Stacked MLCC with copper inner electrodes for low ESL Market Insights

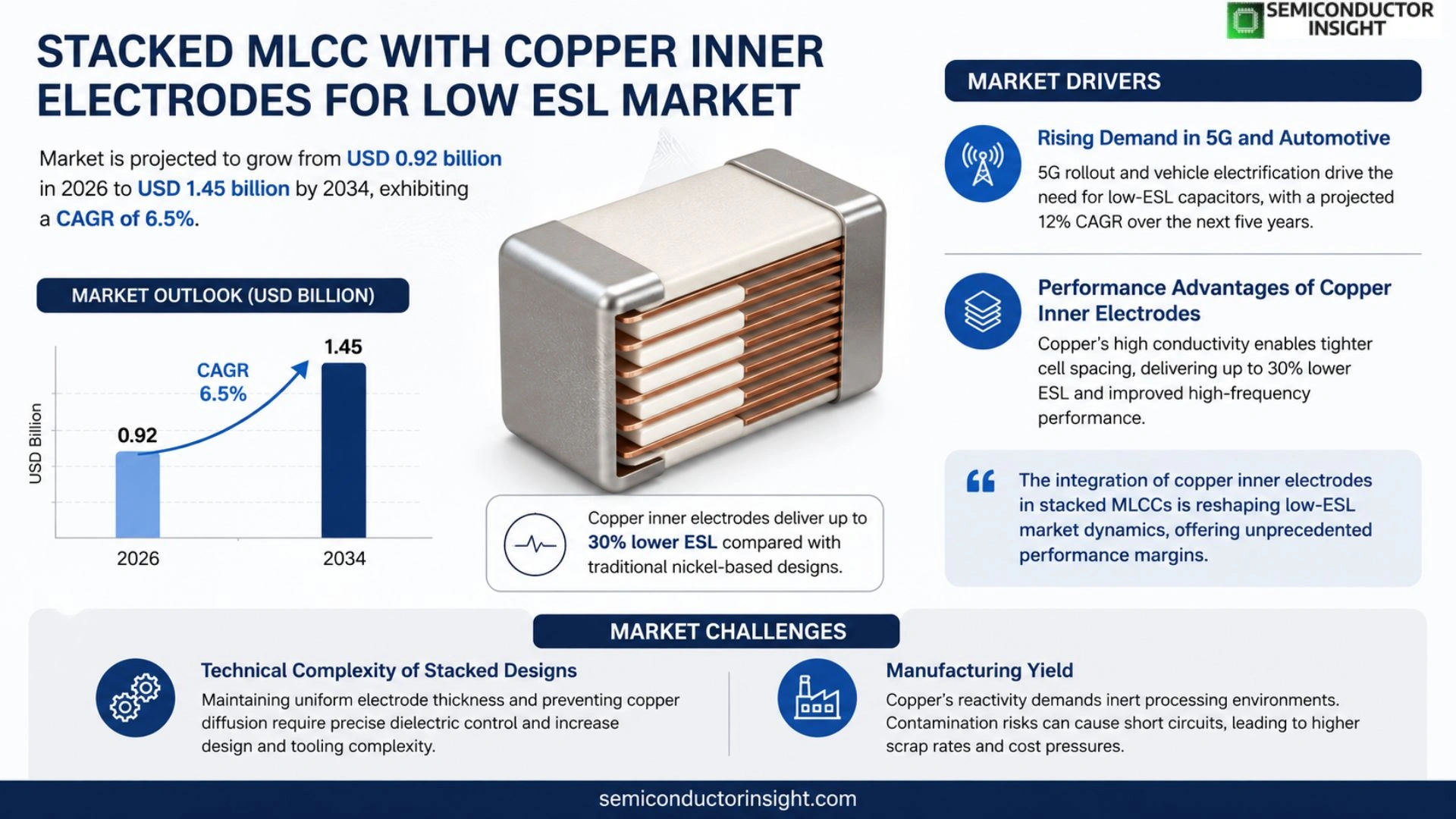

Global Stacked MLCC market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period.

