MARKET INSIGHTS

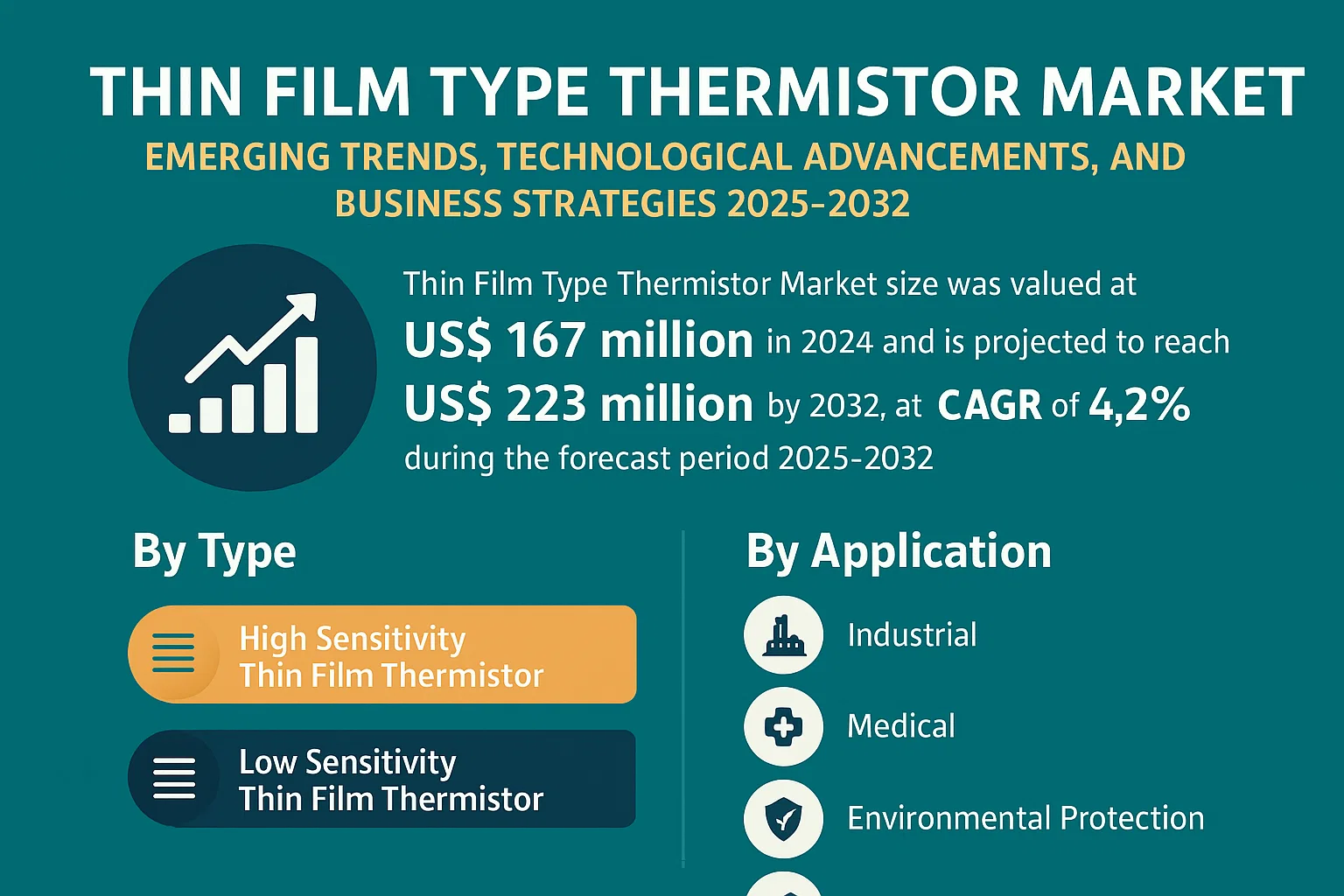

The global Thin Film Type Thermistor Market size was valued at US$ 167 million in 2024 and is projected to reach US$ 223 million by 2032, at a CAGR of 4.2% during the forecast period 2025-2032. The U.S. market accounted for approximately 25% of global revenue in 2024, while China’s market is expected to grow at a faster CAGR of 6.8% through 2032.

Thin film type thermistors are precision temperature sensors that utilize thin film deposition technology to create highly stable resistive temperature detectors. These components offer superior accuracy (±0.1°C), fast response times, and excellent stability compared to conventional thermistors. The technology enables applications requiring miniature sensors with high reproducibility in medical devices, automotive systems, and industrial equipment.

