Tandem OLED for In-Vehicle Displays Market Insights

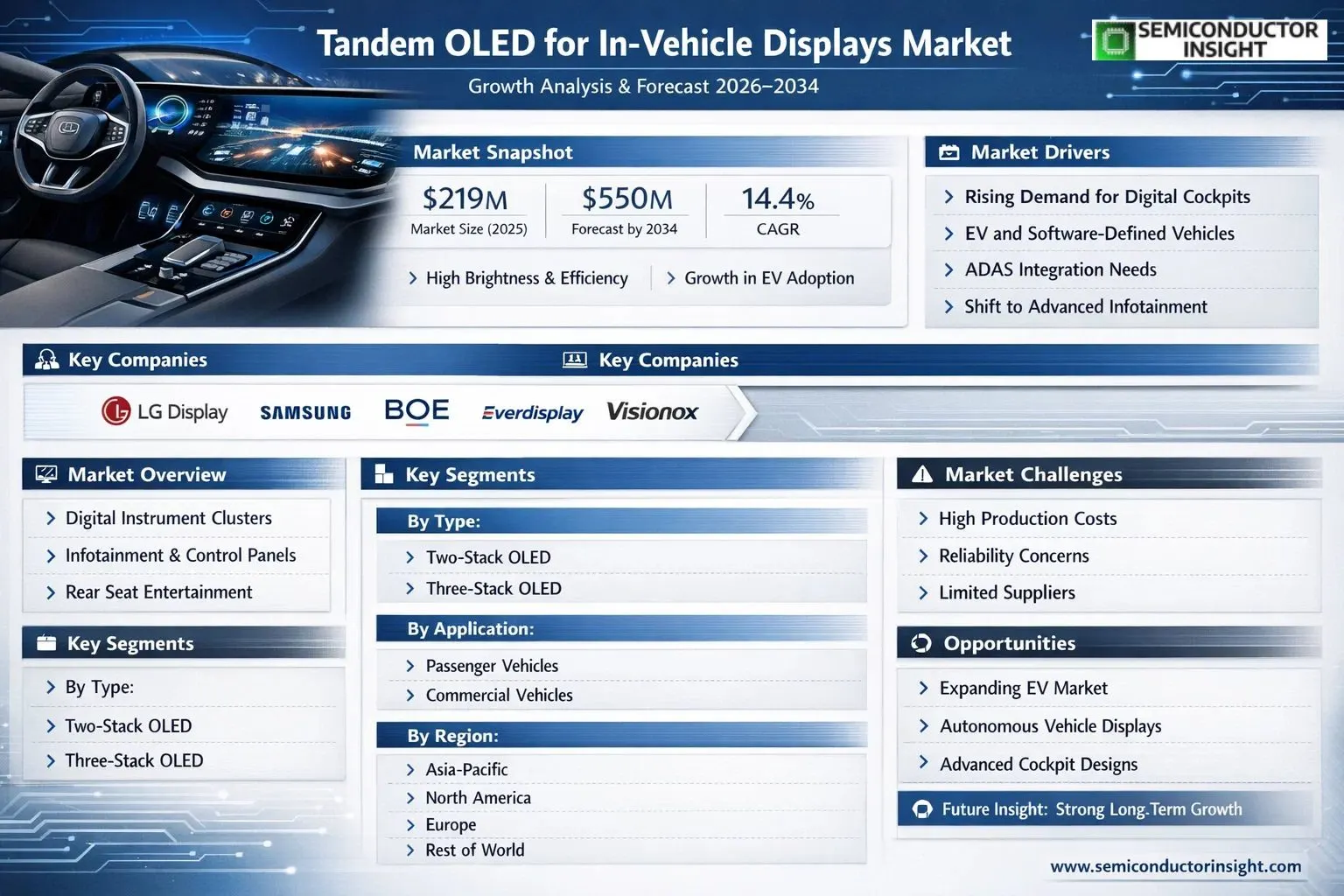

Global Tandem OLED for In-Vehicle Displays market size was valued at USD 219 million in 2025. The market is projected to grow from USD 250.5 million in 2026 to USD 550 million by 2034, exhibiting a CAGR of 14.4% during the forecast period.

