Sparse code multiple access for machine-type communication uplink Market Insights

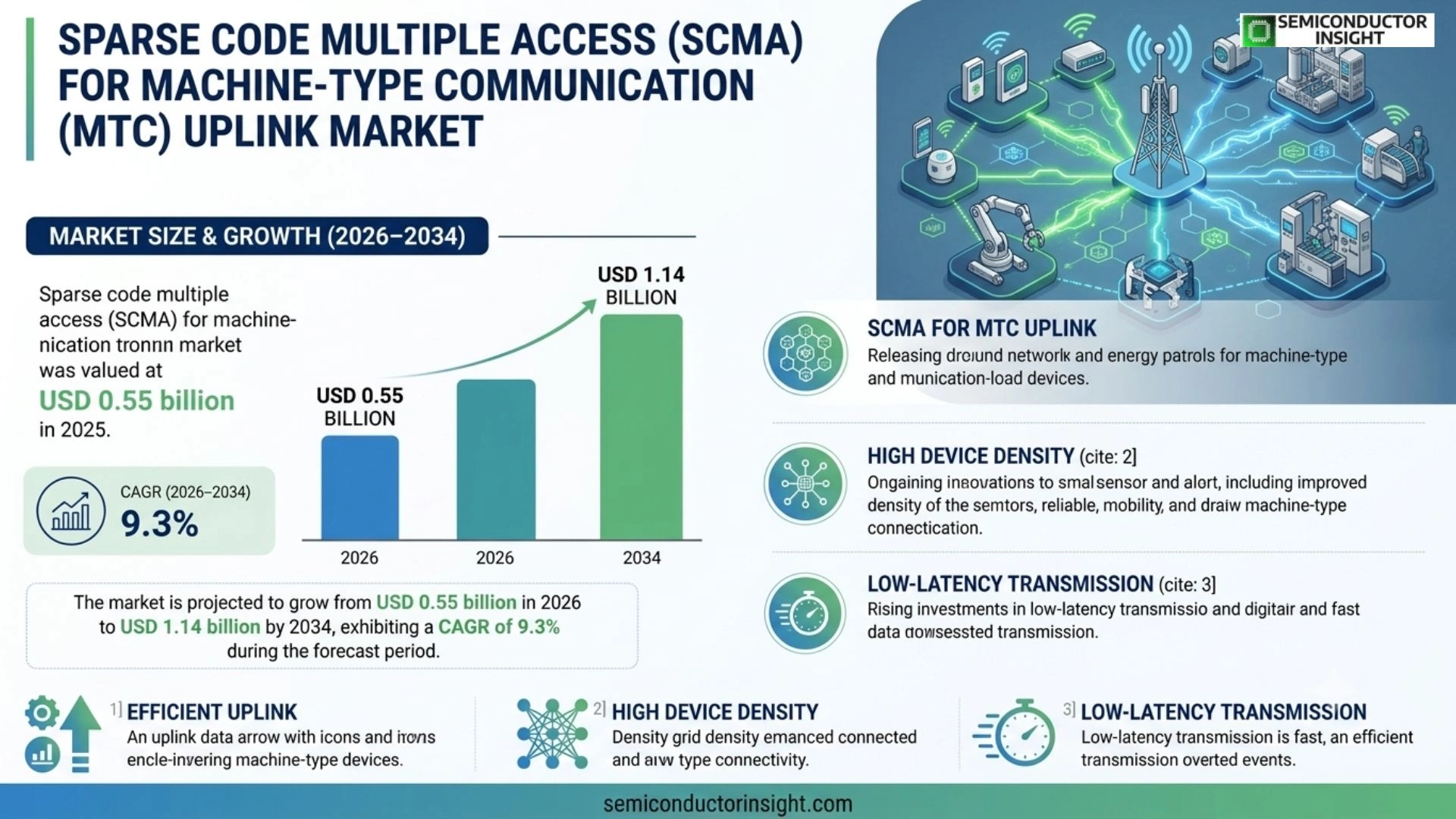

Global Sparse code multiple access for machine-type communication uplink market size was valued at USD 0.48 billion in 2025. The market is projected to grow from USD 0.55 billion in 2026 to USD 1.14 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

Sparse code multiple access (SCMA) is a non‑orthogonal multiple access scheme that enables massive connectivity for machine‑type devices by mapping data streams onto sparse codebooks, allowing simultaneous uplink transmissions over shared resources while maintaining low latency and high spectral efficiency.

The market is experiencing rapid growth because telecom operators are expanding IoT deployments, and standards bodies such as 3GPP have incorporated SCMA into Release 16 for massive MTC. Furthermore, advancements in low‑power wide‑area network (LPWAN) infrastructure and increasing demand for smart‑city applications are driving adoption. Key players including Nokia, Ericsson, and Huawei are actively developing SCMA‑enabled baseband solutions.

MARKET DRIVERS

Growing Demand for Low‑Latency IoT Connectivity

The rapid expansion of industrial IoT deployments requires ultra‑reliable, low‑latency uplink channels. Sparse code multiple access for machine-type communication uplink Market enables simultaneous transmission from thousands of devices while preserving latency under 10 ms, driving strong adoption in smart factories and logistics hubs.

