MARKET INSIGHTS

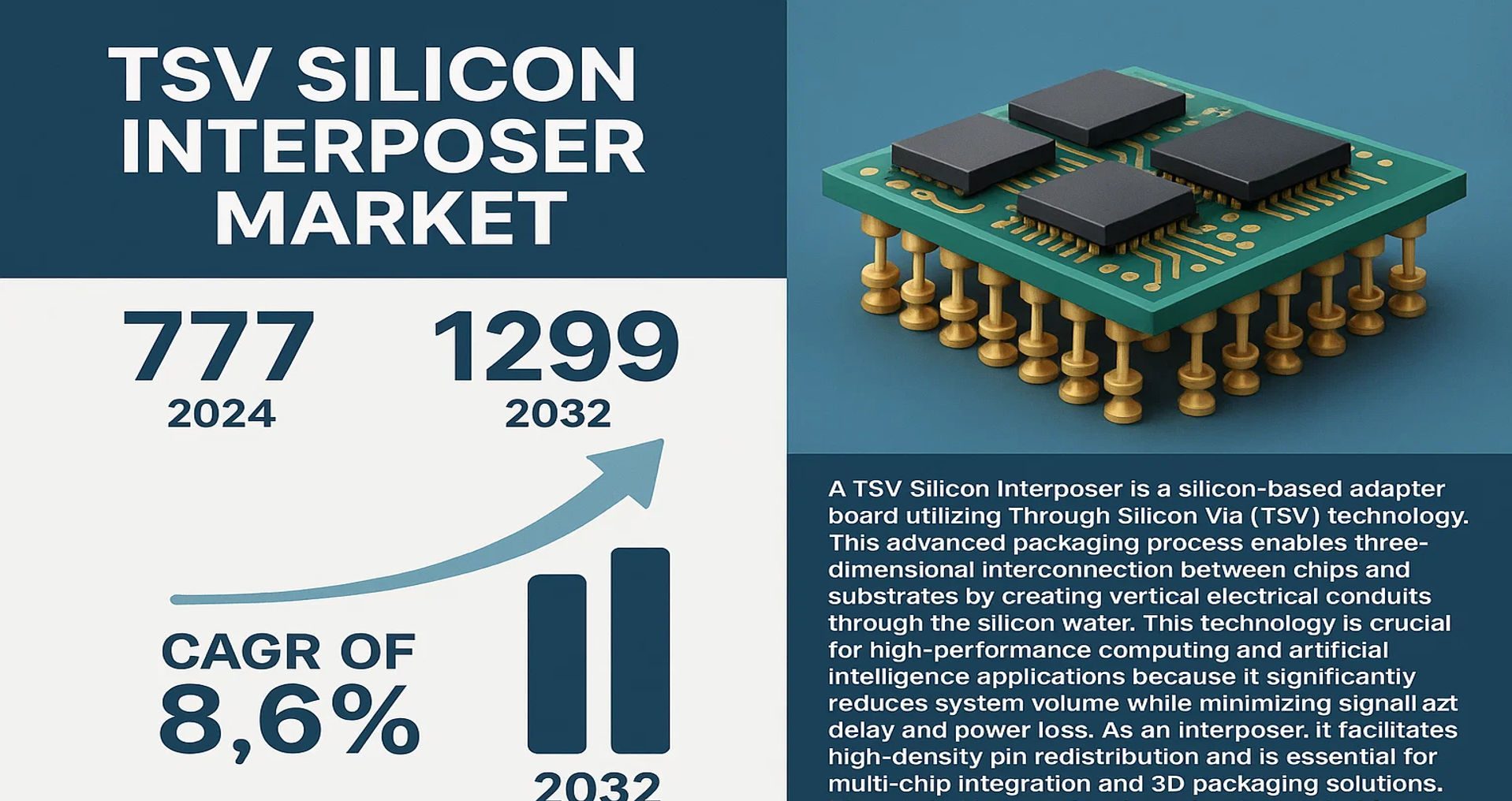

The global TSV Silicon Interposer Market was valued at 777 million in 2024 and is projected to reach US$ 1299 million by 2032, at a CAGR of 8.6% during the forecast period.