Tandem OLED displays are a type of OLED technology where multiple layers of organic material are stacked to improve performance, particularly in terms of brightness, efficiency, and lifespan. Unlike conventional single-stack OLED panels, tandem architecture enables significantly higher luminance output while consuming less power — a critical advantage for automotive applications where displays must remain clearly visible under direct sunlight and varying ambient lighting conditions. The technology encompasses configurations including Two-Stack Tandem OLED, Three-Stack Tandem OLED, and other advanced structural variants, each offering distinct trade-offs between manufacturing complexity, optical performance, and thermal management.

The market is gaining strong momentum because automakers are increasingly prioritizing premium cabin experiences driven by rising consumer demand for digital cockpits and advanced driver-assistance interfaces. Furthermore, the rapid electrification of passenger and commercial vehicles is accelerating the integration of large-format, high-brightness displays for instrument clusters, center stacks, and rear-seat entertainment systems. Key manufacturers shaping the competitive landscape include LG Display, Samsung Display, BOE Technology, Everdisplay Optronics, and Visionox, which collectively held a significant share of global market revenue in 2025. These players continue to invest in capacity expansion and next-generation panel development to meet growing automotive OEM demand across North America, Europe, and Asia.

MARKET DRIVERS

Rising Demand for Premium In-Vehicle Display Experiences Accelerating Tandem OLED Adoption

The automotive industry is undergoing a profound transformation in cabin experience, with automakers increasingly prioritizing high-performance display technologies to differentiate their vehicles in a competitive marketplace. Tandem OLED for In-Vehicle Displays market is gaining significant momentum as original equipment manufacturers (OEMs) seek display solutions that can deliver superior brightness, contrast, and longevity compared to conventional single-stack OLED panels. Tandem OLED technology, which stacks two emissive layers to dramatically enhance luminance output and operational lifespan, is uniquely positioned to meet the stringent performance requirements of automotive environments, where displays must remain legible under direct sunlight and function reliably across extreme temperature ranges.

Electrification and Software-Defined Vehicle Trends Expanding Display Surface Area

The accelerating shift toward electric vehicles (EVs) and software-defined vehicles (SDVs) is fundamentally reshaping interior architectures. With the removal of traditional mechanical instrument clusters and the rise of large-format central infotainment systems, digital instrument panels, and heads-up display (HUD) integration, the demand for high-quality display substrates is expanding rapidly. Tandem OLED panels, capable of sustaining peak brightness levels exceeding 2,000 nits while maintaining energy efficiency, are increasingly favored for these expansive display configurations. Leading EV platforms are actively evaluating and integrating tandem OLED solutions to enhance the visual fidelity of their driver-assistance and infotainment interfaces.

➤ Tandem OLED technology offers approximately twice the brightness and up to three times the operational lifespan of conventional single-stack OLED panels under automotive-grade usage conditions, making it a compelling choice for next-generation in-vehicle display applications.

Furthermore, regulatory emphasis on driver safety and the proliferation of advanced driver-assistance systems (ADAS) are creating additional pull for display technologies that combine high luminance with pixel-level precision. Tandem OLED for In-Vehicle Displays market benefits directly from automakers’ requirements for displays capable of rendering critical ADAS alerts and navigation data with exceptional clarity and responsiveness, reinforcing adoption across both premium and increasingly mid-tier vehicle segments.

MARKET CHALLENGES

High Manufacturing Complexity and Cost Pressures Constraining Broader Market Penetration

Despite the compelling performance characteristics of tandem OLED technology, Tandem OLED for In-Vehicle Displays market faces considerable challenges related to manufacturing complexity and associated cost structures. The deposition of dual emissive layers with the required precision and uniformity demands advanced fabrication equipment and tightly controlled processes, resulting in production costs that are meaningfully higher than those of conventional OLED or LCD alternatives. For automotive OEMs operating under intense margin pressures, the cost premium associated with tandem OLED panels can represent a substantial barrier, particularly in volume segments where display cost sensitivity is acute. Supply chain constraints around specialized organic materials and high-precision deposition systems further compound these cost dynamics.

Other Challenges

Automotive-Grade Qualification and Reliability Validation

Automotive display components must satisfy rigorous qualification standards, including extended temperature cycling, humidity resistance, and operational lifetime requirements that often exceed those applicable to consumer electronics. For tandem OLED panels, the multi-layer architecture introduces additional variables in long-term reliability that must be systematically validated, extending qualification timelines and increasing development costs for both panel manufacturers and automotive integrators within Tandem OLED for In-Vehicle Displays market.

