MARKET INSIGHTS

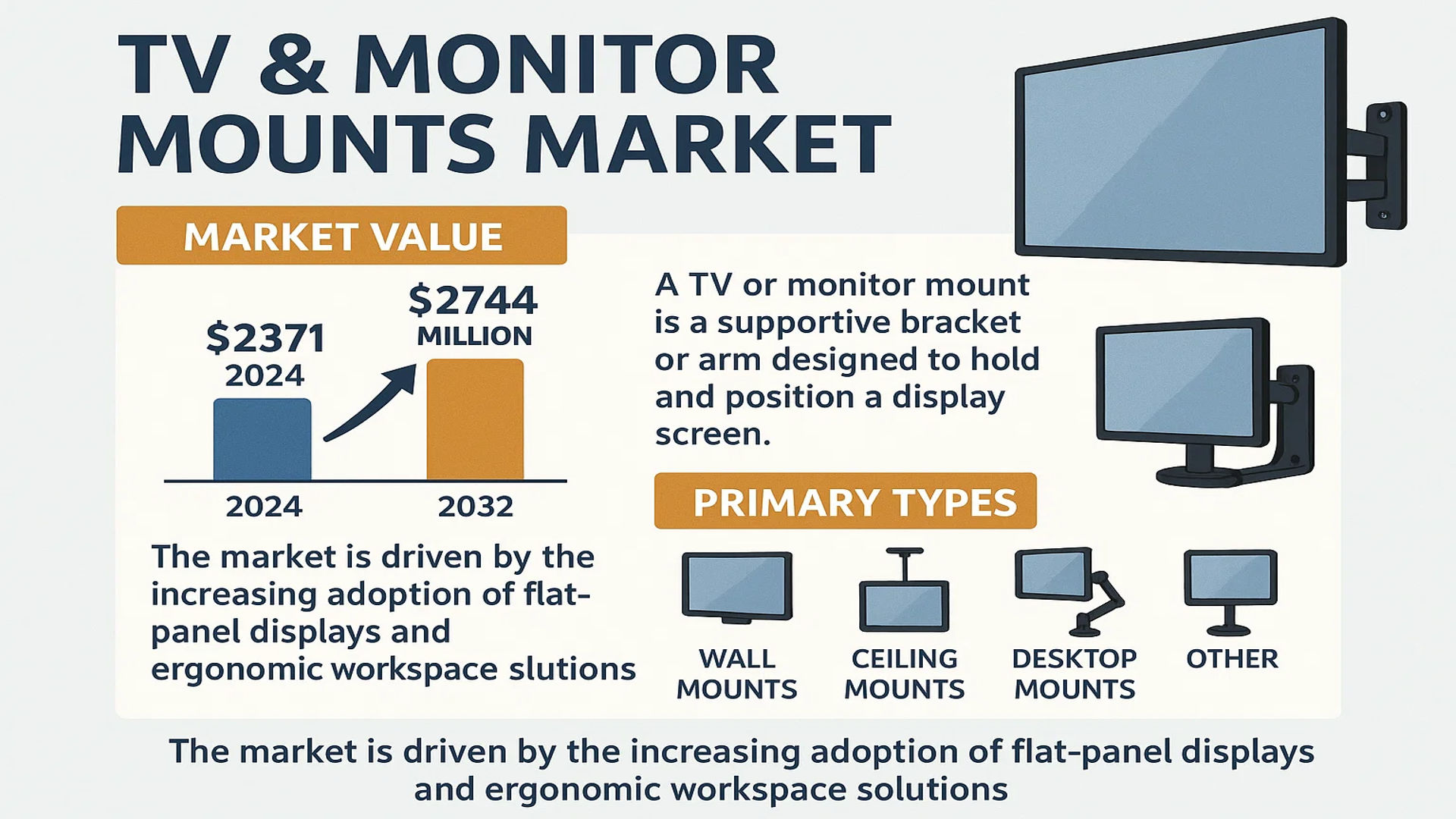

The global TV & Monitor Mounts Market was valued at 2371 million in 2024 and is projected to reach US$ 2744 million by 2032, at a CAGR of 2.2% during the forecast period.

A TV or monitor mount is a supportive bracket or arm engineered to securely hold and position a display screen, such as a television, computer monitor, or laptop. These products constitute a family of standards defined by the Video Electronics Standards Association (VESA), ensuring compatibility and safety for mounting flat panel displays to stands or walls. The primary types include wall mounts, ceiling mounts, desktop mounts, and other specialized solutions.

