MARKET INSIGHTS

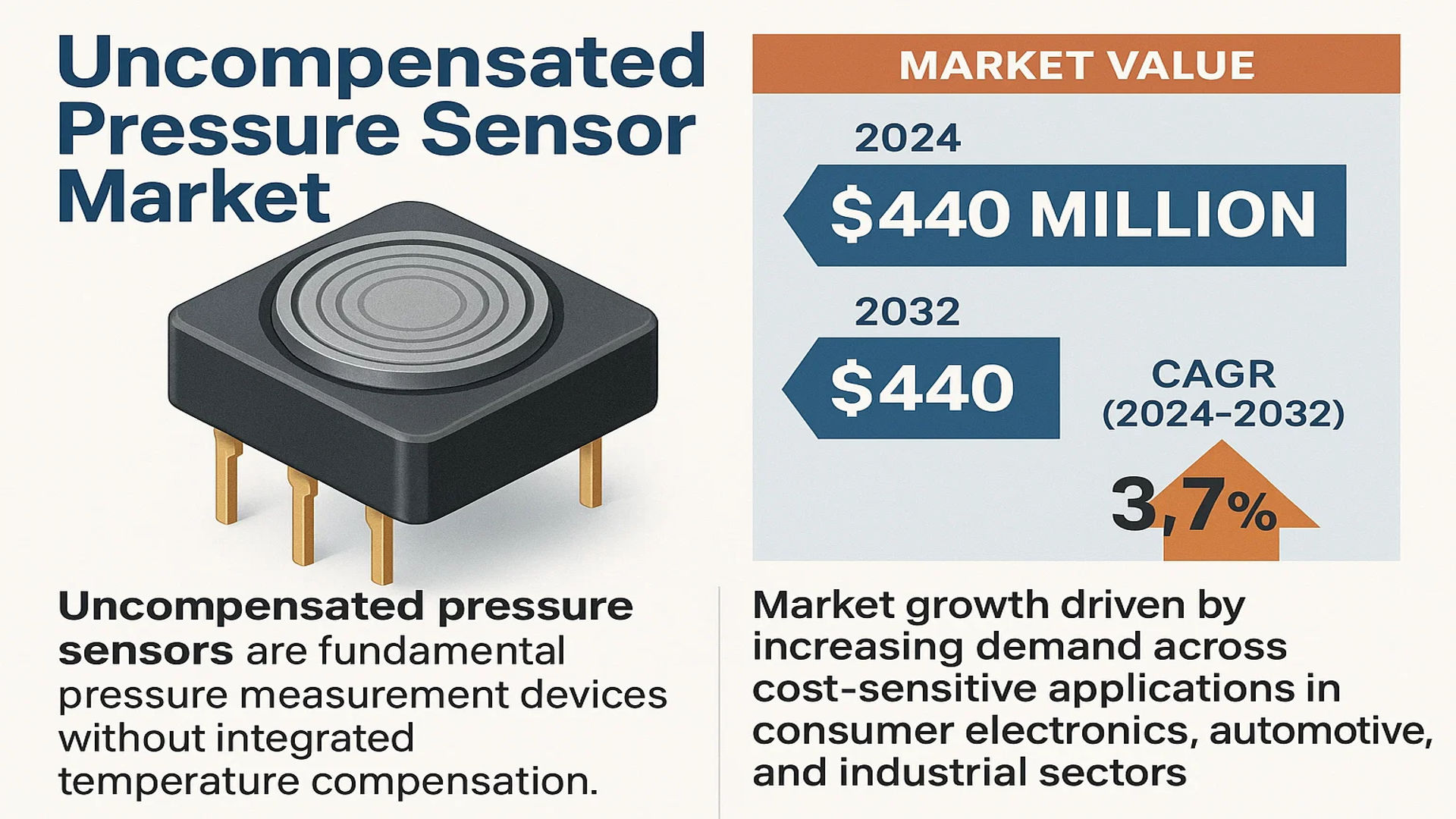

The global Uncompensated Pressure Sensor market was valued at 343 million in 2024 and is projected to reach US$ 440 million by 2032, at a CAGR of 3.7% during the forecast period.

Uncompensated pressure sensors are fundamental pressure measurement devices that directly convert pressure variations into electrical signals without integrated temperature compensation. These sensors operate by detecting deformation or capacitive changes in their sensing elements when subjected to pressure, generating an output proportional to the applied force. While cost-effective, their accuracy may be affected by temperature fluctuations, requiring additional corrective measures in environments with significant thermal variations.

