MARKET INSIGHTS

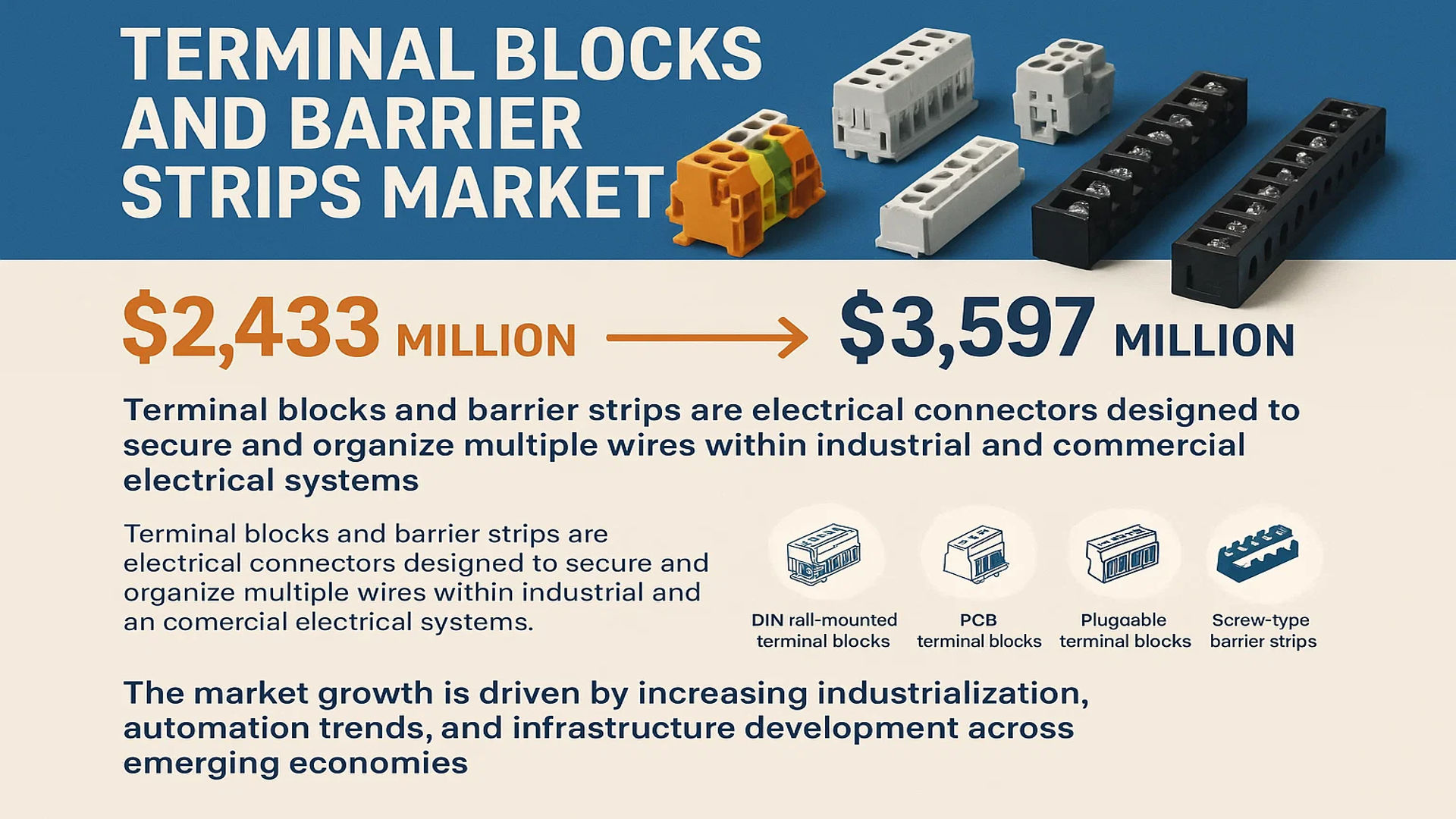

The global Terminal Blocks and Barrier Strips Market was valued at 2433 million in 2024 and is projected to reach US$ 3597 million by 2032, at a CAGR of 6.3% during the forecast period.

