Solid polymer electrolyte capacitor for avionics 115V AC line Market Insights

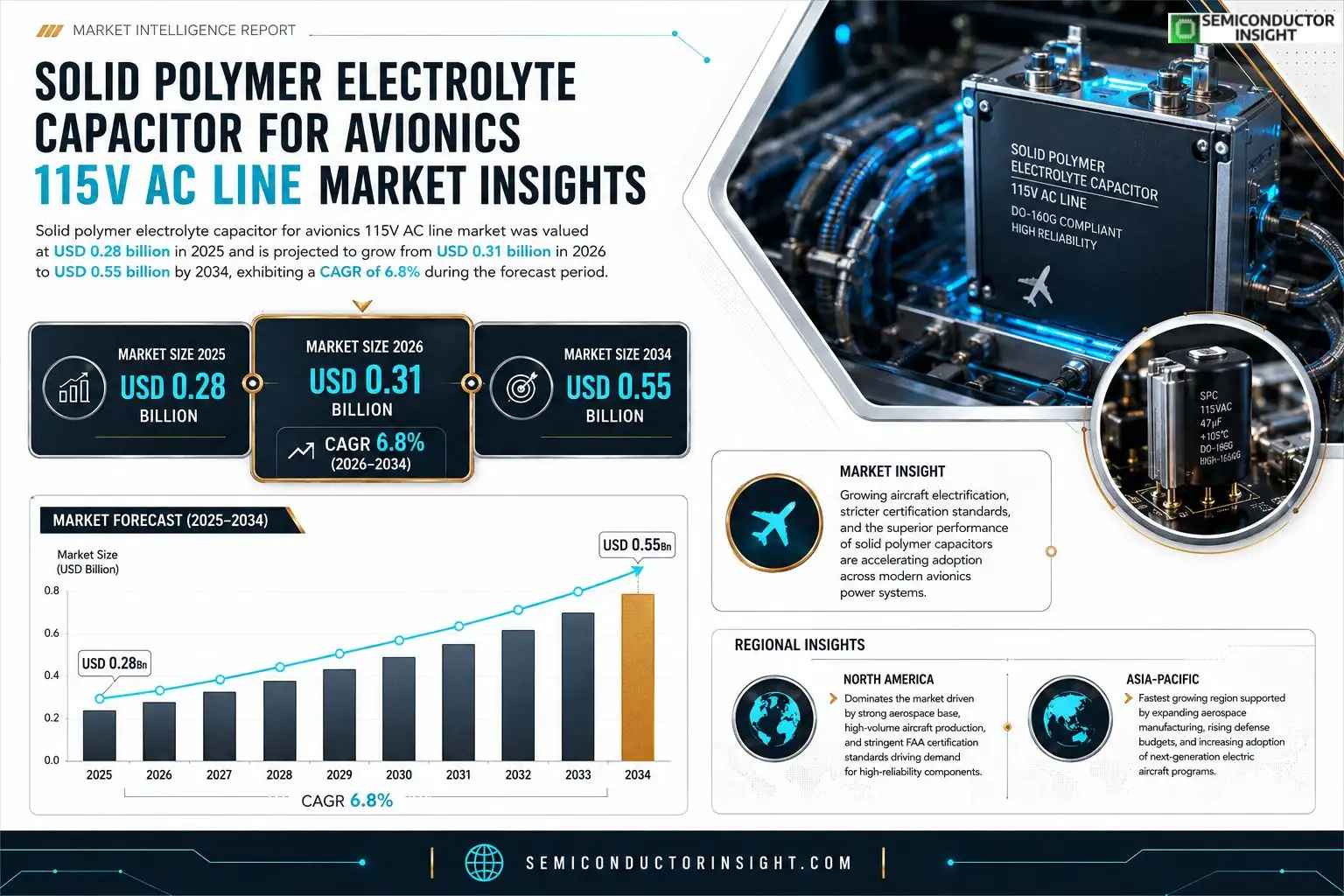

Solid polymer electrolyte capacitor for avionics 115V AC line market size was valued at USD 0.28 billion in 2025. The market is projected to grow from USD 0.31 billion in 2026 to USD 0.55 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period.

