MARKET INSIGHTS

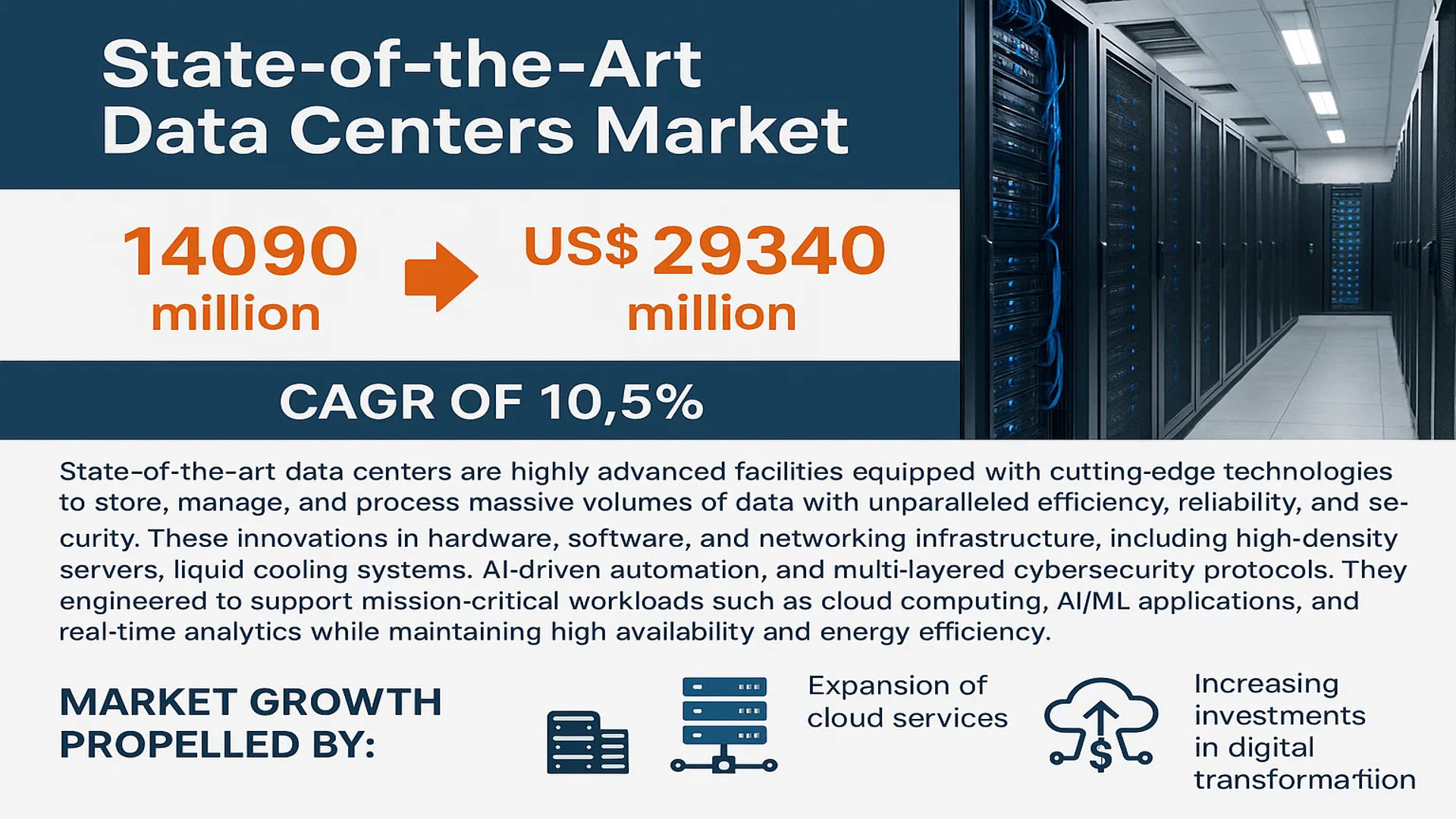

The global State-of-the-Art Data Centers Market was valued at 14090 million in 2024 and is projected to reach US$ 29340 million by 2032, at a CAGR of 10.5% during the forecast period.

