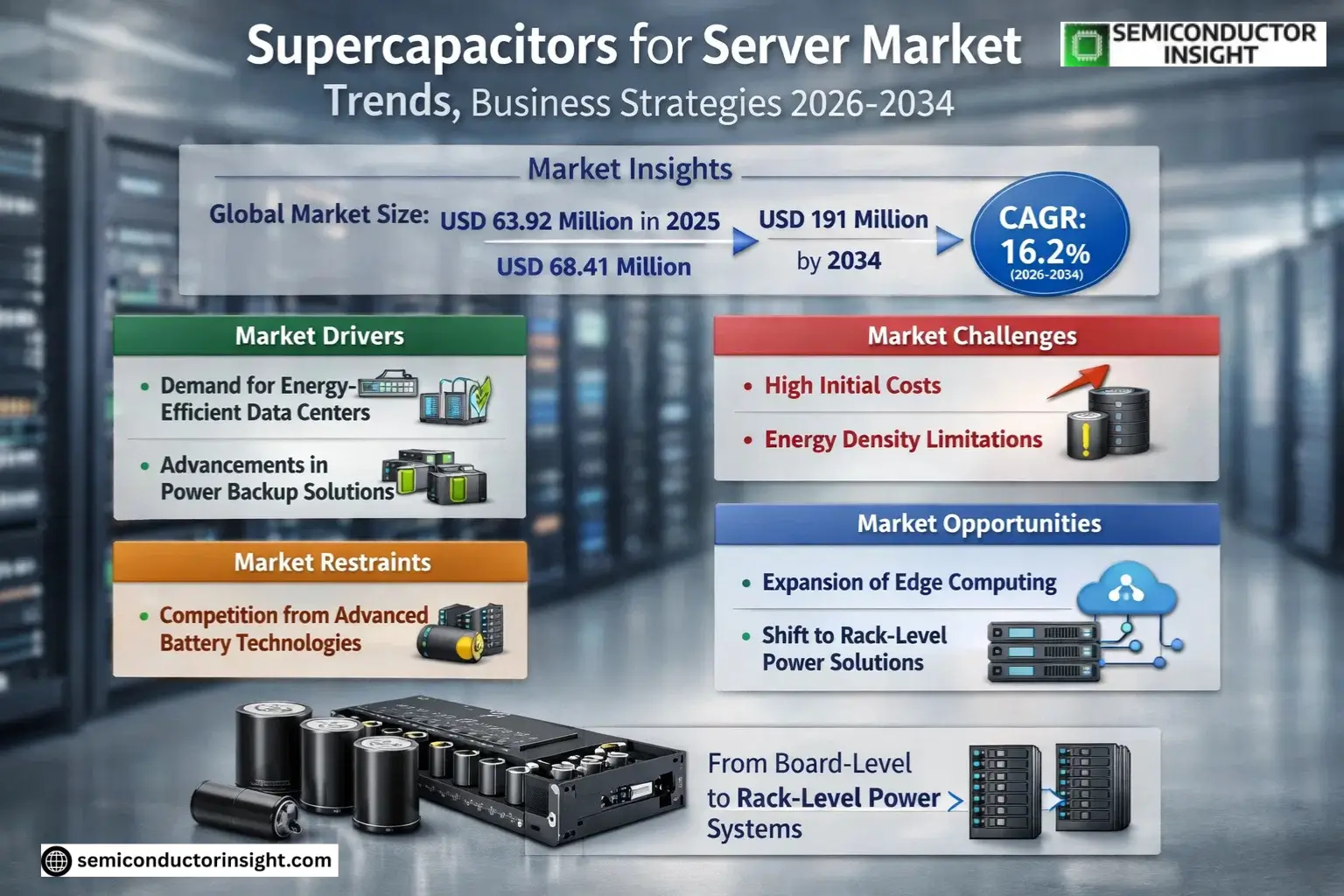

Market Insights

Global Supercapacitors for Server Market size was valued at USD 63.92 million in 2025. The market is projected to grow from USD 68.41 million in 2026 to USD 191 million by 2034, exhibiting a CAGR of 16.2% during the forecast period.

Supercapacitors for servers are advanced energy storage devices designed to provide rapid power delivery and backup in data center environments. These components play a critical role in maintaining uninterrupted server operations during power fluctuations, with applications ranging from board-level hold-up solutions to rack-level power buffering systems. The technology primarily utilizes electrostatic double-layer capacitors (EDLC), pseudocapacitors, or hybrid designs, each offering distinct advantages in power density, cycle life, and energy storage capacity.

