MARKET INSIGHTS

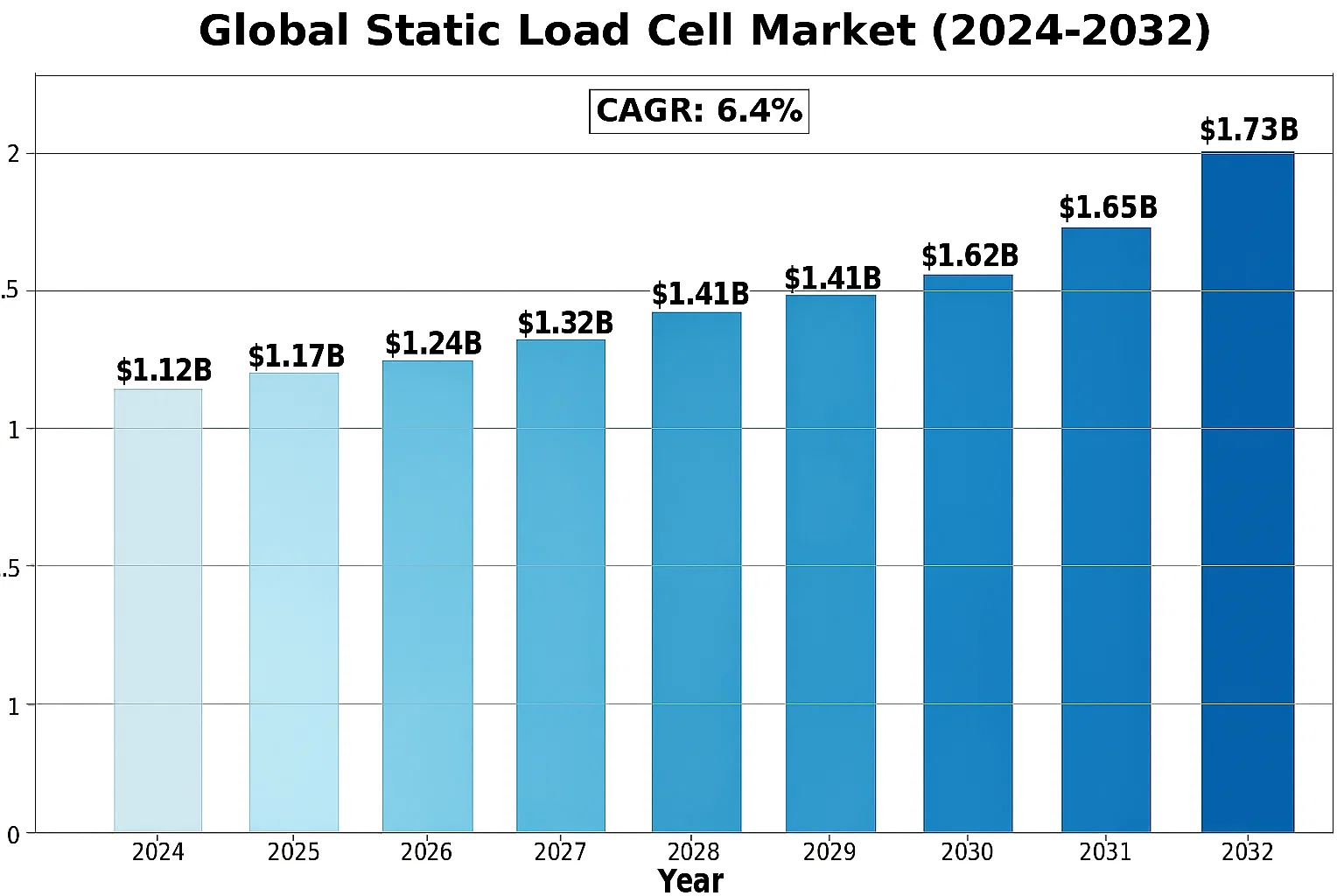

The global Static Load Cell Market size was valued at US$ 1.12 billion in 2024 and is projected to reach US$ 1.73 billion by 2032, at a CAGR of 6.4% during the forecast period 2025-2032.

Static load cells are precision sensors designed to measure compressive or tensile forces in stationary applications. These devices convert mechanical force into electrical signals, playing a critical role in industrial weighing systems, material testing, and structural monitoring. The market offers various types including hydraulic, pneumatic, strain gauge, and capacitive load cells, each suited for specific measurement ranges and environmental conditions.

The market growth is driven by increasing automation in manufacturing, stringent quality control requirements, and expanding infrastructure projects worldwide. While North America leads in technological adoption, Asia-Pacific shows the fastest growth due to rapid industrialization. Recent developments include Instron’s 2024 launch of next-gen load cells with improved accuracy (±0.02% of full scale) for aerospace applications. Key players like HBK and Siemens continue to dominate with over 35% combined market share through advanced R&D and strategic acquisitions.