State-of-the-art data centers are highly advanced facilities equipped with cutting-edge technologies to store, manage, and process massive volumes of data with unparalleled efficiency, reliability, and security. These data centers integrate innovations in hardware, software, and networking infrastructure, including high-density servers, liquid cooling systems, AI-driven automation, and multi-layered cybersecurity protocols. They are engineered to support mission-critical workloads such as cloud computing, AI/ML applications, and real-time analytics while maintaining high availability and energy efficiency.

The market growth is propelled by escalating demand for hyperscale computing, expansion of cloud services, and increasing investments in digital transformation. Notably, the hyperscale data center segment is anticipated to dominate the market, driven by surging requirements from tech giants and enterprises scaling their IT infrastructure. Key players like Dell, HPE, Cisco, and NVIDIA are advancing the market through innovations in server architecture, GPUs, and energy-efficient solutions, further accelerating industry adoption.

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth of Cloud Computing and AI to Accelerate Data Center Demand

The rapid adoption of cloud computing technologies and artificial intelligence applications is fundamentally transforming the global technology landscape, directly fueling demand for state-of-the-art data centers. Cloud service providers continue to expand their infrastructure footprint globally to meet escalating demand, with hyperscale data center count increasing by over 100 facilities in just the past two years. The AI revolution further intensifies this need, as advanced machine learning models require specialized high-performance computing infrastructure. Large language model training demands alone have driven a 10-30x increase in computing requirements compared to traditional workloads, necessitating data centers with advanced cooling solutions and power densities exceeding 50kW per rack.

5G Network Rollouts Creating New Edge Computing Opportunities

The global deployment of 5G networks is creating unprecedented opportunities for edge data centers, with projections indicating the edge computing market will grow at a compound annual rate exceeding 30% through 2030. Edge facilities reduce latency for critical applications like autonomous vehicles, industrial IoT, and augmented reality by processing data closer to end-users. Telecommunication providers are aggressively investing in micro data centers at network edges, with several major carriers announcing deployments of hundreds to thousands of edge nodes annually. This infrastructure evolution supports real-time processing needs while complementing centralized hyperscale facilities.

Sustainability Initiatives Driving Green Data Center Innovations

Environmental concerns and corporate sustainability goals are accelerating investments in energy-efficient data center technologies. Leading operators now achieve power usage effectiveness (PUE) ratings below 1.1 through advanced cooling techniques like liquid immersion and direct-to-chip cooling systems. Renewable energy adoption in data centers has grown over 50% in three years, with hyperscalers committing to 100% renewable operations. Regulatory pressure continues mounting, with new energy efficiency standards emerging across major markets, further incentivizing operators to upgrade or replace legacy facilities with state-of-the-art alternatives featuring superior environmental performance.

MARKET CHALLENGES

Power Availability Constraints Threatening Expansion Plans

The data center industry faces growing challenges securing adequate power capacity for new facilities, particularly in major metropolitan areas. Rising power demands from high-density computing combined with aging electrical infrastructure create bottlenecks, with some regions reporting delays of 2-4 years for new power connections. This power crunch has become so severe that certain markets have implemented temporary moratoriums on new data center construction until grid upgrades are completed. The situation is further complicated by competing demands from electric vehicle charging infrastructure and industrial electrification initiatives.

Other Challenges

Supply Chain Disruptions

Critical equipment lead times have extended dramatically, with some transformer and switchgear deliveries now exceeding 60 weeks compared to historical norms of 12-16 weeks. These delays stem from global semiconductor shortages, transportation bottlenecks, and raw material constraints that continue plaguing the construction sector.

Workforce Shortages

The specialized nature of modern data center operations has created severe talent shortages, with estimates suggesting the industry needs to fill nearly 300,000 additional positions globally by 2025. This skills gap covers everything from electrical engineers and cooling specialists to cybersecurity experts and AI infrastructure architects.

MARKET RESTRAINTS

Regulatory Complexity Creating Implementation Hurdles

Data center operators face an increasingly complex web of regulations spanning energy use, water consumption, noise ordinances, and land use policies. Jurisdictional variations create compliance challenges for multi-market operators, with some regions imposing strict limits on water usage for cooling while others restrict outdoor equipment noise levels. The regulatory landscape continues evolving rapidly, with new sustainability reporting requirements and carbon disclosure mandates adding operational overhead. These compliance burdens frequently delay projects and increase capital expenditure requirements, particularly for retrofitting existing facilities to meet contemporary standards.

