MARKET INSIGHTS

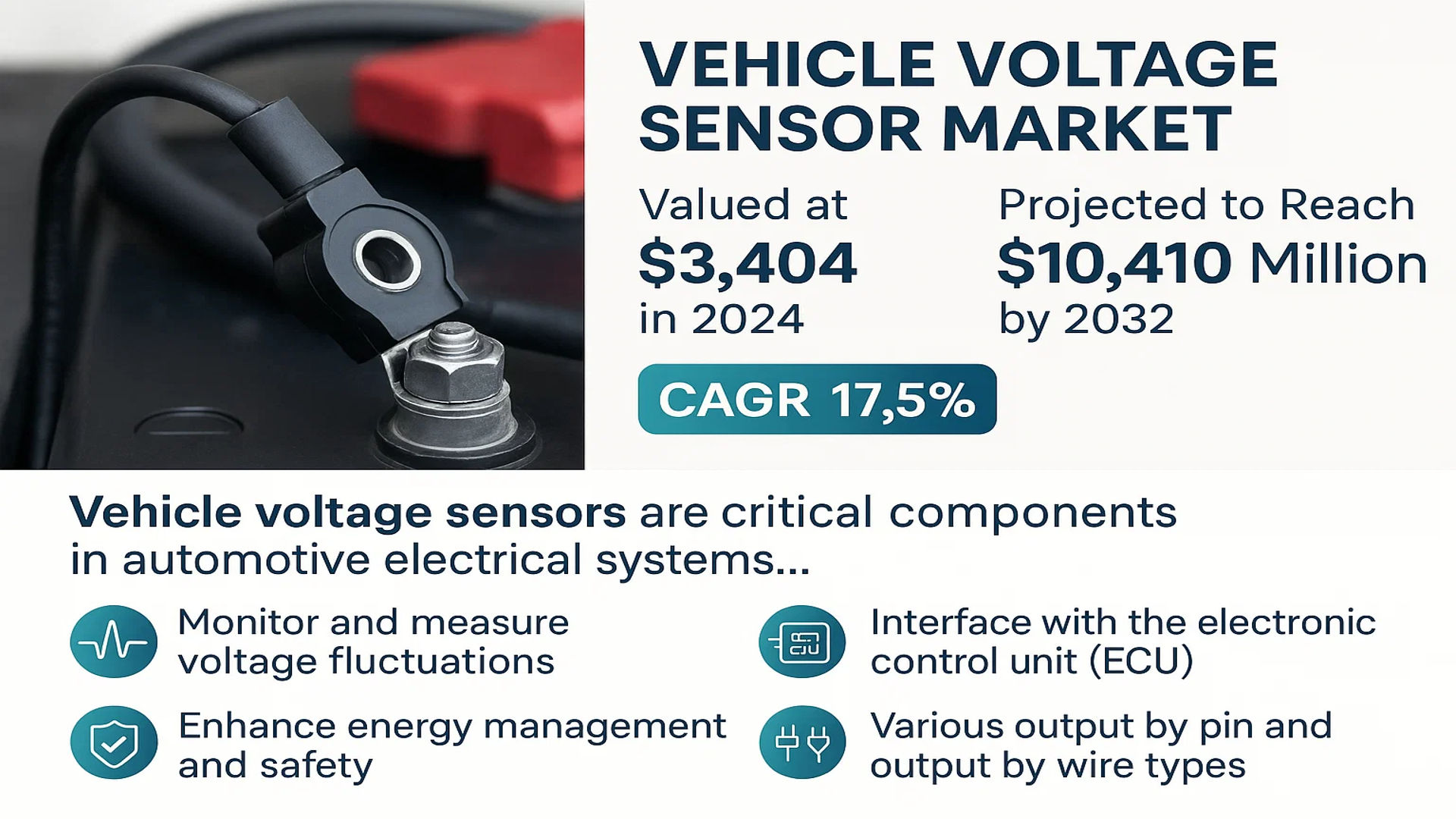

The global Vehicle Voltage Sensor Market was valued at 3404 million in 2024 and is projected to reach US$ 10410 million by 2032, at a CAGR of 17.5% during the forecast period.

