MARKET INSIGHTS

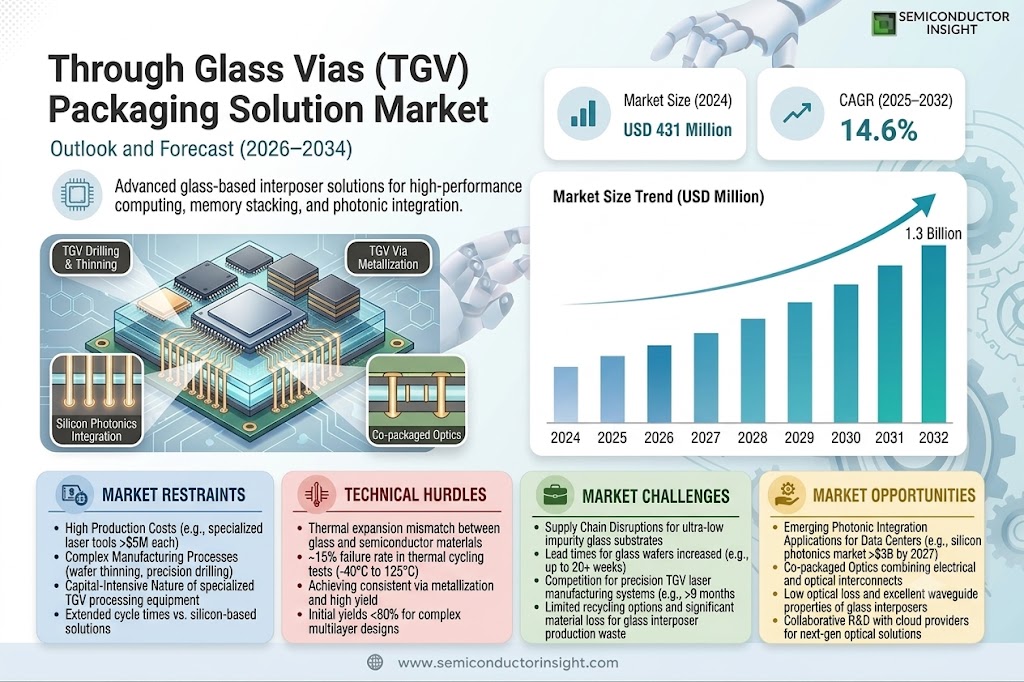

The global Through Glass Vias (TGV) Packaging Solution Market size was valued at US$ 431 million in 2024 and is projected to reach US$ 1.3 billion by 2032, at a CAGR of 14.6% during the forecast period 2025-2032. The U.S. market accounted for 28% of global revenue in 2024, while China is expected to witness the highest growth rate of 18.6% CAGR through 2032.

Through Glass Vias (TGV) are advanced interconnects that enable vertical electrical connections through glass substrates, offering superior high-frequency performance and thermal stability compared to traditional silicon vias. These solutions are critical for applications requiring hermetic sealing, high-speed data transmission, and miniaturization, including semiconductor glass interposers, 3D integrated passive devices (IPDs), and MEMS sensors.

The market growth is driven by increasing demand for compact electronic devices and the rising adoption of 5G and IoT technologies. The 150 mm wafer segment currently dominates with 42% market share, though 300 mm wafers are gaining traction in high-volume manufacturing. Key players like Corning and SCHOTT are investing heavily in TGV technology, with Corning launching new ultra-thin glass solutions in Q1 2024 specifically for advanced packaging applications.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Demand for Advanced Semiconductor Packaging to Accelerate TGV Adoption

The semiconductor industry’s relentless pursuit of miniaturization and performance enhancement is pushing through glass via (TGV) packaging solutions into the spotlight. As Moore’s Law approaches physical limits, 3D packaging technologies like TGV have emerged as critical enablers for next-generation electronics. The global semiconductor packaging market, valued at over $30 billion, is increasingly adopting glass interposers for their superior high-frequency performance and thermal management capabilities. Major foundries report 40% faster signal transmission in TGV-based packages compared to traditional silicon interposers, making them ideal for 5G infrastructure and high-performance computing applications.

Growth in MEMS & Sensor Applications Fueling Market Expansion

The MEMS and sensor device segment is experiencing exponential growth, with projected annual shipments exceeding 30 billion units by 2026. Glass packaging solutions offer distinct advantages for MEMS devices because of their excellent hermetic sealing properties and compatibility with wafer-level packaging processes. Emerging applications in automotive LiDAR systems, biomedical sensors, and IoT devices are creating strong demand for TGV-enabled packages. The automotive sector alone is expected to account for nearly 25% of MEMS packaging demand, driven by advanced driver assistance systems (ADAS) that require highly reliable packaging solutions.