A TSV Silicon Interposer is a silicon-based adapter board utilizing Through Silicon Via (TSV) technology. This advanced packaging process enables three-dimensional interconnection between chips and substrates by creating vertical electrical conduits through the silicon wafer. This technology is crucial for high-performance computing and artificial intelligence applications because it significantly reduces system volume and mass while minimizing signal delay and power loss. As an interposer, it facilitates high-density pin redistribution and is essential for multi-chip integration and 3D packaging solutions.

The market is experiencing robust growth driven by escalating demand for miniaturized, high-bandwidth electronics. The proliferation of data centers and AI hardware necessitates advanced packaging like 2.5D and 3D IC integration, where TSV interposers are critical. Furthermore, substantial investments in semiconductor R&D and supportive government policies worldwide are accelerating adoption. Key industry players, including TSMC and Amkor Technology, are expanding their production capabilities to meet this surging demand, solidifying the market’s upward trajectory.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Performance Computing and AI Applications to Drive Market Growth

The exponential growth in artificial intelligence, machine learning, and high-performance computing applications is significantly driving the TSV silicon interposer market. These advanced computing systems require extremely high bandwidth and low latency between processing units and memory, which TSV technology effectively provides through its 3D integration capabilities. The global AI chip market is projected to exceed $80 billion by 2025, creating substantial demand for advanced packaging solutions like TSV interposers. Major technology companies are increasingly adopting 2.5D and 3D packaging with silicon interposers to achieve the necessary performance levels for AI training and inference workloads. This trend is particularly evident in data centers where performance-per-watt and space efficiency are critical factors driving adoption decisions.

Expansion of 5G Infrastructure and IoT Devices to Accelerate Market Adoption

The global rollout of 5G networks and the proliferation of Internet of Things devices are creating substantial opportunities for TSV silicon interposer technology. 5G infrastructure requires highly integrated, power-efficient components that can handle massive data throughput while maintaining compact form factors. TSV interposers enable the integration of RF components, baseband processors, and memory in single packages, reducing signal loss and improving overall system performance. The IoT market, expected to connect over 75 billion devices by 2025, demands miniaturized yet powerful semiconductor solutions that TSV technology can provide. This dual expansion across telecommunications and consumer electronics represents a significant growth vector for the interposer market.

Advancements in Semiconductor Manufacturing Processes to Fuel Technological Evolution

Continuous improvements in semiconductor manufacturing capabilities are enabling more cost-effective production of TSV silicon interposers. The industry has achieved remarkable progress in via formation, wafer thinning, and bonding technologies, reducing defect rates and improving yields. Recent developments in etching techniques have enabled aspect ratios exceeding 20:1 while maintaining structural integrity, allowing for higher density interconnections. The maturation of temporary bonding and debonding processes has significantly improved handling of thin wafers during manufacturing. These technological advancements are making TSV interposers more accessible across various application segments, from premium high-performance computing to mainstream consumer electronics.

Furthermore, the increasing collaboration between foundries, OSAT companies, and equipment manufacturers is creating a more robust ecosystem for TSV interposer production. This collaborative approach is accelerating technology transfer and knowledge sharing across the semiconductor industry.

➤ For instance, major semiconductor manufacturers have recently demonstrated production-ready TSV processes with yields exceeding 95% for certain applications, marking a significant milestone in manufacturing maturity.

The combination of these technological improvements and ecosystem development is expected to drive substantial market growth throughout the forecast period.

MARKET CHALLENGES

High Manufacturing Complexity and Cost Structure to Challenge Widespread Adoption

The TSV silicon interposer market faces significant challenges related to manufacturing complexity and associated costs. The production process involves multiple sophisticated steps including deep silicon etching, wafer thinning, via filling, and precision bonding, each requiring specialized equipment and expertise. The capital expenditure for establishing a TSV production line can exceed $500 million, creating substantial barriers to entry for new market participants. Additionally, the yield management across these complex processes remains challenging, particularly for interposers with high via densities and large form factors. These factors contribute to higher per-unit costs compared to traditional packaging solutions, limiting adoption to premium applications where performance justifies the additional expense.

Other Challenges

Thermal Management Issues

The high density of active components in 3D packages creates significant thermal management challenges. Power densities can exceed 100 W/cm² in advanced applications, requiring sophisticated cooling solutions that add complexity and cost. The thermal interface between dies and the interposer, as well as heat dissipation through the package, present engineering challenges that must be addressed for reliable operation.

