MARKET INSIGHTS

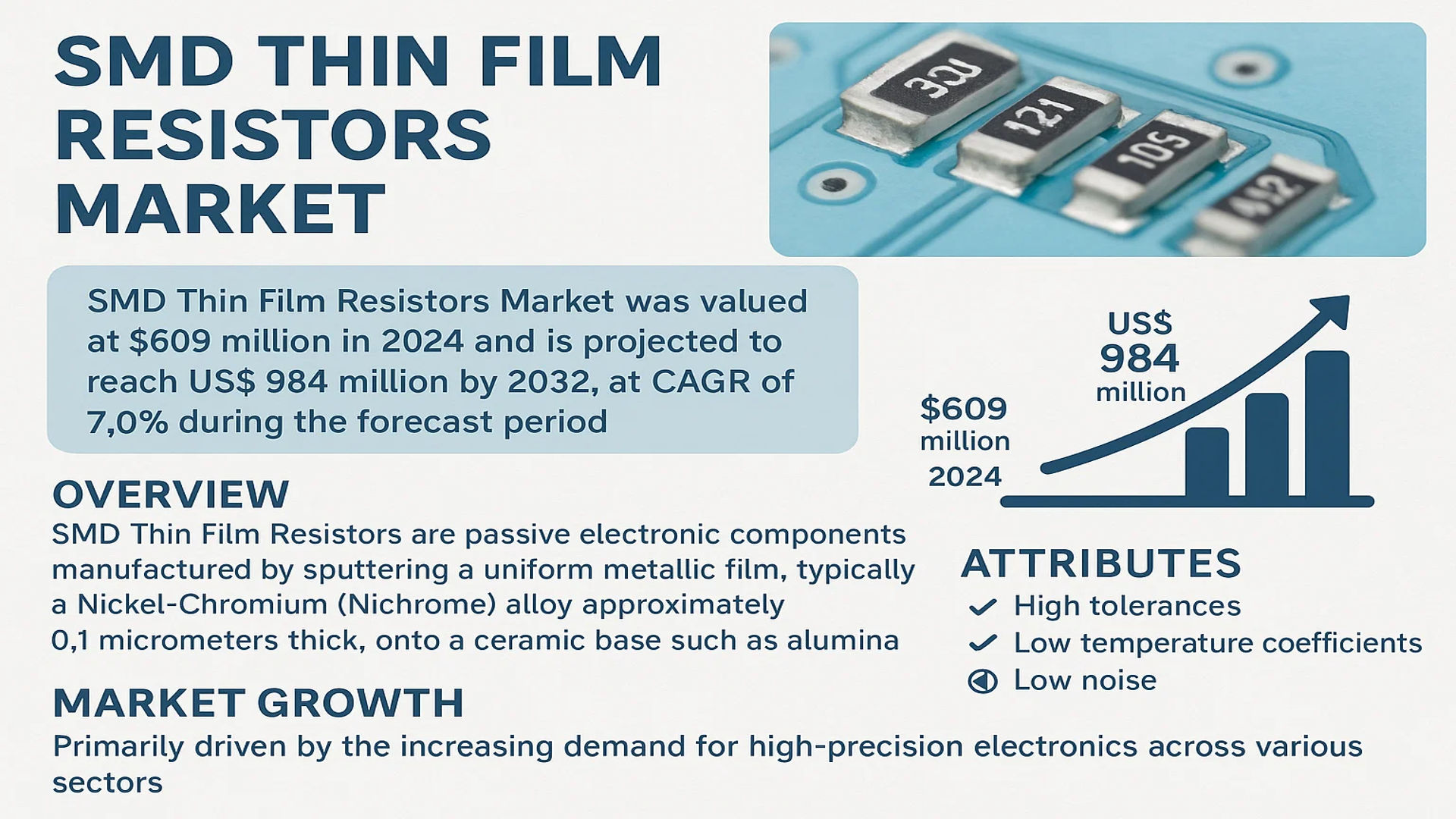

The global SMD Thin Film Resistors Market was valued at 609 million in 2024 and is projected to reach US$ 984 million by 2032, at a CAGR of 7.0% during the forecast period.