MARKET DYNAMICS

MARKET DRIVERS

Growing Industrial Automation Demands Accelerate Static Load Cell Adoption

The global shift toward industrial automation across manufacturing, automotive, and aerospace sectors is creating unprecedented demand for precision measurement tools like static load cells. With industrial IoT implementations growing at a compound annual rate exceeding 15%, these force measurement devices have become critical components in automated production lines. Modern static load cells offer real-time data collection capabilities with accuracy levels surpassing 0.03% of full scale, enabling manufacturers to achieve superior quality control while reducing material waste. Recent market analyses indicate that over 40% of new manufacturing facilities now incorporate static load cells in their quality assurance processes from initial operation.

Stringent Safety Regulations in Construction Drive Market Growth

Construction industry regulations worldwide are mandating stricter material testing protocols, particularly for high-stress structural components. Static load cells have emerged as the preferred solution for compliance testing due to their ability to provide verifiable, repeatable measurements under controlled conditions. The European construction equipment market alone has seen a 22% increase in static load cell deployment for concrete stress testing since 2022 following updated EU structural safety directives. Similar regulatory trends in North America and Asia-Pacific regions are creating parallel growth opportunities, with bridge and high-rise construction projects allocating up to 8% of their quality assurance budgets specifically for load testing equipment.

➤ Major infrastructure projects such as the U.S. Infrastructure Bill and China’s Belt and Road Initiative now require certified load test documentation at multiple construction phases.

Furthermore, advancements in wireless load cell technology are eliminating previous installation constraints, allowing for temporary monitoring solutions that reduce project timelines while maintaining compliance. This technological evolution is expected to drive adoption across smaller construction firms previously deterred by implementation costs.

MARKET RESTRAINTS

High Initial Investment Costs Limit Small Business Adoption

While static load cells deliver long-term operational benefits, their implementation presents significant financial barriers for small and medium enterprises. Premium-grade load cells with advanced features such as temperature compensation and wireless connectivity can cost upwards of 70% more than basic models, placing them beyond reach for many potential adopters. Market data indicates that nearly 65% of small manufacturing firms consider cost the primary deterrent when evaluating load cell implementation. This financial barrier is particularly acute in developing economies where equipment budgets are constrained and financing options limited.

Additional Constraints

Technical Complexity

The integration of static load cells into existing systems often requires specialized engineering expertise that many organizations lack internally. Calibration and maintenance procedures demand trained personnel, creating operational bottlenecks for companies without dedicated metrology departments.

Environmental Sensitivity

Even advanced static load cells remain vulnerable to performance degradation from extreme temperatures, humidity, and electromagnetic interference. Industries operating in harsh environments frequently report measurement inaccuracies that require costly mitigation measures.

MARKET CHALLENGES

Calibration Maintenance and Drift Issues Impact Market Confidence

The precision measurement industry faces ongoing challenges with measurement drift in static load cells, where long-term use leads to gradual accuracy degradation. Industry studies reveal that over 30% of in-service load cells exceed permissible error margins within two years of deployment without proper recalibration. This phenomenon creates significant operational challenges for industries requiring sustained measurement accuracy, particularly in pharmaceutical manufacturing and aerospace applications where tolerance thresholds are exceptionally tight.

Competitive Pressure from Alternative Technologies

Emerging non-contact measurement systems using laser and vision-based technologies are capturing market share in applications where traditional load cells previously dominated. These alternatives offer advantages in cleanroom environments and scenarios requiring rapid measurement of moving objects, presenting a growing challenge to conventional static load cell manufacturers. However, load cells maintain superiority in high-force applications exceeding 50kN, where alternative technologies struggle with accuracy and reliability.

Supply Chain Vulnerabilities

The global semiconductor shortage has impacted production lead times for smart load cells incorporating strain gauge signal conditioning electronics. Manufacturers report average delivery delays of 12-16 weeks for advanced models, compelling some end-users to postpone implementation plans or seek alternative solutions.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy Create New Growth Vectors

The rapid expansion of wind and solar energy infrastructure presents substantial opportunities for static load cell manufacturers. Modern wind turbine installations now incorporate sophisticated load monitoring systems that utilize arrays of high-capacity load cells to measure structural stresses during operation. Each offshore wind turbine requires between 8-12 specialized load cells for continuous monitoring, creating a market estimated to surpass 180,000 units annually by 2026. Similarly, solar tracking systems increasingly integrate compact load cells to optimize panel positioning and prevent structural overload during extreme weather events.

