MARKET INSIGHTS

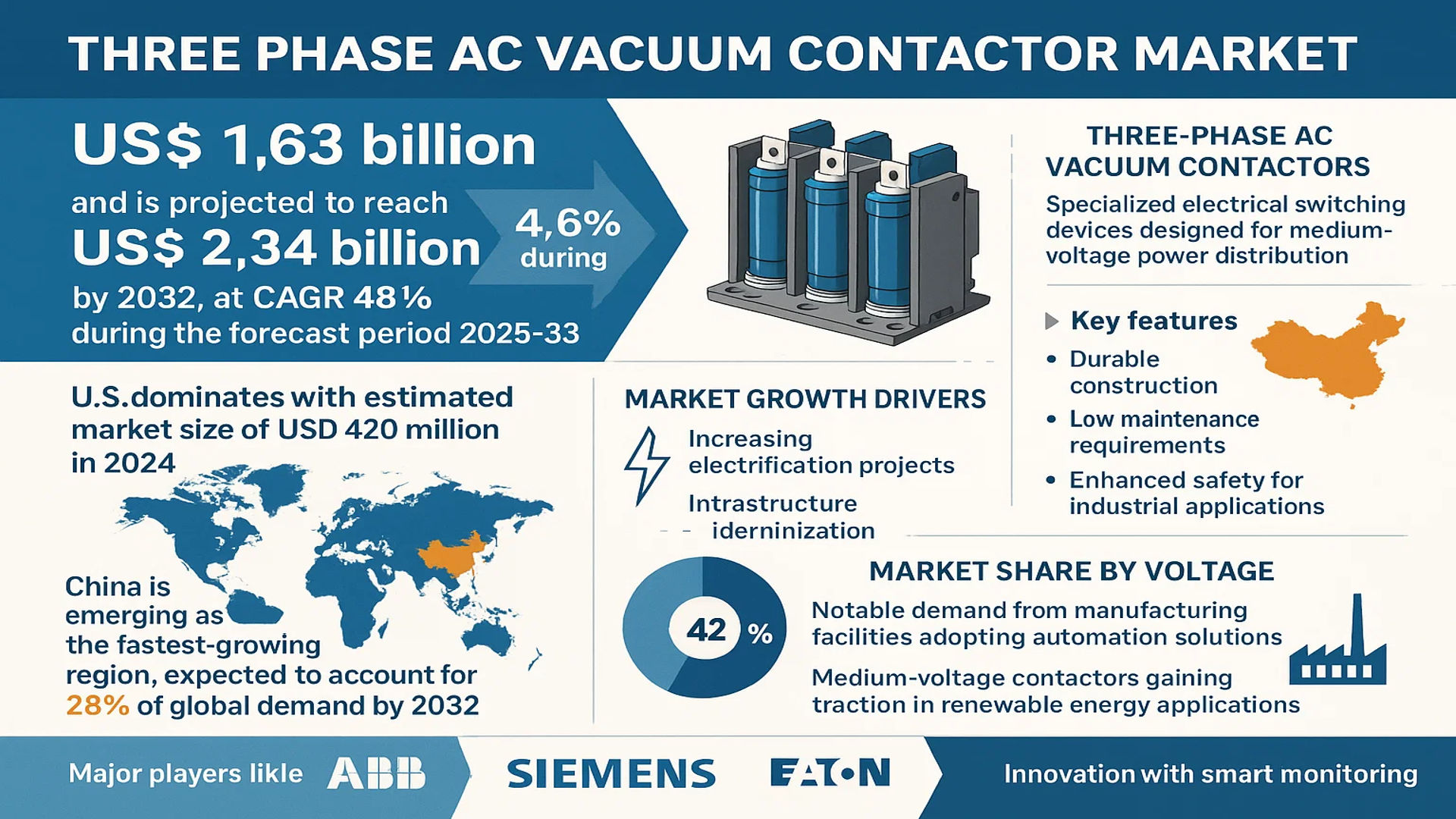

The global Three Phase AC Vacuum Contactor Market size was valued at US$ 1.63 billion in 2024 and is projected to reach US$ 2.34 billion by 2032, at a CAGR of 4.6% during the forecast period 2025-2032. While the U.S. dominates with an estimated market size of USD 420 million in 2024, China is emerging as the fastest-growing region, expected to account for 28% of global demand by 2032.