Vehicle voltage sensors are critical components in automotive electrical systems, designed to monitor and measure voltage fluctuations in batteries, power supplies, and other electrical equipment. These sensors enable real-time voltage detection, helping assess battery health, charging system performance, and overall vehicle electrical stability. They interface with the vehicle’s electronic control unit (ECU) to optimize energy management and enhance safety. Modern voltage sensors come in various configurations, including output by pin and output by wire types, catering to different automotive applications.

The market growth is driven by increasing vehicle electrification, stringent emission norms, and rising demand for advanced battery management systems. Furthermore, the shift toward electric vehicles (EVs) and hybrid electric vehicles (HEVs) is accelerating adoption, as voltage monitoring becomes essential for efficient power distribution. Key players like Renesas Electronics, TE Connectivity, and Omron are investing in R&D to develop high-precision sensors, while regional markets such as China and the U.S. contribute significantly to revenue growth. The passenger vehicle segment currently dominates application-wise, though commercial vehicles are expected to gain traction due to fleet electrification trends.

MARKET DYNAMICS

MARKET DRIVERS

Electrification of Vehicles and Rising Adoption of ADAS to Fuel Market Expansion

The global push toward vehicle electrification is significantly driving demand for voltage sensors in automotive applications. With electric vehicle sales growing at an unprecedented rate, the need for accurate battery monitoring systems has become critical. Voltage sensors play a pivotal role in battery management systems (BMS), ensuring optimal performance and safety of lithium-ion batteries. The integration of these sensors helps prevent overcharging and deep discharging, which are crucial for extending battery life in EVs. As governments worldwide implement stringent emission norms, automakers are accelerating their electrification roadmaps, directly benefiting the voltage sensor market.

Increasing Vehicle Electronics Complexity Creates Demand for Precise Voltage Monitoring

Modern vehicles incorporate an expanding array of electronic components, from infotainment systems to advanced driver assistance systems (ADAS). This proliferation of electronics requires robust power management solutions where voltage sensors ensure stable operation across all systems. The average luxury vehicle now contains over 100 electronic control units, each requiring precise voltage regulation. Voltage sensing technology has become indispensable for maintaining system reliability, particularly in safety-critical applications like brake-by-wire and steer-by-wire systems. This trend toward vehicle electronics consolidation and domain controller architectures will continue to drive sensor adoption.

➤ For instance, the transition to 48V electrical systems in mild hybrid vehicles creates additional demand for high-precision voltage sensors capable of operating across wider voltage ranges.

Furthermore, the automotive industry’s focus on predictive maintenance and vehicle health monitoring is opening new opportunities for voltage sensing applications. Real-time voltage monitoring enables early detection of electrical system faults, reducing warranty costs and improving customer satisfaction.

MARKET RESTRAINTS

Price Pressure and Commoditization Challenges in Mass Vehicle Segments

While demand grows, the vehicle voltage sensor market faces intense pricing pressures, particularly in mainstream passenger vehicle segments. Automakers continually drive component cost reductions to maintain profitability in competitive markets. This creates challenges for sensor manufacturers to deliver advanced features while meeting aggressive cost targets. The trend toward standardization and platform sharing in vehicle architectures further exacerbates this situation, limiting differentiation opportunities for sensor suppliers.

Other Restraints

Integration Challenges with Legacy Systems

The automotive industry’s long product lifecycles mean voltage sensors must maintain compatibility with older vehicle architectures while supporting new technologies. This dual requirement increases development complexity and costs. Many existing vehicle platforms were not designed with modern sensor integration in mind, creating implementation challenges for OEMs and tier-1 suppliers.