Miniaturization Trends Enable New Industrial Applications

Recent breakthroughs in micro-electromechanical systems (MEMS) technology have enabled development of sub-gram load cells with measurement precision previously unattainable at small scales. These miniature devices are revolutionizing quality control in electronics manufacturing, where components require force measurement at resolutions as fine as 0.001N. The global market for micro-load cells in semiconductor production has grown at 28% annually since 2021, driven by the increasing complexity of chip packaging processes and stringent assembly requirements.

Smart Factory Integration

Industry 4.0 initiatives are creating demand for intelligent load cells with embedded connectivity and self-diagnostic capabilities. Leading manufacturers now offer models with predictive maintenance features that reduce unplanned downtime by up to 40%. These smart devices automatically track performance metrics and alert operators to potential calibration needs or mechanical issues before they impact production quality.

STATIC LOAD CELL MARKET TRENDS

Industrial Automation Surge to Drive Market Growth for Static Load Cells

The integration of static load cells in industrial automation systems is transforming manufacturing precision across sectors. With the global industrial automation market projected to exceed $400 billion by 2027, demand for high-accuracy force measurement devices has intensified. Modern static load cells, capable of measuring forces up to 1,000 kN with ±0.1% accuracy, are becoming indispensable in automated production lines. Technological advancements such as wireless data transmission and self-diagnostic capabilities are further enhancing their adoption in smart factories. The automotive sector alone accounts for nearly 30% of total industrial static load cell applications, primarily for component testing and quality control.

Other Trends

Miniaturization and High-Precision Applications

The rising demand for micro-force measurement in electronics and medical device manufacturing is driving innovation in compact static load cell designs. Below 10N capacity models are witnessing 12% annual growth, fueled by needs in semiconductor wafer handling and micro-surgical tool calibration. Manufacturers are developing strain-gauge based models with resolution down to 0.01N while maintaining IP67 protection ratings for harsh environments. This trend aligns with the expansion of nanotechnology research budgets, which have grown 18% year-over-year in major economies.

Material Science Breakthroughs Enhancing Performance

Emerging composite materials are significantly improving static load cell performance characteristics. Nanocomposite strain elements demonstrate 40% better fatigue life compared to traditional alloy-based designs while maintaining temperature stability within ±0.01% FSO from -10°C to 60°C. These advancements are particularly impactful in offshore and aerospace applications where environmental factors traditionally limited measurement accuracy. Simultaneously, the adoption of corrosion-resistant coatings has extended operational lifespans by 2-3 years in chemical processing installations, reducing total cost of ownership.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Precision Drive Competition in the Static Load Cell Market

The global static load cell market exhibits a moderately consolidated structure, with established industrial leaders competing alongside specialized manufacturers. Instron, a division of Illinois Tool Works Inc., dominates the sector with approximately 18% revenue share in 2024, owing to its comprehensive testing solutions and proprietary technology like Bluehill Universal software integration.

HBK (Hottinger Brüel & Kjær) and Siemens collectively hold nearly 25% market share, benefiting from their robust distribution networks and continuous advancements in measurement accuracy. HBK’s recent launch of the C18 load cell series with 0.02% accuracy has particularly strengthened its position in aerospace and automotive testing applications.

While larger players focus on high-capacity load cells for industrial applications, niche manufacturers like X-SENSORS and Changzhou Right are gaining traction in the Below 10N segment, which is projected to grow at 6.3% CAGR through 2032. This underscores the market’s bifurcation between heavy-duty industrial solutions and precision micro-force measurement systems.

Strategic movements in the sector include ADMET‘s 2023 acquisition of Gotech Testing Machines, expanding its Asian footprint, while Wuhan Sinorock has doubled its production capacity to meet growing demand from China’s infrastructure sector. Such developments indicate intensifying competition across regional markets and application segments.

List of Key Static Load Cell Manufacturers Profiled

- Instron (U.S.)

- Siemens (Germany)

- ADMET (U.S.)

- GRL Engineers (India)

- HBK (Germany)

- X-SENSORS (Germany)

- Wuhan Sinorock (China)

- Changzhou Right (China)

- Mettler Toledo (Switzerland)

Segment Analysis:

By Type

Below 10N Segment Expands Due to Rising Miniaturization Needs in Electronics & Automation

The market is segmented based on type into:

- Below 10N

- 10N to 100N

- Above 100N

By Application

Tension Test Application Dominates Market With Widespread Use in Material Strength Testing

The market is segmented based on application into:

- Tension Test

- Compression Test

- Cyclic Test

- Reverse Stress Test

- Others

By End User

Industrial Manufacturing Leads Market Share Owing to Heavy Usage in Quality Control Applications

The market is segmented based on end user into:

- Aerospace & Defense

- Automotive

- Construction

- Industrial Manufacturing

- Others

Regional Analysis: Static Load Cell Market

North America

The North American market for static load cells is driven by stringent industrial standards and the increasing adoption of automation across manufacturing and logistics sectors. The U.S. dominates due to significant demand from aerospace, automotive, and construction industries, with a strong emphasis on high-precision measurement solutions. Investments in infrastructure projects, particularly under initiatives like the Infrastructure Investment and Jobs Act, further stimulate market growth. However, competition from Asian manufacturers offering cost-effective alternatives creates pricing pressures. Key players such as Instron and HBK maintain technological leadership through continuous R&D in strain gauge-based sensors and digital load cell innovations.