The market is experiencing steady growth, primarily driven by the increasing adoption of flat-panel displays in both residential and commercial settings and the growing demand for ergonomic workspace solutions. The rise of remote work and hybrid office models has further accelerated demand for adjustable mounts that enhance productivity and comfort. Geographically, Asia-Pacific dominates the market, holding over 30% of the global share, followed by North America and Europe. Within product segments, wall mounts are the largest, accounting for approximately 40% of the market. Key players such as Milestone, Ergotron, and Mounting Dream operate globally with extensive portfolios, continually innovating to meet evolving consumer needs for flexibility and space optimization.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of Multi-Screen Setups and Ergonomic Workspaces to Propel Market Expansion

The global shift toward hybrid work models and increasing demand for ergonomic office solutions are significantly driving the TV and monitor mounts market. With over 40% of the global workforce operating under hybrid arrangements, there is a substantial need for flexible and space-efficient display mounting solutions. Wall mounts and articulating arms enable users to optimize limited workspace while maintaining proper viewing angles, reducing neck strain, and improving productivity. The commercial sector, particularly corporate offices and educational institutions, has witnessed a 25% increase in demand for mounting solutions since 2022 as organizations prioritize employee comfort and efficient space utilization. Furthermore, the growing trend of multi-monitor configurations among professionals in finance, design, and technology sectors continues to fuel market growth, with dual and triple monitor setups accounting for approximately 35% of commercial installations.

Increasing Consumer Expenditure on Home Entertainment Systems to Accelerate Market Growth

The residential segment is experiencing robust growth due to increasing consumer investment in home entertainment systems and smart home integration. The global flat panel TV market continues to expand, with annual shipments exceeding 210 million units, creating a substantial aftermarket for mounting solutions. Consumers are increasingly opting for sleek, space-saving mounting options that complement modern interior designs, with wall mounts representing approximately 40% of total market share. The trend toward larger television displays, particularly in the 55-inch to 85-inch category, has driven demand for heavy-duty mounting solutions capable of supporting weights exceeding 50 kilograms. Additionally, the integration of smart home features and the desire for clean cable management solutions have made professional-grade mounts increasingly popular among residential consumers seeking premium viewing experiences.

Technological Advancements and Product Innovation to Drive Market Development

Manufacturers are continuously innovating to meet evolving consumer needs, introducing features such as automatic tilt adjustment, integrated cable management systems, and compatibility with varying VESA patterns. The development of low-profile mounts that maintain displays closer to walls has gained significant traction, particularly in residential applications where aesthetics are paramount. Recent innovations include motorized mounts that can be controlled via smartphone applications and mounts with integrated power solutions for cleaner installations. The industry has also seen increased adoption of corrosion-resistant materials and enhanced weight capacities to accommodate increasingly large and heavy displays. These technological improvements not only enhance user experience but also create opportunities for premium product segments, driving average selling prices and overall market value.

MARKET RESTRAINTS

High Installation Complexity and Safety Concerns to Limit Market Penetration

Despite growing demand, the market faces significant restraints related to installation challenges and safety considerations. Many consumers hesitate to adopt wall mounting solutions due to concerns about structural integrity, particularly in older buildings or drywall constructions. The installation process often requires drilling into walls, locating studs, and ensuring proper weight distribution, creating barriers for DIY enthusiasts. Professional installation services can add 30-50% to the total cost of ownership, making the solution less attractive for budget-conscious consumers. Furthermore, safety incidents related to improper installation, including display falls and wall damage, have created apprehension among potential users. Manufacturers must navigate these concerns while ensuring their products meet rigorous safety standards across different regional requirements.

Price Sensitivity and Intense Competition from Alternative Solutions to Constrain Growth

The market faces considerable price pressure from both low-cost manufacturers and alternative display solutions. The availability of inexpensive stands and furniture with integrated display support provides consumers with alternatives to dedicated mounting systems. Additionally, the proliferation of ultra-thin displays that include their own stand solutions has reduced the perceived necessity for aftermarket mounts. Price competition is particularly intense in the entry-level segment, where profit margins can be as low as 10-15%. This environment makes it challenging for manufacturers to invest in research and development while maintaining competitive pricing. The market also faces pressure from the second-hand mount segment, as many mounting systems are reusable when consumers upgrade their displays, reducing the need for new purchases.

Regional Regulatory Variations and Standardization Challenges to Hinder Market Expansion

Diverging regional safety standards and certification requirements create significant challenges for global manufacturers. Different markets require compliance with varying safety regulations, including specific load testing protocols, material standards, and installation guidelines. The absence of universal standards forces manufacturers to develop region-specific products, increasing production complexity and inventory costs. Additionally, the rapid evolution of display technology often outpaces standardization efforts, creating compatibility issues between new displays and existing mounting systems. These regulatory and standardization challenges particularly affect smaller manufacturers who lack the resources to navigate multiple certification processes, thereby limiting their ability to compete in international markets and constraining overall industry growth.

