MARKET INSIGHTS

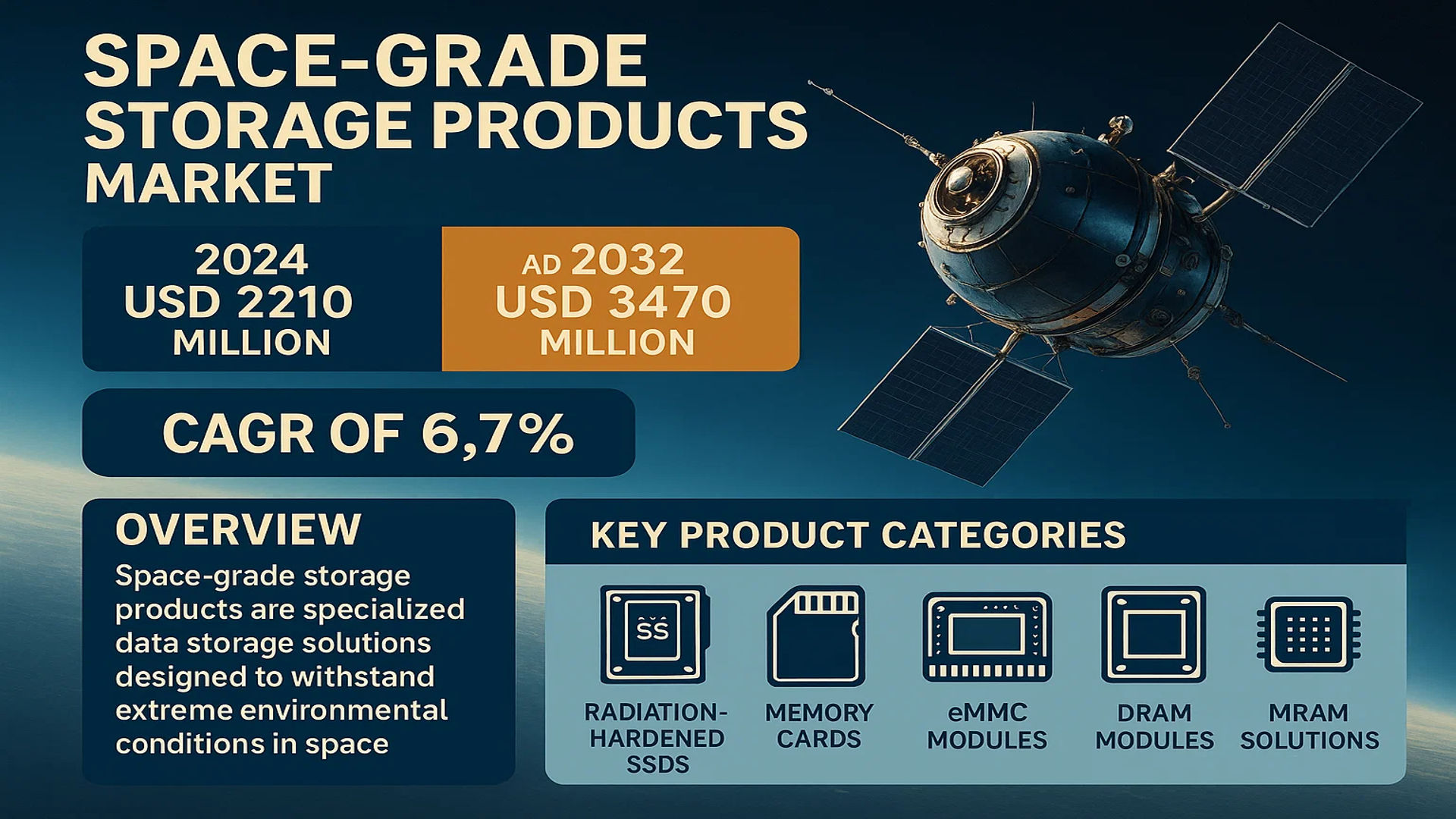

The global Space-Grade Storage Products Market was valued at 2210 million in 2024 and is projected to reach US$ 3470 million by 2032, at a CAGR of 6.7% during the forecast period.

