Transparent display market Insights

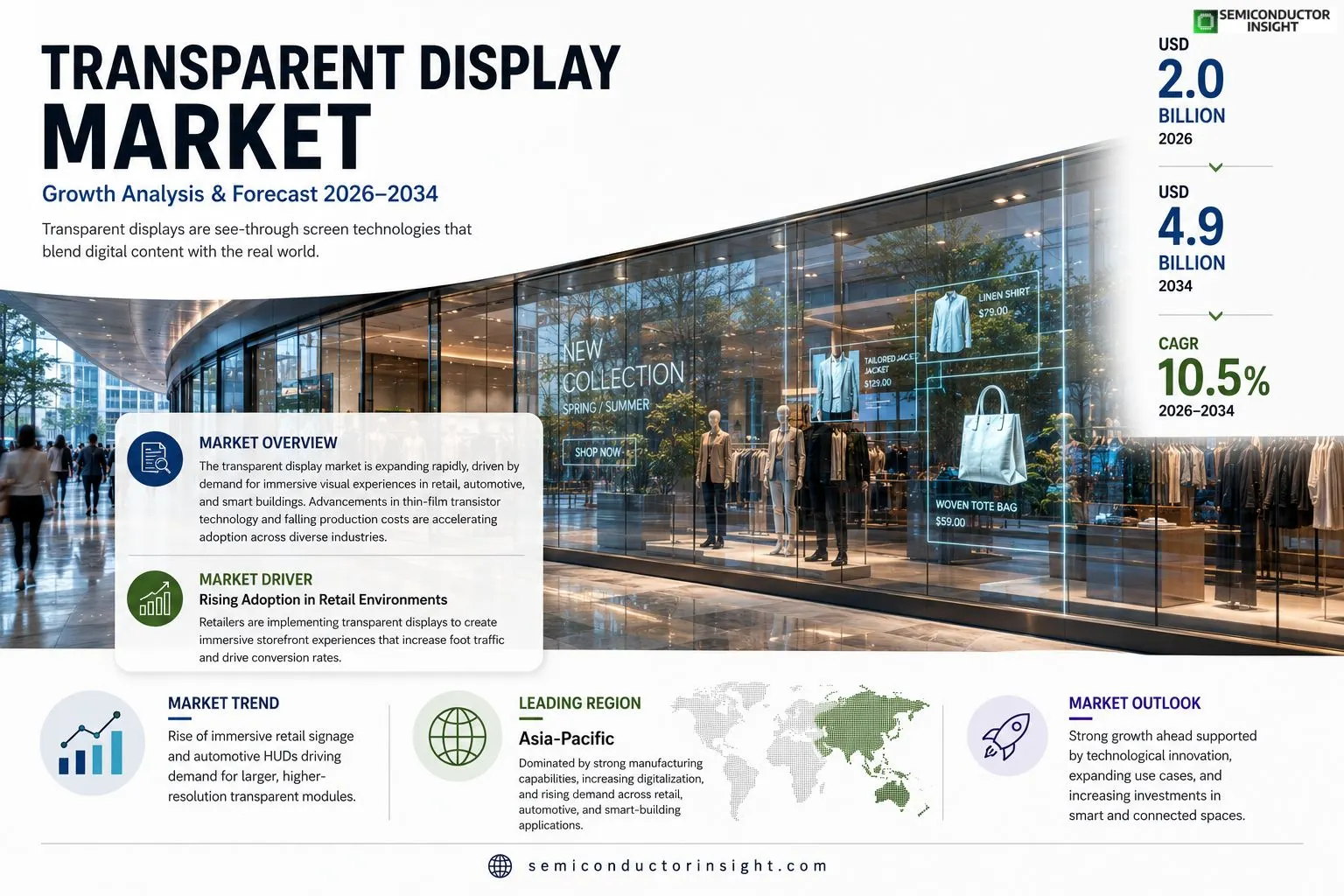

Transparent display market size was valued at USD 1.8 billion in 2025. The market is projected to grow from USD 2.0 billion in 2026 to USD 4.9 billion by 2034, exhibiting a CAGR of 10.5% during the forecast period.

Transparent displays are see‑through screen technologies that integrate LCD or OLED panels with a glass or polymer substrate, enabling visual content to be viewed while maintaining visibility of objects behind the panel. These devices are employed in retail signage, automotive heads‑up displays, smart windows, and augmented‑reality interfaces.The market is accelerating because advertisers seek immersive experiences, automotive manufacturers embed HUDs for safety, and smart‑building initiatives drive demand for interactive glass façades. Furthermore, advancements in thin‑film transistor efficiency and reductions in production cost are expanding adoption. Key players such as Samsung Electronics, LG Display, Planar Systems and Leyard continue to launch larger‑size and higher‑resolution modules, reinforcing growth momentum.

MARKET DRIVERS

Rising Adoption in Retail Environments

Transparent display market is being propelled by retailers seeking immersive window‑shopping experiences that blend digital content with physical storefronts. Customers respond positively to interactive glass panels that showcase products while maintaining storefront visibility, driving higher foot traffic and conversion rates.