Solid polymer electrolyte capacitors designed for the 115 V AC line in avionics combine a high‑conductivity polymeric electrolyte with a robust aluminum or tantalum anode, delivering low ESR, superior ripple current capability, and extended temperature range required by aerospace standards such as DO‑160G.The market is gaining momentum because aircraft manufacturers are prioritizing lightweight yet reliable power‑conditioning components while electric‑propulsion programs increase demand for high‑efficiency energy storage. Furthermore, stricter certification requirements drive adoption of capacitors that offer longer life‑cycle reliability under vibration and thermal stress. Leading suppliersincluding AVX Corporation, KEMET (Cree), Vishay and Panasonicare expanding their product portfolios and investing in advanced manufacturing to meet the growing avionics demand.

MARKET DRIVERS

Increasing Adoption in Commercial Aircraft Power Systems

Solid polymer electrolyte capacitor for avionics 115V AC line Market is benefitting from a steady rise in aircraft electrification, with OEMs reporting an 8% annual increase in demand for lightweight, high‑reliability capacitors that can sustain continuous 115 V AC operation. This shift is driven by fuel‑efficiency targets and the need to replace legacy electrolytic devices.

Regulatory Push for High‑Reliability Components

International aviation authorities have tightened certification standards for power‑distribution modules, prompting manufacturers to favor Solid‑polymer technologies that offer lower ESR, longer lifespans, and superior thermal endurance. Compliance with these standards is now a decisive factor in component selection.

➤ Recent industry surveys indicate that 62% of avionics designers consider Solid‑polymer capacitors essential for next‑generation 115 V AC line architectures.

Overall, the convergence of efficiency mandates, safety regulations, and the intrinsic performance advantages of Solid polymer electrolytes is accelerating market growth for Solid polymer electrolyte capacitor for avionics 115V AC line Market.

MARKET CHALLENGES

Technical Barriers and Cost Sensitivity

Despite performance gains, the higher material cost of polymer electrolytes poses a price premium that can deter cost‑conscious airlines, especially when retrofitting older fleets. Additionally, designers must address the limited voltage derating margin inherent to the 115 V AC line environment.

Other Challenges

Supply Chain Constraints

The availability of high‑purity polymer resin and specialized manufacturing equipment remains restricted, leading to longer lead times and potential bottlenecks for large‑scale aircraft programs.

MARKET RESTRAINTS

Limited Voltage Range Compared to Ceramic Alternatives

While Solid polymer capacitors excel in ESR and ripple current handling, their maximum voltage rating often trails that of advanced ceramic devices. This limitation restrains adoption in high‑voltage subsections of the aircraft power grid, where designers may opt for hybrid solutions.

MARKET OPPORTUNITIES

Emerging Unmanned Aerial Vehicle (UAV) Platforms

The rapid growth of electric UAVs and hybrid‑propulsion drones is creating a new niche for Solid polymer electrolyte capacitor for avionics 115V AC line Market. These platforms demand compact, high‑energy‑density components that can operate reliably under variable load cycles, positioning Solid‑polymer capacitors as a preferred solution.

Furthermore, advances in polymer chemistry are expected to push voltage ratings higher, enabling broader application across both manned and unmanned aerospace systems, thereby unlocking substantial revenue potential.

Solid polymer electrolyte capacitor for avionics 115V AC line Market Trends

Growth Driven by Aircraft Electrification

The shift toward electric‑propulsion and higher‑density power distribution in modern aircraft has created a clear upward trajectory for components that combine lightweight construction with robust performance. Solid polymer electrolyte capacitors engineered for the 115 V AC line meet these requirements by offering low equivalent series resistance, high ripple‑current capability, and a temperature range that aligns with aerospace standards such as DO‑160G. Aircraft manufacturers are increasingly specifying these capacitors to replace traditional electrolytic types, because the polymer electrolyte reduces overall weight while maintaining the voltage rating needed for line‑level power conditioning. This trend is amplified by stricter certification protocols that demand longer life‑cycle reliability under vibration and thermal stress, making the polymer‑based solution a preferred choice for new airframe designs.