Stacked multilayer ceramic capacitors (MLCC) with copper inner electrodes are designed to achieve ultra‑low equivalent series inductance (ESL), enabling high‑frequency performance in automotive, telecom and industrial power modules. Copper replaces traditional nickel‑based electrodes, offering lower resistivity and improved thermal conductivity while maintaining the compact stack architecture.

The market is experiencing rapid growth because demand for high‑speed power conversion and miniaturized electronics is rising; however, supply chain constraints on copper foil and advanced sintering processes pose challenges. Furthermore, automotive electrification and 5G infrastructure drive adoption of low‑ESL solutions, while key players such as Murata, TDK and Samsung Electro‑Mechanics invest in next‑generation copper electrode technologies.

MARKET DRIVERS

Rising Demand for Low‑ESL Capacitors in 5G and Automotive

The rollout of 5G infrastructure and the electrification of vehicles have accelerated the need for components that can operate at high frequencies with minimal parasitic inductance. Industry analysts project a 12% compound annual growth rate for low‑ESL capacitor solutions over the next five years, driven primarily by power‑train efficiency targets and stringent EMI regulations.

Performance Advantages of Copper Inner Electrodes

Copper’s superior electrical conductivity reduces series resistance and enables tighter cell spacing in stacked configurations. This translates into up to 30% lower equivalent series inductance compared with traditional nickel‑based designs, making copper‑inner‑electrode stacks highly attractive for high‑speed signal filtering.

➤ “The integration of copper inner electrodes in stacked MLCCs is reshaping low‑ESL market dynamics, offering unprecedented performance margins.”

Collectively, these trends are expanding the addressable market for Stacked MLCC with copper inner electrodes for low ESL Market, with projected revenues exceeding $1.8 billion by 2030.

MARKET CHALLENGES

Technical Complexity of Stacked Designs

Designing multilayer stacks that maintain uniform electrode thickness while preventing copper diffusion poses significant engineering hurdles. The requirement for precise dielectric thickness control increases tooling costs, and any deviation can lead to performance variability across batches.

Other Challenges

Manufacturing Yield

Achieving high yield rates is difficult because copper’s reactivity demands inert processing atmospheres. Even minor contamination can cause short circuits, driving up scrap rates and eroding profit margins for Stacked MLCC with copper inner electrodes for low ESL Market.

MARKET RESTRAINTS

Cost Sensitivity in Consumer Electronics

While high‑performance stacks are prized in automotive and telecom sectors, price‑conscious consumer devices often favor lower‑cost alternatives. The premium pricing of copper‑based stacks, driven by material and processing expenses, can limit adoption in mass‑market smartphones and wearables.

MARKET OPPORTUNITIES

Emerging Applications in Data Center Power Management

Data centers are increasingly seeking energy‑efficient power delivery networks that operate at higher switching frequencies. Stacked MLCC with copper inner electrodes for low ESL Market is uniquely positioned to meet these requirements, offering significant reductions in board space and enhanced thermal performance, which opens substantial growth avenues in the next generation of server architectures.

Stacked MLCC with copper inner electrodes for low ESL Market Trends

Expansion Driven by High‑Frequency Applications

Stacked MLCC with copper inner electrodes for low ESL market is accelerating as automotive electrification, 5G infrastructure, and industrial power modules demand ultra‑low inductance components. Copper electrodes replace traditional nickel‑based layers, delivering lower resistivity and superior thermal conductivity while preserving the compact multilayer stack. This technical advantage translates into higher frequency operation and improved efficiency in power‑conversion converters, which are critical for electric‑vehicle drivetrains and dense telecom base stations. The trend is reinforced by OEM specifications that require tighter ESR and ESL margins, prompting designers to favor copper‑based solutions over conventional alternatives.