Growth in Automotive Heads‑up Displays

Automakers are integrating transparent displays into windshields to deliver real‑time navigation, safety alerts, and infotainment without distracting drivers. This technological shift supports broader vehicle electrification trends and positions transparent screens as a standard cockpit element.

➤ Enhanced energy‑efficient OLED and micro‑LED technologies are reducing power consumption, making large‑area transparent screens viable for continuous operation in commercial settings.

These innovations, combined with declining component costs, enable a wider range of enterprises,including museums, corporate lobbies, and educational campuses,to deploy transparent visual solutions efficiently.

MARKET CHALLENGES

Technical Integration Complexity

Integrating transparent displays with existing building management and IT infrastructure requires specialized expertise. Compatibility issues with legacy signage systems can extend deployment timelines and increase implementation costs.

Other Challenges

Durability and Maintenance

Continuous exposure to sunlight and cleaning agents can affect display longevity. Manufacturers must balance optical clarity with protective coatings, which may increase unit pricing.

MARKET RESTRAINTS

High Initial Capital Expenditure

Despite long‑term benefits, the upfront investment for large‑scale transparent display installations remains a barrier for small‑to‑mid‑size enterprises. Budget constraints often lead decision‑makers to prioritize traditional LCD or LED signage solutions.

MARKET OPPORTUNITIES

Smart City Infrastructure

Urban planners are evaluating transparent displays for real‑time transit information, public safety alerts, and interactive wayfinding. As cities invest in digital twin initiatives, Transparent display market can capture contracts for large‑scale, publicly funded projects that emphasize aesthetic integration and data accessibility.

Enterprise Collaboration Spaces

Modern offices are redesigning meeting rooms to incorporate glass‑based touchscreens that enable seamless collaboration across physical and virtual participants. This trend opens avenues for vendors offering integrated software platforms that leverage transparent display capabilities.

Transparent display market Trends

Rise of Immersive Retail Signage

Retail environments are leveraging transparent display technology to replace conventional signage with see‑through screens that blend visual content with the underlying merchandise. By overlaying dynamic product information on glass storefronts, advertisers create immersive experiences that drive foot traffic and increase conversion rates. The integration of IoT sensors enables real‑time analytics, allowing retailers to adjust promotions instantly. This shift is supported by advances in thin‑film transistor efficiency, which have lowered power consumption and extended panel lifespan. Key players such as Samsung Electronics, LG Display, Planar Systems and Leyard continue to launch larger, higher‑resolution transparent modules specifically engineered for retail applications, reinforcing the momentum of this trend.

Other Trends

Automotive Heads‑Up Display Expansion

Automotive manufacturers are expanding the use of transparent displays in heads‑up display (HUD) systems to project navigation, speed, and safety alerts directly onto the windshield. This approach keeps drivers’ eyes on the road, enhancing situational awareness and reducing distraction. Recent module designs offer higher resolution and broader viewing angles, making them suitable for both premium and mass‑market vehicles. Partnerships between display suppliers and OEMs have accelerated the rollout of HUDs across new model lines. Consumer acceptance is rising as drivers report clearer perception of critical information, prompting automakers to standardize HUDs in upcoming vehicle platforms. These developments are solidifying Transparent display market relevance in the automotive sector.

Smart‑Building Interactive Glass

Smart‑building initiatives are driving adoption of transparent displays in architectural façades and interior glazing. Interactive glass panels provide occupants with real‑time building information, way‑finding assistance, and ambient advertising without obstructing natural light. Improvements in OLED and LCD integration have enabled larger‑size modules with higher pixel density, meeting the aesthetic demands of modern office and hospitality spaces. Energy‑saving coatings combined with low‑power drive electronics further enhance sustainability credentials. Integration with building management systems allows the displays to adjust brightness based on daylight levels and to present energy‑usage dashboards, aligning with broader sustainability goals. As property developers aim to create connected environments, Transparent display market is poised to play a central role in delivering seamless digital‑physical experiences that improve occupant comfort and operational efficiency.

