MARKET INSIGHTS

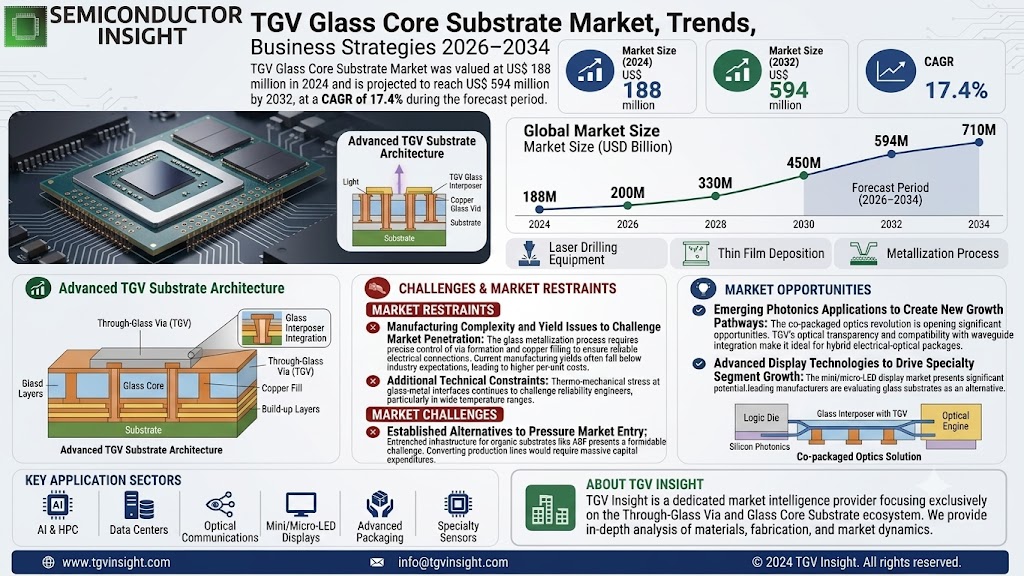

The global TGV Glass Core Substrate Market was valued at 188 million in 2024 and is projected to reach US$ 594 million by 2032, at a CAGR of 17.4% during the forecast period.

TGV (Through Glass Via) Glass Core Substrate is an advanced semiconductor packaging material that uses glass as the core layer, enabling high-density electrical interconnections through precision-drilled vias. This technology offers superior thermal management, excellent signal integrity, and dimensional stability compared to traditional organic substrates like FC-BGA. Key attributes include a low coefficient of thermal expansion (CTE), high flatness for fine-pitch applications, and panel-level manufacturability advantages.

The market growth is primarily driven by increasing demand for high-frequency applications in 5G infrastructure and data centers, where TGV’s low dielectric loss provides critical performance benefits. Furthermore, the miniaturization trend in consumer electronics and the rise of AI/high-performance computing are accelerating adoption. However, challenges remain in manufacturing yield optimization and cost competitiveness against established TSV technologies. Industry leaders like AGC, Schott, and Corning are investing heavily in process improvements to address these barriers.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Frequency and RF Applications to Propel TGV Glass Core Substrate Adoption

The expansion of 5G networks and high-speed data centers is creating unprecedented demand for TGV glass core substrates. With 5G requiring components that minimize signal loss at higher frequencies, TGV’s superior electrical properties make it an ideal solution. The technology’s low dielectric loss (below 0.004 at 10 GHz) and stable electrical characteristics across wide frequency ranges are enabling next-gen RF applications. Major telecommunications equipment providers are increasingly incorporating TGV substrates for millimeter-wave applications, where signal integrity is paramount.

Miniaturization Trends in Electronics to Accelerate Market Expansion

The relentless push for smaller, more powerful electronic devices is driving innovation in advanced packaging solutions. TGV glass core substrates offer distinct advantages in this space, including ultra-thin profiles (as low as 100μm) and superior dimensional stability. Smartphone manufacturers are particularly drawn to TGV technology for its potential to reduce package heights while improving thermal management—critical factors as mobile devices incorporate more powerful processors and 5G modems. The automotive sector is adopting glass substrates for advanced driver assistance systems (ADAS) due to their durability in harsh operating conditions. This dual demand is expected to sustain market growth through the forecast period.

