MARKET INSIGHTS

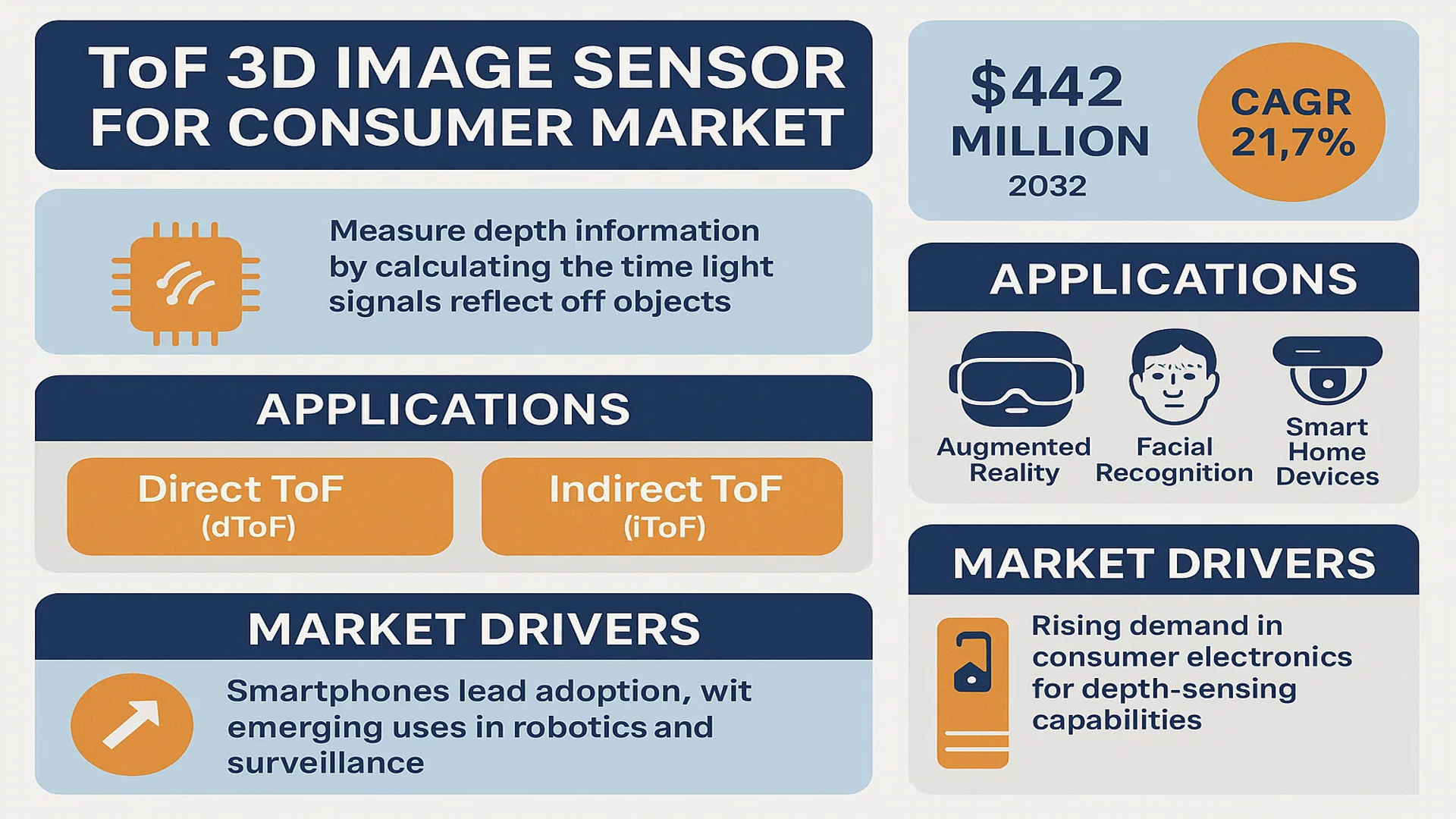

The global ToF 3D Image Sensor for Consumer Market was valued at 142 million in 2024 and is projected to reach US$ 545 million by 2032, at a CAGR of 21.7% during the forecast period.