MARKET CHALLENGES

Compatibility Issues with Evolving Display Technologies to Challenge Market Adaptation

The rapid pace of display technology innovation presents ongoing challenges for mount manufacturers. As display form factors, weights, and VESA patterns continue to evolve, mounting systems must constantly adapt to maintain compatibility. The transition from thicker LCD displays to ultra-thin OLED and QLED panels has required redesigns of clamping mechanisms and weight distribution systems. Additionally, the emergence of curved displays and unconventional aspect ratios has created new engineering challenges for mount manufacturers. The industry must invest significantly in research and development to ensure new products remain compatible with emerging display technologies, while also maintaining backward compatibility to serve customers with older displays. This constant need for adaptation strains manufacturing resources and increases product development cycles.

Other Challenges

Supply Chain Vulnerabilities

The industry faces persistent supply chain challenges, particularly regarding raw material availability and manufacturing capacity fluctuations. Aluminum and steel, primary materials for mount construction, have experienced price volatility and occasional shortages. Specialized components such as gas springs for articulating arms and high-grade fasteners require specialized manufacturing capabilities that can be disrupted by global economic conditions. These supply chain vulnerabilities became particularly evident during recent global disruptions, where lead times extended from typical 4-6 weeks to 12-16 weeks for certain premium products.

Intellectual Property Conflicts

The market experiences ongoing intellectual property disputes regarding mounting mechanism designs and proprietary technologies. Larger manufacturers frequently engage in patent litigation to protect their innovations, creating barriers to entry for smaller companies and potentially stifling innovation. These legal conflicts can result in product recalls, redesign requirements, and significant legal expenses that ultimately increase consumer prices and limit product availability in certain markets.

MARKET OPPORTUNITIES

Growing Smart Home Integration and IoT Connectivity to Create New Market Frontiers

The integration of smart technology and IoT capabilities presents significant growth opportunities for the monitor mounts market. The emergence of motorized mounts with wireless connectivity allows users to adjust their displays remotely through smartphone applications or voice commands. This convergence with smart home ecosystems enables seamless integration with other connected devices, creating opportunities for premium, high-margin products. The market for smart mounting solutions is projected to grow at approximately 18% annually as consumers seek enhanced convenience and automation in their entertainment and workspace setups. Manufacturers developing mounts with integrated power management, environmental sensors, and automated positioning capabilities are positioned to capture value in this evolving segment.

Expansion in Healthcare and Educational Sectors to Provide Substantial Growth Potential

Specialized applications in healthcare and education sectors offer considerable expansion opportunities. Medical facilities require mounting solutions that meet stringent hygiene standards, provide precise positioning for surgical displays, and withstand frequent cleaning protocols. The education sector increasingly adopts interactive display systems that require robust, adjustable mounting solutions for classrooms and lecture halls. These vertical markets often prioritize reliability and specific functionality over price sensitivity, creating opportunities for specialized products with higher profit margins. The global digital education market’s expansion and increasing healthcare infrastructure investments particularly in emerging economies are expected to drive sustained demand for professional-grade mounting solutions in these sectors.

Sustainability Initiatives and Circular Economy Models to Open New Business Avenues

Increasing focus on sustainability and circular economy principles creates opportunities for manufacturers developing environmentally conscious products. The ability to recycle mounting components, use of sustainable materials, and design for disassembly are becoming important differentiators in environmentally conscious markets. Additionally, refurbishment and reuse programs for mounting systems align with growing consumer interest in sustainable consumption. Manufacturers implementing take-back programs and using recycled materials can potentially access new customer segments and comply with increasingly stringent environmental regulations. This shift toward sustainability also creates opportunities for product-as-a-service models where manufacturers retain ownership of mounting systems and provide installation and maintenance services, creating recurring revenue streams.

TV & MONITOR MOUNTS MARKET TRENDS

Ergonomic Workspace Solutions and Heightened Commercial Demand to Emerge as a Trend in the Market

The global shift towards hybrid and remote work models has fundamentally altered workspace dynamics, creating a sustained and growing demand for ergonomic office solutions, including advanced TV and monitor mounts. This trend is particularly pronounced as businesses and individuals invest in creating productive home offices, driving the need for space-efficient and health-conscious setups. The market has responded with innovative products featuring enhanced articulation, greater weight capacities to accommodate larger, ultrawide monitors, and integrated cable management systems to maintain clean and organized workspaces. Furthermore, the commercial sector, including corporate offices, educational institutions, and healthcare facilities, continues to be a major growth driver, accounting for a significant portion of the market’s value. This segment prioritizes durability, ease of installation, and the ability to create multi-screen workstations, which are essential for data-intensive and collaborative environments.