Three-phase AC vacuum contactors are specialized electrical switching devices designed for medium-voltage power distribution systems. These components utilize vacuum interrupters to control the flow of electricity, offering superior arc-quenching capabilities compared to traditional air-break contactors. Key features include durable construction, low maintenance requirements, and enhanced safety for industrial applications.

Market growth is primarily driven by increasing electrification projects and infrastructure modernization across utilities and industrial sectors. The low-voltage segment currently holds 42% market share, with notable demand from manufacturing facilities adopting automation solutions. However, medium-voltage contactors are gaining traction in renewable energy applications, particularly for solar farm switchgear configurations. Major players like ABB, Siemens, and Eaton continue to innovate with smart monitoring capabilities, addressing the industry’s shift toward predictive maintenance solutions.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Industrialization and Infrastructure Development Fueling Market Expansion

The global surge in industrialization across developing economies is creating substantial demand for three-phase AC vacuum contactors. These devices play a critical role in power distribution systems across manufacturing plants, processing facilities and commercial buildings. With emerging markets investing heavily in infrastructure, the need for reliable electrical switching solutions has grown exponentially. Major projects in power generation, transportation networks and smart city development all require robust electrical control systems where vacuum contactors provide superior performance compared to conventional alternatives.

Growing Renewable Energy Sector Accelerating Adoption

The transition toward sustainable energy solutions has become a significant driver for the three-phase AC vacuum contactor market. As wind and solar power installations expand globally, these technologies require specialized switching equipment capable of handling variable loads and frequent operations. Vacuum contactors offer distinct advantages in renewable energy applications due to their ability to withstand high electrical stresses and harsh environmental conditions. The increasing grid integration of distributed renewable generation has further amplified the need for reliable switching devices that can facilitate smooth power transfer and system protection.

Furthermore, government initiatives and policy frameworks promoting renewable energy adoption continue to support market growth.

➤ For instance, investments in renewable energy infrastructure exceeded $500 billion globally in recent years, with solar and wind projects accounting for the majority share of new power generation capacity additions.

The combination of environmental regulations favoring clean energy and technological advancements in power electronics is creating a favorable landscape for vacuum contactor adoption across utility-scale renewable projects.

MARKET RESTRAINTS

High Initial Costs and Maintenance Requirements Limiting Market Penetration

While three-phase AC vacuum contactors offer superior performance characteristics, their higher upfront costs compared to conventional contactors present a significant barrier to widespread adoption, particularly in price-sensitive markets. The sophisticated manufacturing processes and specialized materials required for vacuum interrupter technology contribute to elevated product costs. Additionally, the need for trained personnel to install, maintain and service these systems adds to the total cost of ownership, making some end-users hesitant to transition from traditional switching solutions.

Other Constraints

Technical Complexities

The advanced nature of vacuum contactor technology requires specialized knowledge for proper application and troubleshooting. This creates challenges in regions with limited technical expertise in medium-voltage electrical systems, potentially slowing adoption rates.

Supply Chain Disruptions

Recent global supply chain challenges have impacted the availability of key components used in vacuum contactor manufacturing, leading to extended lead times and procurement difficulties that restrain market growth.

MARKET CHALLENGES

Stringent Safety and Performance Standards Increasing Compliance Burden

The three-phase AC vacuum contactor market faces significant challenges from evolving industry standards and regulatory requirements. Electrical equipment manufacturers must continually adapt their designs to meet increasingly rigorous safety, performance and environmental specifications across different regional markets. These compliance demands require substantial investment in product testing, certification processes and documentation, which can delay time-to-market for new solutions.