Moreover, recent advancements in glass via fabrication technologies have significantly improved production yields while reducing costs. Several leading manufacturers have demonstrated TGV via densities exceeding 10,000 vias per cm² with aspect ratios up to 10:1, opening new possibilities for ultra-high-density interconnects.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing Processes Limit Widespread Adoption

While TGV technology offers compelling technical benefits, its adoption faces significant cost barriers. The specialized laser drilling and wafer thinning processes required for glass interposers can increase packaging costs by 30-50% compared to conventional solutions. Precision glass processing equipment often carries price tags exceeding $5 million per tool, creating substantial capital expenditure requirements for manufacturers. Furthermore, the typical cycle time for TGV formation is nearly twice that of silicon via processes, impacting overall production efficiency.

Material Compatibility Issues Present Technical Hurdles

The thermal expansion mismatch between glass substrates and semiconductor materials creates significant challenges in reliability testing. Current industry data shows that nearly 15% of TGV packages fail thermal cycling tests between -40°C to 125°C, raising concerns about long-term durability in harsh environments. Additionally, achieving consistent via metallization with high yield remains technically demanding, with leading manufacturers reporting initial yields below 80% for complex multilayer designs. These technical constraints have slowed adoption in mission-critical applications where reliability is paramount.

MARKET CHALLENGES

Supply Chain Disruptions Impacting Critical Material Availability

The TGV packaging ecosystem faces mounting challenges from global supply chain instability. Specialty glass substrates requiring ultra-low impurity levels are primarily sourced from a handful of suppliers, creating single-point vulnerabilities. Recent industry surveys indicate that lead times for precision glass wafers have extended from 8-12 weeks to 20+ weeks, disrupting production schedules. Furthermore, the semiconductor industry’s rapid capacity expansion has created competition for essential TGV manufacturing equipment, with delivery times for critical laser systems exceeding nine months in some cases.

Another significant challenge lies in the limited recycling options for glass interposer production waste. Unlike silicon wafers which can be reclaimed, glass processing generates significant material loss with current recycling rates below 30%. This not only raises environmental concerns but also contributes to higher material costs across the supply chain.

MARKET OPPORTUNITIES

Emerging Photonic Integration Applications Create New Growth Avenues

The rapid development of silicon photonics presents a major growth opportunity for TGV solutions. Glass interposers are ideal for photonic integrated circuits (PICs) because of their low optical loss and excellent waveguide properties. Industry projections suggest the silicon photonics market could surpass $3 billion by 2027, with data center optical transceivers accounting for over 60% of demand. Several leading cloud providers are actively evaluating TGV-based solutions for next-generation co-packaged optics that combine electrical and optical interconnects in a single package.

Expansion in Medical Electronics Opens New Application Areas

The medical device industry’s growing need for biocompatible, miniaturized packaging is driving innovation in glass-based solutions. Implantable devices and diagnostic sensors benefit from glass packaging’s superior fluid compatibility and long-term stability in biological environments. The global market for medical sensors is projected to grow at 8% CAGR through 2030, with neural interfaces and continuous monitoring devices representing particularly promising applications. Recent advances in hermetic glass sealing techniques have enabled new product designs that were previously unattainable with conventional packaging approaches.

THROUGH GLASS VIAS (TGV) PACKAGING SOLUTION MARKET TRENDS

Miniaturization of Electronic Devices Driving TGV Adoption

The Through Glass Vias (TGV) Packaging Solution market is witnessing robust growth, primarily fueled by the increasing demand for miniaturized electronic devices in consumer electronics, medical implants, and advanced automotive systems. As compact and high-performance packaging solutions become critical for next-generation applications, TGV technology offers superior electrical performance, thermal stability, and integration capabilities compared to traditional Through Silicon Vias (TSVs). Recent data indicates that the global TGV packaging market is projected to grow at a CAGR of over 18% from 2024 to 2032, with the semiconductor glass interposer segment alone expected to contribute more than 45% of the total revenue by 2030. The rise in 5G, IoT, and AI-driven products is further accelerating this trend, as these applications require high-density interconnects with low signal loss and excellent RF performance.

