MARKET INSIGHTS

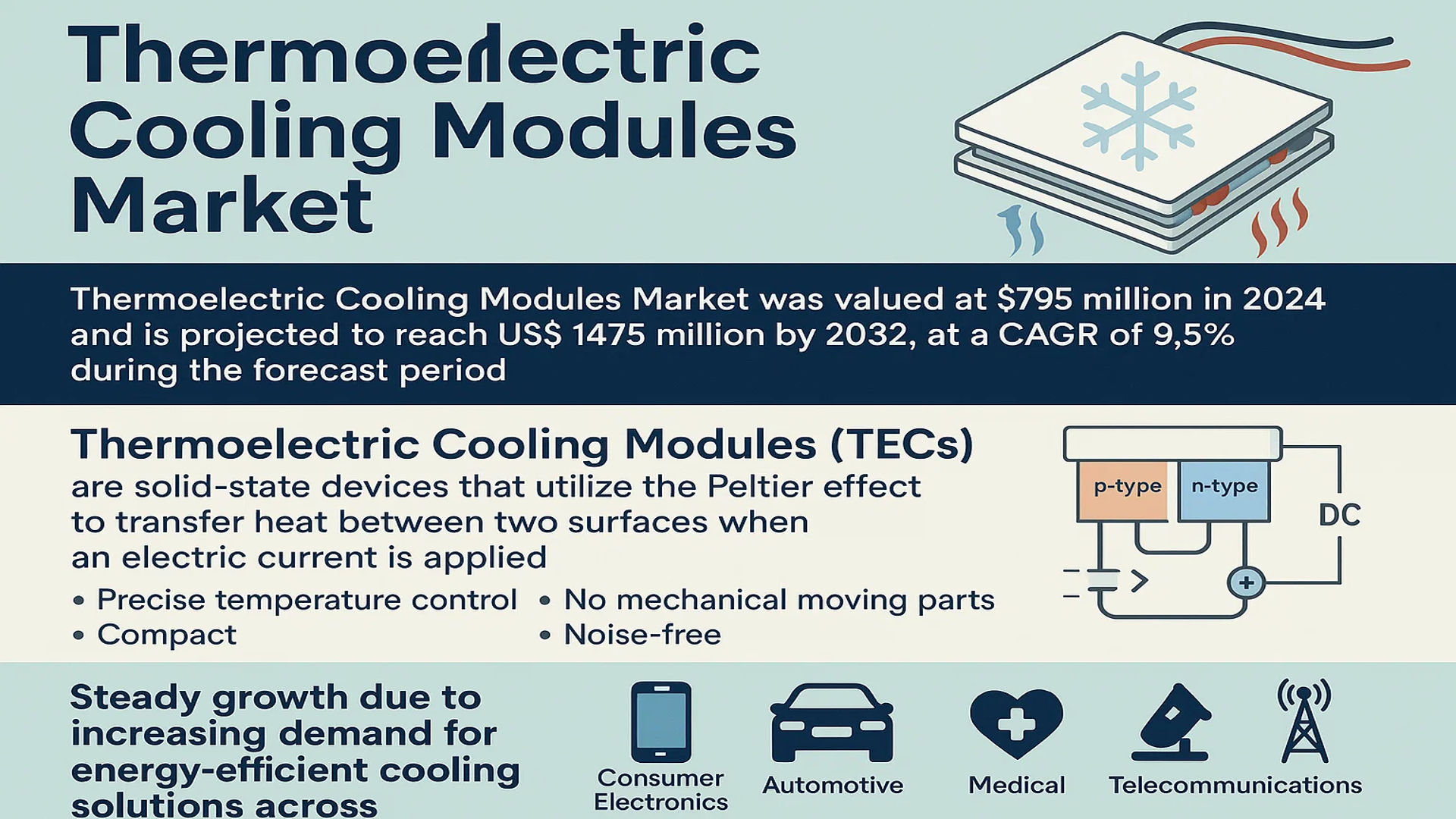

The global Thermoelectric Cooling Modules Market was valued at 795 million in 2024 and is projected to reach US$ 1475 million by 2032, at a CAGR of 9.5% during the forecast period.

