Market Insights

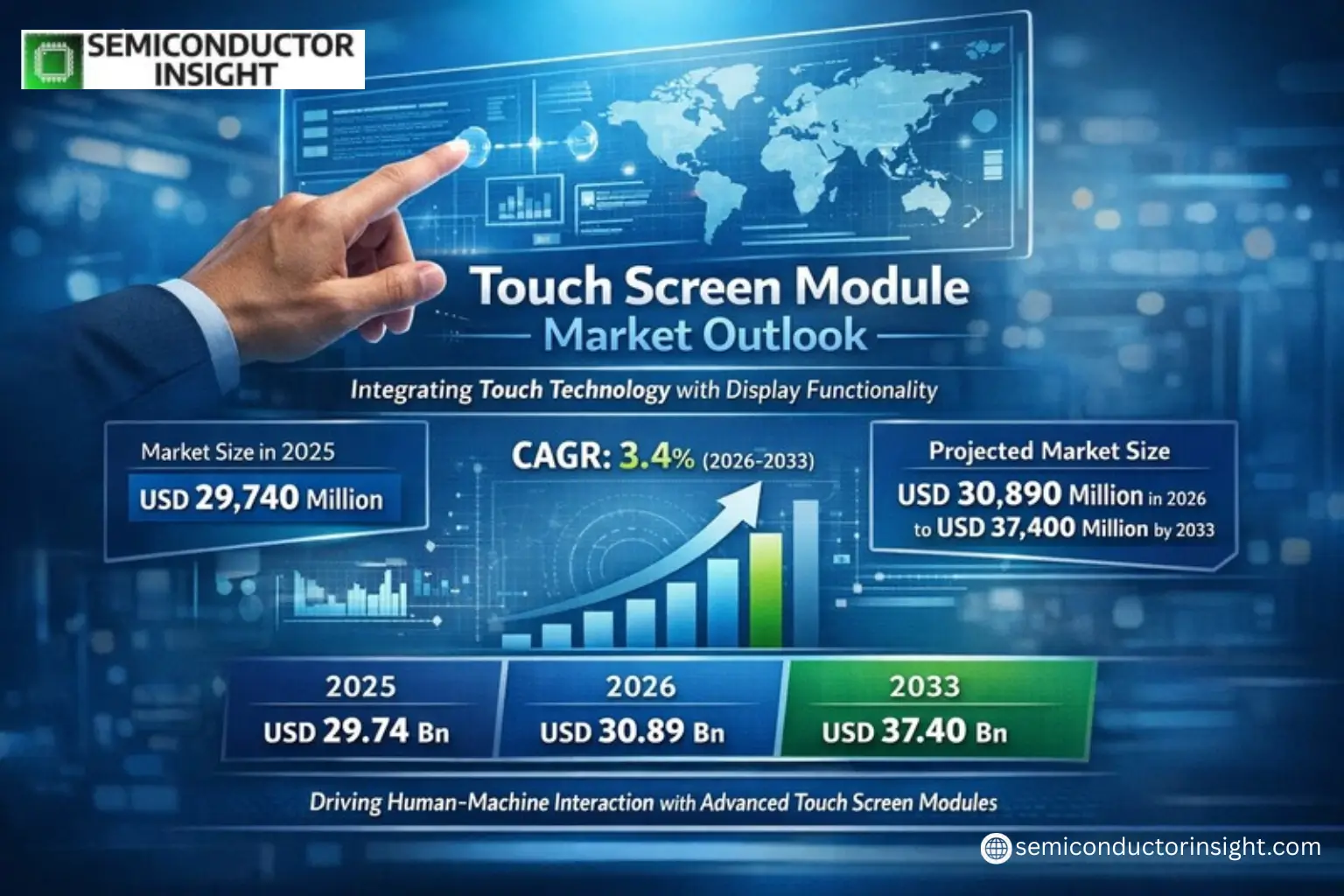

Global Touch Screen Module Market size was valued at USD 29,740 million in 2025. The market is projected to grow from USD 30,890 million in 2026 to USD 37,400 million by 2033, exhibiting a CAGR of 3.4% during the forecast period.

Touch Screen Modules are critical components that integrate touch technology with display functionality, enabling intuitive human-machine interaction. These modules detect user inputs such as taps, swipes, or multi-touch gestures and convert them into electrical signals for device control. Key technologies include resistive, capacitive (projected and surface), infrared, and surface acoustic wave solutions. Capacitive touch screens dominate the market due to their high sensitivity, durability, and multi-touch capabilities.

The market growth is driven by rising demand for smartphones, automotive displays, and industrial automation systems. Advancements like flexible OLED integration and AI-enhanced touch accuracy are accelerating adoption. However, supply chain dependencies on materials like ITO films pose cost challenges. Leading players such as Samsung Display, LG Display, and Tianma are investing in innovations like ultra-thin designs and foldable modules to maintain competitive advantage.