SMD Thin Film Resistors are passive electronic components manufactured by sputtering a uniform metallic film, typically a Nickel-Chromium (Nichrome) alloy approximately 0.1 micrometers thick, onto a ceramic base such as alumina. This process creates a dense, uniform layer that is precisely trimmed using laser or photo etching techniques to achieve high-precision resistance values. These components are characterized by their excellent performance, including high tolerances, low temperature coefficients, and low noise, making them indispensable for precision applications.

The market is experiencing steady growth, primarily driven by the increasing demand for high-precision electronics across various sectors. Key growth factors include the expansion of the medical equipment and automotive electronics industries, alongside the continuous advancement in communication devices. Asia Pacific is the largest consumption region, with China alone accounting for 27.09% of the global sales volume market share in 2024. Leading players such as Vishay, which held a 29.96% revenue market share, Susumu, and KOA Speer Electronics dominate this concentrated market, continually innovating to meet the stringent requirements of modern electronic applications.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of High-Precision Instrumentation to Accelerate Market Growth

The global demand for high-precision electronic instrumentation is a primary driver for the SMD thin film resistors market. These components are essential in applications requiring tight tolerances, low temperature coefficients, and minimal noise, such as medical diagnostic equipment, laboratory instruments, and industrial measurement systems. The instrumentation segment accounted for over 35% of the total market revenue in 2024, reflecting the critical role of precision resistors in ensuring accuracy and reliability. As industries increasingly adopt automated and digitally integrated systems, the need for stable and precise passive components continues to rise. Furthermore, advancements in semiconductor technology and the miniaturization of electronic devices are pushing manufacturers to develop thinner, more efficient resistive films that meet stringent performance criteria.

Rising Adoption in Automotive Electronics to Fuel Demand

Automotive electronics represent a rapidly growing application segment for SMD thin film resistors, driven by the increasing electrification of vehicles and the integration of advanced driver-assistance systems (ADAS). Modern vehicles incorporate numerous electronic control units (ECUs), sensors, and infotainment systems that require high reliability and precision under varying environmental conditions. Thin film resistors offer superior performance in terms of stability and resistance to thermal cycling compared to thick film alternatives, making them ideal for automotive applications. The automotive electronics segment is projected to grow at a compound annual growth rate of approximately 9.2% from 2024 to 2032, significantly contributing to the overall market expansion.

Additionally, the push towards electric vehicles (EVs) and autonomous driving technology is further accelerating the incorporation of precision electronic components. These systems demand resistors with low parasitic effects and high frequency stability, attributes that thin film technology provides effectively.

➤ For instance, leading automotive manufacturers are increasingly specifying thin film resistors for critical safety and control systems to ensure long-term reliability and compliance with automotive-grade standards.

Moreover, regulatory standards emphasizing vehicle safety and emissions control are encouraging the use of higher-quality electronic components, thereby supporting market growth.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing to Limit Market Penetration

Despite their superior performance characteristics, SMD thin film resistors face significant restraints due to their high production costs and complex manufacturing processes. The deposition of thin films through sputtering or vacuum deposition requires specialized equipment and controlled environments, leading to higher capital expenditure and operational costs compared to thick film resistors. These expenses are often passed on to end-users, making thin film resistors less attractive for cost-sensitive applications. In price-competitive markets, such as consumer electronics, manufacturers frequently opt for thick film alternatives, which can be up to 50% cheaper, thereby limiting the adoption of thin film technology.

Additionally, the precision trimming processes, such as laser calibration, add further to the manufacturing complexity and time, impacting overall production scalability. These factors collectively restrain market growth, particularly in regions and industries where cost efficiency is prioritized over performance specifications.

Other Restraints

Intense Competition from Alternative Technologies

Alternative resistor technologies, including thick film and metal foil resistors, present substantial competition. Thick film resistors dominate general-purpose applications due to their cost-effectiveness and adequate performance for many uses. Metal foil resistors, while also premium-priced, compete in ultra-high precision segments, creating a crowded competitive landscape that challenges market expansion for thin film variants.

Supply Chain Vulnerabilities

The market is susceptible to disruptions in the supply of raw materials, such as nickel-chromium alloys and high-purity ceramics. Geopolitical tensions and trade restrictions can lead to price volatility and availability issues, affecting production consistency and delivery timelines for manufacturers.