Limited Supplier Ecosystem and Technology Concentration

The supplier landscape for automotive-grade tandem OLED panels remains highly concentrated, with only a handful of established display manufacturers currently possessing the technical capability and production infrastructure to supply at automotive volumes. This concentration creates supply security concerns for OEMs and limits competitive pricing dynamics, potentially slowing the pace of adoption across the broader Tandem OLED for In-Vehicle Displays Market until the supplier base matures and diversifies.

MARKET RESTRAINTS

Elevated Panel Costs Limiting Adoption Beyond Premium Vehicle Segments

One of the most significant restraints affecting Tandem OLED for In-Vehicle Displays market is the elevated cost per unit that characterizes tandem OLED panels relative to incumbent display technologies such as LCD and mini-LED. While premium and luxury vehicle segments demonstrate sufficient willingness to absorb this cost premium in pursuit of differentiated cabin experiences, the mass-market and entry-level segments remain largely inaccessible to tandem OLED solutions under current pricing structures. Until manufacturing scale, process optimization, and raw material efficiencies converge to reduce panel costs meaningfully, the addressable market for tandem OLED in automotive applications will remain disproportionately concentrated in higher-priced vehicle categories.

Thermal Management and Integration Complexities in Automotive Environments

The integration of tandem OLED displays into automotive cabin environments presents non-trivial thermal management challenges. While tandem OLED panels are inherently more efficient than single-stack counterparts at equivalent brightness levels, the elevated luminance outputs demanded by automotive applications still generate heat that must be carefully managed to preserve panel longevity and prevent performance degradation. Vehicle interior packaging constraints, combined with the diverse thermal environments encountered across global markets — from sub-zero winter conditions to high-temperature desert climates — place complex demands on display system design within Tandem OLED for In-Vehicle Displays market. These integration complexities can extend development cycles and increase system-level costs, acting as a meaningful restraint on near-term market expansion.

MARKET OPPORTUNITIES

Expanding Cockpit Digitalization Creating High-Value Application Opportunities for Tandem OLED

The accelerating trend toward fully digitalized vehicle cockpits presents substantial growth opportunities for Tandem OLED for In-Vehicle Displays market. As automakers transition from discrete instrument clusters and infotainment screens toward expansive, continuously curved, or pillar-to-pillar display architectures, the demand for flexible, high-brightness, and visually immersive display technologies is intensifying. Tandem OLED panels, with their inherent flexibility potential and superior optical performance, are exceptionally well-aligned with these evolving cockpit design philosophies. The increasing adoption of integrated display ribbons and panoramic display configurations in next-generation vehicle platforms represents a high-value expansion vector for tandem OLED technology providers and their automotive supply chain partners.

Asia-Pacific Automotive OEM Activity and EV Volume Growth Presenting Significant Regional Upside

The Asia-Pacific region, led by the robust expansion of Chinese domestic EV manufacturers and the continued technological advancement of Japanese and South Korean automotive OEMs, represents a particularly significant opportunity for Tandem OLED for In-Vehicle Displays market. Chinese EV brands have demonstrated a pronounced willingness to adopt advanced display technologies as core product differentiators, and the scale of their production volumes provides a commercially attractive pathway for tandem OLED panel suppliers to achieve the volume economics necessary to reduce unit costs and broaden market accessibility. Concurrently, established display manufacturers in South Korea and Japan are investing in expanded tandem OLED production capacity, which is expected to progressively improve supply availability and competitive pricing dynamics across Global automotive display ecosystem.

Autonomous and Semi-Autonomous Vehicle Development Unlocking New Passenger-Cabin Display Use Cases

The progression of autonomous and semi-autonomous vehicle technology is anticipated to substantially expand the role of in-vehicle displays, transitioning them from primarily driver-focused interfaces to comprehensive passenger infotainment and productivity platforms. This evolution is expected to drive demand for multiple high-quality display surfaces throughout the vehicle cabin, including rear-seat entertainment systems, pillar-integrated displays, and overhead panels — application contexts in which the brightness, color accuracy, and form-factor flexibility of tandem OLED technology confer meaningful competitive advantages. As regulatory frameworks for higher levels of vehicle autonomy mature and consumer adoption of assisted-driving features accelerates, Tandem OLED for In-Vehicle Displays market stands to benefit from a structural expansion in total display content per vehicle, creating durable long-term demand across the automotive value chain.