Time-of-Flight (ToF) 3D image sensors are advanced sensing devices that measure depth information by calculating the time taken for light signals to reflect off objects. These sensors enable accurate three-dimensional mapping across various applications, from augmented reality (AR) in smartphones to gesture recognition in smart home devices. The technology is primarily categorized into Direct ToF (dToF) and Indirect ToF (iToF), each offering distinct advantages in resolution and power efficiency.

The market’s exponential growth is driven by surging demand for depth-sensing capabilities in consumer electronics, particularly for facial recognition, AR/VR experiences, and advanced photography. While smartphone manufacturers remain the largest adopters, emerging applications in domestic robotics and smart surveillance systems are creating new growth avenues. Recent technological advancements, such as Sony’s 2-layer transistor-pixel stacked CMOS image sensors, are further enhancing performance while reducing form factors, accelerating mainstream adoption.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of AR/VR Applications to Accelerate ToF Sensor Adoption

The augmented and virtual reality market is projected to reach over $300 billion globally by 2026, driving substantial demand for ToF 3D image sensors. These sensors enable precise motion tracking and environment mapping – critical capabilities for immersive AR/VR experiences. Leading headset manufacturers are increasingly integrating ToF sensors for improved spatial awareness and hand gesture recognition. For instance, next-generation mixed reality headsets launched in 2023 feature advanced ToF sensors with sub-millimeter depth accuracy, significantly enhancing user interaction capabilities.

Smartphone Innovation Fuels Global Market Expansion

Smartphone manufacturers continue to drive the consumer ToF sensor market, with over 450 million ToF-equipped devices shipped in 2023 alone. The technology enables critical features like portrait mode photography, 3D facial recognition, and AR gaming. Flagship models now routinely incorporate high-resolution ToF sensors with advanced capabilities such as real-time depth mapping and improved low-light performance. This trend is expanding into mid-range devices as production costs decrease, with ToF sensor ASPs dropping nearly 30% since 2021.

Advancements in Domestic Robotics Create New Demand Streams

The consumer robotics sector is experiencing rapid growth, with home cleaning robots accounting for over 60% of shipments in 2023. These devices increasingly rely on ToF sensors for navigation and obstacle detection, as they offer superior performance to traditional IR sensors in varying lighting conditions. Recent innovations include multi-zone depth sensing and AI-powered object classification – capabilities that are driving replacement cycles and premium product adoption. The integration of ToF sensors in robotic vacuum cleaners has shown to improve cleaning efficiency by up to 40% in independent testing, creating strong consumer demand.

MARKET RESTRAINTS

High Component Costs and Supply Chain Constraints Limit Market Penetration

While ToF sensor adoption is growing, widespread implementation faces significant cost barriers. Premium ToF modules currently cost 3-4 times more than conventional 2D sensors, making them prohibitive for many mid-range consumer applications. Supply chain challenges, particularly for specialized optical components, have further constrained production capacity. These factors contribute to extended lead times of 12-16 weeks for some ToF sensor variants, discouraging adoption in price-sensitive market segments.

Other Restraints

Technical Limitations in Outdoor Environments

ToF performance degrades significantly in direct sunlight and other high-ambient-light conditions, limiting outdoor applications. Sensor accuracy can decrease by up to 60% in bright environments due to photon noise and interference, creating reliability concerns for certain use cases.

Power Consumption Challenges

Current ToF implementations consume substantially more power than alternative depth sensing technologies, reducing battery life in portable devices. Active illumination systems in particular require significant energy, with some implementations increasing overall system power draw by 15-20%.

MARKET OPPORTUNITIES

Emerging Applications in Smart Home Ecosystems Present Growth Potential

The smart home market is projected to incorporate over 50 million ToF sensors annually by 2026, creating significant expansion opportunities. Emerging applications include presence detection for lighting control, gesture-based appliance operation, and security system enhancements. Recent innovations demonstrate successful integration of ToF sensors in smart mirrors for fitness tracking and in kitchen appliances for touchless control, opening new verticals for market penetration.