Market growth is driven by increasing demand from the medical sector for diagnostic equipment and wearable health monitors, where accuracy is critical. The industrial segment also contributes significantly due to automation trends and Industry 4.0 implementations. However, pricing pressures from conventional thermistor alternatives may restrain market expansion. Leading manufacturers including Shenzhen Minchuang Electronics and Semitec Corporation are investing in advanced thin film technologies to maintain competitive advantages.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Applications in Automotive Electronics to Fuel Market Growth

The automotive industry’s rapid electrification and increasing adoption of advanced driver-assistance systems (ADAS) are creating substantial demand for thin film thermistors. These components play a critical role in temperature monitoring and thermal management of lithium-ion batteries, electric motors, and power electronics in electric vehicles. With global EV sales projected to exceed 25 million units annually by 2030, sensor requirements are growing exponentially. Thin film thermistors offer advantages such as fast response times (typically under 1 second), high accuracy (±0.1°C), and miniaturization capabilities that make them ideal for space-constrained automotive applications.

Medical Device Miniaturization Trends to Accelerate Adoption

The healthcare sector’s shift toward portable and wearable medical devices represents a significant growth driver for thin film thermistor technology. Modern medical applications require sensors that combine microscopic form factors with clinical-grade precision. Thin film thermistors are increasingly specified for applications including continuous glucose monitors, smart inhalers, and minimally invasive surgical tools where their ability to be integrated into flexible substrates provides design flexibility. The global wearable medical device market is experiencing 25% annual growth, creating robust demand for temperature sensing solutions that can withstand sterilization processes while maintaining measurement stability.

Furthermore, regulatory approvals for novel medical applications are expanding market opportunities.

➤ For recent example, FDA clearance of continuous core temperature monitoring patches has created immediate demand for thin film thermistor arrays capable of 0.01°C resolution.

The convergence of these factors – alongside advancements in semiconductor fabrication techniques – is positioning thin film thermistors as critical components across multiple high-growth industries.

MARKET RESTRAINTS

Material Cost Volatility to Constrain Margin Expansion

While demand grows, manufacturers face persistent challenges from raw material price fluctuations in the thin film thermistor supply chain. The primary materials – including platinum, nickel oxide, and specialized ceramic substrates – have experienced 15-20% annual price volatility in recent years due to geopolitical factors and supply chain disruptions. This creates pricing pressure in cost-sensitive applications like consumer electronics where thin film solutions compete against bulkier but cheaper thermistor alternatives. The situation is particularly acute for medical-grade components requiring ultra-pure materials meeting ISO 13485 standards.

Other Restraints

Technological Limitations in Extreme Environments

Current thin film architectures demonstrate reduced reliability when operated continuously above 300°C or in highly corrosive chemical environments. This restricts their use in industrial process monitoring and aerospace applications where thick film or wire-wound alternatives remain dominant despite their larger footprints.

Design Complexity in Multi-Sensor Integration

Developing hybrid sensor packages combining temperature, humidity, and pressure sensing functions requires advanced thin film deposition techniques that increase development costs and time-to-market. Many mid-sized manufacturers lack the cleanroom capabilities needed for such complex integrations.

MARKET CHALLENGES

Standardization Gaps to Hinder Cross-Industry Adoption

The absence of unified performance standards across different thin film thermistor applications creates interoperability challenges and slows market penetration. While automotive applications follow AEC-Q200 qualifications and medical devices require ISO 60601 compliance, industrial applications lack equivalent universal standards. This fragmentation forces manufacturers to maintain multiple product variants with different testing protocols, increasing inventory costs and limiting economies of scale.

Additional challenges emerge from the rapid pace of technological change in end-use industries. Sensor specifications valid today may become obsolete within 18-24 months as product designs evolve, requiring continuous R&D investments from thermistor suppliers to remain competitive. The talent shortage in advanced materials science further exacerbates these development challenges, with specialized thin film engineers commanding premium compensation in tight labor markets.

MARKET OPPORTUNITIES

Emerging IoT and Smart Infrastructure Applications to Open New Revenue Streams

The global expansion of IoT networks and smart city initiatives presents transformative opportunities for thin film thermistor manufacturers. Modern building automation systems require thousands of discreet, low-power temperature sensors for HVAC optimization and equipment monitoring. Thin film variants excel in these applications due to their microwatt-level power consumption and ability to be printed directly onto flexible substrates during mass production. Early deployments in Asian smart city projects demonstrate 40% longer service life compared to conventional sensors in outdoor environmental monitoring stations.