Space-grade storage products are specialized data storage solutions designed to withstand extreme environmental conditions in space, including high-energy particle radiation, extreme temperature fluctuations, vacuum exposure, and mechanical shocks. These products ensure data integrity and reliability in critical applications such as satellite operations, space stations, and deep space exploration missions. Key product categories include radiation-hardened SSDs, memory cards, eMMC modules, DRAM modules, and MRAM solutions.

The market growth is driven by increasing space exploration missions and satellite deployments worldwide. While government space agencies remain major adopters, commercial space ventures are accelerating demand for robust storage solutions. The SSD segment shows particular growth potential due to its balance of capacity and reliability in space environments. Major players like Exascend, Curtiss-Wright, and Microchip Technology continue to innovate with radiation-tolerant designs, with the top five companies collectively holding significant market share in 2024.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Satellite Deployments and Space Missions Fuel Demand for Reliable Storage Solutions

The global space industry is witnessing unprecedented growth, with satellite deployments increasing at a compounded annual rate exceeding 15% as space-based communications, earth observation, and navigation systems become critical infrastructure. This surge demands highly reliable storage products capable of withstanding extreme conditions while ensuring data integrity over extended mission durations. Modern satellites require storage solutions that combine radiation hardening, thermal stability, and vibration resistance – features uniquely provided by space-grade storage products.

Government investments in space exploration programs continue to rise significantly, with major space agencies allocating increased budgets for lunar missions, Mars exploration, and deep-space probes. These missions generate vast amounts of scientific data that must be securely stored and retrieved, even in the harshest environments beyond Earth’s atmosphere. The growing complexity of space instrumentation and sensor technologies further amplifies the need for advanced storage capabilities in orbiting platforms and interplanetary spacecraft.

Technological Advancements in Radiation-Hardened Storage Solutions Accelerate Market Adoption

Recent breakthroughs in radiation-hardened semiconductor technologies have significantly improved the performance and reliability of space-grade storage products. Manufacturers are developing innovative solutions that combine high-density NAND flash memory with advanced error correction and wear-leveling algorithms specifically designed for space applications. These technological improvements enable storage capacities previously unattainable for space missions while meeting stringent reliability requirements.

The emergence of new non-volatile memory technologies such as MRAM (Magnetoresistive Random-Access Memory) offers particular promise for space applications due to inherent radiation tolerance and virtually unlimited write endurance. Leading manufacturers are investing heavily in qualifying these technologies for space use, with several products already deployed in recent missions. The transition from traditional bulkier storage solutions to more compact, higher-performance alternatives is driving replacement demand across both existing and new spacecraft platforms.

MARKET RESTRAINTS

Stringent Qualification Processes and Long Development Cycles Limit Market Expansion

Space-grade storage products face significant market barriers due to the extensive qualification and certification requirements mandated by space agencies and satellite manufacturers. The rigorous testing protocols necessary to validate radiation tolerance, thermal performance, and long-term reliability can extend product development timelines to several years, creating substantial upfront costs for manufacturers. These extended qualification cycles often delay market entry for new technologies and limit the pace of innovation adoption in space applications.

The space industry’s conservative approach to technology adoption further exacerbates this challenge, with many programs preferring flight-proven solutions over newer alternatives despite potential performance benefits. This risk-averse mentality stems from the catastrophic consequences of storage failures in space missions and the enormous costs associated with mission failures. While understandable from a reliability perspective, this conservatism can slow the introduction of improved storage technologies that could offer significant advantages in terms of capacity, speed, and power efficiency.

High Development and Manufacturing Costs Create Price Barriers

The specialized materials, manufacturing processes, and testing required for space-grade storage solutions result in substantially higher costs compared to commercial storage products. Radiation-hardened semiconductors can cost orders of magnitude more than their commercial equivalents, while the low production volumes typical of space applications prevent the economies of scale that help reduce costs in other technology sectors. These cost factors make space-grade storage products prohibitively expensive for some potential applications, particularly in the emerging small satellite market where budgets are more constrained.

Moreover, the need for extensive radiation testing and qualification adds significant non-recurring engineering costs that must be amortized over relatively small production runs. The specialized cleanroom facilities and stringent process controls required for manufacturing further contribute to the high price points. While the value proposition remains strong for critical missions where failure is not an option, these cost barriers limit market penetration in price-sensitive segments of the space industry.