COMPETITIVE LANDSCAPEKey Industry Players

Transparent display market – Competitive Overview

Transparent display market is anchored by a handful of vertically integrated electronics giants that control both panel fabrication and system integration. Samsung Electronics leads with its next‑generation OLED transparent panels, leveraging scale in semiconductor manufacturing to drive down unit cost while expanding size options above 55 inches. LG Display follows closely, offering large‑area LCD‑based transparent screens that target retail signage and smart‑glass applications. Leyard’s Planar Systems unit supplies modular transparent modules for corporate and public‑space deployments, emphasizing high brightness and durability. These leaders dominate supply chains, dictate pricing trends, and shape product roadmaps through aggressive R&D in thin‑film transistor efficiency and substrate engineering. Their combined market share exceeds 60 %, creating a concentrated structure where new entrants must either specialize in niche form factors or partner with established OEMs to gain distribution.Beyond the top tier, a diverse set of niche manufacturers contributes depth and regional reach. BOE Technology Group has accelerated its transparent LCD portfolio, focusing on cost‑effective large‑area panels for Asian retail corridors. Sharp supplies transparent OLED panels optimized for automotive heads‑up displays, while AU Optronics and Innolux target smart‑window integrations in commercial real‑estate projects. China Star Optoelectronics and Visionox bring emerging micro‑LED transparent technologies that promise higher contrast ratios. Smaller system integrators such as Christie Digital, ViewSonic, and Prodisplay specialize in turnkey solutions for exhibition and event markets, adding application‑specific value without owning fab facilities. This layered ecosystem sustains competitive pressure, fostering incremental innovation across resolution, size, and power‑efficiency dimensions.

List of Key Transparent Display Companies Profiled

-

Samsung Electronics

- LG Display

- Planar Systems (Leyard)

- BOE Technology Group

- Sharp Corporation

- AU Optronics

- Innolux Corporation

- China Star Optoelectronics Technology (CSOT)

- Visionox

- Christie Digital Systems

- ViewSonic Corporation

- Prodisplay

- Panasonic Corporation

- DeX Digital Technology

- Micron Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

LCD Transparent Displays

|

| By Application |

|

Retail Signage

|

| By End User |

|

Advertisers

|

| By Installation Environment |

|

Indoor

|

| By Technology |

|

Thin‑Film Transistor (TFT) Based

|

Regional Analysis: North America

United States

The automotive sector is a key driver for transparent displays, integrating them into instrument panels, head-up displays, and rear infotainment systems to enhance driver experience and safety.

Transparent displays are revolutionizing retail environments, enabling interactive digital signage, enhanced product visualization, and innovative point-of-sale systems.

Architectural applications are gaining traction, with transparent displays utilized for innovative storefronts, interactive building facades, and smart glass solutions, offering unique design possibilities.

Emerging applications in industrial control panels and medical devices are leveraging the benefits of transparent displays for enhanced information delivery and user interfaces.

Europe

Europe presents a steady and evolving market for Transparent display market solutions, characterized by a strong emphasis on innovation and sustainability. The region’s automotive industry, particularly in Germany and the UK, is a significant driver, with increasing adoption in advanced driver-assistance systems and infotainment. Retail applications are also gaining momentum, driven by the demand for engaging and interactive customer experiences. Architectural integration is a notable segment, with transparent displays enhancing building aesthetics and functionality. The European market is influenced by stringent data privacy regulations and a growing focus on energy-efficient technologies, shaping the development and deployment of transparent display solutions.

Asia-Pacific

The Asia-Pacific region is poised for substantial growth in Transparent display market, fueled by rapid industrialization, increasing disposable incomes, and a burgeoning technology sector. China, South Korea, and Japan are leading markets, with strong demand from the automotive, consumer electronics, and retail industries. The region’s focus on smart cities and connected devices is driving innovation in transparent display applications. The relatively lower cost of manufacturing in some Asia-Pacific countries also contributes to market expansion. However, competition from local manufacturers and varying regulatory landscapes present challenges for players.

South America

South America represents an emerging market for Transparent display market technologies, with growth potential driven by increasing investments in infrastructure and a growing consumer base. The retail sector is a key application area, with transparent displays enhancing shopping experiences and driving sales. The automotive industry is also showing increasing interest, particularly in premium segments. While the market is still relatively nascent, the region’s economic development and growing adoption of digital technologies are expected to foster future growth opportunities. Overcoming economic uncertainties and establishing robust distribution networks are crucial for market penetration.

Middle East & Africa

The Middle East & Africa region exhibits a moderate growth trajectory in Transparent display market, influenced by increasing government spending on infrastructure, urbanization, and a growing focus on technology adoption. The retail and automotive sectors are key drivers, with demand for interactive displays and advanced in-car information systems. Architectural applications are also gaining traction, particularly in high-end commercial and residential projects. The region’s evolving digital landscape and increasing disposable incomes are expected to drive further market expansion in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the Transparent display market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Transparent display market?

-> Transparent display market was valued at USD 1.8 billion in 2025 and is expected to reach USD 4.9 billion by 2034. The market exhibits a CAGR of 10.5% during the forecast period.

Which key companies operate in Transparent display market?

-> Key players include Samsung Electronics, LG Display, Planar Systems, and Leyard, among others.

What are the key growth drivers?

-> Key growth drivers include advertiser demand for immersive experiences, automotive manufacturers embedding HUDs for safety, smart‑building initiatives driving interactive glass façades, and advancements in thin‑film transistor efficiency combined with reduced production costs.

Which region dominates the market?

-> Regional dominance information is not disclosed in the provided market overview.

What are the emerging trends?

-> Emerging trends include larger‑size high‑resolution transparent modules, expanded use in retail signage, automotive heads‑up displays, smart windows, and augmented‑reality interfaces.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...