Terminal blocks and barrier strips are electrical connectors designed to secure and organize multiple wires within industrial and commercial electrical systems. These components provide safe and reliable connection points for wire termination, distribution, and grounding applications while preventing short circuits and electrical hazards. The product categories include DIN rail-mounted terminal blocks, PCB terminal blocks, pluggable terminal blocks, and screw-type barrier strips, among others.

The market growth is driven by increasing industrialization, automation trends, and infrastructure development across emerging economies. Rising adoption in energy distribution systems and growing demand for modular wiring solutions in manufacturing facilities are key growth drivers. However, the market faces challenges from alternative connection technologies and pricing pressures. Leading manufacturers like Phoenix Contact, WAGO, and Weidmüller are investing in innovative products with higher current ratings and space-saving designs to address evolving industry requirements.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Industrial Automation to Accelerate Market Growth

The global push towards Industry 4.0 and smart manufacturing is creating substantial demand for terminal blocks and barrier strips. These components play a critical role in factory automation systems by ensuring secure electrical connections in control panels, motor drives, and PLCs. With industrial automation investments projected to maintain a growth rate exceeding 8% annually, the need for reliable electrical connectivity solutions is intensifying. Terminal blocks offer vibration-resistant connections crucial for harsh industrial environments, while barrier strips provide organized wiring solutions for complex automation systems.

Growth in Renewable Energy Infrastructure to Bolster Demand

The renewable energy sector’s rapid expansion is driving substantial demand for electrical interconnection solutions. Solar farms and wind turbine installations require thousands of terminal connections in junction boxes, combiner panels, and inverter systems. Barrier strips enable efficient parallel connections in solar array wiring, while terminal blocks are essential for safe power distribution in wind turbine control cabinets. With global renewable capacity additions increasing by over 10% annually, the associated growth in electrical interconnection needs presents a significant market opportunity.

Advancements in High-Density Connectivity Solutions

Manufacturers are innovating compact terminal block designs to meet space constraints in modern electrical enclosures. New spring-cage and push-in connection technologies simplify installation while maintaining reliability. These advancements are particularly valuable in applications like telecom cabinets and data center power distribution, where high-density connections are paramount. Leading suppliers have recently introduced terminal blocks with up to 45% space savings compared to traditional designs while maintaining equivalent current ratings.

MARKET RESTRAINTS

Competition from Wireless and Alternative Connection Technologies

While terminal blocks remain essential for many applications, the emergence of wireless control systems and advanced pluggable connectors presents competitive challenges. Some industrial networks are transitioning to wireless I/O modules, reducing the need for traditional terminal blocks in signal connections. However, power distribution applications continue to require robust terminal solutions, particularly in high-current scenarios where wireless alternatives are impractical.

Raw Material Price Volatility Impacting Manufacturing Costs

The terminal block manufacturing process depends on various metals and polymers subject to global commodity price fluctuations. Copper price variations particularly affect production costs, as it’s a primary conductor material. Some manufacturers are responding by developing alternative alloy formulations, though these must maintain the electrical and mechanical properties required for industrial applications. These material challenges are prompting reevaluation of supply chain strategies across the industry.

MARKET CHALLENGES

Compatibility Issues in Legacy System Upgrades

Industrial facilities often face challenges when integrating new terminal block technologies with existing infrastructure. Retrofitting modern high-density terminal blocks into older enclosures sometimes requires costly panel modifications. Some end-users hesitate to upgrade connection systems due to concerns about disrupting operational continuity, particularly in mission-critical applications like power generation or process control.