The market growth is driven by increasing demand for reliable power management solutions in hyperscale data centers and AI server clusters, where power spikes and transient loads require sophisticated energy buffering capabilities. Recent technological advancements have expanded supercapacitor applications from traditional backup functions to active power shaping roles, particularly in GPU-intensive computing environments. Major industry players including Eaton, Skeleton Technologies, and Nippon Chemi-Con are developing higher-voltage DC ecosystem solutions to address the evolving needs of next-generation server architectures.

MARKET DRIVERS

Growing Demand for Energy-Efficient Data Centers

The increasing adoption of Supercapacitors for Server Market is primarily driven by the need for energy-efficient solutions in data centers. With global data traffic expected to grow by 25% annually, supercapacitors provide rapid charge-discharge cycles, reducing power interruptions and improving server reliability. This is particularly crucial for hyperscale data centers that require uninterrupted power supply (UPS) solutions.

Advancements in Power Backup Solutions

Technological advancements in supercapacitor-based energy storage have enhanced their viability as alternatives to traditional batteries in server applications. These components offer longer lifecycle performance (up to 1 million cycles) and superior thermal stability, making them ideal for data center power management.

The integration of hybrid energy storage systems combining lithium-ion batteries and supercapacitors is also gaining traction, further propelling market growth.

MARKET CHALLENGES

High Initial Costs Compared to Traditional Solutions

Despite their advantages, supercapacitors for server applications face challenges due to higher upfront costs compared to lead-acid or lithium-ion batteries. The specialized materials required for manufacturing, such as activated carbon and graphene, contribute to these elevated prices.

Other Challenges

Energy Density Limitations

Supercapacitors currently offer lower energy density than batteries, requiring larger stacks for extended backup durations, which can be a constraint in space-constrained server environments.

MARKET RESTRAINTS

Competition from Advanced Battery Technologies

The rapid development of solid-state batteries and enhanced lithium-ion solutions presents a competitive challenge for the Supercapacitors for Server Market. These alternatives offer improving energy densities and declining costs, potentially limiting supercapacitor adoption in certain server applications.

MARKET OPPORTUNITIES

Expansion of Edge Computing Infrastructure

The growth of edge computing creates significant opportunities for supercapacitor adoption in decentralized server deployments. These applications require compact, high-performance power solutions that can operate reliably in diverse environmental conditions, where supercapacitors excel.

Supercapacitors for Server Market Trends

Shift from Board-Level to Rack-Level Power Solutions

The server supercapacitor market is seeing a fundamental transition from board-level hold-up applications toward rack-level power buffering. This evolution responds to the growing power demands of modern data centers, particularly AI server clusters that experience spiky, fast-changing power loads. Supercapacitors are increasingly deployed to smooth demand profiles and prevent infrastructure overbuild.

Other Trends

Technical Evolution in Chemistry and Form Factors

Market differentiation now centers on three technical axes: chemistry (EDLC vs hybrid), form factors (cells to rack units), and KPI stacks (voltage window, ESR, thermal performance). Hybrid supercapacitors gain traction where energy density requirements conflict with footprint constraints, while EDLC maintains dominance in high-power cycle applications.

Supply Chain and Vendor Landscape Shifts

The supply chain is developing distinct layers – from upstream materials to integrated rack solutions. Leading vendors now differentiate through system-level capabilities including power management integration, thermal design, and validation under real workload conditions. Recent partnerships between power system providers and supercapacitor manufacturers signal a move toward standardized rack-integrated solutions.

Operational Integration Becomes Critical

As deployments scale, lifecycle management capabilities emerge as key differentiators. Top suppliers are implementing health telemetry systems, hot-swap workflows, and standardized interfaces to transform supercapacitors from simple components into managed operational assets. This shift requires tighter integration with power shelves and DC ecosystem architectures.

Voltage Standardization and Power Orchestration

The market is transitioning from 48V in-rack solutions toward higher-voltage DC ecosystems with distributed buffering. Future growth will be driven by supercapacitors’ ability to coordinate power shaping at rack level, reducing infrastructure shocks and enabling higher power ceilings in next-gen server deployments.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Supercapacitor Suppliers Strategically Positioning for Server Market Expansion

Eaton and Skeleton Technologies currently lead the server supercapacitor market with integrated rack-level power solutions, capturing over 30% combined market share. The competitive landscape shows a mix of established capacitor manufacturers diversifying into server applications and specialized energy storage firms developing high-power density solutions. Market leadership hinges on technical capabilities in balancing energy density, thermal management, and rack integration expertise rather than pure manufacturing scale.