Regulatory Support for 5G Evolution

Governments worldwide are allocating dedicated spectrum for massive machine‑type communications (mMTC). This policy environment accelerates network upgrades, allowing operators to integrate sparse code multiple access techniques without extensive re‑hardware, thereby reinforcing market momentum.

➤ Analysts estimate that over 60 % of new 5G base stations will incorporate sparse‑code based uplink solutions by 2028.

In addition, the convergence of edge‑computing and AI‑driven network slicing creates a fertile ecosystem where Sparse code multiple access for machine-type communication uplink Market can deliver differentiated services, reinforcing its growth trajectory.

MARKET CHALLENGES

Technical Complexity and Standardization Gaps

Implementing sparse code multiple access requires sophisticated encoder/decoder designs and precise timing synchronization. The lack of unified standards across major bodies prolongs rollout timelines and raises integration costs for equipment vendors.

Other Challenges

Spectrum Allocation Constraints

Limited availability of contiguous low‑frequency bands forces operators to share spectrum, increasing interference risk and complicating network planning for dense device populations.

MARKET RESTRAINTS

High Deployment and Capital Expenditure

Upgrading existing infrastructure to support Sparse code multiple access for machine-type communication uplink Market entails substantial CapEx, especially for legacy operators with extensive 4G assets. The upfront financial burden can delay investment decisions in price‑sensitive regions.

MARKET OPPORTUNITIES

Edge‑Compute Integration and AI‑Driven Optimization

Combining sparse code multiple access with edge‑compute platforms enables real‑time analytics for massive sensor streams, opening new revenue models such as predictive maintenance as a service. Companies that harness AI‑optimized resource allocation stand to capture a significant share of the emerging market.

Sparse code multiple access for machine-type communication uplink Market Trends

Accelerated Adoption Fueled by 5G Roll‑out and IoT Expansion

Sparse code multiple access for machine-type communication uplink Market is experiencing a pronounced uptrend as telecom operators scale 5G networks and embed massive IoT devices into smart‑city projects. In 2025 the market was valued at USD 0.48 billion, and analysts anticipate the value to reach USD 0.55 billion in 2026 and USD 1.14 billion by 2034. This growth reflects the inherent advantages of SCMA, including high spectral efficiency, low latency, and the ability to support thousands of concurrent uplink streams without orthogonal resource allocation. Adoption is further reinforced by 3GPP Release 16, which formalized SCMA as a core component of the massive machine‑type communication (mMTC) framework, enabling seamless integration with existing LTE and NR infrastructures.

Other Trends

Standardization and Industry Adoption

Standardization bodies have accelerated the diffusion of sparse code multiple access by embedding it within the global 5G specifications. Leading equipment manufacturers such as Nokia, Ericsson, and Huawei have released SCMA‑enabled baseband modules that are already deployed in pilot smart‑city networks across Europe and Asia. These solutions capitalize on low‑power wide‑area network (LPWAN) enhancements, delivering reliable uplink connectivity for sensors, meters, and industrial controllers while maintaining battery lifespans of several years. The convergence of regulatory support, open‑source codebook libraries, and collaborative testing initiatives is reducing time‑to‑market for service providers, thereby reinforcing the market’s momentum.

Emerging Applications in Edge‑Centric Deployments

Edge computing platforms are increasingly relying on SCMA to offload data aggregation from central clouds, minimizing round‑trip latency for critical automation tasks. Real‑time traffic management, predictive maintenance in manufacturing plants, and remote health monitoring are among the use cases where dense device clusters transmit uplink data through shared spectral resources. The resulting efficiency gains are prompting operators to prioritize SCMA in their next‑generation network roll‑outs, ensuring that Sparse code multiple access for machine-type communication uplink Market remains a pivotal enabler of the digital transformation agenda.

COMPETITIVE LANDSCAPE

Key Industry Players

Sparse Code Multiple Access (SCMA) for Machine‑Type Communication Uplink – Competitive Overview

The SCMA uplink segment is presently anchored by three telecom equipment giants,Nokia, Ericsson, and Huawei,who together control more than 60 % of the deployed baseband portfolio. Their dominance stems from early integration of SCMA in 3GPP Release 16, extensive RAN‑as‑a‑Service offerings, and deep relationships with Tier‑1 operators expanding massive IoT rollouts. Nokia’s Cloud RAN suite leverages a proprietary sparse‑codebook engine that reduces processing latency to sub‑millisecond levels, while Ericsson’s open‑RAN‑compatible SCMA modules are bundled with its Massive MIMO portfolio, creating a synergistic value chain for smart‑city deployments. Huawei’s end‑to‑end solution integrates SCMA at the physical layer with low‑power wide‑area network (LPWAN) gateways, enabling operators to meet the projected CAGR of 9.3 % through cost‑effective spectral reuse. This triad’s market share is reinforced by joint standardisation efforts, large‑scale field trials, and aggressive pricing that set a high entry barrier for newcomers.