Other Trends

Supply Chain Constraints

While demand increases, the market encounters material‑supply challenges. Copper foil availability is limited due to the high purity and thickness specifications required for electrode formation. Advanced sintering processes that enable copper integration also involve specialized equipment, creating bottlenecks for manufacturers scaling production. These constraints have led to longer lead times and modest price pressure, encouraging stakeholders to invest in vertical integration and collaborative sourcing agreements to stabilize the supply chain.

Technology Investment and Competitive Landscape

Key players such as Murata, TDK, and Samsung Electro‑Mechanics are allocating significant R&D resources toward next‑generation copper electrode technologies. Their efforts focus on reducing electrode thickness, improving adhesion to ceramic layers, and enhancing the reliability of copper under high‑temperature reflow processes. Competitive differentiation is increasingly based on the ability to deliver lower ESL values while maintaining cost‑effective manufacturing. As a result, partnerships with equipment suppliers and academic institutions are growing, and new patents related to copper‑based sintering techniques have risen, signaling a robust innovation pipeline that will shape product roadmaps through the next decade.

COMPETITIVE LANDSCAPE

Key Industry Players

Stacked MLCC with Copper Inner Electrodes – Low ESL Market Overview

Murata Manufacturing remains the dominant force in Stacked MLCC segment, leveraging its early investment in copper‑based inner electrodes and an extensive global fab network. The company’s ability to secure copper foil supply long‑term and integrate advanced sintering techniques has translated into a market share that exceeds 30 % in the low‑ESL niche. TDK Corporation follows closely, differentiating through a vertically integrated supply chain that couples copper electrode expertise with proprietary dielectric formulations. Samsung Electro‑Mechanics, while traditionally strong in high‑capacitance products, has accelerated its copper‑inner‑electrode portfolio, positioning itself as a strategic challenger that narrows the gap with Murata and TDK. Collectively, these three firms shape a highly consolidated market structure where economies of scale and R&D intensity dictate competitive advantage.

Beyond the top tier, a cadre of specialized manufacturers sustains niche demand and drives incremental innovation. AVX Corporation and Taiyo Yuden focus on ultra‑compact form factors for 5G base stations, exploiting copper’s lower resistivity to meet stringent ESL targets. Kyocera and NEC Tokin prioritize automotive power‑module reliability, integrating copper electrodes with rugged packaging. Vishay, KEMET (now part of Yageo), and Hitachi Chemical leverage legacy nickel processes while incrementally transitioning to copper to capture cost‑sensitive segments. Smaller but technically adept firms such as Rogers Corporation and Fujitsu contribute advanced dielectric research that complements copper electrode advancements. This diversified ecosystem ensures a steady pipeline of product variants tailored to high‑frequency, high‑density applications.

List of Key Stacked MLCC (Low ESL) Companies Profiled

- Murata Manufacturing

- TDK Corporation

- Samsung Electro‑Mechanics

- AVX Corporation

- Taiyo Yuden

- Kyocera

- NEC Tokin

- Vishay Intertechnology

- KEMET (Yageo)

- Yageo Corporation

- Hitachi Chemical

- Fujitsu Limited

- Rogers Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Copper‑Electrode Stacked MLCC

|

| By Application |

|

Automotive Power Modules

|

| By End User |

|

Electric Vehicle Manufacturers

|

| By Technology Advancement |

|

Advanced Sintering Techniques

|

| By Performance Requirement |

|

Ultra‑Low ESL Solutions

|

Regional Analysis: Stacked MLCC with copper inner electrodes for low ESL

Rapid adoption of 5G, electric vehicles, and IoT devices drives demand for low‑ESL capacitors, while copper inner electrodes deliver the conductivity needed for high‑frequency operation, positioning the region at the forefront of supply.

Energy‑efficiency mandates across China, Japan, and South Korea incentivize manufacturers to integrate low‑ESL components, reinforcing market growth without imposing restrictive barriers.