Niche innovators like CAP-XX and LS Materials are gaining traction with hybrid supercapacitor designs optimized for AI server power spike absorption. Japanese and Chinese component manufacturers (Nippon Chemi-Con, Kyocera, Yageo) maintain strong footholds in board-level solutions while expanding into modular systems. The market shows increasing vertical integration, with capacitor manufacturers forming strategic alliances with power supply and server platform vendors to deliver certified rack-compatible solutions.

List of Key Supercapacitor for Server Companies Profiled

- Eaton

- Skeleton Technologies

- Nippon Chemi-Con

- Kyocera

- Yageo

- CAP-XX

- LS Materials

- Nantong Jianghai Capacitor

- Fujian Torch Electron Technology

- Hunan Aihua Group

- Shanghai Yongming Electronic

- Maxwell Technologies

- Ioxus

- Vishay Intertechnology

- Panasonic

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

EDLC Segment dominates with superior power delivery and cycle endurance for server applications:

|

| By Application |

|

AI Servers Segment shows strongest growth potential with specialized power requirements:

|

| By End User |

|

Cloud Service Providers lead adoption due to scale and power management needs:

|

| By Voltage |

|

Higher Voltage Systems emerging as next-generation solution:

|

| By Integration Level |

|

Rack-Level Integration represents the strategic direction:

|

Regional Analysis: Supercapacitors for Server Market

The United States accounts for over 80% of North America’s supercapacitor adoption in server applications, with concentrated demand from Silicon Valley’s hyperscale data centers and financial sector server farms requiring uninterrupted power solutions.

Canada’s growing focus on green data centers has boosted supercapacitor installations, particularly in Quebec and British Columbia where hydroelectric power complements the sustainability benefits of capacitor-based energy storage systems.

Mexico shows growing potential with near-shoring data center investments, though supercapacitor adoption remains in early stages compared to northern neighbors, primarily serving enterprise server rooms rather than large-scale facilities.

Strategic collaborations between American supercapacitor manufacturers and server OEMs are driving customized solutions, particularly for edge computing applications where space constraints favor compact power solutions.

Europe

Europe’s supercapacitor adoption in server infrastructure is gaining momentum, fueled by the EU’s climate neutrality goals and stringent energy efficiency directives. Germany leads regional deployment, especially in Frankfurt’s financial data hubs, while Nordic countries leverage supercapacitors’ cold weather performance advantages. The region sees growing integration with renewable-powered data centers, where supercapacitors provide bridging power during intermittent generation. European manufacturers are focusing on developing ultra-high capacity modules specifically for next-generation server racks.

Asia-Pacific

APAC presents the fastest-growing market for server supercapacitors, with China’s massive data center builds and Japan’s precision electronics driving demand. Singapore and Hong Kong prioritize supercapacitors for their space-efficient properties in high-density urban data centers. South Korean manufacturers lead in hybrid supercapacitor-battery solutions for server applications, while India’s emerging market shows potential with new hyperscale projects incorporating advanced power management systems.

South America

Brazil dominates South America’s nascent server supercapacitor market, primarily serving financial sector data centers in São Paulo. The region faces adoption challenges due to higher upfront costs but benefits from supercapacitors’ lower maintenance needs in tropical climates. Chile’s renewable energy projects are beginning to incorporate capacitor-based power conditioning for server farms.

Middle East & Africa

The UAE and South Africa lead supercapacitor adoption in server applications across MEA, driven by smart city initiatives and growing digital infrastructure. Middle Eastern data centers value supercapacitors for reliable performance in high temperatures, while African deployments focus on micro-data centers where supercapacitors offer maintenance advantages over traditional UPS systems in remote locations.

Report Scope

This market research report provides a comprehensive analysis of the Supercapacitors for Server Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of supercapacitors in powering advancements across server applications such as general purpose servers and AI servers.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, voltage, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, supercapacitor design trends, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Supercapacitors for Server Market?

-> Supercapacitors for Server Market size was valued at USD 63.92 million in 2025. The market is projected to grow from USD 68.41 million in 2026 to USD 191 million by 2034, exhibiting a CAGR of 16.2% during the forecast period.

Which key companies operate in Supercapacitors for Server Market?

-> Key players include Eaton, Skeleton Technologies, Nippon Chemi-Con, Kyocera, Yageo, CAP-XX, LS Materials, Nantong Jianghai Capacitor, Fujian Torch Electron Technology, Hunan Aihua Group, and Shanghai Yongming Electronic.

What are the key growth drivers?

-> Key growth drivers include rising demand for AI servers, shift from board-level hold-up to rack-level power buffering, and increasing need for power management solutions in data centers.

Which region dominates the market?

-> Asia dominates the market, with significant contributions from China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include adoption of hybrid supercapacitors, integration with higher-voltage DC ecosystems, and development of rack-integrated capacitive energy storage systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...