MARKET CHALLENGES

Radiation Effects and Extreme Environmental Conditions Pose Technical Hurdles

Designing storage products that can reliably operate in the space environment presents numerous technical challenges. Cosmic rays and solar particle events can cause single-event effects that corrupt stored data or even permanently damage memory cells. The wide temperature ranges encountered in space – from cryogenic cold in shadow to intense heat when facing the sun – create additional material and reliability concerns. These environmental extremes require innovative designs that go far beyond terrestrial storage solutions.

The cumulative effects of radiation exposure over multi-year missions represents another significant challenge for storage product developers. Total ionizing dose effects gradually degrade semiconductor performance, while displacement damage can alter material properties over time. Manufacturers must implement comprehensive mitigation strategies including error correction codes, redundancy schemes, and radiation-hardened process technologies to ensure data integrity throughout mission lifetimes that often exceed a decade.

Supply Chain Vulnerabilities and Component Obsolescence Create Sustainability Issues

The space storage market faces ongoing challenges related to supply chain reliability and component lifecycle management. Many radiation-hardened components rely on specialized fabrication processes that are only supported by a limited number of semiconductor foundries worldwide. This concentration creates supply chain vulnerabilities that can disrupt production schedules and lead to extended lead times for critical components.

Additionally, the rapid pace of technological change in the commercial semiconductor industry often leads to premature obsolescence of parts used in space applications. Unlike consumer electronics with short lifecycles, space systems typically require stable supply chains spanning decades to support both initial production and potential refurbishment needs. The mismatch between commercial semiconductor lifecycles and space program durations creates significant challenges in maintaining long-term product availability and support.

MARKET OPPORTUNITIES

Commercial Space Sector Expansion Opens New Growth Avenues

The rapid growth of commercial space activities presents significant opportunities for space-grade storage providers. Private companies are launching constellations of hundreds or even thousands of satellites for global internet services, earth observation, and other applications. While some commercial operators use commercial off-the-shelf components with limited modifications, others require the enhanced reliability of radiation-hardened solutions, particularly for satellites in higher orbits with greater radiation exposure.

The increasing commercialization of lunar and deep-space missions also creates demand for storage solutions that can operate beyond low Earth orbit. Private lunar landers, asteroid mining ventures, and other ambitious commercial space projects all require robust data storage capabilities similar to those used in government science missions. This expanding market segment offers storage providers opportunities to develop specialized products optimized for commercial space applications with different cost and performance trade-offs than traditional government programs.

Emerging Space-Based Data Processing Creates Demand for High-Performance Storage

The growing trend toward edge processing in space creates new requirements for storage solutions that can support on-board data analysis and decision-making. Rather than simply storing raw sensor data for transmission to ground stations, modern spacecraft increasingly perform preliminary processing and analysis in orbit to reduce bandwidth requirements and enable rapid response to time-sensitive events. This shift toward space-based computing drives demand for storage products that combine radiation hardening with higher performance characteristics.

Artificial intelligence and machine learning applications in space represent a particularly promising growth area for advanced storage solutions. These applications require both high-capacity storage for training datasets and high-speed, low-latency memory for real-time inference operations. Storage providers that can deliver radiation-tolerant solutions meeting these performance requirements while maintaining reliability will be well-positioned to capitalize on this emerging opportunity as space-based AI adoption increases.

SPACE-GRADE STORAGE PRODUCTS MARKET TRENDS

Growing Space Exploration and Satellite Deployments to Drive Demand

The increasing number of space missions and satellite deployments is significantly boosting the demand for space-grade storage products. With space agencies and private companies focusing on deep-space exploration, Earth observation, and satellite constellations, there is a heightened need for reliable data storage solutions that can withstand extreme environmental conditions. The global space-grade storage products market was valued at $2,210 million in 2024, and with a projected compound annual growth rate (CAGR) of 6.7%, it is expected to reach $3,470 million by 2032. The United States currently leads in market size, followed by rapid growth in China, reflecting the increasing investments in space infrastructure.

Other Trends

Advancements in Radiation-Hardened Storage Technologies

Radiation-hardened SSDs and memory modules are becoming pivotal in ensuring data integrity in space missions. Traditional storage solutions often fail under high-energy particle radiation, prompting manufacturers to innovate with radiation-tolerant designs. For example, companies such as Curtiss-Wright and Microchip Technology have introduced ruggedized SSDs with error-correcting algorithms designed to mitigate single-event upsets—a common challenge in space. Additionally, the adoption of MRAM (Magnetoresistive Random-Access Memory) is growing due to its non-volatility and resilience to radiation, making it ideal for long-duration missions.