Testing and Reliability Concerns

Testing TSV-based packages presents unique challenges due to the limited accessibility to internal nodes and the complexity of fault isolation. Reliability issues such as thermomechanical stress, electromigration in TSVs, and interfacial delamination require extensive characterization and qualification processes. These testing and reliability considerations extend development timelines and increase overall product development costs.

MARKET RESTRAINTS

Supply Chain Constraints and Material Availability to Limit Market Expansion

The TSV silicon interposer market faces constraints related to specialized material requirements and equipment availability. The production process requires high-purity materials including specific types of dielectric layers, barrier materials, and conductive fills that have limited supply sources. The specialized equipment needed for TSV formation, wafer thinning, and precision alignment represents another constraint, with long lead times for delivery and installation. These supply chain challenges are exacerbated by the current global semiconductor equipment shortage, which has extended delivery timelines for critical manufacturing tools to over 18 months in some cases.

Additionally, the industry faces capacity constraints as existing production facilities are operating near maximum utilization rates. The time required to bring new capacity online, typically 2-3 years from planning to production, creates a mismatch between demand growth and available supply. This capacity limitation particularly affects the market’s ability to serve emerging application segments that require volume production capabilities.

MARKET OPPORTUNITIES

Emerging Applications in Automotive Electronics and Healthcare to Create New Growth Frontiers

The automotive industry’s transition toward electric vehicles and advanced driver assistance systems presents substantial opportunities for TSV silicon interposer technology. Modern vehicles incorporate numerous high-performance computing modules for autonomous driving, sensor fusion, and vehicle-to-everything communication, all requiring advanced packaging solutions. The medical electronics sector, particularly implantable devices and advanced diagnostic equipment, represents another promising opportunity where miniaturization and reliability are critical requirements.

Furthermore, the growing demand for heterogeneous integration in various electronic systems provides additional growth avenues. The ability to integrate different technology nodes, various material systems, and diverse functional components using TSV interposers enables system-level optimization that traditional packaging cannot achieve. This heterogeneous integration capability is becoming increasingly valuable across multiple industry segments seeking performance improvements without fundamental technology changes.

Additionally, the ongoing research and development in advanced packaging architectures is expected to uncover new application areas and drive further market expansion. The convergence of different technology trends creates synergistic opportunities that could significantly accelerate market growth beyond current projections.

TSV SILICON INTERPOSER MARKET TRENDS

Advancements in 3D Packaging Technologies to Emerge as a Trend in the Market

Advancements in 3D packaging technologies, particularly the refinement of Through-Silicon Via (TSV) processes, have revolutionized semiconductor integration and significantly increased the demand for silicon interposers. Recent innovations such as hybrid bonding techniques, which enable sub-10μm pitch connections, and improved thermal management solutions have further enhanced the performance and reliability of 3D integrated circuits. The integration of artificial intelligence in design automation has significantly improved yield rates, with some manufacturers reporting production yields exceeding 85% for complex 2.5D interposer structures. This technological progression directly supports the market’s projected growth from $777 million in 2024 to $1299 million by 2032, representing a compound annual growth rate of 8.6%.

Other Trends

Artificial Intelligence and High-Performance Computing Demand

The exponential growth in artificial intelligence applications has created unprecedented demand for advanced packaging solutions that can support the massive data transfer rates required by AI accelerators and high-performance computing systems. TSV silicon interposers enable the necessary bandwidth density for these applications, with current implementations supporting data rates exceeding 4 Gbps per lane. The market for AI chips utilizing 2.5D packaging is experiencing remarkable growth, with estimates suggesting that nearly 70% of all high-performance AI processors will incorporate silicon interposers by 2026. This trend is particularly evident in data center applications, where the need for higher computational density and energy efficiency continues to drive innovation in interposer technology.

Heterogeneous Integration and Advanced Node Challenges

The semiconductor industry’s transition to more advanced nodes below 7nm has created significant challenges in traditional packaging approaches, making TSV silicon interposers increasingly essential for heterogeneous integration. As transistor scaling becomes more difficult and expensive, manufacturers are turning to 2.5D and 3D integration techniques to continue improving system performance. This shift is evidenced by the growing adoption of chiplet architectures, where multiple dies with different process technologies are integrated using silicon interposers. The market for heterogeneous integration solutions has grown approximately 25% annually over the past three years, with silicon interposers playing a crucial role in enabling this architectural transformation. Furthermore, the ability to integrate memory and logic components in close proximity has reduced latency by up to 40% and power consumption by 30% compared to traditional packaging methods.