Automotive In-cabin Sensing Drives Next Wave of Adoption

Automotive manufacturers are increasingly adopting ToF sensors for driver monitoring and in-cabin occupant detection. Regulatory mandates for advanced driver attention systems are accelerating this trend, with forecasts suggesting 25% of new vehicles will incorporate ToF-based monitoring by 2027. Recent product launches demonstrate successful applications in child presence detection and airbag deployment optimization, potentially preventing thousands of injuries annually.

MARKET CHALLENGES

Integration Challenges Create Barriers to Widespread Implementation

While ToF technology offers compelling capabilities, implementation requires complex system integration that many consumer electronics manufacturers find challenging. The need for specialized optical alignment, thermal management, and signal processing creates development cycles 30-40% longer than conventional sensor integration. These technical hurdles have delayed product launches across multiple consumer segments, with some OEMs experiencing 6-9 month delays in bringing ToF-enabled devices to market.

Other Challenges

Data Processing Requirements

ToF sensors generate significantly more data than traditional 2D sensors, requiring dedicated processing resources. The computational overhead can increase system costs by 15-25%, a critical factor in cost-sensitive consumer applications where margins are already thin.

Standardization and Interoperability Gaps

The lack of unified standards for ToF implementations creates compatibility issues across platforms. Proprietary interfaces and data formats hinder ecosystem development, with different manufacturers requiring custom integration solutions for what should be standardized functionality.

ToF 3D IMAGE SENSOR FOR CONSUMER MARKET TRENDS

Smartphone Integration and AR/VR Adoption Drive Explosive Market Growth

The global ToF 3D image sensor market is experiencing unprecedented growth, fueled primarily by widespread adoption in smartphones and augmented reality devices. Time-of-flight technology, which measures the time taken for light to reflect off objects to create depth maps, has become critical for facial recognition, portrait-mode photography, and gesture control in flagship smartphones. With over 45% of premium smartphones now incorporating ToF sensors, manufacturers are racing to improve accuracy while reducing power consumption and component size. Beyond mobile devices, the VR/AR headset market, projected to exceed $50 billion by 2027, is increasingly relying on ToF sensors for precise environment mapping and interactive experiences.

Other Trends

Automotive Safety Applications

While consumer electronics dominate current demand, automotive applications are emerging as a significant growth vector. ToF sensors enable advanced driver monitoring systems that detect driver fatigue and distraction with millimeter-level precision. The technology is also being integrated into in-cabin gesture control systems, with major automakers piloting systems that replace physical buttons with touchless interfaces. This sector is particularly promising as autonomous vehicle development progresses, with ToF sensors providing crucial depth perception for interior monitoring and passenger safety features.

Miniaturization and Cost Reduction Accelerate Market Penetration

Recent breakthroughs in semiconductor manufacturing have enabled dramatic reductions in ToF sensor size and production costs. Leading manufacturers have successfully shrunk sensor packages by over 30% while maintaining or improving performance characteristics. This miniaturization trend is unlocking new applications in wearable devices, smart home products, and even gaming peripherals. Simultaneously, economies of scale achieved through mass smartphone adoption have driven average selling prices down by approximately 18% annually since 2020, making the technology accessible to mid-range consumer electronics. These developments are creating a virtuous cycle of wider adoption and faster technological advancement throughout the industry.

Competitive Landscape and Technological Specialization

The market is witnessing intense competition between established semiconductor giants and innovative startups, with each pursuing distinct technological approaches. Some players focus on optimizing direct ToF systems for maximum range and accuracy in industrial applications, while others refine indirect ToF solutions better suited for consumer electronics. Recent mergers and acquisitions have reshaped the competitive landscape, with strategic partnerships forming between sensor manufacturers and AI software providers to create complete depth-sensing solutions. This specialization is driving rapid innovation, with each segment achieving notable performance improvements in their respective focus areas.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants and Emerging Innovators Compete in Burgeoning ToF Sensor Market

The Time-of-Flight (ToF) 3D image sensor market presents a dynamic competitive environment where established semiconductor leaders compete with specialized sensor developers. Infineon Technologies and STMicroelectronics currently dominate the landscape, collectively holding over 30% market share in 2024. These companies benefit from their integrated semiconductor manufacturing capabilities and strategic partnerships with smartphone OEMs – particularly in the Android ecosystem where ToF adoption is strongest.