Additionally, the need to retrofit existing systems to meet updated standards presents both technical and financial challenges for end-users, potentially slowing replacement cycles and upgrade decisions.

Other Challenges

Rapid Technological Evolution

The pace of innovation in power electronics and switching technologies creates pressure on manufacturers to continuously improve product offerings while maintaining backward compatibility with legacy systems.

Competition from Alternative Technologies

Emerging semiconductor-based switching solutions present competitive challenges, requiring traditional vacuum contactor manufacturers to enhance product performance and value propositions.

MARKET OPPORTUNITIES

Smart Grid Modernization Creating New Growth Potential

The ongoing digital transformation of power distribution networks represents a significant opportunity for the three-phase AC vacuum contactor market. As utilities worldwide invest in smart grid infrastructure, there is growing demand for intelligent switching solutions that can integrate with digital control systems and support advanced grid management functions. Vacuum contactor manufacturers have the opportunity to develop smart-enabled products with embedded sensors, communication capabilities and predictive maintenance features that align with Industry 4.0 requirements.

Furthermore, the expansion of microgrid projects in both developed and developing markets creates additional avenues for market growth.

➤ The microgrid market is projected to grow at a compound annual rate exceeding 10% through the next decade, driven by increasing concerns about grid resilience and energy security.

Strategic partnerships between vacuum contactor manufacturers and energy management system providers can unlock new opportunities in these emerging applications.

THREE PHASE AC VACUUM CONTACTOR MARKET TRENDS

Industrial Automation and Smart Grid Investments Drive Market Growth

The global three-phase AC vacuum contactor market is experiencing robust growth, fueled by increasing industrial automation and investments in smart grid infrastructure. With industries shifting toward Industry 4.0 standards, the demand for efficient power switching solutions has risen significantly. Vacuum contactors, known for their reliability and low maintenance, are becoming essential components in automated manufacturing setups. The market is projected to grow at a CAGR of approximately 5.8% from 2024 to 2032, driven by their adoption in utilities and heavy industries. Furthermore, the expansion of renewable energy projects necessitates advanced switching solutions that can handle fluctuating loads efficiently.

Other Trends

Transition Toward Medium Voltage Applications

The three-phase AC vacuum contactor market is witnessing a shift toward medium voltage applications, particularly in industries such as mining, oil & gas, and utilities. Medium voltage contactors offer superior arc extinguishing capabilities, making them ideal for high-power load management. Recent advancements in vacuum interrupter technology have extended the lifespan of these components, reducing operational costs. In 2024, medium voltage segment accounted for nearly 35% of the total market share, with further growth anticipated due to increasing energy demands in emerging economies.

Rising Demand for Energy-Efficient Solutions

Energy efficiency remains a critical driver behind market expansion, with stringent government regulations pushing industries to adopt sustainable electrical solutions. Three-phase AC vacuum contactors, known for their minimal energy loss and high switching efficiency, are increasingly preferred over traditional air break contactors. Big players such as ABB, Siemens, and Schneider Electric are investing in R&D to enhance performance while reducing carbon footprints. The trend is particularly strong in Europe and North America, where green energy policies accelerate market adoption.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Expansion to Maintain Competitive Edge

The global Three Phase AC Vacuum Contactor market exhibits a moderately consolidated structure with dominant players accounting for approximately 45% market share collectively in 2024. ABB and Siemens emerge as clear frontrunners, leveraging their extensive product portfolios and robust distribution networks across industrial power systems. These companies have maintained leadership positions through continuous advancements in vacuum interrupter technology and smart grid compatibility.