Supply Chain Diversification and Regional Manufacturing Expansion

Recent global supply chain disruptions have accelerated the diversification of TSV silicon interposer manufacturing capabilities across multiple geographic regions. While Taiwan and South Korea currently dominate production, accounting for approximately 65% of global capacity, significant investments are being made in North American and European facilities. The United States CHIPS Act has allocated substantial funding for advanced packaging capabilities, including TSV technology, with several major manufacturers announcing expansion plans totaling over $15 billion in new investments. Similarly, the European Chips Act is driving comparable initiatives, aiming to capture 20% of the global semiconductor market by 2030. This geographic diversification is creating a more resilient supply chain while also fostering increased competition and technological innovation across the industry.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Leverage Advanced Packaging Expertise to Secure Market Position

The global TSV Silicon Interposer market exhibits a semi-consolidated structure, characterized by a mix of established semiconductor giants and specialized foundries. This landscape is driven by the high technological barriers to entry, including significant capital expenditure for TSV fabrication equipment and deep expertise in advanced packaging processes. Taiwan Semiconductor Manufacturing Company (TSMC) is a dominant force, largely due to its industry-leading process technology, massive R&D investments—exceeding $5 billion annually in advanced packaging alone—and its pivotal role as a supplier to major high-performance computing and artificial intelligence chip designers.

Amkor Technology and ASE Group also command significant market share, collectively accounting for a substantial portion of the global outsourced semiconductor assembly and test (OSAT) capacity for 2.5D and 3D packaging. Their growth is propelled by strong relationships with fabless semiconductor companies and strategic expansions of their advanced packaging facilities, particularly in Asia, to meet the surging demand from the data center and AI sectors.

Furthermore, these leading players are aggressively pursuing capacity expansion and technological partnerships. For instance, TSMC’s continuous development of its CoWoS (Chip-on-Wafer-on-Substrate) platform, which heavily relies on silicon interposers, solidifies its leadership. Similarly, Amkor’s recent investments in new factories and its collaboration with substrate suppliers are strategic moves to capture more of the high-growth market.

Meanwhile, specialized pure-play foundries like United Microelectronics Corporation (UMC) and technology innovators such as Tezzaron Semiconductor are strengthening their niches through focused R&D on cost-effective TSV integration and ultra-high-density interconnects, respectively. Their targeted approaches allow them to compete effectively in specific application segments, ensuring a dynamic and evolving competitive environment.

List of Key TSV Silicon Interposer Companies Profiled

- Taiwan Semiconductor Manufacturing Company (TSMC) (Taiwan)

- Amkor Technology, Inc. (U.S.)

- ASE Technology Holding Co., Ltd. (Taiwan)

- United Microelectronics Corporation (UMC) (Taiwan)

- Innovative Micro Technology (IMT) (U.S.)

- ALLVIA, Inc. (U.S.)

- Tezzaron Semiconductor Corporation (U.S.)

- China Wafer Level CSP Co., Ltd. (China)

Segment Analysis:

By Type

3D TSV Silicon Interposer Segment Leads the Market Due to Superior Performance in High-Density Integration

The market is segmented based on type into:

- 2.5D

- 3D

By Application

Artificial Intelligence Segment Dominates Owing to Critical Role in Advanced Computing and Neural Network Hardware

The market is segmented based on application into:

- Artificial Intelligence

- Consumer Electronics

- Data Center

- Others

By End User

Semiconductor Foundries Hold Largest Share Due to In-House Manufacturing Capabilities and Technological Expertise

The market is segmented based on end user into:

- Semiconductor Foundries

- Integrated Device Manufacturers (IDMs)

- Outsourced Semiconductor Assembly and Test (OSAT) Providers

By Wafer Size

300mm Wafers are Preferred for Mass Production Offering Higher Yield and Cost Efficiency

The market is segmented based on wafer size into:

- 200mm

- 300mm

Regional Analysis: TSV Silicon Interposer Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global TSV Silicon Interposer market, driven by its immense semiconductor manufacturing ecosystem. Accounting for over 60% of global production, the region’s dominance is anchored by technological powerhouses like Taiwan, South Korea, and China. Taiwan Semiconductor Manufacturing Company (TSMC) and United Microelectronics Corporation (UMC) are global pioneers in advanced packaging, including 2.5D and 3D integration with TSV interposers. This leadership is fueled by massive domestic demand from consumer electronics giants and strategic government initiatives, such as China’s substantial investments in its semiconductor self-sufficiency goals. While cost competitiveness remains a key advantage, the region is also at the forefront of R&D, continuously pushing the boundaries of miniaturization and performance for applications in artificial intelligence and high-performance computing.