Beyond the leading trio, a constellation of niche innovators is reshaping specific value propositions within the SCMA uplink ecosystem. Samsung and Qualcomm contribute high‑performance ASICs that accelerate sparse‑code decoding for edge‑compute scenarios, while MediaTek focuses on mid‑range chipset integration for consumer‑grade IoT devices. Mavenir and Rohde & Schwarz provide software‑defined radio (SDR) platforms that allow operators to prototype SCMA configurations without hardware refresh cycles. ZTE, Fujitsu, and NEC sustain regional market penetration in Asia‑Pacific through customized RF front‑ends and localized support contracts. Texas Instruments and STMicroelectronics supply power‑efficient analog front‑ends that improve device battery life in massive MTC deployments. Collectively, these firms occupy specialized niches,ranging from chipset optimisation to test‑equipment and system‑integration services,thereby expanding the competitive horizon and fostering a diversified supply chain that mitigates reliance on the dominant three.

List of Key Sparse Code Multiple Access for Machine-Type Communication Uplink Companies Profiled

- Nokia

- Ericsson

- Huawei

- Samsung

- Qualcomm

- MediaTek

- Mavenir

- Rohde & Schwarz

- ZTE

- Fujitsu

- NEC

- Texas Instruments

- STMicroelectronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Grant‑free access

|

| By Application |

|

Industrial automation

|

| By End User |

|

Network operators

|

| By Technology Maturity |

|

Commercially deployed solutions

|

| By Deployment Scenario |

|

Urban dense networks

|

Regional Analysis: North America

The industrial sector is a key consumer of SCMA for MTC uplink, leveraging it for real-time monitoring of assets, predictive maintenance, and automated control systems. The need for robust and reliable communication in demanding industrial environments is a fundamental driver.

Smart city deployments, encompassing applications like intelligent transportation, smart grids, and public safety, significantly benefit from the efficiency of SCMA for MTC uplink. The ability to handle a massive number of connected devices is a crucial factor in these initiatives.

Optimizing logistics and supply chain operations through connected devices, tracking systems, and automated warehousing relies heavily on dependable MTC uplink, where SCMA plays a vital role in ensuring seamless data transmission.

Remote patient monitoring, asset tracking, and connected medical devices within the healthcare sector are increasingly adopting SCMA for MTC uplink, enabling improved patient care and operational efficiency.

Europe

Europe exhibits a steady adoption rate of SCMA for MTC uplink, influenced by strong regulatory frameworks focused on data privacy and security. The emphasis on energy efficiency and sustainable technologies aligns well with the benefits offered by SCMA. Cross-border connectivity and the growing focus on industrial automation across various European nations are key market drivers. The region is witnessing increasing investments in 5G infrastructure, which further supports the deployment of SCMA technologies. While growth might be moderate compared to other regions, the consistent demand from key industrial sectors ensures a stable market.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for SCMA for MTC uplink. The region’s massive population, rapid urbanization, and burgeoning manufacturing sector are fueling the demand for connected devices. Government initiatives promoting digital transformation and smart infrastructure projects are significantly boosting market growth. The proliferation of IoT devices in industries like agriculture, mining, and transportation is a primary growth driver. The cost-effectiveness and energy efficiency of SCMA are particularly attractive in this price-sensitive market.

South America

South America presents a promising, albeit developing, market for SCMA for MTC uplink. The expansion of telecommunications infrastructure and increasing industrialization are creating opportunities for growth. The adoption of SCMA is primarily driven by sectors like agriculture, mining, and logistics, where connected devices are enhancing operational efficiency and productivity. Government initiatives aimed at improving connectivity in rural areas and promoting digital inclusion are contributing to market expansion.

Middle East & Africa

The Middle East & Africa region is witnessing increasing interest in SCMA for MTC uplink, driven by investments in smart city projects, industrial automation, and infrastructure development. The region’s focus on diversification away from traditional oil-based economies is accelerating the adoption of IoT technologies. The demand for low-power, wide-area networks (LPWAN) solutions is particularly strong in this region, where SCMA offers an efficient and cost-effective connectivity option. Government support for digital transformation initiatives is further boosting market growth.

Report Scope

This market research report provides a comprehensive analysis of the Sparse code multiple access for machine-type communication uplink Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Sparse code multiple access for machine-type communication uplink Market?

-> Sparse code multiple access for machine-type communication uplink Market was valued at USD 0.48 billion in 2025 and is expected to reach USD 1.14 billion by 2034.

Which key companies operate in Sparse code multiple access for machine-type communication uplink Market?

-> Key players include Nokia, Ericsson, and Huawei, among others.

What are the key growth drivers?

-> Key growth drivers include telecom operators expanding IoT deployments, incorporation of SCMA into 3GPP Release 16 for massive MTC, advancements in low‑power wide‑area network (LPWAN) infrastructure, and rising demand for smart‑city applications.

Which region dominates the market?

-> The market is global with significant adoption across major regions; the provided data does not identify a single dominant region.

What are the emerging trends?

-> The reference highlights ongoing integration of SCMA with emerging IoT and smart‑city solutions, as well as continued standardization efforts within 3GPP, but does not specify additional emerging trends.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...