MARKET INSIGHTS

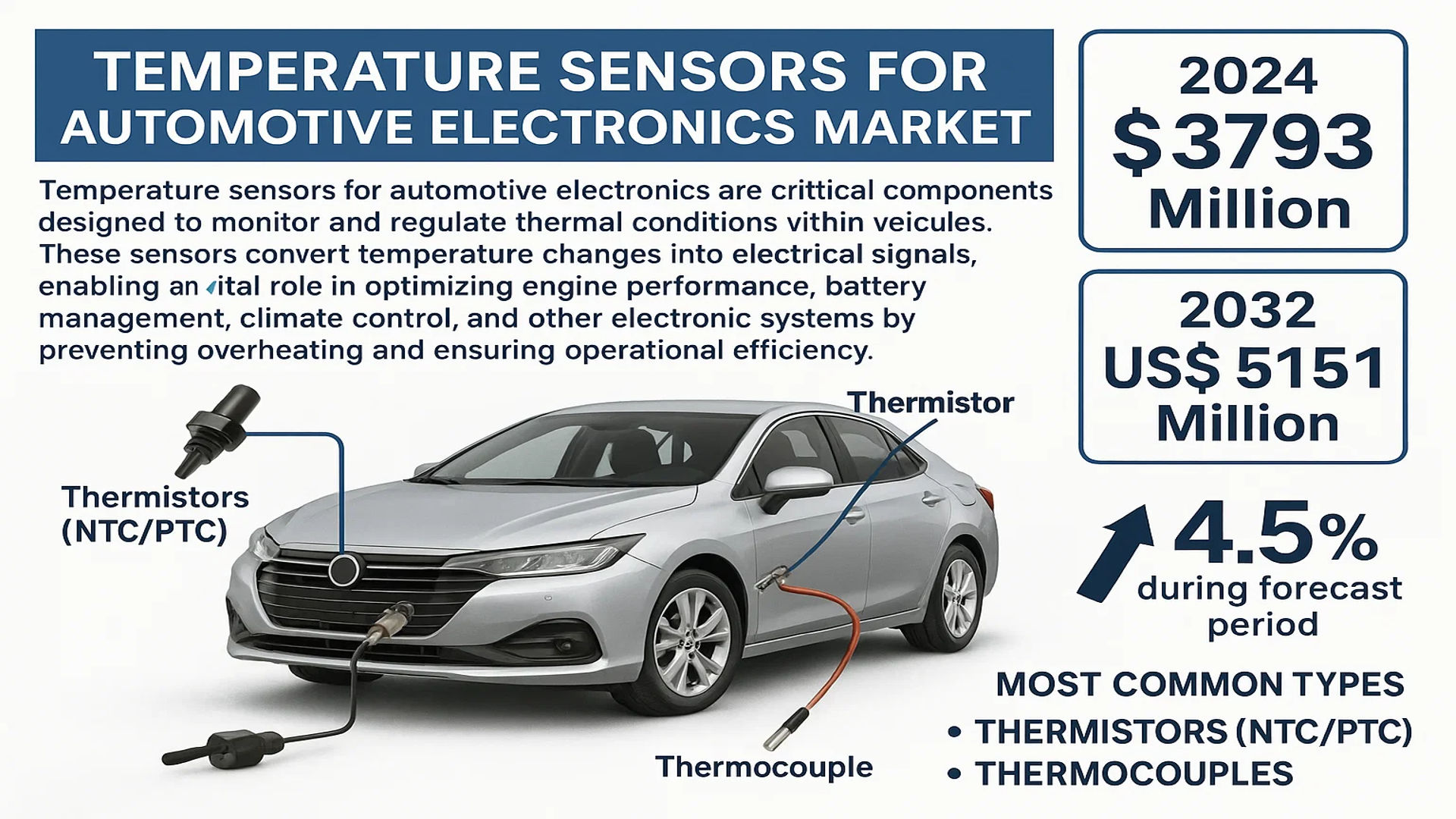

The global Temperature Sensors for Automotive Electronics Market was valued at 3793 million in 2024 and is projected to reach US$ 5151 million by 2032, at a CAGR of 4.5% during the forecast period.

Temperature sensors for automotive electronics are critical components designed to monitor and regulate thermal conditions within vehicles. These sensors convert temperature changes into electrical signals, enabling real-time monitoring by electronic control units (ECUs). They play a vital role in optimizing engine performance, battery management, climate control, and other electronic systems by preventing overheating and ensuring operational efficiency. The most common types include thermistors (NTC/PTC) and thermocouples, each offering distinct advantages for specific automotive applications.