The market growth is driven by increasing demand across cost-sensitive applications in consumer electronics, automotive, and industrial sectors. Furthermore, technological advancements in microelectromechanical systems (MEMS) are enabling wider adoption, particularly in emerging economies. Key players such as NXP, TE Connectivity, and Honeywell dominate the competitive landscape, collectively holding significant market share through continuous product innovation and strategic collaborations.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Industrial Automation to Accelerate Demand for Uncompensated Pressure Sensors

The global industrial automation market has witnessed consistent growth, with automation penetration levels reaching nearly 35% across manufacturing sectors. Uncompensated pressure sensors serve as cost-effective solutions for basic pressure monitoring requirements in automated systems. Their simplicity and reliability make them particularly suitable for high-volume applications where temperature variations remain controlled. The automotive manufacturing sector alone accounts for approximately 25% of industrial sensor demand, with pressure sensors playing a crucial role in hydraulic systems, pneumatic controls, and process monitoring.

Expanding IoT Ecosystem Creates New Application Areas

With over 15 billion IoT devices currently deployed worldwide, the demand for basic sensing solutions has grown exponentially. Uncompensated pressure sensors offer an economical means to integrate pressure monitoring capabilities into cost-sensitive IoT applications. Their straightforward design and compatibility with various microcontrollers have made them attractive for smart home appliances, basic environmental monitoring systems, and entry-level industrial IoT implementations. The consumer electronics segment has shown particular interest, with pressure sensors increasingly being incorporated into wearable devices and smartphones for basic altitude and activity tracking.

Cost-Sensitive Applications Drive Adoption in Emerging Markets

In price-conscious markets, particularly across Asia-Pacific and Latin America, uncompensated pressure sensors have gained significant traction. Their price point, typically 30-40% lower than compensated alternatives, makes them accessible for applications where absolute precision isn’t critical. This has led to widespread adoption in white goods manufacturing, basic automotive systems, and entry-level industrial equipment. The medical devices sector has also shown interest in these sensors for disposable and single-use applications where cost containment is paramount.

MARKET RESTRAINTS

Temperature Sensitivity Limits Application Scope

The inherent temperature dependence of uncompensated pressure sensors presents a significant constraint on market growth. Their output drift with temperature variations, often in the range of ±1-2% per °C, makes them unsuitable for applications experiencing wide thermal swings. This limitation becomes particularly problematic in automotive and aerospace applications where ambient temperature variations can exceed 100°C during operation. As industries increasingly demand more robust measurement solutions, many are willing to pay the premium for temperature-compensated alternatives.

Growing Demand for Smart Sensors Reduces Market Share

The sensor market is evolving toward more intelligent, networked solutions that provide additional diagnostic capabilities. Smart sensors, incorporating onboard compensation and digital interfaces, now account for approximately 45% of the industrial pressure sensor market. This trend has gradually eroded the market position of basic uncompensated sensors in applications where data integrity and additional functionality are prioritized over pure cost considerations.

MARKET CHALLENGES

Intense Price Pressure from Asian Manufacturers

The global pressure sensor market has witnessed increasing commoditization, with Asian manufacturers offering uncompensated pressure sensors at price points up to 50% lower than their Western counterparts. This pricing pressure has forced established players to either reduce margins or exit certain market segments entirely. The situation is particularly challenging for manufacturers targeting cost-sensitive applications where differentiation beyond price becomes difficult.

Supply Chain Vulnerabilities Impact Production Consistency

The sensor manufacturing process depends heavily on stable access to specialized materials and substrates. Recent disruptions in the semiconductor supply chain have exposed vulnerabilities, with lead times for certain critical components extending beyond 30 weeks. These challenges have made it difficult for manufacturers to maintain consistent production schedules and delivery commitments, particularly for high-volume orders.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy Systems

The rapid expansion of renewable energy infrastructure presents new opportunities for uncompensated pressure sensors. Wind turbine hydraulic systems and basic solar thermal installations increasingly incorporate these sensors for cost-effective pressure monitoring. With global renewable energy capacity expected to grow by 60% over the next decade, this sector could become a significant new market for uncompensated pressure sensor manufacturers.

Advancements in Packaging Technologies Expand Possibilities

Recent improvements in sensor packaging have helped mitigate some temperature-related limitations of uncompensated designs. New encapsulation materials and mounting techniques have reduced thermal sensitivity by approximately 30% in certain applications. These packaging innovations may allow uncompensated sensors to penetrate applications previously considered beyond their performance envelope.

Collaborative Development Models Strengthen Market Position

Leading manufacturers are increasingly collaborating with end-users to develop application-specific uncompensated sensor solutions. These partnerships have proven particularly successful in HVAC systems and consumer appliances, where custom calibration at the factory can compensate for known environmental conditions. Such collaborative approaches help maintain relevance in an increasingly competitive market.