HPC and AI Infrastructure Needs to Drive Adoption in Data Centers

Artificial intelligence and high-performance computing applications are creating new requirements for advanced packaging technologies. TGV glass core substrates are uniquely positioned to address the thermal management challenges of modern computing architectures while enabling high-density interconnects needed for chiplet-based designs. High-profile AI accelerator manufacturers are exploring glass substrates to support the increasing I/O density requirements of machine learning processors, where signal integrity and power efficiency are critical performance factors. The superior thermal conductivity (1.1 W/mK) compared to organic substrates makes glass particularly attractive for these demanding applications.

MARKET RESTRAINTS

Manufacturing Complexity and Yield Issues to Challenge Market Penetration

While TGV technology offers numerous advantages, production challenges remain a significant barrier to widespread adoption. The glass metallization process requires precise control of via formation and copper filling to ensure reliable electrical connections. Current manufacturing yields for panels with micron-level features often fall below industry expectations, leading to higher per-unit costs. The specialized equipment needed for laser drilling and thin-film deposition also represents a substantial capital investment, creating barriers for smaller semiconductor packaging firms.

Additional Technical Constraints

Thermo-mechanical stress at glass-metal interfaces continues to challenge reliability engineers, particularly in applications with wide temperature excursions. These technical hurdles are slowing qualification timelines and making some potential adopters hesitant to transition from mature organic substrate technologies.

MARKET OPPORTUNITIES

Emerging Photonics Applications to Create New Growth Pathways

The co-packaged optics revolution is opening significant opportunities for TGV glass core substrates. The material’s optical transparency and compatibility with waveguide integration make it ideal for hybrid electrical-optical packages. Major data center operators are actively developing solutions that combine silicon photonics with glass interposers to address the bandwidth limitations of traditional copper interconnects. This convergence of electrical and optical packaging could establish glass substrates as a critical enabler of next-generation data communications.

Advanced Display Technologies to Drive Specialty Segment Growth

The mini/micro-LED display market presents significant potential for TGV glass core substrates. Their dimensional stability and thermal properties make them well-suited for high-brightness display applications requiring precise alignment of thousands of micro-emitters. Leading display manufacturers are evaluating glass substrates as an alternative to conventional PCB solutions, particularly for large-format commercial displays where uniformity and reliability are critical parameters. The ability to integrate driver ICs directly onto glass packages could revolutionize display packaging architectures.

MARKET CHALLENGES

Established Alternatives to Pressure Market Entry

The semiconductor packaging industry’s entrenched infrastructure for organic substrates presents a formidable challenge to TGV adoption. Many existing packaging lines are optimized for epoxy-based materials like ABF (Ajinomoto Build-up Film), representing billions of dollars in depreciated equipment. Converting these production lines would require massive capital expenditures, creating financial inertia against technology transitions.

Process Standardization Challenges

The lack of industry-wide standards for glass substrate manufacturing complicates supply chain development. Unlike silicon wafers that benefit from decades of process optimization, glass packaging technologies currently require custom fabrication approaches. This fragmentation increases costs and limits economies of scale that could make TGV solutions more cost-competitive.

TGV GLASS CORE SUBSTRATE MARKET TRENDS

Advancements in 5G and High-Performance Electronics Driving Demand for TGV Substrates

The rapid expansion of 5G infrastructure and the increasing demand for high-frequency applications have positioned TGV glass core substrates as a critical enabler for next-generation electronics. With signal loss reduction capabilities of up to 50% lower than traditional organic substrates at millimeter-wave frequencies, these substrates are becoming indispensable for RF front-end modules and antenna-in-package solutions. Innovations in panel-level manufacturing have further improved production scalability, with companies like DNP achieving fine via pitches below 30μm while maintaining superior thermal and mechanical stability. The market is responding strongly, evidenced by the 17.4% CAGR projection through 2032.