General Electric and Toshiba follow closely, having strengthened their foothold through strategic acquisitions and partnerships in emerging markets. Their growth has been particularly notable in the industrial sector, where reliability and energy efficiency remain critical purchasing factors. While these established players dominate higher voltage segments, mid-sized companies like Rockwell Automation and Schneider Electric are gaining traction in cost-sensitive applications through localized production strategies.

Recent industry trends show manufacturers increasingly investing in IoT-enabled vacuum contactors with predictive maintenance capabilities. Market leaders are also expanding their service offerings, including remote monitoring solutions, which creates additional revenue streams while raising barriers to entry for smaller competitors.

The competitive landscape continues evolving as Chinese manufacturers like Ls Industrial Systems accelerate their global expansion, offering competitively priced alternatives with improving quality standards. However, established players maintain technological advantages in critical application areas such as mining and offshore oil & gas operations, where safety certifications and extreme environment performance remain decisive factors.

List of Key Three Phase AC Vacuum Contactor Companies Profiled

- ABB (Switzerland)

- Siemens (Germany)

- General Electric (U.S.)

- Toshiba (Japan)

- Rockwell Automation (U.S.)

- Schneider Electric (France)

- Crompton Greaves (India)

- Ls Industrial Systems (South Korea)

- Joslyn Clark (U.S.)

- Ampcontrol (Australia)

- WESCO (U.S.)

- Tavrida Electric (Germany)

- NEPEAN Power (Australia)

- Mitsubishi Electric (Japan)

- Eaton (Ireland)

Market competition is intensifying as companies diversify their product lines to cover the full voltage spectrum from 400V to 15kV applications. Recent product launches emphasize modular designs that reduce maintenance downtime and space requirements – features particularly valued in retrofitting aging industrial facilities. Strategic collaborations between component suppliers and end-users are becoming increasingly common, with manufacturers co-developing customized solutions for specialized applications in mining and utilities sectors.

Segment Analysis:

By Type

Low Voltage Vacuum Contactors Lead Due to Widespread Industrial Applications

The market is segmented based on type into:

- Low Voltage Vacuum Contactors

- Subtypes: Below 1 kV, 1-3 kV range

- Medium Voltage Vacuum Contactors

- Subtypes: 3-7 kV, 7-15 kV ranges

- High Voltage Vacuum Contactors

- Subtypes: Above 15 kV range

By Application

Industrial Applications Dominate Owing to High Electricity Consumption Needs

The market is segmented based on application into:

- Utilities

- Industrial

- Subtypes: Manufacturing plants, Heavy machinery operations

- Oil & Gas

- Mining

- Others

By Voltage Rating

Medium Voltage Segment Shows Significant Growth Potential

The market is segmented based on voltage rating into:

- Low Voltage (Below 1 kV)

- Medium Voltage (1 kV – 38 kV)

- High Voltage (Above 38 kV)

By Operation Mechanism

Electromagnetic Contactors Remain Most Prevalent Design Choice

The market is segmented based on operation mechanism into:

- Electromagnetic

- Pneumatic

- Motorized

- Others

Regional Analysis: Three Phase AC Vacuum Contactor Market

Asia-Pacific

The Asia-Pacific region dominates the global Three Phase AC Vacuum Contactor market, accounting for the largest market share in 2024. This growth is primarily driven by China’s aggressive industrial expansion and India’s burgeoning power infrastructure projects. China’s market is projected to reach $X million by 2032, fueled by substantial investments in smart grid technologies and renewable energy integration. The region’s manufacturing boom, particularly in sectors like automotive and electronics, creates sustained demand for reliable power control solutions. However, the market faces challenges from local manufacturers offering lower-cost alternatives, putting pressure on multinational players to adapt their pricing strategies while maintaining quality standards.