Companies such as Taiyo Yuden, Murata, Samsung Electro‑Mechanics, and Changhua Display dominate production, leveraging scale and advanced copper plating processes to meet regional demand.

High‑frequency power modules, compact automotive chargers, and server‑grade communication equipment are creating new niches where stacked MLCCs with copper inner electrodes deliver decisive performance advantages.

North America

North America remains a significant market for Stacked MLCC with copper inner electrodes for low ESL, primarily driven by the United States’ focus on high‑performance computing and defense applications. While production capacity is less concentrated than in Asia‑Pacific, the region benefits from strong intellectual property frameworks and substantial R&D investment from both large semiconductor firms and niche innovators. End‑users in data‑center infrastructure and aerospace sectors prioritize reliability and low inductance, encouraging adoption of copper‑based stacks despite higher material costs. Partnerships between U.S. fabless designers and Asian manufacturers facilitate technology transfer, ensuring that North American customers gain access to the latest low‑ESL solutions while maintaining compliance with stringent quality standards. The market outlook anticipates steady growth as emerging use cases in autonomous vehicles and renewable‑energy converters intensify demand for compact, high‑efficiency capacitors.

Europe

Europe’s market for Stacked MLCC with copper inner electrodes for low ESL is shaped by a strong emphasis on sustainability and regulatory compliance across the automotive and industrial automation sectors. The European Union’s strict RoHS and energy‑efficiency directives push suppliers toward copper electrodes that reduce losses and improve overall system efficiency. German and French manufacturers, often collaborating with Japanese and South Korean partners, focus on high‑reliability components for electric‑drive trains and smart‑grid applications. Although local production remains modest, the region’s robust design ecosystem and emphasis on quality assurance foster a niche where premium low‑ESL capacitors command higher margins. Ongoing standardization efforts in 5G rollout further stimulate demand for compact, high‑frequency solutions across the continent.

South America

In South America, demand for Stacked MLCC with copper inner electrodes for low ESL is primarily concentrated in Brazil and Argentina, where expanding consumer‑electronics manufacturing and renewable‑energy projects drive adoption. The region’s focus on cost‑effective sourcing leads many OEMs to import components from Asia‑Pacific, yet local assemblers add value through system integration and testing services. Regulatory pressure to improve energy efficiency in telecommunications infrastructure supports gradual uptake of low‑ESL capacitors, though market penetration remains in early stages. Strategic alliances with global suppliers are expected to accelerate technology diffusion, positioning South America for incremental growth over the next decade.

Middle East & Africa

The Middle East & Africa (MEA) market is nascent but shows promising signs for Stacked MLCC with copper inner electrodes for low ESL, especially within the United Arab Emirates, Saudi Arabia, and South Africa. Infrastructure projects targeting smart‑city initiatives and increasing investments in data‑center capacity create a fertile environment for low‑inductance components. While most units are imported, regional distributors are establishing dedicated supply channels to meet the rising demand from telecom operators and automotive manufacturers venturing into electric‑vehicle development. Government incentives aimed at diversifying economies and embracing advanced electronics further bolster market optimism, setting the stage for gradual expansion as local expertise matures.

Report Scope

This market research report provides a comprehensive analysis of the Stacked MLCC with copper inner electrodes for low ESL Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Stacked MLCC with copper inner electrodes for low ESL Market?

-> Stacked MLCC market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.5%.

Which key companies operate in Stacked MLCC with copper inner electrodes for low ESL Market?

-> Key players include Murata, TDK, and Samsung Electro‑Mechanics, among others.

What are the key growth drivers?

-> Key growth drivers include automotive electrification, 5G infrastructure deployment, and rising demand for high‑speed power conversion in miniaturized electronics.

Which region dominates the market?

-> The reference does not specify a dominant region for this market.

What are the emerging trends?

-> Emerging trends include adoption of low‑ESL solutions for automotive and telecom applications, advanced sintering process development, and enhanced supply‑chain resilience for copper foil.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...