Thermoelectric cooling modules (TECs) are solid-state devices that utilize the Peltier effect to transfer heat between two surfaces when an electric current is applied. These modules consist of multiple pairs of p-type and n-type semiconductor materials connected electrically in series and thermally in parallel. When DC current passes through the module, one side absorbs heat (cooling side) while the other releases heat (heating side), enabling precise temperature control without mechanical moving parts. This makes them compact, reliable, and noise-free solutions for thermal management.

The market is experiencing steady growth due to increasing demand for energy-efficient cooling solutions across consumer electronics, automotive, medical, and telecommunications sectors. The rapid adoption of 5G technology and electric vehicles is creating new opportunities, while advancements in semiconductor materials are improving module efficiency. However, challenges remain in competing with traditional cooling methods in high-power applications. Key players like Ferrotec, Laird Thermal Systems, and II-VI Incorporated continue to innovate, with the top five manufacturers holding approximately 55% market share in 2024.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Electronics and Telecommunication Infrastructure Accelerates Adoption

The global thermoelectric cooling modules market is experiencing robust growth due to the rapid expansion of electronics and telecommunications infrastructure. With 5G network deployments increasing by over 35% annually, telecom equipment manufacturers are increasingly adopting thermoelectric coolers for precise temperature management in base stations and data servers. These solid-state devices offer significant advantages for sensitive electronics, including precise thermal control (±0.1°C), quiet operation, and compact form factors. The telecommunications sector accounted for nearly 18% of thermoelectric module shipments in 2024, with projections indicating this share will grow to 25% by 2030 as 5G adoption expands globally.

Medical Technology Advancements Drive Demand for Precision Cooling

Healthcare applications are emerging as a key growth driver for thermoelectric cooling modules, particularly in diagnostic equipment and portable medical devices. The medical sector’s demand for these modules grew by 12% year-over-year in 2024, reflecting their critical role in maintaining optimal operating temperatures for sensitive equipment. PCR machines, portable oxygen concentrators, and infrared cameras for fever detection all rely on thermoelectric cooling for reliable, maintenance-free operation. Furthermore, the shift toward point-of-care testing and decentralized healthcare models is creating new opportunities for compact, energy-efficient cooling solutions in medical applications.

Government investments in healthcare infrastructure are further amplifying this trend, with multiple countries allocating substantial budgets for medical equipment modernization. Regulatory approvals for novel medical applications of thermoelectric technology continue to expand the addressable market.

MARKET CHALLENGES

Efficiency Limitations Constrain Widespread Adoption

Despite their advantages, thermoelectric cooling modules face significant challenges related to energy efficiency and performance limitations. Typical modules achieve coefficients of performance (COP) ranging only between 0.3 and 0.7, substantially lower than compressor-based systems. This efficiency gap becomes particularly problematic in high-heat-load applications, where excessive power consumption makes thermoelectric solutions economically unfeasible. Manufacturers continue to face technical hurdles in improving the thermoelectric figure of merit (ZT) of semiconductor materials, with current commercial materials typically exhibiting ZT values below 1.0.

Other Challenges

Thermal Stress and Reliability Issues

Cyclic thermal stresses in thermoelectric modules can lead to premature failure through interfacial delamination and solder joint degradation. Industry data indicates that thermal cycling reduces module lifespan by approximately 30% for every 50°C increase in operating temperature differentials, creating reliability concerns in demanding applications.

Material Cost Pressures

Bismuth telluride, the dominant material for commercial thermoelectric modules, faces supply chain vulnerabilities and price volatility. Market prices for tellurium, a critical raw material, fluctuated by ±15% in recent years due to limited production capacity and competing demand from solar cell manufacturers.

