MARKET INSIGHTS

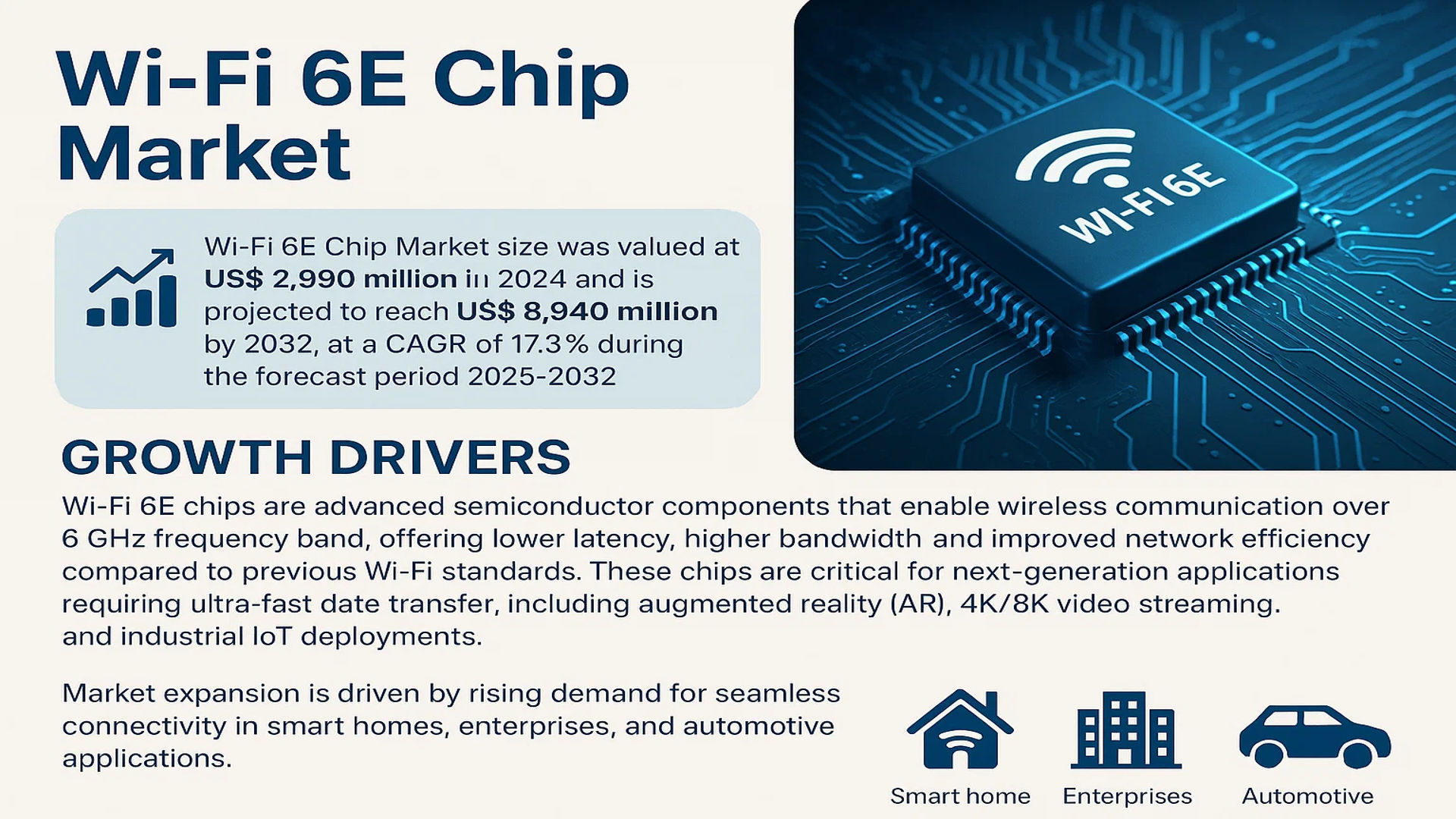

The global Wi-Fi 6E Chip Market size was valued at US$ 2,890 million in 2024 and is projected to reach US$ 8,940 million by 2032, at a CAGR of 17.3% during the forecast period 2025-2032. This growth is fueled by the increasing adoption of high-speed internet connectivity and the proliferation of smart devices across industries.