Technical Limitations in Extreme Conditions

Voltage sensors must operate reliably across harsh automotive environments, from extreme temperatures to electromagnetic interference. Meeting these stringent requirements while maintaining accuracy and long-term stability remains a persistent challenge for the industry, particularly for safety-critical applications.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Semiconductor Shortages Impact Market Stability

The vehicle voltage sensor market continues to grapple with supply chain disruptions that emerged during the global semiconductor shortage. These components rely heavily on specialty semiconductors and packaging technologies that experienced significant supply constraints. While conditions have improved, the industry remains vulnerable to geopolitical tensions and raw material availability. Sensor manufacturers must navigate these challenges while meeting growing demand from automakers ramping up production post-pandemic.

Other Challenges

Cybersecurity Concerns in Connected Vehicles

As vehicles become more connected, voltage sensors are increasingly integrated into vehicle networks that could potentially be vulnerable to cyber threats. Ensuring the security of these components without compromising performance adds another layer of complexity to product development.

Rapid Technology Obsolescence

The fast pace of automotive electronics innovation creates challenges for sensor lifecycle management. Products must be designed to accommodate future vehicle architectures while providing long-term availability for current platforms, a difficult balance for suppliers to maintain.

MARKET OPPORTUNITIES

Vehicle-to-Grid Integration and Smart Charging Create New Application Areas

The emerging vehicle-to-grid (V2G) ecosystem presents significant opportunities for advanced voltage sensing solutions. As bi-directional charging becomes more prevalent, precise voltage monitoring will be critical for managing power flows between vehicles and charging infrastructure. The development of smart charging systems and energy management solutions for EV fleets will further drive demand for sophisticated voltage sensing technologies.

Expansion into Emerging Markets with Growing Automotive Production

Developing economies are seeing rapid growth in vehicle production and electrification initiatives. Localization of automotive supply chains in these regions creates opportunities for voltage sensor manufacturers to establish production facilities and technical support capabilities. Government incentives for domestic EV manufacturing in several Asian markets are particularly promising for component suppliers able to meet local content requirements.

➤ The integration of voltage sensors with AI-based predictive maintenance systems represents another high-potential growth area, enabling proactive fault detection and optimized vehicle performance.

Furthermore, the development of modular and scalable sensor architectures allows for cost-effective adaptation across various vehicle platforms, providing suppliers with opportunities to increase content per vehicle while maintaining production efficiency.

VEHICLE VOLTAGE SENSOR MARKET TRENDS

Surge in Electric and Hybrid Vehicle Adoption Driving Market Growth

The global Vehicle Voltage Sensor market has been experiencing robust growth, with projections indicating a compound annual growth rate (CAGR) of 17.5% from 2024 to 2032, reaching an estimated market value of $10.41 billion by the end of the forecast period. This growth is largely attributed to the accelerating adoption of electric and hybrid vehicles worldwide, where precise voltage monitoring is critical for battery management systems. Modern vehicles are increasingly incorporating complex electrical architectures, necessitating advanced sensors to ensure optimal performance and safety. Furthermore, government mandates for vehicle electrification in regions like Europe and China are creating favorable conditions for market expansion.

Other Trends

Technological Advancements in Sensor Accuracy and Miniaturization

Innovations in voltage sensor technology have significantly improved accuracy, response time, and durability while reducing their physical footprint. Manufacturers are focusing on developing non-contact voltage sensors and integrating advanced signal processing algorithms to minimize energy losses and improve reliability. The shift toward smart sensors capable of real-time data transmission to vehicle ECUs is also gaining momentum, supporting predictive maintenance and enhancing overall vehicle efficiency. These advancements are particularly crucial for autonomous vehicles, where electrical system reliability directly impacts operational safety.