Other Trends

Technological Integration and Smart Mounts

The integration of technology into traditional mounting solutions is rapidly gaining traction, marking a significant evolution in the product category. The development of smart mounts with motorized adjustments, programmable height and tilt settings, and even IoT connectivity for automated workspace optimization represents the next frontier. These advanced systems align with the broader smart home and smart office trends, offering users unprecedented control and customization. While still a niche segment, the potential for growth is substantial as the technology becomes more accessible and cost-effective. This innovation is not merely about convenience; it also enhances accessibility, providing automated solutions for users with mobility challenges and further embedding these products into the ecosystem of connected devices that define modern living and working spaces.

Rising Consumer Focus on Aesthetics and Space Optimization

Beyond pure functionality, a powerful consumer trend is the increasing emphasis on interior design and aesthetics. Modern consumers are no longer satisfied with bulky, utilitarian mounts that detract from a room’s decor. This has led to a surge in demand for sleek, minimalist designs with low visual profiles, finishes that match popular electronics like brushed aluminum or matte black, and the ability to achieve a flushed-to-the-wall appearance for a clean, built-in look. The wall mount segment, which holds the largest market share of approximately 40%, benefits immensely from this trend as it is central to achieving a streamlined aesthetic. This focus on design is equally relevant in both household and commercial applications, where creating an appealing and uncluttered environment is a priority. The market has adapted with a wider array of design-conscious products that do not compromise on the core functional requirements of stability and safety.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The competitive landscape of the global TV & Monitor Mounts market is fragmented, with a diverse mix of established multinational corporations, specialized regional manufacturers, and emerging e-commerce-focused brands vying for market share. Ergotron, Inc. stands as a dominant global leader, primarily due to its pioneering ergonomic designs, robust patent portfolio, and longstanding relationships with corporate and healthcare clients. The company’s focus on cable management, smooth articulation, and high weight capacity has made it the preferred choice for high-end commercial installations.

Milestone AV Technologies and Peerless-AV also command significant market presence, collectively holding a substantial portion of the revenue share. Their growth is heavily attributed to comprehensive product lines that cater to both mass-market consumers and professional integrators, alongside strong distribution networks across North America and Europe. These companies consistently invest in VESA compliance certification and innovative mounting solutions for ultra-thin and large-format displays, which are becoming increasingly popular.

Meanwhile, value-oriented brands like Mounting Dream and VIVO have carved out a considerable niche by leveraging direct-to-consumer online sales channels. Their strategy emphasizes competitive pricing, broad compatibility, and positive user reviews, making them formidable players in the household segment. Their growth is further accelerated by strategic partnerships with e-commerce platforms and digital marketing initiatives.

Additionally, electronics giants such as LG Electronics and Samsung play a notable role, often bundling proprietary mounts with their display products. While their market share in the standalone mount segment is smaller, their influence on design standards and consumer preferences is significant. These companies are strengthening their positions through vertical integration, smart mount concepts with integrated cable management for their own displays, and aesthetic designs that complement their TVs and monitors.

The market is also witnessing increased activity from companies focusing on specialized applications, such as Premier Mounts in the professional audio-visual and public display sectors and Bell’O Digital in designer furniture-style mounts. Their growth is fueled by targeting specific, high-margin applications that require custom solutions, demonstrating how diversification and specialization are key strategies for sustaining competition.

List of Key TV & Monitor Mount Companies Profiled

- Ergotron, Inc. (U.S.)

- Milestone AV Technologies (U.S.)

- Peerless-AV (U.S.)

- Mounting Dream (U.S.)

- VIVO (U.S.)

- LG Electronics (South Korea)

- Premier Mounts (U.S.)

- Bell’O Digital (U.S.)

