MARKET INSIGHTS

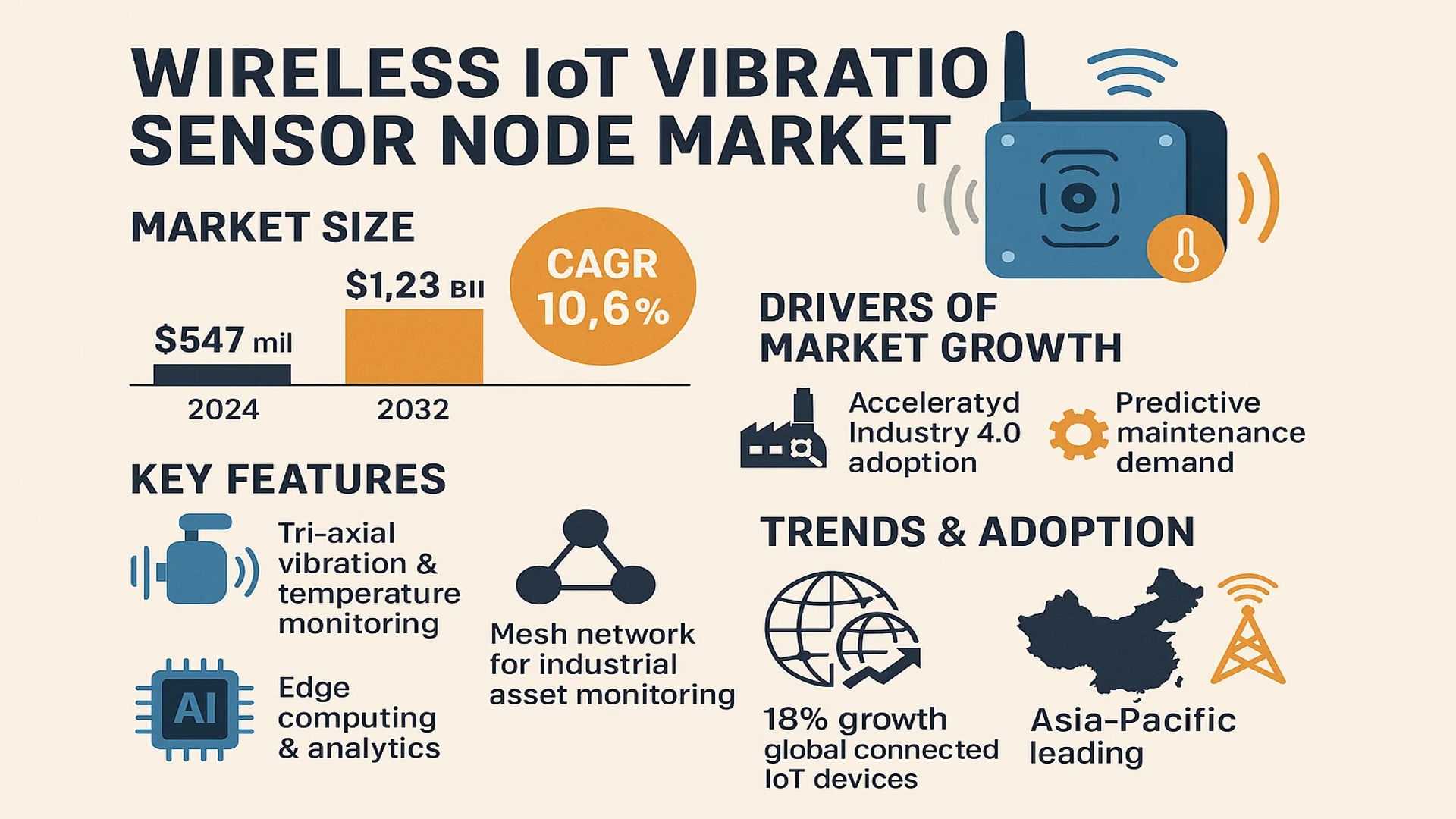

The global Wireless IoT Vibration Sensor Node Market size was valued at US$ 547 million in 2024 and is projected to reach US$ 1.23 billion by 2032, at a CAGR of 10.6% during the forecast period 2025-2032. This growth is fueled by accelerating Industry 4.0 adoption and increasing demand for predictive maintenance solutions across manufacturing sectors.

Wireless IoT Vibration Sensor Nodes are compact, battery-powered devices that monitor equipment health through tri-axial vibration measurement and surface temperature sensing. These nodes form mesh networks to enable cost-effective, continuous monitoring of industrial assets like motors, pumps, and compressors. Advanced units incorporate edge computing capabilities for real-time analytics.