MAIN TITLE HERE () Trends

Rising Demand for High-Brightness, Energy-Efficient Displays Driving Tandem OLED for In-Vehicle Displays market

Tandem OLED for In-Vehicle Displays market is witnessing accelerated momentum as automotive manufacturers increasingly prioritize superior display quality, durability, and energy efficiency in next-generation vehicle interiors. Tandem OLED technology, which stacks multiple organic emissive layers to achieve enhanced brightness and extended operational lifespan, is emerging as a preferred solution for premium cockpit displays, instrument clusters, and infotainment systems. Unlike conventional single-stack OLED panels, tandem configurations deliver significantly higher luminance output while maintaining lower power consumption — a critical advantage for electric vehicles where energy management is paramount. The growing integration of large-format curved and flexible displays across passenger vehicle cabins is further reinforcing the adoption of this advanced display technology across global automotive platforms.

Other Trends

Expansion of Two-Stack and Three-Stack Tandem OLED Configurations

Within Tandem OLED for In-Vehicle Displays market, both Two-Stack and Three-Stack Tandem OLED configurations are gaining traction. Two-Stack Tandem OLEDs are currently the dominant product type, widely deployed in mid-to-premium vehicle segments due to their cost-to-performance balance. Three-Stack variants, offering even greater brightness and longevity, are increasingly being explored for ultra-premium and commercial vehicle applications where display visibility under direct sunlight conditions is critical. Key manufacturers including LG, Samsung, BOE, Everdisplay, and Visionox are actively investing in scaling production capabilities for both configurations to meet rising automotive-grade demand.

Growing Adoption Across Passenger and Commercial Vehicle Segments

The passenger vehicle segment continues to account for the dominant share of demand within Tandem OLED for In-Vehicle Displays market, driven by the rapid proliferation of digital cockpit architectures and multi-display cabin environments. However, commercial vehicle manufacturers are also beginning to explore tandem OLED integration for advanced driver assistance system (ADAS) interfaces and fleet management displays, reflecting a broadening application scope beyond traditional luxury automotive use cases.

Regional Dynamics and Competitive Landscape Shaping Market Trajectory

Asia-Pacific, led by China, South Korea, and Japan, represents the most dynamic regional market for Tandem OLED for In-Vehicle Displays, supported by the presence of leading panel manufacturers and a robust automotive production ecosystem. North America and Europe are also registering strong demand growth, underpinned by automakers’ strategic investments in vehicle digitalization and premium user experience differentiation. The competitive landscape remains concentrated, with the top five global players collectively holding a significant revenue share as of 2025, while ongoing research into next-generation organic material stacks continues to define the technology roadmap for in-vehicle display innovation.

COMPETITIVE LANDSCAPE

Key Industry Players

Tandem OLED Technology Driving the Future of Automotive Cockpits

Global Tandem OLED for In-Vehicle Displays market is characterized by intense competition, primarily driven by established display panel manufacturers with significant technological expertise. LG Display and Samsung Display are the dominant market leaders, leveraging their extensive experience in OLED technology from smartphone and television markets to secure major contracts with automotive OEMs. These top players held a significant collective revenue share in 2025, with their advanced manufacturing capabilities and strong relationships with Tier-1 suppliers providing a substantial competitive edge in delivering high-reliability, high-brightness displays for demanding automotive environments.

Beyond the market leaders, several other significant players are carving out substantial niches through specialized manufacturing and regional focus. Chinese panel makers like BOE, Everdisplay, and Visionox are aggressively expanding their automotive display portfolios, competing strongly on cost and capacity. Other global and regional manufacturers are focusing on specific display sizes, technological variations like Two-Stack and Three-Stack architectures, or forming strategic partnerships with automotive suppliers to address the growing demand for premium in-vehicle infotainment and digital cockpit systems.

List of Key Tandem OLED for In-Vehicle Displays Companies Profiled

- LG Display

- Samsung Display

- BOE Technology

- Everdisplay Optronics

- Visionox Technology

- Japan Display Inc.

- Innolux Corporation

- AU Optronics

- Sharp Corporation

- Tianma Microelectronics

- CSOT (China Star Optoelectronics Technology)

- Universal Display Corporation

- eMagin Corporation

- Royole Corporation

- Kyocera Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Two-Stack Tandem OLED leads the segment by delivering an optimal balance of enhanced brightness, efficiency, and longevity tailored for demanding in-vehicle conditions.

|

| By Application |

|

Passenger Vehicle dominates as it caters to the growing consumer demand for premium interior experiences and advanced connectivity features.

|

| By End User |

|

OEMs are the frontrunners, integrating tandem OLED displays as core components in next-generation vehicle architectures.

|

| By Panel Size |

|

Medium Panels command the forefront, striking a versatile equilibrium for contemporary in-vehicle interface designs.

|

| By Display Function |

|

Infotainment Displays spearhead adoption, serving as the interactive nerve center of modern vehicle interiors.

|

Regional Analysis: Tandem OLED for In-Vehicle Displays Market

Asia-Pacific

Pioneering tandem OLED layers excel in high-luminance output, ideal for dashboard and center stack displays. Innovations focus on power efficiency, extending battery life in electric vehicles while maintaining superior color accuracy.