Increasing Safety and Certification Requirements

Stricter international safety standards are raising the bar for terminal block performance certifications. Products must now meet evolving requirements for creepage distance, flame resistance, and mechanical durability. While these standards improve system safety, they increase development cycles and testing costs for manufacturers. The complexity multiplies when serving global markets with varying regional certification requirements.

MARKET OPPORTUNITIES

Growth Potential in Emerging Economies

Rapid industrialization in developing nations presents significant opportunities for terminal block suppliers. Infrastructure development across Southeast Asia and Africa requires extensive electrical distribution systems. Local manufacturing growth also drives demand for industrial control components. Market penetration strategies must account for price sensitivity in these regions while maintaining product quality expectations.

Integration of Smart Monitoring Capabilities

The convergence of connectivity and power distribution enables new product innovations. “Smart” terminal blocks with integrated current monitoring and temperature sensing capabilities are emerging. These intelligent solutions help prevent electrical failures through predictive maintenance, appealing to facilities prioritizing operational reliability. The development of these advanced products creates differentiation opportunities in a traditionally standardized product category.

Customized Solutions for Niche Applications

Specialized industries such as marine, military, and extreme environment applications require customized terminal solutions. These segments command premium pricing for products meeting stringent environmental and reliability specifications. Manufacturers investing in application-specific R&D can capture these high-value niches while strengthening their technical capabilities for broader markets.

TERMINAL BLOCKS AND BARRIER STRIPS MARKET TRENDS

Increasing Industrial Automation Drives Demand for High-Performance Terminal Blocks

The rapid expansion of industrial automation across multiple sectors, including manufacturing, energy, and transport, is significantly boosting the demand for terminal blocks and barrier strips. These components are critical for ensuring secure and organized wiring systems in automated equipment, control panels, and machinery. In 2024, the industrial segment accounted for approximately 42% of the global terminal blocks market share. Factors such as Industry 4.0 adoption, smart factory development, and the increasing need for modular and scalable electrical connections are accelerating the market growth. Europe and North America are leading contributors due to their advanced manufacturing infrastructure, while the Asia-Pacific region is witnessing the fastest growth, propelled by expanding industrial bases in China and India.

Other Trends

Miniaturization and Space-Saving Designs

The trend toward miniaturization in electronics and electrical systems is shaping the terminal block market. Compact designs, such as pluggable and high-density terminal blocks, are increasingly preferred in applications where space constraints exist, such as automotive control units, consumer electronics, and renewable energy systems. Manufacturers are innovating to develop lightweight yet durable solutions that maintain high current-carrying capacity while reducing footprint. This shift is particularly evident in the automotive sector, where electric vehicles (EVs) necessitate efficient and space-saving wiring components to accommodate complex battery management systems.

Growing Adoption of Renewable Energy Systems

The global push toward clean energy is another major driver for the terminal blocks and barrier strips market. Renewable energy installations, including solar and wind power systems, require robust and corrosion-resistant electrical connections capable of withstanding harsh environmental conditions. Barrier strips with high ingress protection (IP) ratings are increasingly used in photovoltaic arrays, inverters, and energy storage systems. The renewable energy sector is projected to contribute over 18% to the terminal blocks market revenue by 2032, with the solar energy segment leading demand. Emerging economies in Asia and Latin America are rapidly increasing renewable capacity, creating new opportunities for terminal block suppliers.

Smart Buildings and IoT Integration

The proliferation of smart buildings and IoT (Internet of Things) technologies is revolutionizing the terminal block market. Modern building automation systems rely on intelligent terminal blocks that facilitate data transmission alongside power distribution. Features like push-in connectivity and tool-less installation are gaining traction as they reduce installation time and maintenance costs in commercial and residential buildings. The smart building market is expected to expand at a CAGR of 9.1% from 2024 to 2032, further driving innovation in terminal block designs that support digital communication protocols. North America and Europe remain dominant markets due to stringent energy efficiency regulations and high adoption of smart infrastructure.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Market Leaders Innovate to Address Rising Demand for Reliable Electrical Connectivity

The global terminal blocks and barrier strips market features a combination of established multinational corporations and regional specialists competing across multiple industries. Phoenix Contact leads the market with an extensive product portfolio and strong presence across automation, energy, and infrastructure applications. The company reinforced its position in 2024 through strategic acquisitions in North America and the launch of next-generation spring-cage terminal blocks.