Wi-Fi 6E chips are advanced semiconductor components that enable wireless communication over the 6 GHz frequency band, offering lower latency, higher bandwidth, and improved network efficiency compared to previous Wi-Fi standards. These chips are critical for next-generation applications requiring ultra-fast data transfer, including augmented reality (AR), 4K/8K video streaming, and industrial IoT deployments.

The market expansion is driven by rising demand for seamless connectivity in smart homes, enterprises, and automotive applications. While the semiconductor industry faced challenges in 2022 with a growth slowdown to 4.4% (USD 580 billion market size), the wireless communication segment continues to show resilience. Leading manufacturers like Broadcom, Qualcomm, and Intel are investing heavily in Wi-Fi 6E technology to capitalize on the growing need for high-performance networking solutions in an increasingly connected world.

MARKET DYNAMICS

MARKET DRIVERS

Explosive Growth in IoT and Smart Devices Fuels Wi-Fi 6E Chip Demand

The proliferation of IoT devices and smart home ecosystems is creating unprecedented demand for high-speed, low-latency connectivity solutions. Wi-Fi 6E chips, operating in the 6 GHz spectrum, deliver up to 2.4 Gbps peak speeds with significantly reduced interference compared to traditional Wi-Fi standards. With over 30 billion IoT devices projected for deployment by 2025, network congestion has become a critical pain point that Wi-Fi 6E effectively addresses. The technology’s ability to support more than 100 simultaneous device connections per access point makes it ideal for dense deployment environments. Semiconductor manufacturers are reporting year-over-year order growth exceeding 40% for Wi-Fi 6E components as enterprises and consumers upgrade their infrastructure.

Workforce Transformation Accelerates Enterprise Adoption

The global shift toward hybrid work models has created strong demand for enterprise-grade networking solutions. Wi-Fi 6E’s support for advanced features like multi-user MIMO and orthogonal frequency-division multiple access (OFDMA) enables seamless video conferencing and large file transfers across distributed teams. Corporations are allocating an average of 15-20% of their IT budgets to network infrastructure upgrades, with Wi-Fi 6E deployments showing the highest growth rate among wireless technologies. Recent tests in enterprise environments demonstrate Wi-Fi 6E can deliver up to 75% lower latency compared to Wi-Fi 6, making it particularly valuable for latency-sensitive applications like AR/VR collaboration tools.

Regulatory Support Opens New Spectrum Opportunities

Government agencies worldwide are actively reallocating spectrum to support next-generation wireless technologies. The recent availability of 1,200 MHz of spectrum in the 6 GHz band across multiple regions has created immediate opportunities for Wi-Fi 6E expansion. This newly available spectrum provides seven additional 160 MHz channels, effectively tripling the available bandwidth for high-performance applications. In markets where 6 GHz spectrum has been available for over 12 months, Wi-Fi 6E adoption rates have shown 3-4 times faster growth compared to previous Wi-Fi standard transitions. Continued regulatory support is expected to open additional spectrum bands, further accelerating market expansion.

MARKET CHALLENGES

High Implementation Costs Create Adoption Barriers

While the technical advantages of Wi-Fi 6E are clear, its adoption faces significant cost-related challenges. Complete network upgrades require replacing both access points and client devices, with enterprise-grade Wi-Fi 6E routers costing 40-60% more than comparable Wi-Fi 6 models. The premium pricing stems from complex antenna designs, advanced power management circuits, and sophisticated radio frequency components needed for 6 GHz operation. For budget-conscious organizations and consumers, these costs present a substantial barrier to adoption, particularly in price-sensitive markets where wireless infrastructure spending has remained flat.

Other Challenges

Backward Compatibility Issues

Many existing devices cannot leverage the full capabilities of Wi-Fi 6E, creating challenges for gradual network transitions. The majority of smartphones and laptops shipped before 2021 lack the necessary hardware to connect to 6 GHz networks, forcing organizations to maintain legacy infrastructure or risk service disruptions. This compatibility gap is particularly acute in industrial environments where equipment lifecycles often exceed 5-7 years.

Thermal Management Concerns

Wi-Fi 6E chips generate significantly more heat than previous generations due to higher processing demands and advanced modulation schemes. Without proper thermal design, sustained performance can degrade by up to 30% in compact form factors. These thermal challenges require careful engineering solutions that add complexity and cost to product development cycles.

