MARKET INSIGHTS

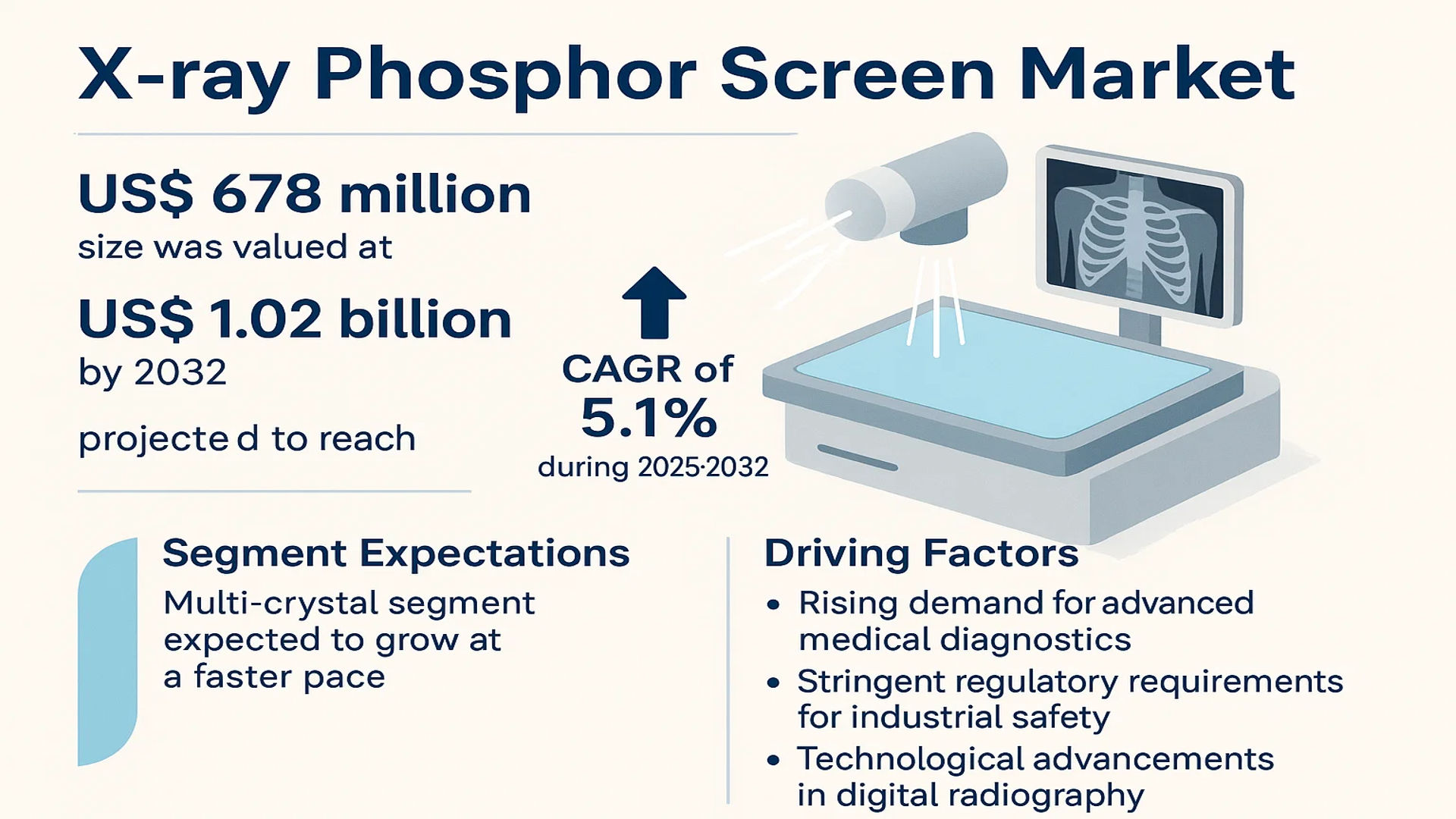

The global X-ray Phosphor Screen Market size was valued at US$ 678 million in 2024 and is projected to reach US$ 1.02 billion by 2032, at a CAGR of 5.1% during the forecast period 2025-2032.

X-ray phosphor screens are critical components in medical imaging and industrial inspection systems, converting X-ray photons into visible light to produce high-quality digital images. These screens are categorized into multi-crystal and single-crystal types, with applications spanning CT scanners, security devices, and non-destructive testing. The multi-crystal segment is expected to grow at a faster pace due to its superior resolution and adaptability.