Advanced Packaging Innovations to Enable Next-Generation Electronics

Semiconductor industry trends toward 3D chip stacking and heterogenous integration create pressing needs for embedded temperature sensing solutions. Thin film thermistors manufactured using semiconductor-compatible processes can be integrated directly into advanced packages for real-time thermal management of high-performance computing chips. Leading foundries are actively partnering with sensor specialists to develop these solutions, with prototype evaluations showing 30% faster thermal response than discrete alternatives in AI accelerator modules.

The convergence of these technological and market trends suggests strong long-term growth potential for thin film thermistor providers who can navigate current challenges while capitalizing on emerging applications across industries.

THIN FILM TYPE THERMISTOR MARKET TRENDS

Miniaturization and IoT Integration Driving Market Expansion

The global thin film type thermistor market is experiencing significant growth, propelled by the increasing demand for miniaturized temperature sensors in IoT-enabled devices. These components are becoming essential in applications requiring high precision, such as automotive electronics, medical devices, and consumer wearables. The market, valued at $123.5 million in 2024, is projected to grow at a CAGR of 7.8% over the next six years, with high-sensitivity variants accounting for 62% of segment revenue. Integrated solutions combining thin film thermistors with wireless communication modules are gaining traction, particularly in smart home and industrial automation applications where real-time thermal monitoring is critical.

Other Trends

Automotive Electrification

Automotive manufacturers are increasingly adopting thin film thermistors for battery management systems in electric vehicles, where temperature control is crucial for safety and performance. The transition to electric powertrains has created demand for sensors capable of operating in extreme conditions (-40°C to 150°C) with rapid response times under 0.5 seconds. This segment represents the fastest-growing application area, with annual growth rates exceeding 12% in major automotive markets including Germany, China, and the United States.

Medical Technology Advancements

The medical sector is witnessing transformative applications of thin film thermistor technology, particularly in diagnostic equipment and implantable devices. Recent breakthroughs in biocompatible thin film materials have enabled their use in continuous glucose monitors and precision thermal therapy systems. The sector accounted for 28% of total market revenue in 2024, with projections indicating this share will grow to 35% by 2030. These components are proving invaluable in applications requiring micro-level temperature measurements with ±0.1°C accuracy, such as PCR machines and neonatal care incubators.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Regional Expansion Drive Thin Film Thermistor Market Competition

The global thin film type thermistor market exhibits a fragmented competitive landscape, with both established electronics manufacturers and specialized sensor companies vying for market share. While the top five players collectively accounted for approximately 25-30% of the 2024 global market revenue, regional champions maintain strong positions in their domestic markets.

Shenzhen Minchuang Electronics Co., Ltd. leads the Asian market with its cost-competitive manufacturing capabilities and extensive distribution networks. The company’s recent expansion into high-sensitivity thermistor variants has strengthened its position across industrial and medical applications. Meanwhile, JPET INTERNATIONAL LIMITED has gained traction through strategic partnerships with European automotive suppliers, particularly for temperature monitoring systems in electric vehicle batteries.

The market’s technological evolution is being driven by R&D investments from key players like Thinking Electronic and Semitec Corporation, who are developing ultra-thin form factors with improved thermal response times. These innovations are critical as industries demand more precise temperature monitoring solutions with minimal space requirements.

While Chinese manufacturers dominate production volumes, Japanese firms like TOPOS maintain a technology edge in high-end applications. The company’s recent development of medical-grade thin film thermistors with 0.01°C accuracy demonstrates this specialization. Furthermore, mergers and acquisitions activity has increased as larger electronics conglomerates seek to vertically integrate thermistor capabilities into broader sensor portfolios.

List of Key Thin Film Type Thermistor Manufacturers

- Shenzhen Minchuang Electronics Co., Ltd. (China)

- HateSensor (South Korea)

- JPET INTERNATIONAL LIMITED (China)

- Sinochip Electronics C0., LTD (China)

- KPD (Japan)

- SHIHENG ELECTRONICS (China)

- Dongguan Jingpin Electronic Technology Co., Ltd (China)

- Qawell Technology (China)

- FENGHUA (HK) ELECTRONICS LTD. (China)

- Thinking Electronic (Taiwan)

- Semitec Corporation (Japan)

- TOPOS (Japan)

Segment Analysis:

By Type

High Sensitivity Thin Film Thermistor Segment Leads Due to Growing Demand in Precision Applications

The market is segmented based on type into:

- High Sensitivity Thin Film Thermistor

- Low Sensitivity Thin Film Thermistor

By Application

Industrial Applications Dominate Market Share Owing to Wide Temperature Sensing Requirements

The market is segmented based on application into:

- Industrial

- Subtypes: Automotive, Manufacturing, Energy, and others

- Medical

- Environmental Protection

- Meteorological

- Others

By End User

Electronics Manufacturers Represent Key Consumers Driving Market Growth

The market is segmented based on end user into:

- Electronics Manufacturers

- Automotive OEMs

- Medical Device Companies

- Research Institutions

- Others

Regional Analysis: Thin Film Type Thermistor Market

North America

The North American market for thin film type thermistors is characterized by strong demand from the industrial and medical sectors, where precision temperature sensing is critical. The U.S. accounts for the majority of regional revenue, supported by advanced manufacturing capabilities and strict quality standards. Key applications include automotive electronics, medical devices, and industrial automation, driving demand for high-sensitivity variants. While technological innovation remains a key growth driver, supply chain constraints and raw material price volatility pose challenges for local manufacturers. Leading players are investing in R&D to enhance product durability and thermal response times.