- Kanto Solutions (Canada)

Segment Analysis:

By Type

Wall Mount Segment Dominates the Market Due to Space Optimization and Aesthetic Appeal

The market is segmented based on type into:

- Wall Mount

- Desktop Mount

- Ceiling Mount

- Others

By Application

Household Segment Leads Due to Rising Consumer Demand for Ergonomic Home Office Setups

The market is segmented based on application into:

- Household

- Commercial

- Public

By Mounting Capacity

Standard Capacity Mounts Hold Significant Share Owing to Compatibility with Mainstream Display Sizes

The market is segmented based on mounting capacity into:

- Light Duty

- Standard Duty

- Heavy Duty

By Motion Type

Fixed Mounts Remain Prevalent Due to Their Stability and Cost-Effectiveness

The market is segmented based on motion type into:

- Fixed Mounts

- Tilt Mounts

- Full Motion Mounts

Regional Analysis: TV & Monitor Mounts Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global TV & Monitor Mounts market, accounting for over 30% of total market share. This leadership is driven by massive manufacturing hubs, particularly in China, which serve both domestic demand and global supply chains. The region’s growth is fueled by rapid urbanization, rising disposable incomes, and the proliferation of affordable flat-panel displays. While cost-effective, basic wall mounts remain highly popular, there is a noticeable and growing consumer shift towards more sophisticated, ergonomic desktop mounts and full-motion articulating arms, especially within the commercial sector. This trend is supported by the expansion of the IT and BPO industries in countries like India and the Philippines, where optimizing workspace efficiency is a priority. The market is highly competitive and fragmented, with numerous local manufacturers alongside global players.

North America

North America represents a mature and high-value market, characterized by a strong demand for premium, feature-rich mounting solutions. The region, particularly the United States, has a high penetration rate of large-screen TVs and multi-monitor computer setups, both in households and commercial environments. This drives demand for advanced mounts with features like articulating arms, height adjustment, and cable management systems. The commercial segment, including corporate offices, control rooms, and healthcare facilities, is a significant contributor, with a focus on ergonomics and productivity. Key market players like Ergotron and Peerless have a strong presence here. Consumer preferences lean towards brands that offer durability, safety certifications (like UL listing), and sleek designs that complement modern interiors.

Europe

Similar to North America, the European market is well-established and emphasizes quality, safety, and design aesthetics. Stringent EU regulations and standards governing product safety and material usage ensure that only compliant, high-quality mounts gain significant market traction. The demand is bifurcated: a robust commercial sector driven by office modernization and a discerning residential consumer base. Countries like Germany, the UK, and France are key markets where consumers are willing to invest in reliable and aesthetically pleasing mounting solutions from reputable brands. The trend towards smart homes and minimalist interior design also influences product choices, favoring low-profile and discreet mounts. Sustainability and the environmental impact of products are becoming increasingly important purchase considerations for European consumers.

South America

The South American market for TV and monitor mounts is in a growth phase, presenting significant potential amidst economic challenges. The region is experiencing a steady increase in display ownership, which is the primary driver of demand. However, market growth is often tempered by economic volatility and fluctuating import tariffs, which can affect pricing and availability. Price sensitivity is a major factor, making cost-effective, basic fixed wall mounts the most prevalent product type. While the market is primarily volume-driven, there is a nascent but growing segment for more advanced products in major urban centers and within the commercial sector, particularly in countries like Brazil and Argentina. Local distribution networks and e-commerce platforms are key to market access.

Middle East & Africa

The MEA region is an emerging market with its growth largely concentrated in the Gulf Cooperation Council (GCC) nations and major urban centers in Africa. High disposable incomes in countries like the UAE and Saudi Arabia fuel demand for luxury consumer electronics and, consequently, high-end mounting solutions for both residential and hospitality projects. The market is characterized by a demand for large, heavy-duty mounts capable of supporting big-screen TVs, often seen in luxury villas and hotels. In contrast, other parts of the region are more price-sensitive, with growth linked to basic infrastructure development and the gradual expansion of the retail sector. Overall, the market potential is substantial but unevenly distributed, with progress dependent on economic stability and continued infrastructure investment.

Report Scope

This market research report provides a comprehensive analysis of the global and regional TV & Monitor Mounts markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of smart features, evolving industry standards, and material advancements.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global TV & Monitor Mounts Market?

->TV & Monitor Mounts Market was valued at 2371 million in 2024 and is projected to reach US$ 2744 million by 2032, at a CAGR of 2.2% during the forecast period.

Which key companies operate in Global TV & Monitor Mounts Market?

-> Key players include Milestone, Ergotron, Mounting Dream, Premier Mounts, Peerless, AVF, LG, and Bell’O Digital, among others.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of flat panel displays, rising demand for ergonomic workspace solutions, and growth in commercial and residential construction activities.

Which region dominates the market?

-> Asia-Pacific is the largest market with over 30% share, followed by North America and Europe.

What are the emerging trends?

-> Emerging trends include motorized mounts with smart controls, integration of cable management systems, and sustainable material usage.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...