MARKET RESTRAINTS

High Initial Costs Limit Penetration in Cost-Sensitive Markets

The premium pricing of thermoelectric cooling modules remains a significant barrier to broader market adoption, particularly in price-sensitive consumer applications. While prices have declined by approximately 8% annually, multi-stage modules for deep cooling applications still cost 3-5 times more than conventional refrigeration systems with comparable cooling capacity. This cost differential limits market penetration in developing regions and mass-market consumer products. Price sensitivity is particularly acute in the automotive sector, where thermoelectric solutions must compete with well-established vapor-compression technologies that benefit from decades of optimization and economies of scale.

Additionally, the need for specialized power supplies and temperature controllers adds to the total system cost, further constraining adoption in budget-conscious applications. Emerging markets in Asia and Africa show particular resistance to these cost premiums, preferring traditional cooling methods despite their lower precision and reliability.

MARKET OPPORTUNITIES

Electric Vehicle Thermal Management Presents New Growth Frontier

The accelerating transition to electric vehicles creates substantial opportunities for thermoelectric cooling modules in battery thermal management systems (BTMS). Automotive manufacturers are increasingly evaluating thermoelectric solutions for their precise temperature control capabilities, with the EV thermal management market projected to grow at 22% CAGR through 2030. Notable developments include progress in reversible thermoelectric systems that can switch between cooling and heating modes, ideal for maintaining optimal battery temperatures in varying climates. Several major automakers have announced pilot programs integrating thermoelectric modules for localized battery cooling, with commercial deployments expected by 2026.

Beyond battery systems, opportunities are emerging in cabin climate control and electronics cooling. The ability of thermoelectric modules to provide zone-specific temperature regulation aligns well with EV manufacturers’ goals for energy-efficient passenger comfort systems. Industry collaborations between thermoelectric suppliers and automotive OEMs have increased by 40% since 2022, signaling strong future growth potential.

Advancements in materials science, particularly in skutterudites and half-Heusler compounds, promise to unlock new applications by improving energy efficiency and temperature ranges. Government funding for thermoelectric research has increased significantly, with several national energy agencies prioritizing next-generation thermal management technologies.

THERMOELECTRIC COOLING MODULES MARKET TRENDS

Advancements in Miniaturization and Energy Efficiency Driving Market Growth

The global Thermoelectric Cooling Modules (TEC) market is experiencing significant growth, driven by the increasing demand for compact, energy-efficient cooling solutions across multiple industries. While TECs have been traditionally used in niche applications, recent advancements in semiconductor materials, such as bismuth telluride-based alloys, have improved their coefficient of performance (COP) by approximately 15-20% compared to earlier generations. These improvements, coupled with the trend toward miniaturization in electronics, have expanded their use in applications like microprocessors, laser diodes, and medical diagnostic equipment. Furthermore, solid-state cooling eliminates the need for refrigerants, aligning with global sustainability initiatives.

Other Trends

Rising Adoption in Electric Vehicle Battery Thermal Management

The rapid growth of electric vehicles (EVs) has created a surge in demand for precise thermal management solutions to optimize battery performance and lifespan. TECs are increasingly being integrated into battery cooling systems due to their ability to provide localized cooling without moving parts. Leading automotive manufacturers are exploring hybrid cooling systems that combine thermoelectric modules with traditional liquid cooling to enhance efficiency. This trend is expected to accelerate, particularly as fast-charging technologies place higher thermal demands on EV batteries.

Expansion in Medical and Telecommunications Applications

The medical and telecommunications sectors are emerging as key growth areas for TECs, driven by their need for precise and reliable temperature control. In medical applications, TECs are widely used in portable diagnostic devices, PCR machines, and imaging equipment where noise and vibration must be minimized. Meanwhile, the rollout of 5G infrastructure has increased demand for TECs in base stations and optical transceivers, where maintaining stable temperatures enhances signal integrity. The global increase in healthcare expenditure and telecommunications infrastructure development is expected to sustain this demand, particularly in emerging economies.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Drive Market Competition

The global thermoelectric cooling modules (TEC) market exhibits a semi-consolidated competitive landscape, characterized by dominant players with strong R&D capabilities alongside regional specialists focusing on niche applications. Ferrotec Corporation leads the market with an estimated 20% revenue share in 2024, leveraging its vertically integrated manufacturing and extensive patent portfolio spanning semiconductor materials to finished modules. The company’s growth is further propelled by strategic acquisitions, including its recent expansion into electric vehicle thermal management systems.