Other Trends

AI Chip Packaging Revolution

The explosive growth in artificial intelligence processors is creating unprecedented demand for TGV substrates in 2.5D/3D chip packaging. These substrates provide critical advantages for AI accelerators through their ultra-low dielectric constant (Dk below 5.5) and exceptional planarity (<0.5μm warpage over 300mm wafers). Major foundries are adopting TGV interposers to address the thermal management challenges of high-power density AI chips exceeding 500W, where traditional organic substrates often fail due to thermal deformation. The market for TGV in AI applications could capture over 35% of advanced packaging substrate demand by 2027.

Mini/Micro LED Display Manufacturing Shift

Display manufacturers are increasingly adopting TGV glass cores to address the interconnection challenges in ultra-high resolution Mini and Micro LED arrays. The technology enables sub-10μm via processes crucial for fine-pitch LED transfer, while the thermal expansion matching with sapphire growth substrates reduces stress-induced defects during bonding. This has led to adoption in premium display segments, with panel makers reporting 30% improvement in yield rates compared to conventional temporary bonding methods. The automotive display sector particularly favors TGV for its high-temperature reliability (>150°C operation) in dashboard and head-up display applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Glass and Semiconductor Suppliers Invest in TGV to Solidify Market Position

The global TGV (Through Glass Via) Glass Core Substrate market is characterized by a mix of established glass manufacturers and emerging technology specialists striving to capitalize on the growing demand for advanced semiconductor packaging solutions. AGC Inc. and Corning Incorporated currently dominate the market, leveraging their decades of expertise in glass technology and extensive R&D capabilities. These companies have made significant strides in developing TGV substrates with superior thermal and electrical properties.

Schott AG and Dai Nippon Printing (DNP) have emerged as key competitors, particularly in the Asian market where demand for advanced packaging solutions is growing rapidly. DNP’s proprietary Glass Core Substrate (GCS) technology has gained traction for its panel-level manufacturing capabilities, making it a preferred choice for high-volume production.

While established players currently hold the majority of market share, new entrants such as Guangdong 3D Chips and WGTech are making inroads by focusing on niche applications like MEMS sensors and micro-LED displays. These companies benefit from government support and local semiconductor ecosystems in China and South Korea.

The competitive intensity is further heightened by collaborations between glass manufacturers and semiconductor companies. For instance, several key players have formed strategic alliances with foundries and OSATs (Outsourced Semiconductor Assembly and Test) to accelerate TGV adoption in high-performance computing and 5G applications.

List of Key TGV Glass Core Substrate Companies Profiled

- AGC Inc. (Japan)

- Schott AG (Germany)

- Corning Incorporated (U.S.)

- Hoya Corporation (Japan)

- Ohara Corporation (Japan)

- Dai Nippon Printing (DNP) (Japan)

- Nippon Electric Glass (NEG) (Japan)

- CrysTop Glass (China)

- Guangdong 3D Chips (China)

- WGTech (South Korea)

Segment Analysis:

By Type

CTE Below 5 ppm/°C Segment Leads the Market Due to High Demand in High-Frequency Applications

The market is segmented based on coefficient of thermal expansion (CTE) into:

- Coefficient of Thermal Expansion (CTE), above 5 ppm/°C

- Coefficient of Thermal Expansion (CTE), below 5 ppm/°C

By Application

Panel Level Packaging Gains Traction Owing to Manufacturing Scalability and Cost Efficiency

The market is segmented based on application into:

- Wafer Level Packaging

- Panel Level Packaging

By End-Use Industry

Consumer Electronics Emerges as Key Growth Sector Driven by Miniaturization Trends

The market is segmented based on end-use industries into:

- Consumer Electronics

- Telecommunications

- Automotive

- Aerospace & Defense

- Others

By Manufacturing Process

Laser Drilling Technology Dominates for Precision Via Formation in Glass Substrates

The market is segmented based on manufacturing processes into:

- Laser Drilling

- Wet Etching

- Photo Structuring

- Others

Regional Analysis: TGV Glass Core Substrate Market

Asia-Pacific

The Asia-Pacific region leads the global TGV Glass Core Substrate market, accounting for over 48% of global demand in 2024. This dominance stems from China’s semiconductor manufacturing expansion, Japan’s advanced glass technology ecosystem, and South Korea’s thriving consumer electronics sector. The region benefits from strong government support, such as China’s 14th Five-Year Plan semiconductor self-sufficiency goals and Japan’s METI-funded advanced packaging initiatives. Local leaders like AGC and Dai Nippon Printing are pioneering panel-level manufacturing techniques, while Taiwanese foundries are actively testing TGV for 3D IC stacking applications. However, the market faces challenges from conventional substrate loyalties and the high capex requirements for TGV production lines.