The market expansion correlates with rapid IoT infrastructure development, as evidenced by the 18% growth in global connected IoT devices to 14 billion units in 2022. Asia-Pacific leads adoption, with China deploying 2.3 million 5G base stations and achieving gigabit network coverage for 500 million households by 2022. Key players like Yokogawa Electric Corporation and Advantech are driving innovation through enhanced power efficiency and AI-integrated diagnostic features, addressing the growing need for smart factory solutions.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Industry 4.0 and Predictive Maintenance to Accelerate Market Growth

The global shift toward Industry 4.0 and smart manufacturing continues to drive substantial demand for wireless IoT vibration sensor nodes. These sensor nodes play a critical role in predictive maintenance strategies by monitoring equipment health in real-time and preventing unplanned downtime. Research indicates that predictive maintenance can reduce maintenance costs by up to 25%, a significant benefit for manufacturing operations. The growing implementation of Industrial Internet of Things (IIoT) solutions across sectors such as oil & gas, automotive, and energy is further propelling market expansion.

Expansion of 5G Infrastructure Enhancing IoT Connectivity Capabilities

The rapid rollout of 5G networks worldwide is creating optimal conditions for wireless IoT vibration sensor deployment. With its low latency and high-bandwidth features, 5G technology enables real-time data transmission from multiple sensor nodes simultaneously. This is particularly valuable for applications requiring immediate response to vibration anomalies, such as in critical infrastructure monitoring. The 5G infrastructure expansion, including over 2.3 million base stations already deployed in China alone, significantly lowers barriers for large-scale IoT implementations.

Additionally, the increasing integration of edge computing capabilities directly into sensor nodes allows for local data processing, reducing bandwidth requirements while improving response times. This technological convergence is expected to drive further adoption across industrial applications.

MARKET RESTRAINTS

High Initial Deployment Costs and ROI Uncertainty Limit Market Penetration

While wireless IoT vibration sensors offer long-term cost savings, their high initial investment remains a significant barrier for small and medium enterprises. Comprehensive system implementation often requires substantial capital expenditure for sensors, gateways, software platforms, and integration services. Many organizations hesitate to adopt these solutions due to uncertainty regarding return on investment timelines, particularly in industries with tight profit margins.

Other Restraints

Power Consumption Challenges

Battery life remains a critical constraint for wireless sensor nodes, especially in hard-to-access locations. Frequent battery replacements can significantly increase total cost of ownership and limit deployment scalability. While energy harvesting technologies show promise, their current reliability and consistency often fail to meet industrial requirements.

Interoperability Issues

The lack of standardized communication protocols across different manufacturers creates integration challenges. Many end-users face difficulties when attempting to combine sensor nodes from multiple vendors into a unified monitoring system, potentially leading to vendor lock-in situations.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy Sector Present Significant Growth Potential

The global push toward renewable energy creates substantial opportunities for wireless vibration monitoring solutions. Wind turbine monitoring represents a particularly promising application, where vibration sensors can detect early signs of bearing wear or structural issues in remote, hard-to-access locations. With wind capacity expected to grow significantly by 2030, the demand for reliable condition monitoring solutions in this sector is projected to increase accordingly.

Integration with AI and Machine Learning Opens New Possibilities

Advanced analytics powered by artificial intelligence and machine learning are transforming vibration monitoring capabilities. These technologies enable more accurate fault detection, predictive analytics, and even prescriptive maintenance recommendations. As AI algorithms become more sophisticated, wireless sensor nodes equipped with edge processing capabilities can provide actionable insights without requiring constant cloud connectivity.

Furthermore, the development of hybrid systems combining vibration data with other parameters such as temperature and acoustic emissions is creating more comprehensive equipment health monitoring solutions. This multi-parameter approach enhances diagnostic accuracy while maximizing the value derived from wireless sensor networks.

MARKET CHALLENGES

Data Security Concerns in Industrial IoT Networks Pose Implementation Challenges

As wireless IoT vibration sensor networks become more prevalent, cybersecurity risks emerge as a significant concern. Industrial facilities handling sensitive operations require robust security measures to protect against potential cyber threats. The distributed nature of wireless sensor networks increases potential attack surfaces, making comprehensive security protocols essential.

Other Challenges

Environmental Limitations

Harsh industrial environments with extreme temperatures, electromagnetic interference, or hazardous conditions present operational challenges for wireless sensor nodes. While ruggedized solutions exist, they often come at a premium cost, limiting their widespread adoption.

Skill Gap in Advanced Analytics

The effective utilization of vibration data requires specialized technical expertise in condition monitoring and predictive analytics. Many organizations lack personnel with the necessary skills to interpret complex vibration signatures and derive meaningful insights from the collected data.