Construction and Land Acquisition Costs Pressuring Profitability

Development costs for state-of-the-art data centers have increased 20-30% over the past three years due to rising construction material prices, labor costs, and land values in strategic locations. Prime data center markets near major network hubs command land prices up to 300% higher than comparable industrial properties. These cost pressures squeeze operator margins and extend return-on-investment timelines, particularly for facilities designed to support smaller-scale edge computing deployments where economies of scale are less pronounced.

MARKET OPPORTUNITIES

Emerging Markets Offering Untapped Growth Potential

Secondary and tertiary markets present compelling expansion opportunities as enterprises seek geographic diversity for disaster recovery and latency optimization. Regions with favorable climate conditions for free cooling, renewable energy availability, and supportive regulatory environments are attracting developer interest. Southeast Asia, Latin America, and parts of Africa demonstrate particularly strong potential, with internet penetration and cloud adoption rates climbing rapidly. Several hyperscalers have announced plans to establish new cloud regions in these emerging markets, which will drive accompanying data center investments.

AI-Specific Infrastructure Creating Specialization Niches

The artificial intelligence boom is spawning demand for specialized data center configurations optimized for machine learning workloads. These facilities require unique power distribution architectures, liquid cooling solutions, and ultra-high-speed networking capabilities. This specialization creates opportunities for operators to develop premium-priced AI-ready infrastructure while differentiating their service offerings. Early movers in this space report achieving 15-20% pricing premiums compared to traditional colocation services while maintaining occupancy rates exceeding 90%.

Modular and Prefabricated Solutions Gaining Traction

Prefabricated modular data centers are emerging as a compelling solution for rapid deployment and scalability challenges. These factory-built units can be deployed in weeks rather than months, with some designs supporting power densities up to 100kW per rack. The modular approach offers particular advantages for edge computing deployments and temporary capacity expansions, with adoption rates growing at approximately 25% annually. This segment represents an increasingly important growth channel for equipment manufacturers and service providers alike.

STATE-OF-THE-ART DATA CENTERS MARKET TRENDS

Hyperscale Data Centers Dominate Due to Cloud and AI Expansion

The hyperscale data center segment is leading market growth, driven by the rapid adoption of cloud computing and artificial intelligence workloads. Global hyperscale data center investments reached $220 billion in 2023 as enterprises increasingly migrate to multi-cloud environments. Major providers are deploying liquid cooling solutions to address the extreme power densities of AI server racks—some consuming over 50 kW per cabinet. Furthermore, modular designs with prefabricated components now reduce deployment times by 60% compared to traditional builds. Edge computing proliferation complements this growth, requiring hyperscale operators to decentralize infrastructure while maintaining centralized management.

Other Trends

Sustainability Becomes a Strategic Imperative

Energy efficiency innovations are reshaping data center design, with average Power Usage Effectiveness (PUE) ratios improving to 1.55 in 2024 from 1.67 five years prior. Operators increasingly adopt renewable energy power purchase agreements (PPAs), accounting for 35% of hyperscale energy sourcing. Waste heat recycling systems—now operational in 12% of Northern European facilities—are gaining traction as regulatory pressures intensify. The EU’s Energy Efficiency Directive mandates a maximum PUE of 1.3 by 2027, accelerating the retrofit of legacy infrastructure with AI-driven cooling optimization and lithium-ion battery backups.

AI and 5G Drive Architectural Reinvention

The convergence of AI inferencing and 5G networks necessitates ultra-low latency architectures, spurring investments in edge data centers forecasted to grow at 22% CAGR through 2030. NVIDIA’s Grace Hopper superchips and AMD’s Instinct accelerators are prompting facility redesigns to support 400Gbps+ interconnects and pooled GPU resources. Simultaneously, cybersecurity investments now constitute 18% of data center capex, up from 11% in 2020, as zero-trust architectures require specialized hardware security modules. This technological arms race is compressing refresh cycles—leading vendors now introduce server upgrades every 12-18 months versus the traditional 3-5 year timeline.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Technology Giants and Infrastructure Providers Drive Market Innovation

The global state-of-the-art data centers market is characterized by intense competition among established technology companies, infrastructure providers, and emerging innovators. Dell Technologies and Hewlett Packard Enterprise (HPE) dominate the market with their comprehensive data center solutions, which include advanced server architectures, storage systems, and hybrid cloud capabilities. Their strong brand recognition and extensive customer base across enterprises and hyperscalers reinforce their leadership position.