The market growth is driven by increasing vehicle electrification, stringent emission regulations, and rising demand for advanced driver-assistance systems (ADAS). Furthermore, the expansion of electric vehicles (EVs) has significantly boosted the adoption of high-precision temperature sensors for battery thermal management. Key players like Bosch, Denso, and Continental are investing in innovative sensor technologies to enhance accuracy and durability, further propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Adoption of Advanced Safety and Emission Control Systems

The automotive industry’s rapid adoption of advanced safety features and stringent emission regulations is significantly driving demand for temperature sensors. Modern vehicles now incorporate multiple temperature monitoring systems that optimize fuel efficiency, reduce emissions, and prevent engine damage. With governments worldwide implementing stricter environmental policies, automakers are integrating more sophisticated thermal management systems, directly increasing sensor deployment. For example, the average premium vehicle now contains over 15-20 temperature sensors, compared to just 5-8 in conventional models from a decade ago.

Accelerated Growth of Electric Vehicles Creating New Demand

The global EV revolution presents substantial opportunities for temperature sensing technologies. Battery thermal management systems in electric vehicles require 30-40% more temperature sensors than traditional internal combustion engines to ensure optimal performance and safety. As EV production is projected to grow at over 25% CAGR through 2030, this sector will become increasingly crucial for temperature sensor manufacturers. New battery chemistries with specific thermal requirements are further driving innovation in sensor accuracy and response times.

Integration of Smart Features and ADAS Systems

Modern vehicles incorporating autonomous driving features and advanced driver assistance systems (ADAS) require precise thermal monitoring of critical components. Temperature sensors play a vital role in preventing electronic system failures that could compromise vehicle safety. The growing complexity of automotive electronics, coupled with the need for real-time thermal data in intelligent vehicles, is pushing automakers to upgrade their sensor technologies. This trend is particularly evident in premium vehicle segments where sensor redundancy and fail-safe thermal monitoring are becoming standard requirements.

➤ The average luxury vehicle now contains temperature sensors monitoring over 30 distinct points compared to less than 10 in economy models, reflecting the growing importance of thermal management in vehicle electronics.

MARKET CHALLENGES

High Cost Pressure and Component Miniaturization Demands

While demand grows, manufacturers face significant cost pressures from automakers seeking to reduce bill-of-materials expenses. Temperature sensors must deliver higher performance at declining price points, creating margin compression throughout the supply chain. Simultaneously, the push for miniaturization—particularly in electric vehicles where space is at a premium—requires sensor manufacturers to invest heavily in R&D for smaller form factors without compromising accuracy or durability.

Other Challenges

Supply Chain Disruptions

The automotive industry’s recovery from semiconductor shortages has highlighted vulnerabilities in sensor supply chains. Many temperature sensor components rely on specialized materials and manufacturing processes susceptible to geopolitical tensions and trade restrictions.

Technical Performance Requirements

Modern applications demand sensors with faster response times (often under 3 seconds), wider operating ranges (-40°C to 150°C), and higher accuracy (±0.5°C). Meeting these specifications while maintaining long-term reliability presents ongoing engineering challenges.

MARKET RESTRAINTS

Standardization Issues and Compatibility Constraints

The lack of universal standards for automotive temperature sensors creates integration challenges across vehicle platforms and OEMs. While major manufacturers have developed proprietary solutions, the industry faces fragmentation that increases development costs and limits component reuse. This becomes particularly problematic when supporting legacy vehicle architectures while developing next-generation systems, requiring sensor suppliers to maintain multiple product lines and development tracks.

MARKET OPPORTUNITIES

Emerging Wireless and Smart Sensor Technologies

The transition toward wireless temperature monitoring presents significant growth potential, particularly for battery systems in electric vehicles. Wireless sensors eliminate wiring complexity while enabling more flexible placement and easier retrofitting. Additionally, smart sensors with integrated diagnostics and predictive capabilities are gaining traction, allowing early detection of thermal issues before they cause system failures. These advanced solutions command premium pricing while reducing total cost of ownership for automakers.

Expansion in Developing Markets

Emerging economies are witnessing rapid automotive sector growth, particularly in the mid-range vehicle segments. As these markets modernize their vehicle fleets and implement stricter emissions standards, demand for temperature sensing solutions will increase substantially. Local manufacturing initiatives in regions like Southeast Asia and Eastern Europe are creating new opportunities for sensor suppliers to establish regional production and strengthen customer relationships.

TEMPERATURE SENSORS FOR AUTOMOTIVE ELECTRONICS MARKET TRENDS

Electrification of Vehicles Driving Demand for Advanced Temperature Sensing Solutions

The rapid shift toward electric vehicles (EVs) and hybrid electric vehicles (HEVs) is significantly propelling the adoption of high-precision temperature sensors in automotive electronics. As battery thermal management becomes critical for ensuring safety and optimizing performance, automakers are increasingly integrating thermistor-based sensors (NTC/PTC) for real-time temperature monitoring. The global EV market is expected to grow at a CAGR exceeding 20% through 2030, creating a substantial demand for thermal management solutions. Additionally, the rise of autonomous driving technologies has intensified the need for reliable temperature sensors to safeguard onboard computing systems from overheating, further accelerating market expansion.