Rising Demand for High-Capacity Storage in Deep Space Missions

As deep-space exploration missions extend farther into the solar system, the need for high-capacity, low-power storage solutions is intensifying. Missions like NASA’s Artemis program and commercial ventures by SpaceX and Blue Origin demand storage systems capable of handling vast amounts of telemetry, scientific, and imaging data. Solid-state drives (SSDs) are expected to dominate, with projections indicating that the SSD segment will experience significant growth, driven by their superior speed and durability. Further developments in 3D NAND flash technology are also enabling higher storage densities, making them increasingly viable for prolonged space applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Reliability Drive Competition in the Space-Grade Storage Market

The global space-grade storage products market features a mix of established players and specialized manufacturers, all vying for contracts in this high-stakes sector. Curtiss-Wright and Microchip Technology currently lead the market, leveraging their decades of experience in radiation-hardened electronics and aerospace-grade components. These companies benefit from long-standing relationships with space agencies, securing their position in critical missions.

Meanwhile, 3D PLUS has emerged as a key innovator in compact storage solutions for small satellites, while Exascend gains traction with its radiation-tolerant SSDs for deep space applications. The growth of these players reflects broader industry demands for ruggedized data storage capable of withstanding extreme cosmic radiation and temperature fluctuations.

Several manufacturers are expanding capacity to meet growing demand from both government space programs and commercial satellite operators. Mercury Systems recently enhanced its production facilities to support the Artemis program, reflecting the industry’s preparation for upcoming lunar missions. Similarly, European supplier MSA Components GmbH secured additional funding to boost its MRAM production for next-generation space applications.

The market also sees increasing specialization, with companies like Trident Systems focusing on secure storage for defense satellites and Galleon Embedded Computing developing customizable modules for CubeSats. This product diversification helps manufacturers differentiate themselves in an increasingly competitive landscape where reliability and radiation-hardening certifications often determine contract awards.

List of Key Space-Grade Storage Product Manufacturers

- Curtiss-Wright (U.S.)

- Microchip Technology (U.S.)

- 3D PLUS (France)

- Exascend (U.S.)

- Mercury (U.S.)

- Seagate (U.S.)

- Galleon Embedded Computing (UK)

- MSA Components GmbH (Germany)

- Trident Systems (U.S.)

- Texas Instruments (U.S.)

Segment Analysis:

By Type

SSDs Lead the Market Due to High Reliability and Radiation-Hardened Design for Space Applications

The market is segmented based on type into:

- SSDs (Solid State Drives)

- Subtypes: SATA-based, NVMe-based, and ruggedized variants

- Memory Cards

- Subtypes: Rad-hard flash cards and specialized space-grade SD cards

- eMMC (Embedded MultiMediaCard)

- DRAM Modules

- MRAM Products

- Subtypes: Toggle MRAM, STT-MRAM

- Others

By Application

Satellite Segment Dominates Due to Increasing Commercial and Government Space Missions

The market is segmented based on application into:

- Satellite

- Subtypes: Communication, Navigation, Earth Observation, Scientific

- Space Station

- Deep Space Exploration

- Subtypes: Orbital probes, landers, rovers

- Others

By Technology

Radiation-Hardened Storage Solutions Dominate for Critical Space Applications

The market is segmented based on technology into:

- Radiation-Hardened (Rad-Hard)

- Radiation-Tolerant

- Commercial-Off-The-Shelf (COTS)

- Others

By Storage Capacity

Medium-Capacity Segment (64GB-1TB) Leads Due to Balanced Performance and Reliability Requirements

The market is segmented based on storage capacity into:

- Low Capacity (Below 64GB)

- Medium Capacity (64GB-1TB)

- High Capacity (Above 1TB)

Regional Analysis: Space-Grade Storage Products Market

North America

North America, led by the United States, dominates the space-grade storage products market due to its advanced aerospace infrastructure and substantial government investments in space exploration programs. NASA’s Artemis program, with a projected budget exceeding $93 billion by 2025, is driving demand for radiation-hardened storage solutions. The presence of key manufacturers like Curtiss-Wright and Microchip Technology supports technological advancements in high-reliability SSDs and memory modules. However, stringent certification requirements increase product development costs, creating barriers for new entrants. The region’s market growth is further fueled by increasing private sector participation through companies like SpaceX and Blue Origin, which require robust storage solutions for satellite constellations and deep-space missions.