Growing Demand for Enhanced Vehicle Diagnostics and Predictive Maintenance

The automotive industry’s increasing emphasis on predictive maintenance solutions is creating new opportunities for voltage sensor manufacturers. Modern sensors provide continuous voltage monitoring, enabling early detection of electrical system faults before they escalate into critical failures. This capability is especially valuable for commercial fleets, where unplanned downtime can have significant economic consequences. The integration of voltage sensor data with telematics systems allows fleet operators to optimize battery replacement schedules and reduce overall maintenance costs. Additionally, the rising penetration of connected car technologies is expected to further amplify demand for sophisticated voltage monitoring solutions across all vehicle segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Market Leadership in Vehicle Voltage Sensor Space

The global vehicle voltage sensor market features a dynamic competitive environment with both established multinational corporations and emerging regional players vying for market share. Renesas Electronics currently leads the market, commanding a significant portion of revenue share in 2024, primarily due to its comprehensive product portfolio and strong OEM relationships across multiple automotive sectors. Their technological edge in integrated circuit design gives them particular advantage in precision voltage measurement solutions.

Omron Corporation and TE Connectivity follow closely, having strengthened their positions through continuous R&D investments and strategic acquisitions. Omron’s strength lies in its compact sensor designs ideal for electric vehicles, while TE Connectivity dominates in ruggedized solutions for commercial vehicle applications. Both companies have reported above-market growth rates due to their focus on customized solutions for EV battery management systems.

The competitive intensity is further heightened by Chinese manufacturers like BYD and Shenzhen BJXK, who are rapidly gaining traction through cost-effective solutions tailored for Asia-Pacific markets. These companies benefit from strong domestic supply chains and government support in China’s booming EV sector. Meanwhile, European players such as LEM Holding SA maintain technological superiority in high-accuracy measurement solutions, particularly for luxury and performance vehicle segments.

Several players are adopting innovative strategies to differentiate themselves. Novosense recently launched a breakthrough contactless voltage sensing technology, while ABLIC Inc. focuses on ultra-low power consumption sensors for hybrid vehicles. Such specialized offerings help companies carve out niche markets and defend against pricing pressures in standard product categories.

List of Key Vehicle Voltage Sensor Manufacturers Profiled

- Renesas Electronics Corporation (Japan)

- Omron Corporation (Japan)

- TE Connectivity Ltd. (Switzerland)

- LEM Holding SA (Switzerland)

- BYD Company Ltd. (China)

- Shenzhen BJXK Technology Co., Ltd. (China)

- ABLIC Inc. (Japan)

- Pemch Technology Co., Ltd. (China)

- Novosense Microelectronics (China)

- Panasonic Corporation (Japan)

Segment Analysis:

By Type

Output by Pin Segment Leads Due to Higher Integration in Modern Automotive Electronics

The market is segmented based on type into:

- Output by Pin

- Subtypes: 3-pin, 4-pin, and others

- Output by Wire

- Subtypes: Single-wire, Multi-wire, and others

- Others

By Application

Passenger Vehicles Segment Dominates Owing to Increasing Demand for Advanced Safety Features

The market is segmented based on application into:

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Others

By Technology

Digital Voltage Sensors Gain Traction Due to Improved Accuracy and Connectivity

The market is segmented based on technology into:

- Analog Voltage Sensors

- Digital Voltage Sensors

- Hybrid Voltage Sensors

By Vehicle Type

Electric Vehicles Show Significant Growth Potential for Voltage Sensors

The market is segmented based on vehicle type into:

- Internal Combustion Engine Vehicles

- Hybrid Electric Vehicles

- Plug-in Hybrid Electric Vehicles

- Battery Electric Vehicles

Regional Analysis: Vehicle Voltage Sensor Market

Asia-Pacific

The Asia-Pacific region dominates the global Vehicle Voltage Sensor market, driven by rapid automotive production, increasing electrification of vehicles, and strong government support for EV adoption. China, Japan, and South Korea are the key contributors, accounting for over 60% of regional demand. China’s aggressive push toward new energy vehicles (NEVs) under its ‘Made in China 2025’ initiative has significantly boosted sensor adoption. Japan’s technological advancements in hybrid vehicles and South Korea’s robust semiconductor industry further solidify the region’s leadership. Local manufacturers like Shenzhen BJXK and BYD play a critical role in supplying cost-effective solutions, while global players like Renesas Electronics and Omron maintain strong partnerships with automakers.