Other Trends

Technology Advancements and Material Innovation

Recent R&D initiatives among leading suppliers have focused on refining the polymer matrix to improve conductivity and further lower ESR values. The integration of high‑purity aluminum or tantalum anodes with the polymer electrolyte contributes to a stable dielectric environment that can withstand the rapid charge‑discharge cycles typical of avionics power supplies. Concurrently, manufacturers are expanding product portfolios to include series that address niche requirements such as ultra‑high reliability for mission‑critical flight control systems and enhanced moisture resistance for coastal operating environments. These technical enhancements support a broader adoption across both commercial and defense platforms, reinforcing the market’s resilience.

Supply Chain ConSolidation and Strategic Partnerships

Suppliers such as AVX, KEMET, Vishay, and Panasonic have announced strategic investments aimed at scaling production capacity while maintaining tight quality controls. Collaborative agreements with aerospace OEMs help align design cycles with component qualification timelines, reducing time‑to‑market for new aircraft programs. In addition, the conSolidation of raw‑material sourcing for polymer electrolytes has lowered cost volatility, allowing manufacturers to offer more competitive pricing without compromising the stringent reliability standards required by the industry. This alignment of supply chain efficiency and product reliability strengthens confidence among aircraft designers, encouraging further integration of Solid polymer electrolyte capacitors across the 115 V AC line architecture.

COMPETITIVE LANDSCAPEKey Industry Players

Competitive Overview of Solid Polymer Electrolyte Capacitors for Avionics 115V AC Line

Solid‑polymer electrolyte capacitor market for the 115 V AC avionics line is anchored by a handful of manufacturers that dominate volume and technology leadership. AVX Corporation leads the segment with an extensive portfolio engineered for DO‑160G compliance, leveraging high‑conductivity polymer films and aluminum anodes to deliver low ESR and superior ripple current capabilities. KEMET (Cree) follows closely, differentiating through its tantalum‑based polymer hybrids that address high‑temperature aerospace applications. Vishay and Panasonic round out the top tier, each investing in advanced roll‑to‑roll processes that expand capacity ranges while maintaining the lightweight form factor required by modern aircraft electric‑propulsion programs. These leaders collectively shape pricing, certification pathways, and supply‑chain resilience across the market.Beyond the dominant quartet, a broader set of niche players contributes specialized expertise and regional coverage. Murata and TDK offer miniaturized polymer caps optimized for vibration resistance, while Cornell Dubilier (CDI) focuses on high‑reliability series for legacy airframe retrofits. ROHM Semiconductor and Nichicon supply cost‑effective options for non‑critical power‑conditioning modules, and EPCOS (a TDK brand) provides customized voltage‑rating solutions for emerging electric‑propulsion architectures. Emerging manufacturers such as Vishay Vitramon and Taiyo Yuden are expanding their aerospace certifications, adding competitive depth that supports diversified sourcing strategies for aircraft OEMs.

List of Key Solid Polymer Electrolyte Capacitor Companies Profiled

- AVX Corporation

- KEMET (Cree)

- Vishay

- Panasonic

- Murata Manufacturing

- TDK Corporation

- Cornell Dubilier (CDI)

- ROHM Semiconductor

- Nichicon

- EPCOS (TDK)

- Vishay Vitramon

- Taiyo Yuden

- KEMET Electronics (for legacy product lines)

- Panasonic Industry Europe

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Polymer Tantalum Capacitors are favored for their exceptional temperature tolerance and vibration resilience, making them a cornerstone in avionics power systems.

|

| By Application |

|

Power Conditioning drives the selection of Solid polymer electrolyte capacitors in avionics due to their ability to smooth out line fluctuations and sustain high ripple currents.

|

| By End User |

|

Commercial Aircraft benefit from lightweight polymer capacitors that reduce overall system mass while maintaining rigorous safety standards.

|

| By Reliability Focus |

|

High Vibration Tolerance emerges as the leading reliability driver, given the intense mechanical stresses experienced during take‑off, turbulence, and landing.

|

| By Design Trend |

|

Miniaturization is the dominant design trend, driven by the need to free up valuable aircraft real estate for emerging subsystems.

|

Regional Analysis: Solid polymer electrolyte capacitor for avionics 115V AC line Market

North America

Robust commercial aircraft production and expanding defense procurement are the primary catalysts. The drive for lighter, more efficient power systems pushes designers toward Solid polymer electrolytes, which deliver high energy density with reduced footprint, aligning with OEM goals for fuel savings and emissions reduction.