MARKET RESTRAINTS

Limited Global Spectrum Harmonization Impacts Scalability

The Wi-Fi 6E market faces significant growth constraints due to inconsistent spectrum allocation across global markets. While some regions have fully opened the 6 GHz band for unlicensed use, others have implemented partial allocations or maintained restrictions. This fragmentation creates challenges for manufacturers developing global products and limits economies of scale. In markets where the full 6 GHz band remains unavailable, Wi-Fi 6E performance advantages are substantially diminished, reducing its value proposition compared to Wi-Fi 6. Recent regulatory delays in several key markets have pushed back projected adoption timelines by 12-18 months.

Other Restraints

Security Concerns with New Spectrum

The expansion into 6 GHz operation introduces new security considerations that some enterprise IT departments find concerning. Unlike the crowded 2.4 GHz and 5 GHz bands where interference can act as a natural security layer, the relatively empty 6 GHz spectrum may require additional security measures to prevent long-range signal interception. These concerns have slowed adoption in security-sensitive industries like finance and healthcare.

Supply Chain Constraints for Specialized Components

Manufacturing high-performance Wi-Fi 6E chips requires specialized semiconductor processes and RF components that face production bottlenecks. Lead times for certain gallium nitride (GaN) power amplifiers and advanced packaging solutions have extended beyond 30 weeks, delaying product launches. These constraints are particularly affecting smaller manufacturers attempting to enter the market.

MARKET OPPORTUNITIES

Emerging Applications in Industrial Automation Create New Growth Avenues

The industrial sector represents one of the most promising opportunities for Wi-Fi 6E adoption. Factory automation systems demand reliable, high-throughput wireless connectivity with deterministic latency below 10ms—a requirement perfectly aligned with Wi-Fi 6E capabilities. Early implementations in smart manufacturing facilities demonstrate 60-70% reductions in communication latency compared to wired alternatives while maintaining five-nines reliability. The ability to support real-time control of robotic systems and AR-assisted maintenance applications positions Wi-Fi 6E as a transformative technology for Industry 4.0 implementations. Market projections indicate industrial applications could account for over 25% of Wi-Fi 6E chip revenues by 2027.

Gaming and XR Ecosystems Drive Premium Consumer Adoption

The consumer gaming market presents a significant opportunity for Wi-Fi 6E, with next-generation consoles and XR headsets demanding more bandwidth than current networks can provide. Cloud gaming platforms require consistent sub-20ms latency to deliver high-quality experiences—a benchmark regularly exceeded by Wi-Fi 6E in controlled tests. Major gaming peripheral manufacturers have begun integrating Wi-Fi 6E capabilities into premium products, with early adopters reporting 2-3 times faster response times in competitive multiplayer environments. As AAA game titles increasingly incorporate VR elements and real-time ray tracing, the performance advantages of Wi-Fi 6E will become increasingly compelling for hardcore gamers.

Integration with 5G Networks Creates Convergence Opportunities

The convergence of Wi-Fi 6E and 5G networks presents substantial growth opportunities for chip manufacturers. Network operators are increasingly deploying architectures that intelligently switch between cellular and Wi-Fi based on application requirements and network conditions. Wi-Fi 6E’s performance characteristics make it particularly suitable for handling data-intensive tasks in these hybrid networks, reducing strain on cellular infrastructure. Several major carriers have begun trials of converged 5G/Wi-Fi 6E solutions that could redefine indoor wireless coverage. This convergence trend is expected to drive demand for multi-mode chipsets that can optimize traffic across both network types.

WI-FI 6E CHIP MARKET TRENDS

Expansion of High-Bandwidth Applications Drives Wi-Fi 6E Adoption

The global Wi-Fi 6E chip market is experiencing robust growth due to increasing demand for high-speed connectivity across multiple industries. Wi-Fi 6E, which operates in the 6 GHz frequency band, offers significantly higher bandwidth and lower latency compared to previous Wi-Fi standards. This makes it ideal for applications such as 4K/8K video streaming, augmented reality (AR), virtual reality (VR), and cloud gaming. The proliferation of smart home devices, industrial IoT applications, and the rise of remote work have further accelerated market adoption. Recent estimates suggest the Wi-Fi 6E chip market will grow at a CAGR of over 15% between 2024 and 2032, with enterprise and consumer segments leading the charge.