Other Trends

Expansion in Advanced 3D IC Packaging

3D integrated circuit (IC) packaging has emerged as a key driver for TGV adoption, particularly in high-performance computing (HPC), artificial intelligence (AI) chips, and memory stacking applications. Unlike traditional packaging methods, TGV-enabled solutions enable vertical integration of multiple dies with reduced parasitic effects and improved power efficiency. Glass substrates provide advantages such as lower processing temperatures, cost-effectiveness for large panels, and compatibility with existing wafer-level packaging techniques. The 300 mm wafer segment is growing rapidly, with a projected 20% CAGR by 2032, as major semiconductor foundries shift toward glass-based substrates to meet the increasing demand for heterogeneous integration.

Growing Demand in MEMS & Optical Applications

The expansion of MEMS & sensor devices and optical communication systems is creating new opportunities for TGV packaging solutions. Glass substrates offer exceptional transparency for photonic applications, making them ideal for devices such as LiDAR sensors, biomedical imaging systems, and augmented reality (AR) components. With the MEMS market expected to surpass $28 billion by 2027, manufacturers are increasingly adopting TGV technology to enhance device reliability and performance. Additionally, advancements in hermetic sealing for glass vias are addressing critical challenges in harsh environment applications, further broadening the adoption in medical implants and aerospace electronics.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Technological Leadership Drive Competition in TGV Packaging

The global Through Glass Vias (TGV) Packaging Solution market features a dynamic competitive environment with dominant players leveraging technological expertise and production scalability. Corning Incorporated maintains a leadership position, capturing approximately 22% of the 2024 market revenue share due to its proprietary glass substrate technologies and strategic collaborations with semiconductor giants.

LPKF Laser & Electronics and Samtec collectively account for nearly 30% of the market, benefiting from their specialized laser drilling systems and high-performance interconnects respectively. These companies are expanding their manufacturing capabilities across Asia-Pacific to meet growing demand for 3D glass interposers in 5G and IoT applications.

Mid-tier players like Kiso Micro and Tecnisco are gaining traction through wafer-level packaging innovations, particularly in the 200mm wafer segment which shows a projected 11.7% CAGR through 2032. Recent industry consolidation has seen larger players acquiring niche technology providers, as evidenced by NSG Group’s 2023 acquisition of Allvia’s TGV patent portfolio.

While Japanese and American companies currently dominate, Chinese manufacturers including AGC and Vitrion are rapidly closing the technology gap through substantial R&D investments, particularly in MEMS packaging solutions.

List of Key Through Glass Vias (TGV) Packaging Solution Providers

- Corning Incorporated (U.S.)

- LPKF Laser & Electronics AG (Germany)

- Samtec Inc. (U.S.)

- Kiso Micro Co.LTD (Japan)

- Tecnisco Limited (Japan)

- Microplex (Germany)

- Plan Optik AG (Germany)

- NSG Group (Japan)

- Allvia, Inc. (U.S.)

- AGC Inc. (Japan)

Segment Analysis:

By Type

150 mm Wafer Segment Leads Due to Cost-Effective Manufacturing Solutions

The market is segmented based on type into:

- 150 mm Wafer

- Applications: Mid-range semiconductor packaging, consumer electronics

- 200 mm Wafer

- 300 mm Wafer

- Others

By Application

Semiconductor Glass Interposer Segment Dominates with High Demand in Advanced Packaging Solutions

The market is segmented based on application into:

- Semiconductor Glass Interposer

- 3D Glass IPD

- MEMS & Sensor Device

- Others

By End User

Consumer Electronics Sector Accounts for Significant Adoption Due to Miniaturization Trends

The market is segmented based on end user into:

- Consumer Electronics

- Automotive

- Healthcare

- Telecommunications

- Others

Regional Analysis: Through Glass Vias (TGV) Packaging Solution Market

Asia-Pacific

The Asia-Pacific region dominates the global TGV packaging solution market, driven by strong semiconductor manufacturing ecosystems in China, Japan, South Korea, and Taiwan. China alone accounts for over 35% of global semiconductor production capacity, creating immense demand for advanced packaging technologies like TGV. The region benefits from robust government support for electronics manufacturing, with initiatives like Japan’s “Semiconductor and Digital Industry Strategy” and South Korea’s K-Semiconductor Belt fostering innovation. While cost-sensitive markets still favor traditional packaging methods, increasing adoption of 5G, AI, and IoT devices is accelerating TGV implementation. Leading manufacturers like AGC and NSG Group have established strong production bases across the region to serve local demand.