While the market remains semi-consolidated, several niche players are gaining traction through technological differentiation. Texas Instruments has made significant inroads in industrial applications, while AMS (now part of ams OSRAM) has secured design wins in Apple’s ecosystem with its advanced indirect ToF solutions. The competitive dynamics are further complicated by emerging Chinese firms like Orbbec that are aggressively pricing their solutions to capture share in cost-sensitive consumer electronics segments.

Market leaders are responding to these challenges through both organic R&D and strategic acquisitions. For instance, STMicroelectronics’ 2023 acquisition of a French ToF specialist significantly enhanced its depth-sensing capabilities for AR/VR applications. Similarly, Infineon continues to invest in next-generation SPAD (single-photon avalanche diode) technology that could redefine the power efficiency benchmarks for mobile devices.

Meanwhile, Japanese players like OMRON are leveraging their expertise in industrial automation to develop ruggedized ToF solutions for domestic robots and smart appliances. The competitive pressure is driving rapid innovation cycles, with most major players now committing to bi-annual product refreshes to maintain technological leadership in this fast-evolving sector.

List of Key ToF 3D Image Sensor Companies Profiled

- Infineon Technologies (Germany)

- Texas Instruments (U.S.)

- Analog Devices (U.S.)

- STMicroelectronics (Switzerland)

- OMRON Corporation (Japan)

- Nuvoton Technology (Taiwan)

- Brookman Technology (Japan)

- ams OSRAM (Austria)

- Elmos Semiconductor (Germany)

- PMD Technologies (Germany)

- Espros Photonics (Switzerland)

- Orbbec (China)

- Evisionics (Israel)

- Opnous (U.S.)

Segment Analysis:

By Type

Direct ToF Segment Leads Due to Higher Accuracy in Depth Sensing Applications

The market is segmented based on type into:

- Direct ToF

- Subtypes: Single-photon avalanche diode (SPAD), Vertical-cavity surface-emitting laser (VCSEL), and others

- Indirect ToF

- Subtypes: Phase-shift measurement, Amplitude modulation, and others

By Application

Personal Electronics Segment Dominates with Rising Adoption in Smartphones and AR/VR Devices

The market is segmented based on application into:

- Monitoring Systems

- Domestic Robots

- Personal Electronics

- Subtypes: Smartphones, Tablets, AR/VR Headsets, and others

- Others

By End User

Consumer Electronics Manufacturers Drive Market Growth Through Advanced Device Integration

The market is segmented based on end user into:

- Smartphone Manufacturers

- AR/VR Device Manufacturers

- Home Automation System Providers

- Security Solution Providers

- Others

Regional Analysis: ToF 3D Image Sensor for Consumer Market

Asia-Pacific

As the dominant region in ToF 3D image sensor adoption, Asia-Pacific holds over 48% of the global market share in 2024, driven by massive smartphone production and next-gen consumer electronics development. China leads this expansion with smartphone OEMs like Huawei, Xiaomi, and OPPO integrating ToF sensors for facial recognition and AR applications. Meanwhile, South Korea’s Samsung and LG continue to push boundaries in premium devices featuring depth-sensing cameras. Japan maintains strong demand for ToF in robotics and industrial applications, while India emerges as a high-growth market with increasing localization of electronics manufacturing under initiatives like Make in India. The region benefits from established semiconductor supply chains and aggressive R&D investments (China allocated $43 billion to semiconductor self-sufficiency in 2023 alone), making it the innovation hub for cost-optimized ToF solutions.

North America

North America represents the second-largest ToF 3D sensor market, characterized by early adoption in AR/VR devices and automation technologies. The U.S. accounts for nearly 75% of regional demand, with tech giants like Apple (implementing ToF in iPads and iPhones) and Meta (for VR headsets) driving innovation. Silicon Valley remains the epicenter for advanced ToF applications, particularly in gesture recognition and spatial computing. Canada shows growing traction in automotive and smart home applications, leveraging partnerships between sensor manufacturers and IoT developers. Strict data privacy regulations influence sensor specifications, with emphasis on secure biometric implementations. The region’s mature tech ecosystem ensures premium positioning of ToF-enabled products, though higher costs limit penetration in budget consumer segments.