Other Trends

Integration in Next-Gen Consumer Electronics

Leading smartphone, laptop, and gaming console manufacturers are rapidly integrating Wi-Fi 6E chips to enhance performance. Flagship devices from major brands now increasingly feature this technology, with penetration expected to exceed 30% in premium consumer electronics by 2025. The demand for seamless, high-bandwidth connectivity in smart TVs, wireless routers, and home automation systems is also contributing to market expansion. Furthermore, as content providers shift toward higher resolution formats, Wi-Fi 6E’s ability to handle multiple high-bandwidth streams simultaneously is becoming a critical differentiator.

Automotive Sector Emerges as Key Growth Area

The automotive industry is adopting Wi-Fi 6E for in-vehicle infotainment systems, connected car technologies, and autonomous driving applications. As vehicles become more data-intensive with advanced telematics and real-time navigation updates, the need for reliable, high-speed wireless connectivity grows substantially. Market projections indicate that automotive Wi-Fi 6E chip shipments could surpass 50 million units annually by 2030, driven by increasing investments in vehicle-to-everything (V2X) communication. Additionally, industrial applications such as smart factories and warehouse automation are leveraging Wi-Fi 6E to support low-latency machine-to-machine communication, a key enabler for Industry 4.0 initiatives.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Semiconductor Giants Dominate the Wi-Fi 6E Chip Market Through Innovation

The competitive landscape of the global Wi-Fi 6E chip market is highly concentrated, with established semiconductor companies leveraging their technological expertise and manufacturing capabilities to capture market share. Qualcomm Technologies has emerged as a dominant player, accounting for approximately 35% of revenue share in 2024, primarily due to its comprehensive portfolio of Wi-Fi 6E solutions for smartphones, routers, and IoT devices.

Broadcom Inc. follows closely with about 28% market share, benefiting from its strong presence in networking equipment and enterprise solutions. The company’s latest Wi-Fi 6E chipsets feature advanced beamforming technology and enhanced multi-user MIMO capabilities, making them particularly suitable for high-density environments.

These industry leaders continue to invest heavily in R&D and strategic collaborations to maintain their competitive edge. For instance, Intel’s partnerships with major OEMs have enabled seamless integration of its Wi-Fi 6E chips into next-generation laptops and PCs, while NXP Semiconductors has focused on automotive and industrial applications through customized solutions.

Meanwhile, emerging players are carving out niches in specific segments, with MediaTek gaining traction in consumer electronics and Qorvo expanding its RF front-end solutions for Wi-Fi 6E devices. This dynamic competition is accelerating innovation across the value chain.

List of Key Wi-Fi 6E Chip Manufacturers

- Qualcomm Technologies, Inc. (U.S.)

- Broadcom Inc. (U.S.)

- Intel Corporation (U.S.)

- NXP Semiconductors N.V. (Netherlands)

- MediaTek Inc. (Taiwan)

- Texas Instruments Incorporated (U.S.)

- ON Semiconductor Corporation (U.S.)

- Qorvo, Inc. (U.S.)

- Microchip Technology Inc. (U.S.)

Segment Analysis:

By Type

6 GHz Band Segment Poised for Rapid Growth Due to Unlicensed Spectrum Availability

The Wi-Fi 6E chip market is segmented based on frequency band types into:

- 2.4 GHz

- Subtypes: Legacy Wi-Fi (802.11b/g/n) compatible chips

- 5 GHz

- 6 GHz

- Subtypes: Tri-band (2.4/5/6 GHz) and dual-band (5/6 GHz) configurations

By Application

Consumer Electronics Segment Leads Due to High Adoption in Smartphones and Laptops

The market is segmented based on application into:

- Industrial Internet of Things (IIoT)

- Automotive

- Consumer Electronics

- Subtypes: Smartphones, laptops, tablets, gaming consoles

- Household Appliances

- Others

By End User

Enterprise Sector Adopting Wi-Fi 6E for High-Density Environments

The market is segmented based on end users into:

- Residential

- Enterprise

- Subtypes: Offices, education, healthcare facilities

- Service Providers

By Architecture

Integrated SoCs Gaining Traction for Compact Device Designs

The market is segmented based on chip architecture into:

- Discrete Chipsets

- Integrated SoCs

- Modular Solutions

Regional Analysis: Wi-Fi 6E Chip Market

North America

As the leading market for Wi-Fi 6E technology, North America benefits from rapid adoption driven by early regulatory approval (FCC allocated the 6GHz band in 2020) and strong demand for high-speed connectivity. The region accounted for over 40% of global Wi-Fi 6E chip sales in 2023, with the US dominating due to enterprise infrastructure upgrades and consumer adoption of 6GHz-enabled routers. Major tech hubs like Silicon Valley and the presence of chip designers (Qualcomm, Broadcom, Intel) accelerate innovation. However, supply chain constraints continue affecting production timelines, while price sensitivity in consumer markets may slow widespread adoption.