WAGO GmbH & Co. KG and Weidmüller Interface GmbH & Co. KG maintain robust market positions through continuous innovation in modular connection technologies. Both German manufacturers have recently expanded their barrier strip offerings with IP68-rated solutions for harsh environments, catering to growing industrial automation demands.

Meanwhile, several companies are focusing on smart connectivity solutions, recognizing the industry’s shift toward IoT-enabled electrical distribution. TE Connectivity introduced its CONNEXIS™ networked terminal blocks in 2023, while ABB Ltd. integrated sensor technology into its terminal block lineup, demonstrating how traditional components are evolving for Industry 4.0 applications.

American competitors Molex LLC and Eaton Corporation are strengthening their market positions through vertical integration strategies. Both companies have recently enhanced their manufacturing capabilities for high-voltage barrier strips, targeting renewable energy and data center markets where safety certifications are paramount.

List of Key Terminal Blocks and Barrier Strips Manufacturers

- Phoenix Contact (Germany)

- WAGO GmbH & Co. KG (Germany)

- Weidmüller Interface GmbH & Co. KG (Germany)

- TE Connectivity (Switzerland)

- ABB Ltd. (Switzerland)

- Molex LLC (U.S.)

- Omron Corporation (Japan)

- Eaton Corporation (Ireland)

- Schneider Electric (France)

- Altech Corporation (U.S.)

The competitive environment continues evolving with regional players expanding globally, particularly Asian manufacturers investing in R&D to challenge European dominance in high-end terminal block solutions. Recent patent filings indicate intensifying innovation across smart connectivity features and materials science, suggesting the competitive landscape will remain dynamic throughout the forecast period.

Segment Analysis:

By Type

Terminal Blocks Segment Leads Due to High Adoption in Industrial and Commercial Applications

The market is segmented based on type into:

- Terminal Blocks

- Subtypes: Barrier Terminal Blocks, DIN Rail Terminal Blocks, PCB Terminal Blocks, and Others

- Barrier Strips

By Application

Industrial Segment Dominates Owing to Wide Usage in Automation and Control Systems

The market is segmented based on application into:

- Industrial

- Communications

- Healthcare

- Financial

- Others

By Mounting Type

DIN Rail Mounting is Preferred for Its Secure and Organized Wiring Solutions

The market is segmented based on mounting type into:

- DIN Rail Mounting

- Panel Mounting

- PCB Mounting

- Others

By End User

Manufacturing Sector Leads Due to Rising Automation and Electrical Infrastructure Needs

The market is segmented based on end user into:

- Manufacturing

- Telecommunications

- Energy & Power

- Transportation

- Others

Regional Analysis: Terminal Blocks and Barrier Strips Market

Asia-Pacific

The Asia-Pacific region dominates the global terminal blocks and barrier strips market, accounting for the largest revenue share. This growth is primarily driven by rapid industrialization, urbanization, and infrastructure development in countries like China, India, and Japan. The region benefits from strong manufacturing bases in electronics, automotive, and energy sectors – all of which are key consumers of terminal blocks. China’s ‘Made in China 2025’ initiative has particularly boosted demand for high-quality electrical components. However, price sensitivity in emerging markets remains a challenge for premium product adoption.