MARKET CHALLENGES

Technical Complexity in Miniaturization Poses Significant Challenges

As electronic devices continue to shrink in size, the challenge of manufacturing increasingly miniature SMD thin film resistors without compromising performance becomes more pronounced. Achieving tolerances as tight as 0.05% on smaller form factors requires advanced lithography and trimming technologies, which escalate production costs and technical hurdles. The industry is grappling with maintaining low noise and high stability in increasingly compact designs, particularly as operating frequencies rise in modern applications like 5G communication devices and high-speed data acquisition systems.

Other Challenges

Thermal Management Issues

Effective heat dissipation becomes more challenging as component sizes decrease. Thin film resistors must maintain performance under power loading without excessive temperature rise, which can alter resistance values and affect circuit accuracy. Designing resistors that balance miniaturization with thermal stability requires innovative materials and structural approaches.

Standardization and Compatibility Constraints

The lack of global standardization in certain performance parameters and footprints can create compatibility issues across different manufacturers and systems. This variability may lead to design inefficiencies and increased validation time for OEMs integrating these components into larger assemblies.

MARKET OPPORTUNITIES

Growth in Telecommunications and 5G Infrastructure to Unlock New Opportunities

The rapid global deployment of 5G networks and telecommunications infrastructure presents substantial growth opportunities for the SMD thin film resistors market. These components are critical in RF circuits, base stations, and network equipment where high frequency stability, low inductance, and precise impedance matching are essential. The expansion of 5G requires massive investments in infrastructure, with projections indicating that over 70% of the world’s population will have 5G coverage by 2030. This expansion drives demand for high-performance passive components capable of operating reliably in demanding RF environments.

Additionally, the Internet of Things (IoT) ecosystem, which relies heavily on robust connectivity, further amplifies the need for precision resistors in sensors, gateways, and communication modules. This convergence of telecommunications and IoT creates a sustained demand pipeline for advanced thin film resistor solutions.

Furthermore, ongoing research in materials science, such as the development of novel resistive alloys and substrate materials, promises to enhance the performance and reduce the cost of thin film resistors, potentially opening up new application areas and market segments.

SMD THIN FILM RESISTORS MARKET TRENDS

Miniaturization and High-Frequency Applications Driving Market Evolution

The relentless push towards miniaturization in electronics is a primary catalyst for innovation within the SMD thin film resistor market. As devices shrink, components must follow suit, demanding resistors with smaller footprints while maintaining or even enhancing performance characteristics. This trend is particularly evident in the telecommunications and consumer electronics sectors, where the proliferation of 5G infrastructure and compact wearable technology necessitates components capable of operating reliably at high frequencies. Thin film technology excels here because its manufacturing process allows for extremely precise patterning and lower parasitic inductance and capacitance compared to thick film alternatives. The market has responded with a growing portfolio of ultra-compact chip sizes, such as 0201 and 01005, which are increasingly specified in new designs. This drive for smaller components is intrinsically linked to the demand for higher circuit density and improved power efficiency, making thin film resistors a critical enabling technology for next-generation electronic devices.

Other Trends

Expansion in Automotive Electronics

The automotive industry’s rapid transformation towards electrification and advanced driver-assistance systems (ADAS) is creating substantial new demand for high-reliability SMD thin film resistors. Modern vehicles are essentially complex networks of electronic control units (ECUs), sensors, and infotainment systems, all requiring precise and stable passive components. Thin film resistors are indispensable in these applications due to their excellent temperature coefficient of resistance (TCR), often as low as ±5 ppm/°C, and their high tolerance, which ensures accuracy over the vehicle’s entire operating life and under harsh environmental conditions. The growth of electric vehicles (EVs) further amplifies this demand, as their battery management systems (BMS) and power conversion units rely heavily on precision resistors for monitoring and control functions. This sector’s stringent quality and longevity requirements align perfectly with the performance attributes of thin film technology, securing its position as a key component in the future of automotive electronics.