North America

North America’s TGV Glass Core Substrate market is primarily driven by HPC and AI chip demand from tech giants and defense applications. The U.S. accounts for 89% of regional demand, with Corning leading material innovation through DARPA-funded projects for radar systems and quantum computing packaging. Recent CHIPS Act allocations include provisions for advanced packaging R&D, indirectly benefiting TGV adoption. Key challenges include competition from established TSV technologies in Intel’s packaging ecosystem and the higher cost sensitivity of commercial aerospace applications compared to defense budgets.

Europe

Europe’s TGV market focuses on automotive MEMS sensors and industrial IoT applications, with Germany and France collectively representing 72% of regional consumption. Schott AG’s HERMES project demonstrates the region’s strength in thin-glass processing for heterogeneous integration. EU Horizon Europe funding supports TGV development for photonics applications, particularly in Sweden’s growing photonics cluster. The market faces slower adoption curves due to conservative automotive supply chains and preference for proven organic substrates in consumer wearables.

Middle East & Africa

This emerging market shows promise through strategic investments in 5G infrastructure and smart city projects. Israel’s tech ecosystem is exploring TGV for military RF applications, while UAE’s semiconductor ambitions include TGV evaluation for harsh-environment electronics. The region currently accounts for less than 3% of global demand but presents long-term growth potential as local fab projects mature. Primary barriers include limited local expertise in advanced packaging and dependence on imported substrate materials.

South America

South America’s TGV market remains in early stages, with Brazil’s CEITEC conducting preliminary research on glass substrates for agricultural sensors. The lack of local semiconductor fabs and minimal government support for advanced packaging restricts market growth. Most demand stems from imported automotive electronics rather than local production. Economic instability further discourages capital-intensive TGV manufacturing investments, though some multinational OEMs are evaluating the technology for mining equipment applications in Chile’s copper industry.

Report Scope

This market research report provides a comprehensive analysis of the global TGV Glass Core Substrate market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global TGV Glass Core Substrate market was valued at USD 188 million in 2024 and is projected to reach USD 594 million by 2032, growing at a CAGR of 17.4%.

- Segmentation Analysis: Detailed breakdown by product type (CTE above/below 5 ppm/°C), technology, application (wafer level packaging, panel level packaging), and end-user industries to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis of key markets.

- Competitive Landscape: Profiles of leading market participants including AGC, Schott, Corning, Dai Nippon Printing (DNP), and others, covering their product portfolios and strategic initiatives.

- Technology Trends: Assessment of emerging technologies in semiconductor packaging, including integration with 5G, AI chips, and advanced computing applications.

- Market Drivers & Restraints: Analysis of factors driving adoption (5G expansion, HPC demand) and challenges (manufacturing complexity, high capital costs) in the TGV substrate market.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, packaging specialists, investors, and policymakers on market opportunities and risks.

The research employs both primary and secondary methodologies, including interviews with industry leaders and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global TGV Glass Core Substrate Market?

-> TGV Glass Core Substrate Market was valued at 188 million in 2024 and is projected to reach US$ 594 million by 2032, at a CAGR of 17.4% during the forecast period.

Which key companies operate in Global TGV Glass Core Substrate Market?

-> Key players include AGC, Schott, Corning, Dai Nippon Printing (DNP), Hoya, Ohara, and NEG, among others.

What are the key growth drivers?

-> Key growth drivers include 5G infrastructure expansion, demand for high-performance computing, and miniaturization trends in electronics packaging.

Which region dominates the market?

-> Asia-Pacific leads in both market share and growth, driven by semiconductor manufacturing hubs in Japan, South Korea, and China.

What are the emerging trends?

-> Emerging trends include adoption in AI chip packaging, integration with CPO technology, and development of ultra-low CTE glass formulations.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...