North America

North America represents a high-growth market for TGV solutions, particularly for defense and aerospace applications where glass-based packaging offers superior reliability. The U.S. accounts for over 70% of regional demand, supported by substantial R&D investments from companies like Corning and significant defense sector spending. Challenges include high production costs and limited local manufacturing capacity, pushing many North American firms to partner with Asian foundries. However, recent CHIPS Act funding is stimulating domestic advanced packaging capabilities, with several TGV-related projects receiving government support. MEMS and sensor applications show particularly strong growth potential as industries adopt more sophisticated IoT and automation technologies.

Europe

Europe maintains a specialized position in the TGV market, focusing on high-performance applications in automotive, medical, and industrial sectors. Germany and France lead adoption due to their strong MEMS and photonics industries, with companies like SCHOTT and LPKF driving innovation. The region benefits from EU-funded semiconductor initiatives but faces challenges from higher production costs compared to Asia. Stringent environmental regulations promote use of TGV’s lead-free and RoHS-compliant properties. While lagging behind Asia in volume production, European manufacturers excel in niche applications like biomedical sensors and high-frequency RF components, where glass interposers offer technical advantages over silicon.

Middle East & Africa

The MEA region represents an emerging market for TGV technology, with growth concentrated in Israel and UAE as they develop localized high-tech manufacturing capabilities. Israel’s strong semiconductor design industry creates demand for advanced packaging, while UAE invests in modern electronics manufacturing through initiatives like Dubai’s Silicon Oasis. However, limited local production infrastructure means most TGV components must be imported from Asia or Europe. The region shows potential for specialized applications in harsh environments (such as oil/gas sensing) where glass packaging’s thermal and chemical stability proves advantageous. Market growth remains constrained by high costs and lack of supporting ecosystem.

South America

South America represents the smallest TGV market currently, though Brazil and Argentina show early adoption in medical and aerospace sectors. Economic volatility and limited semiconductor manufacturing presence hinder widespread adoption, with most applications relying on imported finished components. Domestic companies focus primarily on lower-cost packaging alternatives, though some research institutions are exploring TGV applications for specialized sensors. The region’s growing electronics assembly industry may drive future demand, particularly if regional trade agreements facilitate technology transfer from North American and Asian partners.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Through Glass Vias (TGV) Packaging Solution markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global TGV Packaging Solution market was valued at US$ 431 million in 2024 and is projected to reach US$ 1.3 billion by 2032, growing at a CAGR of 14.6% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (150 mm Wafer, 200 mm Wafer, 300 mm Wafer, Others), application (Semiconductor Glass Interposer, 3D Glass IPD, MEMS & Sensor Device, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates with 48.2% market share in 2024, driven by semiconductor manufacturing growth in China, Japan, and South Korea.

- Competitive Landscape: Profiles of leading market participants including Corning, LPKF, Samtec, Kiso Micro Co.LTD, Tecnisco, Microplex, Plan Optik, NSG Group, Allvia, AGC, SCHOTT, and Vitrion, covering their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging TGV fabrication techniques, integration with advanced packaging solutions, and development of ultra-thin glass substrates for next-generation applications.

- Market Drivers & Restraints: Evaluation of factors such as increasing demand for high-density interconnects, growth in 5G and IoT devices, and automotive electronics expansion, along with challenges like high manufacturing costs and technical complexities.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, packaging solution providers, equipment suppliers, and investors regarding market opportunities and competitive positioning.

This report combines primary research with industry experts and secondary data from authoritative sources to deliver accurate market intelligence and actionable insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Through Glass Vias (TGV) Packaging Solution Market?

-> Through Glass Vias (TGV) Packaging Solution Market size was valued at US$ 431 million in 2024 and is projected to reach US$ 1.3 billion by 2032, at a CAGR of 14.6% during the forecast period 2025-2032.

Which key companies operate in Global TGV Packaging Solution Market?

-> Key players include Corning, LPKF, Samtec, Kiso Micro Co.LTD, Tecnisco, Microplex, Plan Optik, NSG Group, Allvia, AGC, SCHOTT, and Vitrion.

What are the key growth drivers?

-> Key growth drivers include rising demand for advanced packaging in semiconductor industry, miniaturization of electronic devices, and increasing adoption in 5G and automotive applications.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (48.2% in 2024), with significant growth expected in North America and Europe.

What are the emerging trends?

-> Emerging trends include development of wafer-level packaging solutions, integration with fan-out technologies, and increasing use in RF and MEMS applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...