North America

North America is a critical innovation and high-value application hub for TSV silicon interposers. The market is primarily driven by demand from leading technology firms in the United States, particularly those developing cutting-edge artificial intelligence accelerators, GPUs, and data center processors. These applications require the high-bandwidth, low-latency connectivity that TSV interposers provide for 2.5D and 3D IC packaging. The region benefits from strong collaboration between fabless semiconductor companies, integrated device manufacturers (IDMs), and advanced packaging specialists like Amkor Technology. Furthermore, supportive policies, including the CHIPS and Science Act, which allocates billions for domestic semiconductor research and production, are expected to bolster the advanced packaging ecosystem, including TSV technology, ensuring its strategic role in the region’s tech infrastructure.

Europe

Europe’s market for TSV Silicon Interposers is characterized by a strong focus on research, development, and specialized, high-performance applications. The region’s automotive industry, a global leader in innovation, is a significant driver, integrating advanced semiconductors for autonomous driving and electric vehicle systems that increasingly benefit from 3D packaging solutions. Additionally, European research institutions and companies are deeply involved in developing technologies for aerospace, defense, and medical electronics, where the reliability and performance of TSV-based packaging are paramount. While the region’s volume manufacturing may be smaller compared to Asia-Pacific, its strength lies in creating high-margin, technologically sophisticated products. Collaboration within the EU framework supports these innovation efforts, positioning Europe as a key player in the high-end segment of the market.

South America

The TSV Silicon Interposer market in South America is in a nascent stage of development. The region’s semiconductor industry is primarily focused on assembly, testing, and packaging of less advanced nodes, with limited domestic capability for cutting-edge technologies like TSV. Market growth is currently constrained by a reliance on imported advanced components and a smaller local ecosystem for electronics manufacturing. However, countries like Brazil are making gradual efforts to develop their technology sectors. The long-term potential for growth exists, particularly as global supply chains diversify and regional demand for consumer electronics and IT infrastructure increases. For now, adoption is slow, with progress hinging on greater economic stability, increased foreign investment, and the development of more robust technical expertise and infrastructure.

Middle East & Africa

The market for TSV Silicon Interposers in the Middle East & Africa is emerging and highly selective. Growth is concentrated in a few nations with significant investment capital and strategic diversification plans, such as Israel, Saudi Arabia, and the UAE. Israel, with its strong high-tech and defense sectors, shows the most promise for adopting advanced packaging for specialized applications. Meanwhile, oil-rich Gulf states are investing in technology hubs and smart city initiatives, which could eventually generate demand for the high-performance computing infrastructure that utilizes these components. However, the region lacks a foundational semiconductor manufacturing base, making it almost entirely dependent on imports. Widespread adoption faces significant hurdles, including a underdeveloped supporting ecosystem and a primary focus on earlier-stage technology investments rather than leading-edge manufacturing processes.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor and Electronics markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global TSV Silicon Interposer Market?

-> TSV Silicon Interposer Market was valued at 777 million in 2024 and is projected to reach US$ 1299 million by 2032, at a CAGR of 8.6% during the forecast period.

Which key companies operate in Global TSV Silicon Interposer Market?

-> Key players include Amkor Technology, TSMC, UMC, ASE, Innovative Micro Technologies, ALLVIA, Tezzaron, and China Wafer Level CSP Co., Ltd, among others.

What are the key growth drivers?

-> Key growth drivers include advancements in semiconductor technology, rising demand for high-performance computing and AI chips, increasing data center investments, and supportive government policies for semiconductor manufacturing.

Which region dominates the market?

-> Asia-Pacific dominates the market, with Taiwan, China, South Korea, and Japan being major hubs for semiconductor manufacturing and advanced packaging technologies.

What are the emerging trends?

-> Emerging trends include increased adoption of 3D IC packaging, integration of TSV interposers in AI accelerators and HPC applications, development of hybrid bonding techniques, and expansion into automotive and 5G applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...