Meanwhile, Cisco Systems and NVIDIA are rapidly gaining market share with their specialized offerings. Cisco’s networking expertise and NVIDIA’s AI-optimized GPU infrastructure are becoming increasingly critical for modern data centers, especially those supporting machine learning workloads. These companies are accelerating innovation through strategic partnerships—for instance, NVIDIA’s collaborations with major cloud providers to deploy AI-ready data center solutions.

On the hardware front, Intel and AMD remain pivotal due to their high-performance processors designed for data center workloads. Their continuous R&D investments in energy-efficient chips are addressing the growing demand for sustainable computing. Meanwhile, storage specialists like Seagate and Western Digital are expanding their footprint with next-gen solutions for high-density data storage, which is vital for hyperscale operators.

The competitive intensity is further amplified by infrastructure providers such as Vertiv and Schneider Electric, which offer critical power and cooling solutions. Their energy-efficient designs are helping data centers reduce operational costs while meeting stringent environmental regulations. Additionally, network security players like Palo Alto Networks and Fortinet are becoming indispensable as cybersecurity threats grow in complexity.

List of Key State-of-the-Art Data Center Companies Profiled

- Dell Technologies (U.S.)

- Hewlett Packard Enterprise (HPE) (U.S.)

- Cisco Systems (U.S.)

- NVIDIA Corporation (U.S.)

- Intel Corporation (U.S.)

- Advanced Micro Devices (AMD) (U.S.)

- Seagate Technology (U.S.)

- Western Digital (U.S.)

- Supermicro (U.S.)

- Vertiv Holdings (U.S.)

- Fortinet (U.S.)

- Arista Networks (U.S.)

- Juniper Networks (U.S.)

- Palo Alto Networks (U.S.)

- Extreme Networks (U.S.)

- Schneider Electric (France)

- QNAP Systems (Taiwan)

- Samsung Electronics (South Korea)

- Huawei Technologies (China)

- Lenovo Group (China)

Segment Analysis:

By Type

Hyperscale Data Centers Lead the Market with Their Scalability and Cost Efficiency

The market is segmented based on type into:

- Hyperscale Data Centers

- Subtypes: Cloud-based and enterprise-based

- Edge Data Centers

- Subtypes: Modular and micro data centers

- Colocation Data Centers

- Subtypes: Retail and wholesale colocation

- Others

By Application

IT & Telecom Sector Dominates Adoption Due to Rising Cloud Computing and 5G Requirements

The market is segmented based on application into:

- IT & Telecom

- BFSI

- Healthcare

- Retail & eCommerce

- Autonomous Vehicles

- Manufacturing

- Others

By Technology

Liquid Cooling Technology Gains Traction for Energy-Efficient Operations

The market is segmented based on technology into:

- Air Cooling

- Liquid Cooling

- Subtypes: Immersion and direct-to-chip cooling

- Free Cooling

- Others

By Ownership

Enterprise-Owned Data Centers Show Significant Growth for Customized Solutions

The market is segmented based on ownership into:

- Enterprise-Owned

- Cloud Service Providers

- Colocation Providers

- Others

Regional Analysis: State-of-the-Art Data Centers Market

North America

North America dominates the global State-of-the-Art Data Centers market, primarily driven by the U.S., which accounts for the largest share of hyperscale data center deployments. The region benefits from substantial investments in cloud computing, AI infrastructure, and 5G networks, with tech giants like Amazon, Google, and Microsoft leading the expansion. Stringent data security regulations, including GDPR compliance for international operations and CCPA for domestic data privacy, have accelerated the adoption of advanced cybersecurity measures in data centers. The growing demand for edge computing, particularly in autonomous vehicles and IoT applications, is further fueling market growth. Energy-efficient designs, such as liquid cooling and renewable energy integration, are gaining traction due to sustainability initiatives.