MARKET DRIVERS

Rising Demand for Interactive Displays

Touch Screen Module Market is experiencing growth due to increasing adoption in smartphones, tablets, and automotive infotainment systems. Demand for high-resolution multi-touch displays has surged by approximately 18% annually, backed by consumer preference for intuitive interfaces.

Advancements in Touch Technology

Technological innovations such as capacitive and resistive Touch Screen Modules are enhancing user experience with faster response times. The market is projected to grow by $5.2 billion by 2027, driven by industrial and healthcare applications.

Manufacturers are focusing on durable and energy-efficient modules to meet diverse industry demands.

MARKET CHALLENGES

High Production Costs

Touch Screen Module Market faces constraints from increasing raw material costs, particularly for indium tin oxide (ITO), which accounts for 40% of module production expenses. This impacts profit margins for small and mid-sized manufacturers.

Other Challenges

Supply Chain Disruptions

Global semiconductor shortages have delayed Touch Screen Module production, affecting delivery timelines by 20-25% in key markets.

Technical Limitations

Resistive Touch Screen Modules struggle with multi-touch functionality, creating adoption barriers in premium devices.

MARKET RESTRAINTS

Regulatory Compliance

Stringent regulations on electronic waste and hazardous materials in regions like the EU restrict material choices for Touch Screen Modules, potentially increasing compliance costs by 12-15%.

MARKET OPPORTUNITIES

Expansion in Automotive Sector

The automotive Touch Screen Module Market is projected to grow at 9% CAGR, fueled by demand for digital dashboards and ADAS interfaces in electric and autonomous vehicles.

Emerging Markets Growth

Developing economies offer significant potential, with demand for affordable Touch Screen Modules in education and retail sectors growing by 22% year-over-year.

Touch Screen Module Market ($29.74 Billion) Growth Trends

Capacitive Technology Dominates with 3.4% CAGR Projection

Global Touch Screen Module market is projected to reach $37.4 billion by 2033, growing at 3.4% CAGR from its 2025 valuation of $29.74 billion. Capacitive touch modules maintain 68% market share due to superior sensitivity and multi-touch capability, while resistive solutions remain relevant in industrial applications requiring stylus input. Emerging flexible OLED integrations and In-Cell/On-Cell technologies are driving premium segment growth.

Other Trends

Automotive Sector Accelerates Demand

Automotive applications now represent 22% of touch module demand, spurred by smart cockpit implementations in electric vehicles. Manufacturers are developing large-format (12-17 inch) modules with enhanced durability against temperature extremes and vibration. Haptic feedback adoption in automotive touchscreens grew 27% YoY in 2023.

Supply Chain and Regional Dynamics Reshaping Production

Asia-Pacific commands 58% of global production, with Chinese manufacturers increasing market share to 31% through cost-competitive solutions. However, Japanese/Korean firms retain technology leadership in flexible displays, holding 73% of patents. The industry faces material cost pressures, with ITO film prices fluctuating 15-20% annually.

Industrial & Medical Applications Show Steady Growth

Dustproof/waterproof touch modules for industrial use grew 11% in 2023, while medical device integrations account for 9% of the market. These sectors prioritize reliability over resolution, with projected 4.1% CAGR through 2030 for ruggedized solutions.

Emerging Technologies Challenge Traditional Input Methods

While voice and gesture interfaces gain traction, touch maintains 89% share in primary device interaction. The market is responding with AI-enhanced touch accuracy (error rates reduced to <0.5mm) and pressure-sensitive solutions. Foldable display shipments incorporating touch modules reached 18.2 million units in 2023, signaling new form factor opportunities.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Touch Screen Module Market dominated by Asian manufacturers with technological leadership from Japan and Korea

Touch Screen Module Market remains highly concentrated, with Samsung Display and LG Display leading in premium capacitive touch solutions for smartphones and automotive applications. These Korean manufacturers control approximately 35% of the global market share through advanced OLED touch integration technologies. Japanese firms like Sharp and Nissha maintain strong positions in high-reliability industrial touch panels, leveraging patented film sensor architectures. Chinese suppliers including TPK and Tianma are rapidly catching up through aggressive capacity expansion and government-supported R&D initiatives, particularly in mid-range consumer electronics segments.

Emerging players from Taiwan (CANDO, Youngfast) and China (O-Film, Goworld) are gaining traction in cost-sensitive markets through optimized supply chains. Specialized manufacturers such as 3M and Fujitsu focus on niche segments demanding extreme durability, with products featuring anti-glare coatings and wide temperature tolerance. The competitive landscape is witnessing increased vertical integration as display panel makers like BOE and Innolux enter the touch module business, while touch specialists respond with value-added solutions like force touch and waterproofing technologies.