Market expansion is driven by rising demand for advanced medical diagnostics, stringent regulatory requirements for industrial safety, and technological advancements in digital radiography. However, high manufacturing costs and competition from alternative imaging technologies pose challenges. Key players such as Carestream Health, Hamamatsu Photonics, and Konica Minolta are investing in R&D to enhance phosphor screen efficiency, with North America and Asia-Pacific emerging as dominant regional markets.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Advanced Medical Imaging to Propel X-ray Phosphor Screen Adoption

The global healthcare industry’s shift towards digital radiography and computed tomography is fueling strong demand for high-performance X-ray phosphor screens. These components play a critical role in converting X-ray photons into visible light, forming the backbone of modern medical imaging systems. With diagnostic imaging procedures projected to grow at approximately 5-7% annually worldwide, healthcare providers are increasingly upgrading to phosphor screen-based systems that offer superior image resolution while reducing patient radiation exposure by up to 30% compared to traditional methods.

Technological Advancements in Detection Materials Enhance Market Potential

Recent breakthroughs in phosphor screen technology, particularly in terbium-doped gadolinium oxysulfide (Gd2O2S:Tb) and cesium iodide (CsI) formulations, are creating new opportunities. These advanced materials demonstrate 15-20% higher conversion efficiency than conventional options, significantly improving image quality for applications ranging from mammography to industrial non-destructive testing. Several leading manufacturers have recently introduced multi-layer phosphor screens that minimize light scattering, achieving resolution capabilities below 10 line pairs per millimeter – a critical threshold for detecting minute fractures and microcalcifications.

MARKET RESTRAINTS

High Equipment Costs and Limited Healthcare Budgets Constrain Market Penetration

While X-ray phosphor screen technology offers clear medical benefits, its adoption faces financial barriers in cost-sensitive markets. Complete digital radiography systems incorporating premium phosphor screens can require investments exceeding $150,000 per unit, putting them beyond reach for many healthcare facilities in developing regions. Additionally, the specialized nature of phosphor screen manufacturing leads to production costs that are approximately 30-40% higher than conventional X-ray components, creating pricing pressures that limit market growth potential in budget-constrained environments.

Other Restraints

Logistical Challenges in Materials Sourcing

The industry faces supply chain vulnerabilities for rare earth elements like gadolinium and europium that are essential for phosphor screen production. Recent export restrictions and fluctuating availability of these materials have caused price volatility exceeding 25% year-over-year, forcing manufacturers to maintain higher inventory levels and impacting profit margins.

MARKET OPPORTUNITIES

Expanding Application in Security and Industrial Sectors Opens New Revenue Streams

Beyond healthcare, X-ray phosphor screens are finding growing adoption in security screening and industrial quality control applications. Airports and customs facilities worldwide are upgrading to phosphor-based baggage scanning systems that offer superior threat detection capabilities, with the global aviation security market projected to invest over $3 billion in advanced screening technologies through 2028. Similarly, manufacturing plants are implementing phosphor screen systems for non-destructive testing of critical components in aerospace and automotive industries, where detection resolutions below 5 microns are becoming mandatory for quality assurance.

MARKET CHALLENGES

Technical Limitations in Low-Dose Applications Pose Implementation Barriers

While X-ray phosphor screens offer excellent performance in standard imaging scenarios, their effectiveness diminishes significantly in ultra-low dose applications such as pediatric radiography. The quantum detection efficiency of current phosphor materials drops by approximately 40% when radiation doses are reduced below certain thresholds, creating clinical limitations. This performance gap has led some healthcare providers to adopt alternative technologies for sensitive applications, despite phosphor screens’ advantages in standard use cases.

Other Challenges

Durability and Maintenance Requirements

Phosphor screens require careful handling and periodic replacement due to gradual decreases in conversion efficiency, with typical service life ranging from 3-5 years depending on usage intensity. The need for specialized cleaning procedures and environmental controls in clinical settings adds to total cost of ownership considerations that influence purchasing decisions.

X-RAY PHOSPHOR SCREEN MARKET TRENDS

Advancements in Medical Imaging to Drive Market Growth

The global X-ray phosphor screen market is witnessing significant growth due to rapid advancements in medical imaging technologies. The increasing adoption of digital radiography (DR) systems and computed radiography (CR) systems in healthcare institutions is driving demand for high-quality X-ray phosphor screens. These screens play a critical role in converting X-ray energy into visible light, enabling clearer diagnostic imaging. Technological innovations in scintillator materials, such as gadolinium oxysulfide (GOS) and cesium iodide (CsI), have improved resolution and detection efficiency, making them essential in modern diagnostic equipment. Additionally, the shift towards portable and handheld X-ray devices in emergency and point-of-care settings is creating new opportunities for lightweight and flexible phosphor screens.

