

North America represents the second-largest market, driven primarily by defense applications and automotive electrification. The U.S. Department of Defense’s FY2024 budget allocated $145 billion for next-gen avionics, fueling demand for military-grade ZTA DBC substrates that can withstand extreme environments. In the private sector, Rogers Corporation leverages its Arizona manufacturing facility to supply ceramic substrates for EV inverters as automakers accelerate transitions to 800V battery systems. Stringent thermal performance requirements from companies like Tesla and GM continue to push substrate manufacturers toward higher ZTA compositions with improved fracture toughness.

Europe

Europe’s market grows steadily through applications in renewable energy and industrial drives, with Germany accounting for 35% of regional consumption. The EU’s Power Electronics Initiative promotes ceramic substrates as key enablers for efficient energy conversion in wind turbines, creating partnerships between Heraeus Electronics and Siemens Energy. Environmental regulations like RoHS 3.0 drive innovation in lead-free bonding techniques, though high production costs remain a barrier against cheaper Asian imports. Recent R&D projects at Fraunhofer IKTS focus on hybrid ZTA-AlN substrates to bridge the performance-cost gap for European manufacturers.

South America

The South American market shows nascent growth, concentrated in Brazil’s automotive sector and Argentina’s emerging solar industry. Limited local production capabilities force reliance on imports from China and Germany, though trade agreements are improving supply chain access. Investments in EV charging infrastructure across Chile and Colombia may stimulate future demand, but currency volatility and import tariffs continue to inflate substrate costs by 15-20% compared to North American prices. Brazilian firms are beginning to explore partnerships with Asian suppliers to develop localized assembly capabilities.

Middle East & Africa

This region represents the smallest but fastest-growing market, with UAE and Israel leading adoption in defense and oil/gas applications. National initiatives like Saudi Vision 2030 drive investments in semiconductor infrastructure, though most ZTA DBC substrates are currently sourced through distributors like Taotao Technology. The lack of local testing facilities for high-temperature validation remains a key adoption barrier, forcing manufacturers to rely on European or Asian certification partners. Emerging opportunities exist in South Africa’s rail electrification projects, which require durable substrates for power control modules.

Report Scope

This market research report provides a comprehensive analysis of the global ZTA DBC Ceramic Substrate market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global ZTA DBC Ceramic Substrate market was valued at USD 266 million in 2024 and is projected to reach USD 431 million by 2032, growing at a CAGR of 7.3%.

- Segmentation Analysis: Detailed breakdown by product type (0.25mm and 0.32mm ZTA DBC substrates) and application (Automotive & EV/HEV, PV and Wind Power, Industrial Drives, Military & Avionics, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific currently holds the largest market share, driven by semiconductor manufacturing growth in China and Japan.

- Competitive Landscape: Profiles of leading market participants including Rogers Corporation, Heraeus Electronics, NGK Electronics Devices, and Jiangsu Fulehua Semiconductor Technology, which collectively account for over 80% market share.

- Technology Trends & Innovation: Assessment of material science advancements in ZTA ceramic formulations and Direct Bonded Copper (DBC) technology improvements for better thermal management.

- Market Drivers & Restraints: Evaluation of factors such as growing EV adoption, renewable energy expansion, and 5G infrastructure development driving demand, countered by raw material price volatility and technical challenges in manufacturing.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, power electronics suppliers, and investors regarding supply chain optimization and emerging opportunities.

Primary and secondary research methods were employed, including interviews with industry experts and analysis of verified market data, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global ZTA DBC Ceramic Substrate Market?

->ZTA DBC Ceramic Substrate Market was valued at 266 million in 2024 and is projected to reach US$ 431 million by 2032, at a CAGR of 7.3% during the forecast period.

Which key companies operate in Global ZTA DBC Ceramic Substrate Market?

-> Key players include Rogers Corporation, Heraeus Electronics, NGK Electronics Devices, Jiangsu Fulehua Semiconductor Technology, and KCC, among others.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of electric vehicles, expansion of renewable energy infrastructure, and growing demand for high-power electronics.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 45% of global demand, led by China’s semiconductor manufacturing sector.

What are the emerging trends?

-> Emerging trends include development of thinner substrates for compact electronics, improved thermal management solutions, and integration with advanced semiconductor packaging technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...