North America

Stringent emissions regulations and growing EV investments shape the Vehicle Voltage Sensor market in North America. The U.S. leads with initiatives like the Bipartisan Infrastructure Law, which allocates $7.5 billion for EV charging infrastructure, indirectly driving sensor demand. Canada and Mexico are gradually catching up, with increasing automotive manufacturing activities. The presence of TE Connectivity and LEM Sensors ensures high-quality sensor supply for both passenger and commercial vehicles. However, higher costs of advanced voltage sensors remain a challenge for widespread adoption in budget-sensitive segments.

Europe

Europe stands as a key market due to strict Euro 7 emissions norms and rapid EV adoption. Germany and France spearhead demand, supported by automakers like Volkswagen and Renault, who rely on precision sensors for battery management systems. The region also benefits from the presence of ABLIC and Crosschip Micro, which focus on high-performance, low-power sensors. Policy frameworks like the European Green Deal accelerate the transition to electrified mobility, further fueling market growth. Despite this, supply chain disruptions and semiconductor shortages occasionally hinder production scalability.

South America

South America’s Vehicle Voltage Sensor market is nascent but growing, primarily driven by Brazil and Argentina. The region’s cost-sensitive automotive sector favors Output by Pin sensors for their affordability, though adoption in EVs remains limited. Economic instability and underdeveloped charging infrastructure slow down progress, but local assembly plants and foreign investments offer long-term potential. Manufacturers are gradually shifting toward Output by Wire sensors for modern vehicle models, aligning with global trends.

Middle East & Africa

The market in this region is emerging, with growth concentrated in the GCC countries, particularly the UAE and Saudi Arabia. Luxury vehicle sales and infrastructural developments in smart cities drive demand for advanced sensors. However, weak regulatory frameworks and low EV penetration restrict large-scale adoption. Partnerships with global suppliers like Panasonic and gradual investments in local manufacturing hint at future opportunities, especially for commercial fleet electrification.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Vehicle Voltage Sensor markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Vehicle Voltage Sensor market was valued at USD 3,404 million in 2024 and is projected to reach USD 10,410 million by 2032, growing at a CAGR of 17.5%.

- Segmentation Analysis: Detailed breakdown by product type (Output by Pin, Output by Wire), application (Passenger Vehicles, Commercial Vehicles), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis for key markets like the U.S., China, Germany, and Japan.

- Competitive Landscape: Profiles of leading market participants including Renesas Electronics, Omron, TE Connectivity, LEM sensor, and BYD, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with vehicle ECUs, and advancements in battery management systems.

- Market Drivers & Restraints: Evaluation of factors such as electric vehicle adoption, automotive electronics growth, and supply chain challenges.

- Stakeholder Analysis: Strategic insights for automotive OEMs, sensor manufacturers, component suppliers, and investors.

The research employs both primary and secondary methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Vehicle Voltage Sensor Market?

-> Vehicle Voltage Sensor Market was valued at 3404 million in 2024 and is projected to reach US$ 10410 million by 2032, at a CAGR of 17.5% during the forecast period.

Which key companies operate in Global Vehicle Voltage Sensor Market?

-> Key players include Renesas Electronics, Omron, TE Connectivity, LEM sensor, Shenzhen BJXK, Pemch, ABLIC, BYD, Novosense, and Crosschip Micro.

What are the key growth drivers?

-> Key growth drivers include rising electric vehicle production, increasing automotive electronics integration, and stringent vehicle safety regulations.

Which region dominates the market?

-> Asia-Pacific is the largest market, led by China’s automotive manufacturing sector, while North America shows strong growth potential.

What are the emerging trends?

-> Emerging trends include integration with advanced battery management systems, development of multi-functional sensors, and adoption in autonomous vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...