Other Trends

Integration of Smart Sensors with IoT Capabilities

The automotive industry is witnessing a surge in smart temperature sensors equipped with IoT connectivity, enabling predictive maintenance and real-time diagnostics. These sensors not only monitor temperature variations but also communicate data to centralized control units for proactive system adjustments. Automakers are leveraging this technology to enhance fuel efficiency in combustion engines and extend battery life in EVs. The growing penetration of connected cars, projected to account for over 30% of global vehicle sales by 2025, underscores the importance of intelligent sensing systems in modern automotive electronics.

Stringent Emission Regulations Accelerating Technological Innovation

Governments worldwide are imposing rigorous emission standards, compelling manufacturers to develop more sophisticated engine management systems that rely heavily on temperature feedback. For instance, Euro 7 standards and China’s China VI emissions regulations mandate precise thermal monitoring to optimize combustion efficiency and reduce harmful emissions. This regulatory pressure has led to increased R&D investments in MEMS-based temperature sensors and hybrid sensing solutions that combine multiple measurement technologies. The automotive temperature sensor market is consequently experiencing a shift toward compact, multi-functional designs capable of operating in harsh under-hood environments while maintaining high accuracy.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership in Automotive Temperature Sensors

The global temperature sensors for automotive electronics market features a dynamic competitive landscape where established multinational corporations and regional specialists compete for market share. The market is moderately consolidated, with the top five players accounting for approximately 45-50% of global revenue in 2024. Leading manufacturers are accelerating product innovation to meet growing demand for accurate thermal monitoring in electric vehicles (EVs), advanced driver-assistance systems (ADAS), and battery management solutions.

Bosch maintains a dominant position in the market through its comprehensive sensor portfolio and deep integration with automotive OEMs across Europe and Asia. The company recently introduced next-generation NTC thermistors with ±0.5°C accuracy for EV battery packs, strengthening its position in the rapidly growing electric mobility segment. Similarly, TE Connectivity expanded its automotive sensor business through strategic acquisitions and now offers one of the industry’s widest temperature sensing ranges (-40°C to +1,500°C).

Japanese conglomerate Denso leverages its vertical integration capabilities to provide complete thermal management systems, while Sensata Technologies specializes in high-precision sensors for critical automotive applications. These market leaders are facing increasing competition from specialized Asian manufacturers such as TDK and Nippon Thermostat, who are gaining traction through cost-optimized solutions for mass-market vehicles.

The competitive environment continues to evolve with technological shifts toward MEMS-based sensors, wireless temperature monitoring, and AI-driven predictive thermal management systems. Several tier-1 suppliers are forming strategic alliances with semiconductor companies to develop integrated sensing solutions, while smaller players focus on niche applications in commercial vehicles and aftermarket segments.

List of Key Temperature Sensor Manufacturers Profiled

- Bosch GmbH (Germany)

- Denso Corporation (Japan)

- TE Connectivity (Switzerland)

- Sensata Technologies (Netherlands)

- Continental AG (Germany)

- Valeo SA (France)

- Hella GmbH (Germany)

- TDK Corporation (Japan)

- Panasonic Corporation (Japan)

- BorgWarner Inc. (U.S.)

- Qufu Temb Auto Parts Manufacturing (China)

- Nippon Thermostat (Japan)

- Wuhan Huagong Xingaoli Electron (China)

- Inzi Controls (South Korea)

Segment Analysis:

By Type

Thermistor Temperature Sensors Dominate the Market Due to High Accuracy and Cost-Effectiveness

The market is segmented based on type into:

- Thermistor Temperature Sensors

- Subtypes: NTC (Negative Temperature Coefficient), PTC (Positive Temperature Coefficient)

- Thermocouple Temperature Sensors

- Resistance Temperature Detectors (RTDs)

- Infrared Temperature Sensors

- Others

By Application

Engine Management Systems Lead the Market Due to Critical Temperature Monitoring Requirements

The market is segmented based on application into:

- Engine Management Systems

- Climate Control Systems

- Battery Management Systems

- Transmission Systems

- Exhaust Systems

By Vehicle Type

Passenger Vehicles Segment Accounts for Largest Market Share

The market is segmented based on vehicle type into:

- Passenger Vehicles

- Subtypes: Sedans, SUVs, Hatchbacks

- Commercial Vehicles

- Subtypes: Light Commercial Vehicles, Heavy Commercial Vehicles

- Electric Vehicles

By Technology

Contact Type Sensors Lead Due to Widespread Adoption

The market is segmented based on technology into:

- Contact Type Sensors

- Non-Contact Type Sensors

Regional Analysis: Temperature Sensors for Automotive Electronics Market

Asia-Pacific

The Asia-Pacific region dominates the global temperature sensors market for automotive electronics, spearheaded by China and Japan. As the largest automotive manufacturing hubs, these countries contribute significantly to the demand for advanced temperature sensing solutions. The shift toward electric vehicles (EVs) in China, supported by government policies and increasing environmental awareness, has accelerated the adoption of precision sensors for battery thermal management systems. In India, the growing middle-class population and rising vehicle ownership are expanding the market for passenger cars equipped with sophisticated electronics, requiring reliable temperature monitoring. Cost competitiveness remains a key factor in this region, with local manufacturers like Qufu Temb Auto Parts Manufacturing gaining traction alongside global players.

North America

North America’s temperature sensors market is driven by stringent safety regulations and the integration of advanced driver-assistance systems (ADAS) in modern vehicles. The U.S., in particular, focuses on innovation, with major automakers collaborating with sensor manufacturers like Sensata Technologies and TE Connectivity to enhance thermal monitoring in engines and EV battery packs. The region’s strong emphasis on fuel efficiency and emission control further necessitates accurate temperature sensing technologies. Additionally, Canada’s growing EV adoption and Mexico’s expanding automotive production capabilities reinforce the market’s steady growth trajectory.

Europe

Europe’s stringent automotive safety and emission norms, including Euro 6 standards, propel the demand for high-performance temperature sensors. Germany leads the region, with Bosch and Continental providing cutting-edge sensor solutions for premium and luxury vehicles. The rapid transition to electric mobility in countries like Norway and France has also heightened the need for precise thermal management in battery systems. Furthermore, investments in autonomous vehicle technologies across the region are expected to create new opportunities for temperature sensor applications in predictive maintenance and real-time diagnostics.

South America

South America’s market is gradually evolving, with Brazil and Argentina as key contributors. Vehicle electrification is still in early stages, but traditional internal combustion engine (ICE) vehicles continue to drive demand for temperature sensors in engine and exhaust systems. Economic challenges and volatile currency fluctuations have hindered large-scale investments in advanced automotive electronics, yet local suppliers are exploring cost-effective solutions to cater to regional automakers’ needs. The aftermarket segment remains a vital component of the temperature sensors business in this region.

Middle East & Africa

This region shows nascent growth potential, primarily fueled by increasing vehicle production in Turkey and rising luxury car demand in the UAE and Saudi Arabia. Harsh climatic conditions necessitate robust thermal monitoring solutions to ensure vehicle performance and safety. While strict emission regulations are still under development, automakers are gradually incorporating advanced temperature sensing technologies to meet global standards. Regional players are expected to expand partnerships with multinational sensor manufacturers to tap into emerging opportunities in commercial fleets and public transportation.

Report Scope

This market research report provides a comprehensive analysis of the Global Temperature Sensors for Automotive Electronics Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 3,793 million in 2024 and is projected to reach USD 5,151 million by 2032, growing at a CAGR of 4.5%.

- Segmentation Analysis: Detailed breakdown by product type (thermistor, thermocouple), application (passenger vehicles, commercial vehicles), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading players including Panasonic, Bosch, Sensata Technologies, Denso, and Continental, covering their market share, R&D focus, and strategic developments.

- Technology Trends & Innovation: Assessment of sensor miniaturization, integration with IoT platforms, and advanced materials enhancing temperature measurement accuracy.

- Market Drivers & Restraints: Analysis of factors such as rising vehicle electrification, stringent emission norms, and supply chain challenges impacting market growth.

- Stakeholder Analysis: Strategic insights for automakers, sensor manufacturers, and investors on emerging opportunities in electric and autonomous vehicle segments.

The report employs primary and secondary research methodologies, including expert interviews and validated market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Temperature Sensors for Automotive Electronics Market?

->Temperature Sensors for Automotive Electronics Market was valued at 3793 million in 2024 and is projected to reach US$ 5151 million by 2032, at a CAGR of 4.5% during the forecast period.

Which key companies operate in this market?

-> Major players include Panasonic, Bosch, Sensata Technologies, Denso, BorgWarner, Continental, TE Connectivity, and Valeo.

What are the key growth drivers?

-> Growth is driven by increasing vehicle electrification, demand for advanced driver assistance systems (ADAS), and stringent thermal management requirements in EVs.

Which region dominates the market?

-> Asia-Pacific leads in market share due to high automotive production, while North America shows strong growth in electric vehicle adoption.

What are the emerging trends?

-> Key trends include integration of AI for predictive maintenance, development of MEMS-based sensors, and increasing use in battery thermal management systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...