WIRELESS IOT VIBRATION SENSOR NODE MARKET TRENDS

Industrial IoT Connectivity Expansion Drives Market Growth

The adoption of Wireless IoT Vibration Sensor Nodes is being propelled by the rapid expansion of Industrial IoT infrastructure worldwide. These sensor nodes are increasingly deployed in factories, power plants, and manufacturing facilities to enable predictive maintenance of critical machinery. The global market for these devices grew at a CAGR of 20.3% between 2020 and 2024, as industries shift from traditional wired systems to flexible wireless solutions. With 5G networks now covering many industrial zones, these battery-operated sensors can transmit vibration and temperature data in real-time with minimal latency, reducing unplanned downtime by up to 45% according to operational data from early adopters.

Other Trends

Energy Efficiency Innovations

Recent advancements in ultra-low-power wireless technologies have significantly extended the battery life of vibration sensor nodes, with some models now operating for 5+ years without maintenance. This breakthrough is particularly crucial for hard-to-access industrial equipment where frequent battery replacements were previously a major limitation. The integration of energy harvesting techniques, such as vibration-powered charging, is further enhancing the sustainability of these IoT solutions while reducing total cost of ownership.

AI-Powered Predictive Analytics Integration

The combination of wireless vibration sensors with machine learning algorithms is transforming condition monitoring from reactive to truly predictive maintenance. Advanced sensor nodes now incorporate edge computing capabilities to perform initial vibration pattern analysis before transmitting only critical data to central systems. This not only reduces network congestion but also enables near-instant anomaly detection. Industries implementing these intelligent systems report a 30-60% reduction in equipment failures, creating strong demand for next-generation sensor nodes with built-in analytics capabilities.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Market Leadership in Wireless IoT Vibration Monitoring

The global wireless IoT vibration sensor node market features a dynamic competitive landscape with a mix of established industrial automation providers and specialized IoT solution developers. Yokogawa Electric Corporation and Advantech currently dominate market share, collectively accounting for over 25% of 2024 revenues, owing to their robust industrial IoT ecosystems and extensive distribution networks across manufacturing hubs.

Second-tier players like Bently Nevada (a Baker Hughes company) are gaining traction through vertical-specific solutions for oil & gas applications, while startups such as Petasense and Broadsens are disrupting traditional predictive maintenance models with AI-powered vibration analytics platforms. The market remains fragmented in developing regions, where local players like China’s Miniotec compete aggressively on price-performance ratios.

Recent industry shifts show mainstream adoption of wireless protocols – with 72% of new deployments in 2024 utilizing Bluetooth Low Energy (BLE) or 802.15.4 mesh networks rather than traditional WiFi. This transition favors agile innovators like TWTG and iQunet, whose ultra-low-power designs enable 5+ year battery life in harsh environments. Meanwhile, industrial heavyweights are responding through acquisitions – notably Advantech’s 2023 purchase of BeanAir to strengthen wireless sensor capabilities.

The competitive intensity is further amplified by growing cross-industry applications. While traditional manufacturing equipment monitoring still drives 58% of demand, emerging use cases in building automation (22% CAGR projected through 2032) and medical device monitoring are creating new battlegrounds. Companies like National Control Devices are leveraging modular designs to serve these diverse applications, whereas specialists such as Erbessd Instruments focus on high-precision solutions for aerospace and defense sectors.

List of Key Wireless IoT Vibration Sensor Node Companies Profiled

- Yokogawa Electric Corporation (Japan)

- Advantech (Taiwan)

- Bently Nevada (U.S.)

- Petasense (U.S.)

- Broadsens (Germany)

- TWTG (Netherlands)

- Miniotec (China)

- iQunet (Germany)

- National Control Devices (U.S.)

- Erbessd Instruments (Mexico)

- Althen (Germany)

- Bean Air (France)

Segment Analysis:

By Type

WiFi Connection Segment Dominates Owing to Higher Data Transmission Capabilities in Industrial Settings

The market is segmented based on connectivity type into:

- WiFi Connection

- Bluetooth Connection

- Cellular Connection

- Others

By Application

Industrial Equipment Monitoring Leads the Market Due to Growing Demand for Predictive Maintenance

The market is segmented based on application into:

- Industrial equipment monitoring

- Building automation

- Energy infrastructure

- Transportation systems

- Others

By End User

Manufacturing Sector Holds Largest Share Due to Increased Adoption of Industry 4.0 Technologies

The market is segmented based on end user into:

- Manufacturing

- Oil & gas

- Energy & utilities

- Transportation

- Others

By Sensing Axis

Tri-Axial Sensors Dominate Market Due to Comprehensive Vibration Measurement Capabilities

The market is segmented based on sensing axis into:

- Single-axis

- Tri-axial

- Others

Regional Analysis: Wireless IoT Vibration Sensor Node Market

Asia-Pacific

Asia-Pacific dominates the Wireless IoT Vibration Sensor Node market, driven by rapid industrialization and widespread adoption of Industry 4.0 technologies. China leads regional growth with extensive 5G infrastructure deployment (2.3 million base stations operational by 2022) and government-backed IoT initiatives. Japan and South Korea contribute significantly through advanced manufacturing sectors leveraging vibration sensors for predictive maintenance. India’s market is expanding due to rising demand in automotive and energy applications, though cost sensitivity slows high-end adoption. The region’s CAGR is projected to exceed the global average, fueled by urbanization and smart city projects.