Rising Demand from Medical and Test & Measurement Equipment

Precision is non-negotiable in medical diagnostics and high-accuracy test and measurement instrumentation, solidifying the role of SMD thin film resistors in these high-value sectors. Equipment such as MRI machines, patient monitoring systems, laboratory analyzers, and precision oscilloscopes require components that deliver minimal drift, low noise, and long-term stability. The thin film deposition process creates a uniform metallic layer that provides these exact characteristics, making it the technology of choice for critical analog circuits where measurement integrity is paramount. Furthermore, the ongoing technological advancements in medical devices, including the trend towards more portable and personalized healthcare equipment, are driving the need for components that offer high performance in a small form factor. This consistent demand from sectors where performance outweighs cost considerations provides a stable and growing market segment for thin film resistor manufacturers, insulating them from some of the price pressures found in consumer markets.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The competitive landscape of the global SMD Thin Film Resistors market is semi-consolidated, characterized by a mix of large multinational corporations, specialized medium-sized enterprises, and smaller niche players. This structure fosters a dynamic environment where innovation, precision manufacturing capabilities, and strategic market positioning are critical for success. The market exhibits a relatively high concentration rate, with the top players commanding significant revenue shares.

Vishay Intertechnology, Inc. stands as the undisputed market leader, a position solidified by its extensive and technologically advanced product portfolio. In 2024, Vishay accounted for a commanding 29.96% of the global thin film chip resistors revenue market share. Its dominance is attributed to its strong global distribution network, consistent investment in research and development, and a reputation for high reliability in precision applications across sectors like medical equipment, automotive electronics, and instrumentation.

Following Vishay, Susumu Co., Ltd. and KOA Speer Electronics, Inc. are also pivotal players, holding significant portions of the market with revenue shares of approximately 12.26% and 9.48% respectively in 2024. The growth of these companies is primarily driven by their deep expertise in thin-film technology, focus on miniaturization and performance, and strong relationships with OEMs in the consumer electronics and telecommunications industries, particularly within the Asia-Pacific region.

Additionally, these leading companies are actively pursuing growth through strategic initiatives. Geographical expansion into emerging markets, particularly in Southeast Asia, is a key focus to tap into new demand centers. Concurrently, new product launches featuring enhanced tolerances, lower temperature coefficients, and improved high-frequency performance are expected to further grow their market share over the projected period. For instance, recent developments have seen a push towards ultra-precise 0.05% tolerance resistors for advanced medical diagnostic equipment.

Meanwhile, other key participants like Yageo Corporation, Panasonic Corporation, and TE Connectivity are strengthening their market presence through significant investments in production automation and capacity expansion. They are also engaging in strategic partnerships and acquisitions to broaden their technological reach and customer base, ensuring continued growth and adaptation within the competitive landscape. The intense competition ensures a continuous drive for innovation, ultimately benefiting end-users with higher performance components.

List of Key SMD Thin Film Resistor Companies Profiled

- Vishay Intertechnology, Inc. (U.S.)

- Susumu Co., Ltd. (Japan)

- KOA Speer Electronics, Inc. (U.S.)

- Viking Tech Corporation (Taiwan)

- Yageo Corporation (Taiwan)

- Panasonic Corporation (Japan)

- Walsin Technology Corporation (Taiwan)

- Ta-I Technology Co., Ltd. (Taiwan)

- Bourns, Inc. (U.S.)

- UniOhm Co., Ltd. (China)

- TE Connectivity Ltd. (Switzerland)

- Samsung Electro-Mechanics (South Korea)

- Ralec Electronics Corp. (Taiwan)

- Ever Ohms Technology Co., Ltd. (Taiwan)

Segment Analysis:

By Type

0.05% Tolerance Segment Leads Due to Critical Demand in High-Precision Instrumentation

The market is segmented based on tolerance into:

- 0.05% Tolerance

- 0.1% Tolerance

- 1% Tolerance

- Others

By Application

Instrumentation Segment Dominates Owing to Uncompromising Requirements for Accuracy and Stability

The market is segmented based on application into:

- Instrumentation

- Medical Equipment

- Automotive Electronics

- Communication Device

- Others

By End-User Industry

Industrial Manufacturing Represents a Core End-User Driven by Automation and Process Control Needs