Europe

European demand focuses on high-precision ToF applications in industrial and automotive sectors, with Germany and France leading adoption. Automotive OEMs like BMW and Volkswagen integrate ToF for in-cabin monitoring and autonomous driving systems, while consumer electronics growth remains steady through brands like Bosch and STMicroelectronics. The EU’s emphasis on data privacy (GDPR compliance) shapes sensor development, with companies prioritizing secure, low-power designs. While smartphone adoption lags behind Asia-Pacific, niche applications in smart appliances (e.g., Siemens’ touchless controls) and healthcare devices present growth opportunities. Regional R&D initiatives like Horizon Europe allocate significant funding to 3D sensing advancements, aiming to reduce dependency on non-European semiconductor suppliers amidst global chip shortages.

Middle East & Africa

This emerging market shows promising growth in security and smart city applications, particularly in UAE and Saudi Arabia. Dubai’s smart city initiatives deploy ToF sensors for facial recognition in public infrastructure, while South Africa explores mining automation uses. Limited local manufacturing means most sensors are imported, creating cost challenges. However, rising disposable incomes drive demand for premium smartphones with ToF capabilities, and regional governments actively partner with global tech firms to develop local expertise. The market’s growth trajectory remains uneven, with oil-dependent economies prioritizing ToF investments more aggressively than others. Long-term potential exists in retail analytics and contactless payment systems as digital transformation accelerates.

South America

Brazil dominates regional ToF sensor demand, primarily for smartphone applications, while Argentina sees growth in agricultural automation. Economic volatility restricts widespread adoption, causing manufacturers to prioritize cost-effective indirect ToF solutions over premium direct ToF variants. The gaming industry presents unexpected growth potential, with Brazilian developers creating AR content for global markets. Chile and Colombia show interest in ToF for border security applications, though budget constraints slow implementation. Regional trade agreements with Asian suppliers help moderate prices, but lack of local semiconductor infrastructure keeps the market heavily import-dependent. Consumer awareness of ToF benefits remains low outside urban tech hubs, requiring targeted marketing by device manufacturers.

Report Scope

This market research report provides a comprehensive analysis of the global and regional ToF 3D Image Sensor for Consumer markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global ToF 3D Image Sensor for Consumer market was valued at USD 142 million in 2024 and is projected to reach USD 545 million by 2032, growing at a CAGR of 21.7%.

- Segmentation Analysis: Detailed breakdown by product type (Direct ToF, Indirect ToF), application (Monitoring Systems, Domestic Robots, Personal Electronics), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis for key markets like China, US, Japan, and Germany.

- Competitive Landscape: Profiles of leading market participants including Infineon Technologies, Texas Instruments, STMicroelectronics, and Sony, covering their product offerings, R&D focus, manufacturing capacity, and recent M&A activities.

- Technology Trends & Innovation: Assessment of emerging ToF technologies, integration with AR/VR systems, smartphone applications, and evolving industry standards for 3D sensing.

- Market Drivers & Restraints: Evaluation of factors driving market growth (rising demand for facial recognition, AR applications) along with challenges (high development costs, technical complexity).

- Stakeholder Analysis: Insights for sensor manufacturers, consumer electronics OEMs, component suppliers, and investors regarding market opportunities and strategic positioning.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global ToF 3D Image Sensor for Consumer Market?

-> ToF 3D Image Sensor for Consumer Market was valued at 142 million in 2024 and is projected to reach US$ 545 million by 2032, at a CAGR of 21.7% during the forecast period..

Which key companies operate in Global ToF 3D Image Sensor for Consumer Market?

-> Key players include Infineon Technologies, Texas Instruments, STMicroelectronics, Sony, AMS, and PMD Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption in smartphones, increasing demand for AR/VR applications, and advancements in facial recognition technology.

Which region dominates the market?

-> Asia-Pacific is the largest market, driven by smartphone manufacturers in China and South Korea, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with AI for advanced applications, and development of low-power consumption solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...