Major panel manufacturers collaborate with automotive giants, customizing Tandem OLED solutions for curved and flexible in-vehicle screens, strengthening regional supply chain dominance.

Electrification trends and smart cockpit demands fuel expansion, supported by policy frameworks encouraging indigenous production and export of advanced display technologies.

North America

North America exhibits strong momentum in Tandem OLED for In-Vehicle Displays market, propelled by innovation hubs and premium vehicle segments. Automakers prioritize these displays for their exceptional contrast and reliability in harsh environments, integrating them into digital clusters and entertainment systems. Strategic partnerships between display suppliers and U.S.-based firms accelerate customization for autonomous driving interfaces. Regulatory emphasis on safety enhances adoption, as tandem structures offer consistent performance across temperature extremes. Venture capital inflows support startups refining blue-light stability, vital for longevity. Consumer affinity for tech-laden vehicles in this region drives demand, particularly among electric SUV buyers seeking immersive experiences. While facing supply dependencies, localized assembly initiatives mitigate risks, positioning North America as a key growth area.

Europe

Europe advances steadily within Tandem OLED for In-Vehicle Displays market, leveraging automotive engineering prowess. Luxury brands incorporate tandem panels for seamless panoramic displays, emphasizing sustainability and recyclability. Stringent emission norms align with energy-efficient OLED traits, boosting electric vehicle integrations. Collaborative R&D consortia refine anti-reflective coatings for superior daytime visibility. Heritage manufacturers adapt tandem tech for heads-up displays, enhancing driver assistance features. Supply chain diversification efforts counter global disruptions, fostering resilient production. Affluent markets favor high-fidelity visuals, supporting market penetration amid electrification shifts. Europe’s focus on user-centric designs solidifies its competitive stance in premium segments.

South America

South America emerges as a promising frontier in Tandem OLED for In-Vehicle Displays market, with rising middle-class aspirations fueling demand for upgraded interiors. Local assemblers partner with international suppliers to embed tandem displays in mid-range SUVs, prioritizing cost-effective brightness enhancements. Urban mobility trends favor compact, vibrant screens for navigation and connectivity. Infrastructure improvements enable better distribution channels, while economic stabilization encourages investments. Challenges like import tariffs spur interest in regional adaptations, tailoring tandem OLED for tropical climates. Growing electric vehicle pilots accelerate adoption, positioning South America for accelerated expansion in connected cockpits.

Middle East & Africa

Middle East & Africa show nascent yet accelerating interest in Tandem OLED for In-Vehicle Displays market, driven by luxury import surges and diversification strategies. High-end vehicles feature tandem panels for opulent infotainment, resilient to extreme heat. Sovereign funds invest in display tech localization, fostering joint ventures. Africa’s urbanization pushes demand for durable, sunlight-readable displays in public transport and premium cars. Oil-rich economies pivot towards electric fleets, valuing tandem OLED efficiency. Skill development programs bridge expertise gaps, enabling gradual integration. This region’s strategic outlook promises untapped potential amid infrastructure modernization.

Report Scope

This market research report provides a comprehensive analysis of the Tandem OLED for In-Vehicle Displays Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Tandem OLED for In-Vehicle Displays Market?

-> Global Tandem OLED for In-Vehicle Displays market was valued at USD 219 million in 2025 and is expected to reach USD 550 million by 2034, at a CAGR of 14.4% during the forecast period.

Which key companies operate in Tandem OLED for In-Vehicle Displays Market?

-> Key players include LG, Samsung, BOE, Everdisplay, Visionox, among others.

What are the key growth drivers?

-> Key growth drivers include demand for brighter, more efficient, and longer-lasting displays in vehicles, automotive electrification, and premium infotainment systems.

Which region dominates the market?

-> Asia is the fastest-growing region, while North America remains a key market.

What are the emerging trends?

-> Emerging trends include two-stack and three-stack Tandem OLED technologies, applications in passenger vehicles, and advancements in light emission control.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...