Europe

Europe demonstrates steady demand for thin film thermistors, particularly in Germany and France, where automotive and industrial applications dominate. The region benefits from stringent regulatory frameworks that emphasize energy efficiency and component reliability. The focus on renewable energy systems and electric vehicles has created new opportunities for thin film thermistor suppliers. Challenges include competition from alternative temperature sensing technologies and the high cost of advanced materials. However, European manufacturers maintain an edge through specialization in high-performance thermistors for mission-critical applications like aerospace and medical diagnostics.

Asia-Pacific

As the largest and fastest-growing market, Asia-Pacific is driven by China’s massive electronics manufacturing sector and Japan’s leadership in precision components. The region benefits from cost-effective production capabilities and expanding application areas, including consumer electronics and environmental monitoring systems. While price sensitivity remains a key market characteristic, there is growing demand for high-reliability thermistors in industrial automation and automotive applications. Local players continue to gain market share through competitive pricing and vertical integration, though quality standardization remains inconsistent across emerging markets in Southeast Asia.

South America

The South American market presents a developing opportunity, with Brazil showing the most promising growth potential. Demand stems primarily from industrial temperature control applications, though adoption is constrained by economic instability and limited technical expertise. Local manufacturers face challenges in competing with imported products from Asia, particularly in price-sensitive segments. The medical equipment sector offers a niche growth area, with increasing investments in healthcare infrastructure driving demand for reliable temperature monitoring components. Market growth remains modest but steady, with potential for expansion as industrial automation increases across the region.

Middle East & Africa

This region represents an emerging market with growth concentrated in oil-rich Gulf nations and South Africa. The primary demand comes from industrial applications in the energy sector, particularly for equipment monitoring in harsh environments. While the market remains relatively small, increasing investments in infrastructure and industrial diversification initiatives are creating new opportunities. Challenges include a fragmented supply chain and reliance on imported components. However, the region’s extreme climate conditions create unique demand for durable thin film thermistors capable of withstanding temperature extremes, presenting opportunities for specialized manufacturers.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Thin Film Type Thermistor markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Thin Film Type Thermistor market was valued at USD million in 2024 and is projected to reach USD million by 2032, growing at a CAGR of % during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (High Sensitivity and Low Sensitivity Thin Film Thermistors), application (Industrial, Medical, Environmental Protection, Meteorological, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market is estimated at USD million in 2024, while China is projected to reach USD million by 2032.

- Competitive Landscape: Profiles of leading market participants including Shenzhen Minchuang Electronics Co., Ltd., HateSensor, JPET INTERNATIONAL LIMITED, Sinochip Electronics C0., LTD, and KPD, among others. In 2024, the global top five players held approximately % market share.

- Technology Trends & Innovation: Assessment of emerging technologies, precision manufacturing techniques, and evolving industry standards in thin film thermistor production.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing demand for temperature sensors in electronics, along with challenges including raw material price volatility.

- Stakeholder Analysis: Insights for component manufacturers, OEMs, system integrators, and investors regarding strategic opportunities in the evolving thermistor market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Thin Film Type Thermistor Market?

-> Thin Film Type Thermistor Market size was valued at US$ 167 million in 2024 and is projected to reach US$ 223 million by 2032, at a CAGR of 4.2% during the forecast period 2025-2032.

Which key companies operate in Global Thin Film Type Thermistor Market?

-> Key players include Shenzhen Minchuang Electronics Co., Ltd., HateSensor, JPET INTERNATIONAL LIMITED, Sinochip Electronics C0., LTD, KPD, SHIHENG ELECTRONICS, and Dongguan Jingpin Electronic Technology Co., Ltd, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for precision temperature sensing in electronics, growth in medical devices, and expansion of IoT applications.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by electronics manufacturing in China, Japan, and South Korea, while North America maintains strong demand for high-performance thermistors.

What are the emerging trends?

-> Emerging trends include miniaturization of thermistor components, development of ultra-sensitive thin films, and integration with smart monitoring systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...