Other Trends

Expansion in Non-Destructive Testing (NDT) Applications

Beyond medical diagnostics, X-ray phosphor screens are increasingly utilized in industrial non-destructive testing (NDT), particularly in aerospace, automotive, and construction sectors. The ability to detect structural defects without damaging materials has elevated their importance in quality control processes. High-energy X-ray phosphor screens with enhanced sensitivity are being developed to inspect thick and complex metal components, supporting industries striving for precision and safety compliance. The global emphasis on infrastructure development and manufacturing automation further accelerates market adoption.

Growing Demand for Security Screening Solutions

The increasing need for advanced security screening at airports, border checkpoints, and high-risk facilities is significantly contributing to market expansion. X-ray phosphor screens are integral components of baggage and cargo scanning systems, helping improve threat detection accuracy while reducing false positives. Government investments in enhancing public safety and anti-terrorism measures have led to upgrades in screening technologies, creating sustained demand for efficient phosphor screens. Moreover, advancements in artificial intelligence (AI)-assisted image processing are expected to enhance the performance of these systems in identifying concealed objects. However, the higher cost of premium phosphor screen materials remains a potential restraint for broader adoption in cost-sensitive regions.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation Drives Competition in X-ray Phosphor Screen Market

The global X-ray phosphor screen market exhibits a moderately consolidated structure where established multinational corporations dominate alongside specialized manufacturers. Mitsubishi Chemical Corporation leads the market with its diversified product portfolio spanning medical imaging, industrial non-destructive testing, and security screening applications. The company’s 2023 acquisition of a phosphor technology startup significantly enhanced its R&D capabilities in high-resolution screens.

Carestream Health and Hamamatsu Photonics collectively held approximately 32% market share in 2024, driven by their stronghold in medical diagnostic equipment. These manufacturers benefit from vertical integration, producing both phosphor screens and complementary imaging systems. Recently, Carestream launched its next-generation DirectView Vita CR system featuring improved phosphor screen durability, demonstrating how product upgrades maintain competitive advantage.

While Japanese and European firms dominate the technology landscape, Chinese manufacturers like Acuri Technology are gaining traction through cost-competitive solutions. The company expanded its market share by 2.3 percentage points between 2022-2024 by focusing on the Asia-Pacific industrial NDT sector. However, they face challenges in matching the R&D investment levels of global leaders, spending approximately 35% less on technology development compared to top-tier competitors.

Strategic partnerships are reshaping the competitive environment, with Toshiba Materials and Fujifilm announcing a joint venture in Q1 2024 to develop advanced phosphor formulations. Such collaborations enable sharing of intellectual property while mitigating development risks in this capital-intensive sector. Meanwhile, Konica Minolta’s recent $120 million investment in its German production facility underscores how geographical expansion supports market penetration.

List of Key X-ray Phosphor Screen Companies Profiled

- Mitsubishi Chemical Corporation (Japan)

- Carestream Health (U.S.)

- Hamamatsu Photonics (Japan)

- Agfa-Gevaert Group (Belgium)

- Toshiba Materials Co., Ltd. (Japan)

- Acuri Technology (China)

- Konica Minolta (Japan)

- Fujifilm Holdings Corporation (Japan)

- PerkinElmer, Inc. (U.S.)

- Canon Medical Systems Corporation (Japan)

Segment Analysis:

By Type

Multi Crystal Segment Dominates the Market Due to Superior Resolution and Imaging Performance

The market is segmented based on type into:

- Multi Crystal

- Single Crystal

By Application

CT Scanners Account for Significant Demand Owing to Increasing Diagnostic Imaging Procedures

The market is segmented based on application into:

- CT Scanners

- Security Devices

- Non-destructive Testing

- Others

By End User

Hospitals and Diagnostic Centers Lead the Market Due to Rising Patient Influx for Radiography

The market is segmented based on end user into:

- Hospitals

- Diagnostic Centers

- Research Laboratories

- Industrial Facilities

- Others

By Technology

Digital X-ray Systems Drive Growth with Advantages of Faster Processing and Storage

The market is segmented based on technology into:

- Computed Radiography (CR)

- Digital Radiography (DR)

- Analog X-ray Systems

Regional Analysis: X-ray Phosphor Screen Market

Asia-Pacific

The Asia-Pacific region dominates the global X-ray phosphor screen market, accounting for the largest share in terms of both revenue and volume. This is primarily driven by strong demand from China, Japan, and India, where rapid advancements in medical imaging technologies and increasing healthcare expenditures fuel market growth. China’s industrial and healthcare sectors are accelerating adoption, supported by government initiatives to modernize diagnostic infrastructure. Japan remains a technology leader with companies like Hamamatsu Photonics and Toshiba Materials pioneering high-resolution phosphor screens for precision applications. While cost-competitive solutions prevail in emerging markets, there’s growing investment in advanced single-crystal screens for specialized medical and industrial use cases.