Europe

Europe maintains a strong position in the space-grade storage market through robust ESA programs and collaborative defense initiatives. The EU’s commitment to satellite navigation (e.g., Galileo) and Earth observation (Copernicus) programs creates steady demand. Countries like France and Germany lead in developing radiation-tolerant flash storage and error-correction technologies, with firms like 3D PLUS and EXA Tech supplying critical components. While environmental regulations promote innovation in power-efficient designs, Brexit-related supply chain disruptions have temporarily impacted component availability. The region shows growing interest in quantum-resistant encryption for space data storage, anticipating future cybersecurity needs.

Asia-Pacific

As the fastest-growing region, Asia-Pacific benefits from China’s aggressive space program and India’s cost-effective satellite deployments. China’s Tiangong space station and lunar exploration missions stimulate demand for high-capacity radiation-hardened storage, while Japan focuses on miniaturized solutions for compact satellites. The lack of indigenous radiation testing facilities in emerging markets remains a bottleneck, forcing reliance on foreign certification. Collaborative projects like the Asia-Pacific Space Cooperation Organization foster technology transfer, though export controls on advanced components from Western nations constrain some developments. Regional players are making strides in thermal management solutions crucial for tropical launch environments.

Middle East and Africa

This emerging market is witnessing strategic investments in satellite technologies by GCC nations, particularly the UAE’s ambitious Mars Mission and Saudi Arabia’s Space Commission initiatives. While storage demands currently focus on Earth observation satellites, plans for regional navigation systems indicate future growth. South Africa’s existing aerospace infrastructure provides some local manufacturing capabilities. Challenges include high dependence on imports for critical components and limited local expertise in radiation-hardened electronics. However, partnerships with European and Chinese firms are gradually building indigenous capabilities in space-grade data storage solutions.

South America

South America’s market remains nascent but shows potential through Brazil’s revitalized space program and Argentina’s satellite manufacturing capabilities. The region primarily sources storage products from global suppliers due to limited local production of radiation-tolerant components. Budget constraints and political instability have delayed some planned satellite projects, though commercial small satellite deployments offer growth opportunities. Collaborative ventures with China in remote sensing satellites are introducing new technology streams, while historical partnerships with European agencies continue to influence technical standards. The focus remains on cost-effective solutions suitable for the region’s developing space economy.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Space-Grade Storage Products markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Space-Grade Storage Products market was valued at USD 2,210 million in 2024 and is projected to reach USD 3,470 million by 2032, growing at a CAGR of 6.7%.

- Segmentation Analysis: Detailed breakdown by product type (SSDs, Memory Cards, eMMC, DRAM Modules, MRAM Products), application (Satellite, Space Station, Deep Space Exploration), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. market is a key contributor, while China shows significant growth potential.

- Competitive Landscape: Profiles of leading market participants, including Exascend, Curtiss-Wright, Mercury, 3D PLUS, Microchip Technology, Seagate, among others. The top five players accounted for a significant revenue share in 2024.

- Technology Trends & Innovation: Assessment of emerging technologies, radiation-hardened storage solutions, high-reliability memory products, and evolving industry standards for space applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Space-Grade Storage Products Market?

-> Space-Grade Storage Products Market was valued at 2210 million in 2024 and is projected to reach US$ 3470 million by 2032, at a CAGR of 6.7% during the forecast period.

Which key companies operate in Global Space-Grade Storage Products Market?

-> Key players include Exascend, Curtiss-Wright, Mercury, 3D PLUS, Microchip Technology, Seagate, Galleon Embedded Computing, MSA Components GmbH, Trident Systems, and Texas Instruments (TI), among others.

What are the key growth drivers?

-> Key growth drivers include increasing space exploration missions, rising satellite deployments, and demand for radiation-hardened storage solutions in extreme environments.

Which region dominates the market?

-> North America leads the market due to significant space agency investments, while Asia-Pacific is emerging as the fastest-growing region.

What are the emerging trends?

-> Emerging trends include development of high-capacity space-grade SSDs, radiation-tolerant memory solutions, and miniaturized storage devices for small satellites.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...