KELK Ltd. (Komatsu Group) and Laird Thermal Systems maintain significant market positions through specialization in high-performance industrial and medical cooling solutions. KELK’s proprietary thin-film thermoelectric technology demonstrates 15-20% higher efficiency in laboratory testing compared to conventional bulk materials, while Laird’s cross-industry application expertise spans telecommunications infrastructure to aerospace thermal regulation.

Mid-tier competitors such as Phononic and TE Technology are gaining traction through disruptive innovations in miniature cooling systems, particularly for optoelectronics and medical devices. The emergence of Chinese manufacturers including Guangdong Fuxin Technology and Zhejiang Wangu Semiconductor is reshaping cost structures, though their market presence remains concentrated in consumer electronics applications rather than high-performance segments.

The competitive intensity is expected to escalate as market leaders accelerate next-generation material development and manufacturing automation investments. Ferrotec’s recent $45 million facility expansion in Japan for automotive-grade TEC production exemplifies this trend, while smaller players are forming strategic alliances with end-users to co-develop customized solutions.

List of Key Thermoelectric Cooling Modules Manufacturers

- Ferrotec Corporation (Japan)

- KELK Ltd. (Komatsu Group) (Japan)

- Coherent Corp (U.S.)

- Laird Thermal Systems (U.K.)

- Z-MAX Co., Ltd. (Japan)

- Phononic (U.S.)

- Guangdong Fuxin Technology (China)

- KYOCERA Corporation (Japan)

- Thermonamic Electronics (China)

- TE Technology, Inc. (U.S.)

- Same Sky (formerly CUI Devices) (U.S.)

- Kryotherm Industries (Russia)

Thermoelectric Cooling Modules Market: Segment Analysis

By Type

Single-stage Modules Lead the Market Due to Higher Adoption in Small-Scale Cooling Applications

The market is segmented based on type into:

- Single-stage modules

- Subtypes: Standard single-stage, Micro single-stage

- Multi-stage modules

- Subtypes: Two-stage, Three-stage, and others

- Others

By Application

Consumer Electronics Segment Dominates Owing to Widespread Use in Smartphones and Wearables

The market is segmented based on application into:

- Consumer electronics

- Communication equipment

- Medical devices

- Automotive systems

- Industrial equipment

- Others

By Cooling Capacity

Low Capacity Modules are Most Popular for Portable Applications

The market is segmented based on cooling capacity into:

- Low capacity (below 50W)

- Medium capacity (50W-200W)

- High capacity (above 200W)

By Functionality

Cryogenic Cooling Functionality Gains Traction in Specialized Applications

The market is segmented based on functionality into:

- Conventional cooling

- Precision temperature control

- Cryogenic cooling

- Others

Regional Analysis: Thermoelectric Cooling Modules Market

Asia-Pacific

Asia-Pacific dominates the global thermoelectric cooling modules market, with China, Japan, and South Korea leading in both production and consumption. The region accounted for over 50% of the global market share in 2024, valued at nearly $500 million, driven by rapid industrialization and booming electronics manufacturing. China remains the largest consumer, owing to its expansive electronics sector and emerging electric vehicle industry. Meanwhile, Japan and South Korea contribute significantly due to their advanced semiconductor and telecommunications sectors. The widespread adoption of 5G infrastructure is accelerating demand for efficient thermal management solutions. However, the competitive pricing pressure from local manufacturers creates a challenging landscape for international players.