Europe

Europe’s Wi-Fi 6E chip market grows steadily under supportive EU policies, though delayed spectrum allocation in key nations until 2023 created initial barriers. Germany and the UK lead regional adoption, with industrial IoT applications driving 30% year-over-year growth in chip demand. Strict data security laws push development of specialized enterprise solutions, while consumer adoption lags due to higher device costs. Competition from wired alternatives in commercial settings remains a challenge, though upcoming smart city projects in Barcelona, Berlin, and Amsterdam present significant opportunities.

Asia-Pacific

The fastest-growing Wi-Fi 6E market, Asia-Pacific shows divergent trends: While Japan and South Korea lead in early adoption (with government-backed 6GHz trials since 2021), China’s delayed spectrum approval limits growth despite massive manufacturing capacity. India emerges as a wildcard with projected 45% CAGR through 2030, fueled by digital infrastructure projects. Price competition from domestic chipmakers pressures global suppliers, while smartphone OEMs increasingly integrate 6E capabilities in premium models across Southeast Asia. Infrastructure gaps in rural areas may delay nationwide implementation.

South America

Market development remains in early stages, with Brazil and Chile making progressive spectrum allocations in 2023-24. Economic instability limits consumer adoption, though enterprise demand grows for industrial and agricultural IoT applications where wired solutions are impractical. Regional chip sales currently represent under 5% of global volume, but partnerships between telecom providers and equipment manufacturers signal long-term potential. Infrastructure challenges and import dependency continue restraining faster growth across most nations.

Middle East & Africa

The niche market shows promise in Gulf states (UAE, Saudi Arabia) where smart city initiatives drive early 6GHz deployments. Special economic zones utilize Wi-Fi 6E for high-density commercial applications, though consumer adoption remains minimal. Africa’s growth hinges on improving baseline connectivity – while South Africa and Nigeria test 6GHz applications, most nations prioritize fundamental network expansion. Chip sales currently focus on enterprise-grade equipment imports, with projected growth accelerating post-2025 as regional infrastructure matures.

Report Scope

This market research report provides a comprehensive analysis of the Global Wi-Fi 6E Chip market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Wi-Fi 6E Chip market was valued at US$ 2,890 million in 2024 and is projected to reach US$ 8,940 million by 2032, growing at a CAGR of 17.3 % during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (2.4 GHz, 5 GHz, 6 GHz), application (Industrial IoT, Automotive, Consumer Electronics, Household Appliances, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis of key markets including the US, China, Japan, and Germany.

- Competitive Landscape: Profiles of leading market participants including Broadcomm, Qualcomm, Intel, and NXP, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Analysis of emerging Wi-Fi 6E technologies, integration with 5G networks, and advancements in semiconductor design and fabrication.

- Market Drivers & Restraints: Evaluation of factors such as increasing demand for high-speed connectivity, growth in IoT applications, alongside challenges like spectrum allocation and regulatory hurdles.

- Stakeholder Analysis: Strategic insights for chip manufacturers, device OEMs, network equipment providers, and investors regarding market opportunities and competitive positioning.

The report employs rigorous primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Wi-Fi 6E Chip Market?

-> Wi-Fi 6E Chip Market size was valued at US$ 2,890 million in 2024 and is projected to reach US$ 8,940 million by 2032, at a CAGR of 17.3% during the forecast period 2025-2032.

Which key companies operate in Global Wi-Fi 6E Chip Market?

-> Key players include Broadcomm, Qualcomm, Intel, and NXP, among other leading semiconductor manufacturers.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-speed wireless connectivity, proliferation of IoT devices, and increasing adoption in consumer electronics and automotive applications.

Which region dominates the market?

-> Asia-Pacific is the largest market, driven by semiconductor manufacturing in China, South Korea, and Taiwan, while North America leads in technology adoption.

What are the emerging trends?

-> Emerging trends include integration with 5G networks, development of Wi-Fi 6E enabled smart home devices, and advancements in chip fabrication technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...