The market is segmented based on end-user industry into:

- Industrial Manufacturing

- Healthcare

- Telecommunications

- Automotive

- Consumer Electronics

Regional Analysis: SMD Thin Film Resistors Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global SMD Thin Film Resistors market, accounting for the largest consumption share. This is primarily driven by the massive electronics manufacturing base in China, which alone occupied 27.09% of the global sales volume market share in 2024. The region’s growth is fueled by extensive production of instrumentation, medical equipment, and communication devices. Countries like Japan and South Korea are home to leading technology firms and component manufacturers, such as Panasonic and Samsung Electro-Mechanics, which demand high-precision resistors for advanced applications. While cost sensitivity remains a factor, the push towards more sophisticated electronics and automation is steadily increasing the adoption of thin film over thick film solutions. The region also benefits from a robust supply chain and significant investments in research and development, ensuring its continued leadership.

North America

North America holds the position of the second-largest consumption region, with a market share of over 28.71%. The market is characterized by high demand for precision components from the aerospace, defense, medical technology, and telecommunications sectors. Stringent performance requirements and a focus on reliability and quality over cost drive the adoption of SMD thin film resistors. The presence of major players like Vishay and TE Connectivity, who are leaders in innovation, further strengthens the regional market. Investments in next-generation technologies, including 5G infrastructure, electric vehicles, and advanced medical diagnostics, are key growth drivers. The market is mature and values components with low temperature coefficients and high stability for critical applications.

Europe

Europe’s market is driven by its strong industrial and automotive electronics sectors, particularly in Germany, France, and the U.K. The region has a significant demand for high-reliability components used in automotive control systems, industrial automation, and measurement equipment. European OEMs prioritize components that meet strict quality standards and environmental regulations, such as those outlined by EU directives. While the market is well-established, growth is steady, supported by continuous innovation in automotive electronics (especially electric vehicles) and industrial IoT. The presence of specialized manufacturers and a focus on engineering excellence underpins the demand for precision SMD thin film resistors in this region.

South America

The SMD Thin Film Resistors market in South America is emerging and is currently characterized by smaller volume consumption compared to other regions. Growth is primarily linked to the gradual expansion of the industrial and consumer electronics manufacturing base in countries like Brazil and Argentina. However, the market’s development is often constrained by economic volatility, which can limit capital investment in advanced manufacturing equipment that utilizes high-precision components. While there is a baseline demand for these resistors in repair and maintenance markets, the widespread adoption for new, high-end applications is slower. The market potential exists but is contingent on greater economic stability and increased industrial investment.

Middle East & Africa

This region represents an emerging market with nascent growth potential for SMD Thin Film Resistors. Demand is primarily concentrated in specific sectors such as telecommunications infrastructure development and the oil & gas industry, which require reliable electronic components for control and monitoring systems. However, the overall market size remains limited due to a less developed local electronics manufacturing ecosystem. Growth is further tempered by a reliance on imported components and a focus on cost-effective solutions rather than high-precision options. Long-term market expansion will be tied to broader economic diversification and increased technological adoption across various industries.

Report Scope

This market research report provides a comprehensive analysis of the global and regional SMD Thin Film Resistors markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by tolerance level, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging fabrication techniques, integration of AI/IoT, semiconductor design trends, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global SMD Thin Film Resistors Market?

-> SMD Thin Film Resistors Market was valued at 609 million in 2024 and is projected to reach US$ 984 million by 2032, at a CAGR of 7.0% during the forecast period.

Which key companies operate in Global SMD Thin Film Resistors Market?

-> Key players include Vishay, Susumu, KOA Speer Electronics, Viking Tech, Yageo, Panasonic, Walsin Technology, Ta-I Technology, Bourns, and UniOhm, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for precision instrumentation, growth in medical equipment manufacturing, and the expansion of automotive electronics and communication devices.

Which region dominates the market?

-> Asia-Pacific is the largest consumption region, with China alone accounting for 27.09% of global sales volume, while North America holds a significant market share of over 28.71%.

What are the emerging trends?

-> Emerging trends include advancements in laser trimming technology, development of ultra-high precision resistors for next-gen electronics, and increased adoption in 5G communication infrastructure.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...