Europe

Europe’s State-of-the-Art Data Centers market is characterized by robust growth in colocation and hyperscale facilities, particularly in Germany, the UK, and the Nordic countries. The region’s focus on green data centers, supported by EU directives on energy efficiency and carbon neutrality, has driven innovation in cooling technologies and renewable energy adoption. Countries like Iceland and Sweden are emerging as attractive locations due to their naturally cool climates and access to hydroelectric and geothermal power. The implementation of the EU Data Strategy and upcoming digital sovereignty initiatives are expected to create opportunities for localized data center solutions. However, land scarcity in urban hubs and complex permitting processes remain key challenges.

Asia-Pacific

The Asia-Pacific region is experiencing the fastest growth in State-of-the-Art Data Centers, with China, India, Japan, and Singapore as primary markets. China’s digital economy expansion and government support for 5G and AI development have spurred massive hyperscale data center investments. India is witnessing a surge in demand due to rapid digital transformation across banking, e-commerce, and government services. Southeast Asian markets are growing as regional hubs, though they face challenges in power infrastructure stability. Japan and South Korea continue to lead in technological sophistication, particularly in high-density computing and disaster-resilient designs. The region’s diversity creates both opportunities for localization and challenges in standardizing operations.

South America

South America’s State-of-the-Art Data Centers market is in a growth phase, with Brazil and Chile emerging as regional hubs. Increasing cloud adoption by enterprises and government digitalization programs are driving demand, though the market remains heavily concentrated in major cities. Limited domestic hyperscale providers have created opportunities for international operators, particularly in the colocation segment. Challenges include inconsistent power infrastructure, complex tax structures, and limited availability of skilled personnel. The growing fintech sector and increasing cross-border data requirements are expected to accelerate market development in coming years.

Middle East & Africa

The Middle East & Africa region shows promising growth potential for State-of-the-Art Data Centers, led by UAE, Saudi Arabia, and South Africa. Gulf countries are positioning themselves as regional data hubs through strategic initiatives like UAE’s Digital Government Strategy and Saudi Vision 2030. The region benefits from substantial investments in digital infrastructure and increasing adoption of cloud services. Africa’s market is more fragmented, with growth concentrated in major economies and driven by mobile money services and improving internet penetration. While power reliability and connectivity constraints persist, the development of carrier-neutral facilities and submarine cable connections are addressing these limitations over time.

Report Scope

This market research report provides a comprehensive analysis of the global State-of-the-Art Data Centers market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 14.09 billion in 2024 and is projected to reach USD 29.34 billion by 2032, growing at a CAGR of 10.5%.

- Segmentation Analysis: Detailed breakdown by type (Hyperscale, Edge, Colocation), application (IT & Telecom, BFSI, Healthcare, etc.), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants including Dell, HPE, Cisco, NVIDIA, Intel, AMD, and Schneider Electric, covering their product portfolios, R&D focus, and strategic developments.

- Technology Trends & Innovation: Assessment of AI integration, advanced cooling solutions, energy-efficient designs, and cybersecurity enhancements in modern data centers.

- Market Drivers & Restraints: Evaluation of cloud computing adoption, 5G deployment, and AI demand versus challenges like high capital expenditure and energy consumption.

- Stakeholder Analysis: Strategic insights for data center operators, cloud service providers, hardware manufacturers, and investors navigating this dynamic market.

Primary and secondary research methods are employed, including interviews with industry experts and analysis of verified market data, to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global State-of-the-Art Data Centers Market?

-> State-of-the-Art Data Centers Market was valued at 14090 million in 2024 and is projected to reach US$ 29340 million by 2032, at a CAGR of 10.5% during the forecast period.

Which key companies operate in Global State-of-the-Art Data Centers Market?

-> Key players include Dell, HPE, Cisco, NVIDIA, Intel, AMD, Schneider Electric, Vertiv, and Huawei, among others.

What are the key growth drivers?

-> Key growth drivers include cloud computing adoption, AI/ML workloads, 5G deployment, and increasing data generation.

Which region dominates the market?

-> North America currently leads the market, while Asia-Pacific is experiencing the fastest growth.

What are the emerging trends?

-> Emerging trends include liquid cooling solutions, AI-optimized infrastructure, edge computing deployment, and sustainable data center designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...