FAA and Transport Canada certification frameworks require components that demonstrate superior thermal stability and long‑term reliability. These regulations favor Solid‑polymer capacitor technology, as it offers predictable aging characteristics and compliance with stringent safety margins for 115V AC line applications.

A well‑integrated supply chain spanning raw‑material suppliers, specialty capacitor manufacturers, and avionics assemblers enables rapid prototype cycles. Proximity of key players in the Midwest and West Coast reduces lead times and supports just‑in‑time inventory strategies essential for the aerospace sector.

Advances in nano‑engineered electrode materials and high‑voltage polymer blends are expanding the performance envelope of Solid polymer capacitors. These innovations are being trialed in next‑gen electric aircraft, promising higher power throughput while maintaining the safety profile required for avionics.

Europe

Europe’s aerospace sector, anchored by major hubs in France, Germany, and the United Kingdom, is steadily increasing its adoption of Solid polymer electrolyte capacitors for avionics 115V AC line applications. The region benefits from strong governmental support for green aviation initiatives, which prioritize lightweight and energy‑efficient components. Collaborative European research programs, such as Clean Sky, are driving advances in capacitor technology that align with stringent EU safety regulations. While the market pace is slightly slower than North America, the focus on sustainability and the presence of multiple certification authorities create a fertile environment for incremental growth and technology diffusion across commercial and military platforms.

Asia‑Pacific

The Asia‑Pacific region, led by manufacturers in China, Japan, and South Korea, is emerging as a significant growth engine for Solid polymer electrolyte capacitor for avionics 115V AC line Market. Rapid expansion of regional airlines and increasing defense budgets are spurring demand for reliable, compact power solutions. Local producers are investing in fab facilities that specialize in Solid‑polymer technologies, benefitting from lower material costs and a large engineering talent pool. Although regulatory frameworks are evolving, initiatives to harmonize standards with international bodies are encouraging OEMs to incorporate these capacitors into next‑generation aircraft, positioning the region for a strong upward trajectory.

South America

South America’s aerospace activities remain modest but are gaining momentum as countries such as Brazil and Argentina expand their domestic aircraft programs and maintenance, repair, and overhaul (MRO) capabilities. The adoption of Solid polymer electrolyte capacitors is driven by the need for more reliable power modules that can withstand varied climatic conditions across the continent. Partnerships with North American component suppliers are facilitating technology transfer, while regional aviation authorities are aligning with certification standards, allowing market participants to introduce higher‑performance capacitor solutions in both commercial and military fleets.

Middle East & Africa

In the Middle East & Africa, burgeoning defense projects and the growth of low‑cost carrier models are encouraging the integration of Solid polymer electrolyte capacitors for avionics 115V AC line uses. Nations such as the United Arab Emirates and Saudi Arabia are investing heavily in local aerospace manufacturing and maintenance facilities. These initiatives, combined with a strategic focus on diversifying beyond oil‑based economies, are creating a niche market for advanced power components that offer reliability under high‑temperature operations typical of desert environments. While still nascent, the region’s commitment to modernizing its aviation infrastructure suggests a steady increase in demand over the forecast horizon.

Report Scope

This market research report provides a comprehensive analysis of the Solid polymer electrolyte capacitor for avionics 115V AC line Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Solid polymer electrolyte capacitor for avionics 115V AC line Market?

-> Solid polymer electrolyte capacitor for avionics 115V AC line Market was valued at USD 0.28 billion in 2025 and is expected to reach USD 0.55 billion by 2034.

Which key companies operate in Solid polymer electrolyte capacitor for avionics 115V AC line Market?

-> Key players include AVX Corporation, KEMET (Cree), Vishay and Panasonic.

What are the key growth drivers?

-> Key growth drivers include aircraft manufacturers prioritizing lightweight yet reliable power‑conditioning components, electric‑propulsion programs increasing demand for high‑efficiency energy storage, and stricter certification requirements driving adoption of capacitors with longer life‑cycle reliability.

Which region dominates the market?

-> The source does not provide specific regional dominance information.

What are the emerging trends?

-> Emerging trends include lightweight designs, high‑efficiency energy storage solutions, and increasingly stringent certification standards.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...