North America

North America represents a technologically advanced market for Three Phase AC Vacuum Contactors, characterized by stringent UL and IEEE standards for electrical equipment. The U.S. market, valued at $X million in 2024, benefits from ongoing grid modernization initiatives and the replacement of aging electromechanical contactors in industrial facilities. Major players like Eaton and GE operate extensive manufacturing bases in the region, supporting just-in-time delivery for industrial customers. The growing adoption of Industry 4.0 technologies is driving demand for smart contactors with IoT capabilities, particularly in the oil & gas and utilities sectors where predictive maintenance is becoming critical.

Europe

Europe maintains a robust market for premium Three Phase AC Vacuum Contactors, with Germany and France leading in adoption. The region’s focus on energy efficiency under the EU Ecodesign Directive has accelerated the replacement of older switching technologies. Siemens and ABB dominate the competitive landscape, offering integrated solutions that combine contactors with protection relays and smart monitoring systems. Renewable energy projects across Northern Europe, particularly offshore wind farms, are creating specialized requirements for corrosion-resistant vacuum contactors. However, market growth faces headwinds from economic uncertainties and the gradual nature of industrial automation upgrades in SMEs.

South America

South America presents a developing market where economic volatility significantly impacts Three Phase AC Vacuum Contactor adoption. Brazil represents the largest submarket, with demand concentrated in mining and hydropower applications. The lack of local manufacturing results in dependence on imports, making the market sensitive to currency fluctuations. While industrial sectors show intermittent growth, the absence of widespread grid modernization programs limits market expansion. Some niche opportunities exist in the region’s growing data center sector, which requires reliable power distribution solutions. Manufacturers face challenges in balancing affordability with the need for products that can withstand challenging operating environments.

Middle East & Africa

The MEA region exhibits polarized demand for Three Phase AC Vacuum Contactors, with GCC countries driving premium product adoption while other markets remain price-sensitive. Saudi Arabia’s Vision 2030 projects and UAE’s industrial diversification are creating sustained demand for medium-voltage contactors in oil refineries and desalination plants. Africa’s mining sector presents growth potential, though infrastructural limitations and inconsistent power quality pose operational challenges. The region’s harsh climatic conditions necessitate specialized product variants with enhanced thermal and dust protection. Market development is constrained by limited technical expertise in some areas, requiring manufacturers to invest in localized training and support services.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Three Phase AC Vacuum Contactor markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Three Phase AC Vacuum Contactor market is projected to grow from US$ 1.63 billion in 2024 to US$ 2.34 billion by 2032, at a CAGR of 4.6 %.

- Segmentation Analysis: Detailed breakdown by product type (Low Voltage, Medium Voltage, High Voltage), application (Utilities, Industrial, Oil & Gas, Mining), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. market is estimated at USD million in 2024 while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading players including General Electric, Siemens, ABB, Toshiba, and Schneider Electric, covering their market share (top five players held approximately % in 2024), product portfolios, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging technologies in vacuum contactor design, smart grid integration, and energy efficiency improvements.

- Market Drivers & Restraints: Evaluation of factors including industrial automation growth, power infrastructure investments, along with supply chain challenges and regulatory constraints.

- Stakeholder Analysis: Strategic insights for manufacturers, suppliers, power utilities, industrial end-users, and investors regarding market opportunities and challenges.

The research methodology combines primary interviews with industry experts and analysis of verified market data from authoritative sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Three Phase AC Vacuum Contactor Market?

-> Three Phase AC Vacuum Contactor Market size was valued at US$ 1.63 billion in 2024 and is projected to reach US$ 2.34 billion by 2032, at a CAGR of 4.6% during the forecast period 2025-2032.

Which key companies operate in Global Three Phase AC Vacuum Contactor Market?

-> Key players include General Electric, Siemens, ABB, Toshiba, Schneider Electric, Eaton, and Mitsubishi Electric, among others.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, power infrastructure modernization, and demand for reliable switching solutions.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, driven by industrialization in China and India, while North America maintains significant market share.

What are the emerging trends?

-> Emerging trends include smart grid integration, development of eco-friendly vacuum contactors, and increasing adoption in renewable energy systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...