North America

The North American market is characterized by high demand from the medical, defense, and communication sectors, where precise temperature control is critical. The U.S. is the largest contributor, leveraging its strong presence of key players like Ferrotec and Laird Thermal Systems. Government initiatives, such as investments in semiconductor manufacturing under the CHIPS and Science Act, are expected to further stimulate growth. The trend toward energy-efficient cooling solutions in data centers and electric vehicles also bolsters the market. However, stringent regulatory requirements and high costs of advanced thermoelectric solutions remain barriers for some applications.

Europe

Europe’s market is driven by sustainability-focused policies and advancements in automotive and medical applications. Countries like Germany and France emphasize eco-friendly thermal solutions, aligning with the EU’s strict environmental and energy efficiency regulations. The automotive sector, particularly in electric vehicle battery cooling, presents significant opportunities. Additionally, increasing R&D investments in medical refrigeration and telecommunications contribute to steady demand. European manufacturers such as Kryotherm Industries and TE Technology are key innovators, focusing on high-efficiency, low-power-consumption modules.

South America

The South American market is still in its growth phase, with Brazil and Argentina as the primary contributors. While adoption is slower compared to other regions due to economic instability and limited industrial investments, there is growing potential in consumer electronics and niche medical applications. Local manufacturing remains underdeveloped, with reliance on imports from Asia and the U.S. Nevertheless, infrastructure modernization efforts and a gradual shift toward industrial automation could drive future demand.

Middle East & Africa

The MEA market is nascent but evolving, with increasing applications in telecom infrastructure and refrigeration across Saudi Arabia, UAE, and Turkey). Investments in smart cities and data centers present opportunities for thermoelectric cooling adoption, particularly due to the region’s harsh climatic conditions. However, market expansion is hindered by high costs and lack of local expertise in advanced thermal management solutions. The dominance of conventional cooling technologies further slows adoption, though long-term prospects remain promising with increasing technological awareness.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Thermoelectric Cooling Modules markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Thermoelectric Cooling Modules market was valued at USD 795 million in 2024 and is projected to reach USD 1475 million by 2032, at a CAGR of 9.5%.

- Segmentation Analysis: Detailed breakdown by product type (single-stage, multi-stage), technology, application (consumer electronics, communication, medical, automotive, industrial, aerospace & defense), and end-user industry.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates with 50% market share (USD 500 million in 2024), led by China.

- Competitive Landscape: Profiles of 25+ leading participants including Ferrotec (20% market share), KELK Ltd., Laird Thermal Systems, and Coherent Corp, covering product portfolios and strategic developments.

- Technology Trends: Assessment of Peltier effect innovations, material science advancements, and integration with 5G/IoT applications driving 10% CAGR in unit shipments.

- Market Drivers & Restraints: Evaluation of factors like 5G adoption and EV growth versus challenges in energy efficiency and material costs.

- Stakeholder Analysis: Strategic insights for semiconductor suppliers, OEMs, and investors in this 250+ million unit annual shipment market.

Primary research includes interviews with 50+ industry experts, while secondary research incorporates verified market data and real-time intelligence from manufacturers and distributors.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Thermoelectric Cooling Modules Market?

-> Thermoelectric Cooling Modules Market was valued at 795 million in 2024 and is projected to reach US$ 1475 million by 2032, at a CAGR of 9.5% during the forecast period.

Which key companies operate in this market?

-> Top players include Ferrotec, KELK Ltd., Laird Thermal Systems, Coherent Corp, and Guangdong Fuxin Technology, with the top 5 holding 55% market share.

What are the key growth drivers?

-> Growth is driven by 5G infrastructure, electric vehicle adoption, medical device demand, and miniaturization in consumer electronics.

Which region dominates the market?

-> Asia-Pacific leads with 50% market share (USD 500 million), while North America shows strong growth in medical and aerospace applications.

What are the emerging trends?

-> Emerging trends include high-efficiency semiconductor materials, AI-optimized thermal management, and sustainable manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...