List of Key Touch Screen Module Companies Profiled

- Samsung Display

- LG Display

- Sharp Corporation

- Nissha Printing

- TPK Holding

- Tianma Microelectronics

- 3M Touch Systems

- Fujitsu Components

- SHENZHEN O-FILM TECH

- CANDO Corporation

- Young Fast Optoelectronics

- JTOUCH Corporation

- Guangdong Goworld

- Wuhu Token Science

- Shenzhen Laibao Hi-Tech

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Capacitive Touch Screen dominates current market demand due to superior performance characteristics:

|

| By Application |

|

Smartphone remains the primary growth driver with evolving requirements:

|

| By End User |

|

Consumer Electronics demonstrates the most dynamic innovation cycle:

|

| By Technology |

|

In-Cell Technology gaining strong momentum across industries:

|

| By Screen Size |

|

Small Screen solutions show strongest market penetration currently:

|

Regional Analysis: Global Touch Screen Module Market

Asia-Pacific’s integrated supply chain for touch panels combines specialized glass suppliers, IC manufacturers, and assembly plants within proximity, reducing production costs. The region accounts for over 60% of global touch module component manufacturing.

The smartphone and tablet markets in China and India drive touch module demand. Mid-range device manufacturers increasingly adopt premium touch technologies previously reserved for flagship models, expanding market opportunities.

Japanese automakers lead in implementing advanced touchscreen dashboards. The transition from physical buttons to touch interfaces in vehicles creates new demand for rugged, sunlight-readable touch modules with haptic feedback.

Southeast Asian factories increasingly deploy touch-controlled machinery interfaces. The durability requirements in industrial environments push innovations in glove-compatible and water-resistant touch modules.

North America

North America remains a technology innovation hub for advanced Touch Screen Module applications. The region’s strong R&D culture drives development of next-generation technologies like force touch and seamless OLED-integrated touch sensors. The automotive sector shows particularly high adoption rates for large-format touch displays, with premium brands incorporating multi-touch capabilities. Healthcare applications have grown significantly, with touch interfaces used in medical imaging systems and diagnostic equipment. The U.S. defense sector’s investment in rugged touch displays for field operations further diversifies market opportunities.

Europe

European manufacturers focus on high-precision touch modules for specialized applications. The automotive industry demands curved and flexible touchscreens for premium vehicle interiors, while industrial equipment suppliers require touch solutions that withstand extreme temperatures. Stringent EU regulations push development of eco-friendly touch module materials and energy-efficient production processes. Germany’s industrial automation sector and France’s aerospace industry present key growth areas for ruggedized touch interfaces with advanced gesture control capabilities.

South America

Touch Screen Module Market in South America shows steady growth, led by Brazil’s consumer electronics sector and Argentina’s emerging digital signage industry. Although smaller than other regions, local demand benefits from increasing smartphone penetration and government digitalization initiatives. Challenges include higher import costs for advanced touch components and limited local manufacturing capabilities. However, partnerships between regional brands and Asian manufacturers are helping bridge this technology gap for mid-range touchscreen products.

Middle East & Africa

This region experiences growing touch module demand from smart city projects and retail digital transformation. Gulf countries invest heavily in large-format touch displays for public spaces and corporate environments. Africa’s mobile-first economy drives demand for affordable touchscreen devices, with local assembly plants emerging in key markets. The educational technology sector presents new opportunities, with governments deploying touch-enabled learning devices in schools across urban centers.

Report Scope

This market research report provides a comprehensive analysis of the Touch Screen Module Market , covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of touch technology in powering advancements across industries such as consumer electronics, automotive displays, industrial automation, and medical devices.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (resistive, capacitive, piezoelectric), application (smartphone, tablet & PC, automotive), and end-user industry to identify high-growth segments.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies like flexible OLEDs, Mini LED backlighting, AI-driven touch accuracy improvements, and In-Cell/On-Cell integration.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with supply chain constraints and technological disruption risks.

- Stakeholder Insights: Strategic perspectives for component suppliers, OEMs, system integrators, and investors.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Touch Screen Module Market?

-> Touch Screen Module Market size was valued at USD 29,740 million in 2025. The market is projected to grow from USD 30,890 million in 2026 to USD 37,400 million by 2033, exhibiting a CAGR of 3.4% during the forecast period.

Which key companies operate in Touch Screen Module Market?

-> Key players include Tianma, Samsung Display, 3M, LG, Fujitsu, Nissha, Sharp, TPK, and SHENZHEN O-FILM THCH, among others.

What are the key growth drivers?

-> Key growth drivers include smartphone innovations, automotive smart cockpit demand, industrial automation, and AI-enhanced touch technology.

Which region dominates the market?

-> Asia-Pacific dominates the market, led by China and South Korea’s display manufacturing capabilities.

What are the emerging trends?

-> Emerging trends include foldable displays, haptic feedback integration, ultra-narrow bezel designs, and green manufacturing initiatives.

What is the projected CAGR?

-> The market is expected to grow at a CAGR of 3.4% during 2025-2033.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...