North America

North America represents a mature yet innovation-driven market for terminal blocks and barrier strips. Strict safety regulations (UL certification standards) and the need for reliable power distribution in industrial automation push demand for advanced connectivity solutions. The U.S. market benefits from strong industrial and commercial construction activities, with growing emphasis on modular and maintenance-friendly designs. Recent infrastructure investments in renewable energy projects are creating new opportunities for specialized terminal block applications in solar and wind power installations.

Europe

Europe maintains a steady market position characterized by technological sophistication and stringent quality requirements. German engineering excellence drives innovation in terminal block design, particularly for industrial automation applications. The region’s focus on energy efficiency and smart manufacturing (Industry 4.0) increases demand for intelligent terminal solutions with diagnostic capabilities. However, market growth faces some constraints from economic stagnation in certain countries and the high penetration of existing installed base equipment.

South America

The South American market shows moderate growth potential, primarily driven by Brazil’s industrial sector and mining activities. While the market remains price-sensitive, increasing electrification projects and efforts to upgrade aging infrastructure create opportunities for terminal block suppliers. Political and economic instability in some countries continues to impact investment decisions, causing uneven growth patterns across the region. Local manufacturers face strong competition from Asian imports in the low-to-mid range product segments.

Middle East & Africa

This emerging market benefits from large-scale infrastructure projects in Gulf Cooperation Council (GCC) countries, particularly in commercial construction and oil/gas applications. The UAE and Saudi Arabia lead in adopting advanced terminal solutions for harsh environment applications. However, markets in Africa develop more slowly due to limited industrialization and unreliable power infrastructure. The region’s growth prospects remain tied to economic diversification plans and foreign investment in energy and construction projects.

Market Leaders’ Insight

Phoenix Contact and Weidmüller continue to dominate the premium segment globally, while Asian manufacturers like CHINT and Dinkle Electronics capture significant market share in cost-sensitive regions. The competitive landscape shows increasing consolidation as major players acquire regional manufacturers to expand their product portfolios and geographic reach.

Report Scope

This market research report provides a comprehensive analysis of the global Terminal Blocks and Barrier Strips market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Terminal Blocks and Barrier Strips market was valued at USD 2,433 million in 2024 and is projected to reach USD 3,597 million by 2032, growing at a CAGR of 6.3%.

- Segmentation Analysis: Detailed breakdown by product type (Terminal Blocks, Barrier Strips), application (Communications, Financial, Industrial, Healthcare, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market due to rapid industrialization, while North America and Europe remain key revenue generators.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Phoenix Contact, WAGO GmbH & Co. KG, Weidmüller Interface GmbH & Co. KG, TE Connectivity, and ABB Ltd.

- Technology Trends & Innovation: Assessment of emerging technologies, including smart terminal blocks with IoT integration, high-current handling capabilities, and fire-resistant materials.

- Market Drivers & Restraints: Evaluation of factors driving market growth, such as industrial automation and renewable energy investments, along with challenges like supply chain disruptions and raw material price volatility.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in the electrical connectivity solutions market.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Terminal Blocks and Barrier Strips Market?

-> Terminal Blocks and Barrier Strips Market was valued at 2433 million in 2024 and is projected to reach US$ 3597 million by 2032, at a CAGR of 6.3% during the forecast period.

Which key companies operate in Global Terminal Blocks and Barrier Strips Market?

-> Key players include Phoenix Contact, WAGO GmbH & Co. KG, Weidmüller Interface GmbH & Co. KG, TE Connectivity, ABB Ltd., Molex LLC, Omron Corporation, Eaton Corporation, Schneider Electric, and Altech Corporation.

What are the key growth drivers?

-> Key growth drivers include industrial automation, renewable energy projects, smart grid deployments, and increasing demand for safe electrical connectivity solutions across various industries.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region due to rapid industrialization, while Europe and North America maintain strong market positions with advanced manufacturing sectors.

What are the emerging trends?

-> Emerging trends include miniaturization of terminal blocks, smart connectivity solutions with integrated diagnostics, and development of eco-friendly materials to meet sustainability requirements.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...