Europe

Europe’s market is characterized by advanced industrial applications and strict regulatory frameworks ensuring product accuracy and reliability. Countries like Germany and France lead in deploying static load cells for automotive testing and renewable energy projects. The region prioritizes sustainability, fostering demand for energy-efficient load cells with minimal environmental impact. Collaboration between academic institutions and manufacturers accelerates adoption of smart load cells with IoT integration. Nonetheless, high production costs and market saturation in Western Europe pose challenges. Key competitors include Siemens and X-SENSORS, which specialize in customized solutions for niche applications.

Asia-Pacific

Asia-Pacific is the fastest-growing market, fueled by rapid industrialization in China, India, and Japan. The region benefits from extensive manufacturing hubs requiring high-volume load cells for quality control in electronics and heavy machinery. Cost competitiveness drives demand for entry-level load cells, though premium segments are expanding due to stricter quality norms. China’s dominance is reinforced by local players like Wuhan Sinorock, offering economical alternatives. However, intellectual property concerns and inconsistent standardization across countries create fragmented growth. Infrastructure development and automation trends in Southeast Asia present untapped opportunities for market penetration.

South America

The South American market exhibits moderate growth, with Brazil and Argentina as primary adopters in agriculture and mining sectors. Economic instability and reliance on imports limit local manufacturing capabilities, but the rise of small-scale industries boosts demand for affordable load cells. Governments’ focus on infrastructure modernization could drive future investments, though currency fluctuations and logistical inefficiencies remain barriers. Partnerships with global suppliers are critical to bridging technology gaps and improving after-sales support in the region.

Middle East & Africa

This region presents a mixed landscape, with Gulf nations like Saudi Arabia and the UAE leading in oil & gas applications, where load cells are used in drilling and refining processes. Infrastructure projects in Qatar and Egypt contribute to steady demand. Africa’s market is nascent but holds promise with mining and construction activities in South Africa and Nigeria. Challenges include limited domestic production and reliance on foreign suppliers. Long-term growth hinges on economic diversification and industrial policy reforms.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Static Load Cell markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Static Load Cell market was valued at US$ 1.12 billion in 2024 and is projected to reach US$ 1.73 billion by 2032, growing at a CAGR of 6.4%.

- Segmentation Analysis: Detailed breakdown by product type (Below 10N, 10N to 100N, Above 100N), application (Tension Test, Compression Test, Cyclic Test, Reverse Stress Test), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America (26% market share), Europe (22%), Asia-Pacific (38%), Latin America (8%), and Middle East & Africa (6%), including country-level analysis.

- Competitive Landscape: Profiles of leading market participants including Instron, Siemens, HBK, and ADMET, covering their product portfolios, market share (top 5 players hold 42% share), and strategic developments.

- Technology Trends & Innovation: Assessment of emerging load cell technologies, integration with Industry 4.0 systems, and advancements in measurement accuracy (±0.03% typical for premium models).

- Market Drivers & Restraints: Evaluation of automation growth (industrial automation market growing at 8.9% CAGR) versus challenges like raw material price volatility (stainless steel prices fluctuated 12-18% in 2023).

- Stakeholder Analysis: Strategic insights for OEMs, testing equipment manufacturers, industrial automation providers, and investors regarding market opportunities.

Research methodology incorporates primary interviews with 35+ industry experts, analysis of 120+ product specifications, and validation through trade data from customs databases and industry associations.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Static Load Cell Market?

-> Static Load Cell Market size was valued at US$ 1.12 billion in 2024 and is projected to reach US$ 1.73 billion by 2032, at a CAGR of 6.4% during the forecast period 2025-2032.

Which key companies operate in Global Static Load Cell Market?

-> Key players include Instron, Siemens, ADMET, HBK, GRL Engineers, X-SENSORS, Wuhan Sinorock, and Changzhou Right, with the top five holding 42% market share.

What are the key growth drivers?

-> Key growth drivers include industrial automation expansion, quality control requirements in manufacturing, and infrastructure development projects globally.

Which region dominates the market?

-> Asia-Pacific dominates with 38% market share, driven by China’s manufacturing growth, while North America leads in technological advancements.

What are the emerging trends?

-> Emerging trends include wireless load cell integration, smart factory compatibility, and miniaturization for portable testing equipment.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...