UNCOMPENSATED PRESSURE SENSOR MARKET TRENDS

Cost-Effectiveness Drives Adoption in Industrial and Consumer Electronics Applications

The uncompensated pressure sensor market is witnessing significant growth due to its cost-effectiveness, particularly in industrial automation and consumer electronics. These sensors, which lack integrated temperature compensation, are more affordable than their compensated counterparts, making them ideal for budget-sensitive applications. While accuracy may be impacted by temperature fluctuations, their simplicity and lower production costs position them favorably in high-volume manufacturing scenarios. The industrial sector accounted for a major share of revenue in 2024, with manufacturers prioritizing cost-efficient solutions for HVAC systems, process monitoring, and hydraulic equipment. Automation trends are accelerating demand, though precision-critical applications still favor compensated alternatives.

Other Trends

Miniaturization of Pressure Sensing Components

The demand for compact electronic devices is driving innovation in uncompensated pressure sensor designs. Manufacturers are developing smaller form-factor sensors that maintain adequate performance for applications where space constraints outweigh precision requirements. The automotive industry is adopting these miniaturized sensors for non-critical systems such as cabin pressure monitoring, while consumer electronics brands integrate them into wearables and smartphones. Design improvements like MEMS-based solutions are enabling smaller footprints, though challenges remain in maintaining signal integrity without compensation circuitry. The miniaturization trend aligns with the broader electronics industry movement toward space-efficient components.

Developing Markets Show Faster Growth Potential

While mature markets like North America and Europe demonstrate steady adoption, developing regions are emerging as high-growth areas for uncompensated pressure sensors. Price sensitivity in markets such as Southeast Asia and parts of Latin America makes these cost-effective solutions particularly attractive for local manufacturers. The Asia Pacific region, excluding China and Japan, is projected to grow at above-average rates through 2032, supported by expanding industrial bases and rising electronics production. However, quality perception challenges persist in some applications, requiring careful market positioning by manufacturers. Government initiatives supporting local electronics manufacturing in these regions are creating additional demand drivers for affordable sensor technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Global Supply Chains Define Market Competition

The global uncompensated pressure sensor market features a mix of established semiconductor manufacturers and specialized sensor producers. NXP Semiconductors leads with its comprehensive MEMS pressure sensor portfolio, benefitting from strong automotive and industrial sector partnerships. Their market dominance is reinforced by continuous R&D investment, with the company allocating approximately 15% of annual revenue to development efforts.

While NXP holds technological leadership, TE Connectivity and Honeywell compete aggressively through application-specific solutions. TE Connectivity’s diversified industrial sensor range captured significant market share in 2024, particularly in medical and HVAC applications where their cost-efficient uncompensated sensors gained traction. Honeywell maintains competitive advantage through aerospace and defense contracts, though these sectors represent smaller portions of the overall uncompensated sensor market.

Mid-sized players like Bourns and Merit Sensor differentiate themselves through price competitiveness and regional specialization. Bourns has strengthened its position in Asian consumer electronics markets, while Merit Sensor focuses on custom sensor solutions for industrial automation clients. These companies leverage faster product iteration cycles compared to larger competitors, allowing quicker adaptation to emerging application needs.

Emerging Chinese manufacturer Memsensing Microsystems demonstrates rapid growth, particularly in domestic markets where government support helps local firms compete internationally. Their recent capacity expansion in Suzhou positions them as a serious contender for Asia-Pacific market leadership by 2030. Meanwhile, joint ventures between sensor manufacturers and automotive suppliers are reshaping competitive dynamics, as seen in Fujikura’s partnership with a major Japanese automaker announced in early 2024.

List of Key Uncompensated Pressure Sensor Companies Profiled

- NXP Semiconductors (Netherlands)

- TE Connectivity (Switzerland)

- Bourns, Inc. (U.S.)

- Fujikura Ltd. (Japan)

- Merit Sensor Systems (U.S.)

- Honeywell International Inc. (U.S.)

- Memsensing Microsystems (China)

Segment Analysis:

By Type

Gauge Pressure Sensor Segment Leads Due to Widespread Industrial and HVAC Applications

The market is segmented based on type into:

- Gauge Pressure Sensor

- Subtypes: Digital Output, Analog Output

- Differential Pressure Sensor

- Subtypes: High Accuracy, Standard

- Absolute Pressure Sensors

- Others

By Application

Industrial Segment Dominates Due to High Demand in Process Control and Automation

The market is segmented based on application into:

- Consumer Electronics

- Medical

- Industrial

- Automotive

- Others

By Sensing Technology

Piezoresistive Technology Remains Prevalent Due to Cost-Effectiveness

The market is segmented based on sensing technology into:

- Piezoresistive

- Capacitive

- Optical

- Resonant

Regional Analysis: Uncompensated Pressure Sensor Market

Asia-Pacific

The Asia-Pacific region dominates the global uncompensated pressure sensor market, accounting for the largest revenue share due to rapid industrialization and widespread adoption in consumer electronics, automotive, and industrial applications. China is the key growth engine, driven by its extensive manufacturing capabilities and cost-driven demand for budget-friendly sensing solutions. The country’s emphasis on IoT and smart device proliferation further boosts adoption. India and Southeast Asia show increasing potential as local manufacturing expands, though price sensitivity remains a primary factor in product selection. While high-precision applications still prefer compensated variants, the affordability of uncompensated sensors makes them ideal for mass-produced goods in this region.

North America

North America represents a technologically advanced market where uncompensated pressure sensors find niche applications in cost-constrained segments of industrial automation and HVAC systems. The U.S. leads regional demand, with manufacturers balancing between performance requirements and budget considerations. Medical device OEMs occasionally utilize these sensors in non-critical monitoring equipment where temperature fluctuations are minimal. Graduate adoption persists in automotive tire pressure monitoring and white goods, though stricter accuracy standards in sectors like aerospace limit broader penetration. Innovation focuses on improving baseline performance of uncompensated variants to bridge the gap with premium alternatives.

Europe

European demand for uncompensated pressure sensors centers on industrial equipment and appliance manufacturers seeking reliable yet economical solutions. Germany and France lead consumption, particularly in pneumatic systems and hydraulic controls where moderate precision suffices. The market faces constraints due to the region’s preference for high-accuracy sensing technologies in automotive and medical applications. However, recent supply chain reevaluations have prompted some manufacturers to consider uncompensated sensors for secondary systems to reduce overall production costs. Environmental sensor manufacturers also utilize these components in basic weather monitoring stations where occasional calibration proves acceptable.

South America

South America presents a developing market where price sensitivity drives adoption of uncompensated pressure sensors, particularly in Brazil’s growing automotive manufacturing sector and Argentina’s industrial equipment production. Market growth remains tempered by economic volatility and preference for imported compensated sensors in critical applications. Local manufacturers increasingly incorporate these sensors in consumer appliances and agricultural equipment, valuing their cost-effectiveness over absolute precision. The lack of stringent performance regulations in many end-use sectors supports continued adoption, particularly for non-safety-related functions where minor measurement variances are tolerable.

Middle East & Africa

This emerging market shows gradual uptake of uncompensated pressure sensors, primarily in oil & gas monitoring equipment and basic industrial controls. GCC countries demonstrate higher adoption rates due to active infrastructure development, while African nations face slower growth due to limited manufacturing bases. The region’s extreme temperature variations sometimes challenge uncompensated sensor performance, leading to selective usage in climate-controlled environments. Water management systems and building automation represent growth areas as urbanization accelerates, with cost considerations outweighing precision requirements in many projects.

Report Scope

This market research report provides a comprehensive analysis of the Global Uncompensated Pressure Sensor Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 343 million in 2024 and is projected to reach USD 440 million by 2032, growing at a CAGR of 3.7%.

- Segmentation Analysis: Detailed breakdown by product type (Gauge Pressure Sensor, Differential Pressure Sensor, Absolute Pressure Sensors), application (Consumer Electronics, Medical, Industrial, Automotive, Others), and end-user industry.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. and China represent key growth markets.

- Competitive Landscape: Profiles of leading market participants including NXP, TE Connectivity, Bourns, Fujikura, Merit Sensor, Honeywell, and Memsensing Microsystems (Suzhou), covering their market share, product portfolios, and strategic initiatives.

- Technology Trends & Innovation: Assessment of sensor miniaturization, MEMS technology adoption, and integration with IoT platforms.

- Market Drivers & Restraints: Evaluation of factors including cost-effectiveness in industrial applications, automotive sector demand, and challenges from temperature sensitivity limitations.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, OEMs, system integrators, and investors regarding emerging opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data from reputable sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Uncompensated Pressure Sensor Market?

-> Uncompensated Pressure Sensor market was valued at 343 million in 2024 and is projected to reach US$ 440 million by 2032, at a CAGR of 3.7% during the forecast period.

Which key companies operate in this market?

-> Key players include NXP, TE Connectivity, Bourns, Fujikura, Merit Sensor, Honeywell, and Memsensing Microsystems (Suzhou).

What are the key growth drivers?

-> Growth is driven by cost-sensitive industrial applications, automotive sector demand, and increasing adoption in consumer electronics.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America maintains significant market share due to industrial automation trends.

What are the emerging trends?

-> Emerging trends include MEMS technology integration, IoT connectivity, and development of hybrid sensor solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...