North America

North America holds a strong second position, propelled by mature industrial automation and stringent regulatory standards for equipment safety. The U.S. accounts for the majority of demand, with sectors like oil & gas and aerospace prioritizing wireless vibration monitoring to minimize downtime. Canada’s market is growing steadily, supported by investments in renewable energy infrastructure. However, higher device costs and competition from wired alternatives temper growth in price-sensitive segments. Recent collaborations between sensor manufacturers and cloud service providers (e.g., AWS IoT integrations) are accelerating market penetration.

Europe

Europe’s market thrives on tight EU regulations mandating machine health monitoring and energy efficiency. Germany and the U.K. lead in adopting wireless sensor networks for manufacturing and utilities, driven by Industry 4.0 policies. Scandinavia shows high uptake in wind energy applications, where sensors optimize turbine performance. Challenges include slower replacement cycles of legacy systems and data privacy concerns under GDPR. Nevertheless, innovation in low-power wireless protocols (e.g., LoRaWAN) and edge computing is creating new opportunities.

South America

Adoption remains nascent but promising, with Brazil and Argentina spearheading growth in mining and agriculture sectors. Economic instability limits large-scale deployments, though foreign investments in infrastructure (e.g., renewable energy plants) are driving demand for condition monitoring. Local manufacturers focus on cost-competitive solutions, often prioritizing Bluetooth-based nodes over WiFi due to lower power requirements. The lack of standardized IoT frameworks hinders interoperability, but pilot projects in smart cities indicate long-term potential.

Middle East & Africa

The region is in the early stages of adoption, with UAE and Saudi Arabia leading through oil & gas and smart building projects. Wireless vibration sensors are increasingly used in predictive maintenance for critical machinery, though reliance on imported technology and limited local expertise pose barriers. Africa’s growth is sporadic, concentrated in South Africa’s mining sector. Expanding telecom infrastructure (e.g., 5G rollouts in major cities) could unlock opportunities, but funding gaps and fragmented policies delay widespread implementation.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Wireless IoT Vibration Sensor Node markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Wireless IoT Vibration Sensor Node market was valued at US$ 547 million in 2024 and is projected to reach US$ 1.23 billion by 2032, growing at a CAGR of 10.6% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (WiFi Connection, Bluetooth Connection), application (Wearable Electronic Devices, Medical Devices, Consumer Electronics, Building Automation), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with China accounting for 32% of the global market share in 2024.

- Competitive Landscape: Profiles of leading market participants including Althen, Advantech, Yokogawa Electric Corporation, and Bently Nevada, covering their product portfolios, market strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies including AI-powered predictive maintenance, edge computing integration, and 5G-enabled sensor networks.

- Market Drivers & Restraints: Evaluation of growth drivers (industrial IoT adoption, predictive maintenance demand) and challenges (battery life limitations, data security concerns).

- Stakeholder Analysis: Strategic insights for sensor manufacturers, IoT platform providers, industrial equipment OEMs, and investors.

The research methodology combines primary interviews with industry experts and analysis of verified market data from regulatory bodies and trade associations, ensuring accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Wireless IoT Vibration Sensor Node Market?

-> Wireless IoT Vibration Sensor Node Market size was valued at US$ 547 million in 2024 and is projected to reach US$ 1.23 billion by 2032, at a CAGR of 10.6% during the forecast period 2025-2032.

Which key companies operate in Global Wireless IoT Vibration Sensor Node Market?

-> Key players include Althen, Advantech, Yokogawa Electric Corporation, Bently Nevada, Petasense, and TWTG, among others.

What are the key growth drivers?

-> Key growth drivers include industrial IoT adoption, predictive maintenance demand, and 5G network expansion with over 2.3 million 5G base stations deployed in China alone by 2022.

Which region dominates the market?

-> Asia-Pacific leads the market with 42% share, followed by North America at 28% market share in 2024.

What are the emerging trends?

-> Emerging trends include energy harvesting sensors, AI-powered analytics, and mesh network deployments for industrial asset monitoring.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...