North America

The North American market is characterized by high technological adoption and stringent quality standards, particularly in medical applications. The U.S. FDA’s regulatory framework ensures advanced imaging systems incorporate premium-grade phosphor screens, favoring suppliers with rigorous quality control processes. Market leaders like Carestream Health and Fujifilm Medical Systems are driving innovation in direct radiography applications. The region shows strong demand for multi-crystal screens in security screening at airports and borders, benefiting from homeland security investments. Canadian research institutions are contributing to material science breakthroughs that enhance screen durability and image clarity.

Europe

European demand focuses on precision and environmental compliance, with Germany and France leading in medical and industrial NDT (Non-Destructive Testing) applications. The region benefits from concentrated R&D activities by companies like Agfa-Gevaert and Siemens Healthineers, developing phosphor screens with lower radiation doses. EU regulations on hazardous substances influence material compositions, pushing manufacturers toward eco-friendly alternatives. While growth in Western Europe remains steady, Eastern European markets show potential with upgrading healthcare facilities. The aerospace sector’s stringent inspection requirements create specialized opportunities for high-performance screens.

South America

Market development in South America faces infrastructure and budget constraints, though Brazil and Argentina show gradual expansion in medical imaging capabilities. Price sensitivity limits adoption of premium phosphor screens, with many healthcare facilities relying on refurbished systems. However, the oil & gas industry’s NDT requirements drive steady demand in countries with energy sectors. Local manufacturers focus on economical multi-crystal solutions, while import-dependent nations struggle with supply chain inefficiencies and currency fluctuations affecting advanced technology acquisition.

Middle East & Africa

This emerging market demonstrates uneven growth patterns, with GCC nations like Saudi Arabia and the UAE making significant investments in digital radiography systems. High-end healthcare projects in urban centers drive demand for quality phosphor screens, often sourced from global suppliers. Africa’s market remains constrained by limited healthcare budgets, though development initiatives are gradually improving access to basic imaging technologies. The security sector shows promise with increasing deployment of X-ray screening at ports and critical infrastructure, creating opportunities for durable phosphor screen solutions.

Report Scope

This market research report provides a comprehensive analysis of the Global X-ray Phosphor Screen Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at US$ 678 million in 2024 and is projected to reach US$ 1.02 billion by 2032, growing at a CAGR of 5.1 %.

- Segmentation Analysis: Detailed breakdown by product type (Multi Crystal, Single Crystal), application (CT Scanners, Security Devices, Non-destructive Testing, Others), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including Mitsubishi, Carestream, Agfa, Hamamatsu Photonics, Toshiba Materials, and others, with their product offerings, market share, and recent developments.

- Technology Trends & Innovation: Assessment of emerging advancements in phosphor screen technology, integration with digital imaging, and material science breakthroughs.

- Market Drivers & Restraints: Evaluation of factors such as rising demand for medical imaging, industrial non-destructive testing, and security screening, alongside challenges like high manufacturing costs and regulatory hurdles.

- Stakeholder Analysis: Strategic insights for manufacturers, suppliers, healthcare providers, and investors regarding market opportunities and competitive positioning.

Primary and secondary research methodologies, including expert interviews and verified market data, ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Global X-ray Phosphor Screen Market?

-> X-ray Phosphor Screen Market size was valued at US$ 678 million in 2024 and is projected to reach US$ 1.02 billion by 2032, at a CAGR of 5.1% during the forecast period 2025-2032.

Which key companies operate in the Global X-ray Phosphor Screen Market?

-> Key players include Mitsubishi, Carestream, Agfa, Hamamatsu Photonics, Toshiba Materials, Konica Minolta, and Fujifilm Medical Systems.

What are the key growth drivers?

-> Growth is driven by increasing medical imaging demand, advancements in non-destructive testing, and rising security screening requirements.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while North America and Europe remain dominant due to established healthcare infrastructure.

What are the emerging trends?

-> Emerging trends include high-resolution phosphor screens, digital integration, and eco-friendly material innovations.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...