Smartphone Light Sensors Market Insights

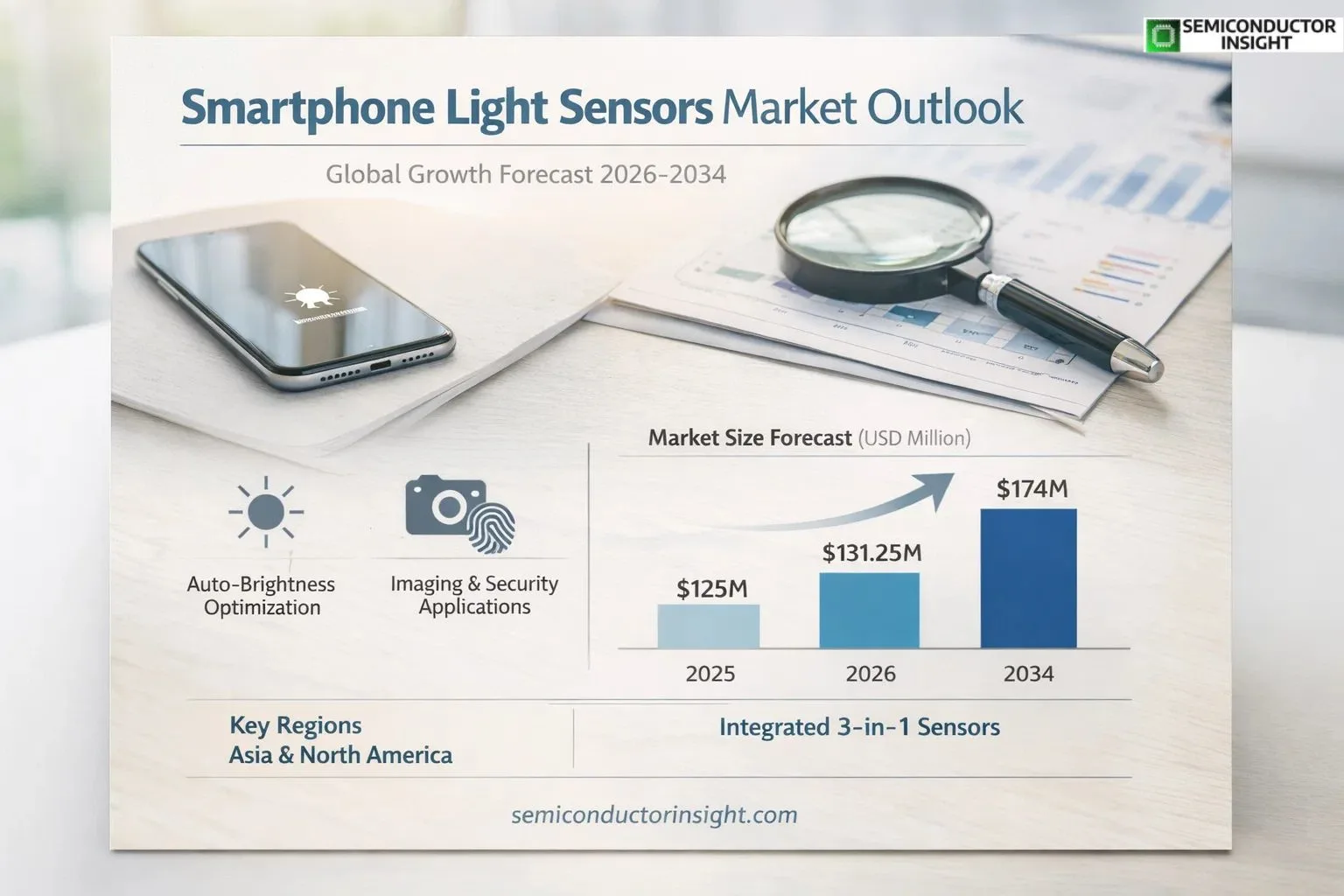

Global smartphone light sensors market size was valued at USD 125 million in 2025. The market is projected to grow from USD 131.25 million in 2026 to USD 174 million by 2034, exhibiting a CAGR of 5.0% during the forecast period.

Smartphone light sensors are integral components in modern smartphones, designed to measure the intensity of ambient light in the surrounding environment. These sensors are primarily used to enhance the user experience by automatically adjusting settings such as screen brightness, ensuring optimal visibility and conserving battery power. They also play a crucial role in other features like auto-focus in cameras, gesture recognition, and advanced power management systems.

The market is experiencing steady growth due to several factors, including the persistent consumer demand for premium smartphones with enhanced display and camera capabilities. Furthermore, the integration of more sophisticated multi-functional sensor modules, such as 3-in-1 units combining ambient light sensing (ALS), proximity detection, and RGB color sensing, is a key driver. However, the market faces challenges from smartphone commoditization and price pressures in emerging regions. Initiatives by key players are expected to fuel innovation; for instance, companies like ams-OSRAM AG and STMicroelectronics continuously develop smaller, more accurate, and lower-power sensors to meet OEM specifications for flagship devices. Sensortek, Broadcom, Vishay, and Lite-On Technology are some of the key players that operate in this competitive market with a wide range of portfolios.

MARKET DRIVERS

Superior Display and Power Management

The demand for smarter, more energy-efficient mobile devices is a primary driver for the smartphone light sensors market. These sensors optimize screen brightness by measuring ambient light, a crucial feature for modern OLED displays. This not only enhances outdoor visibility and user comfort but also significantly reduces battery consumption by automatically dimming the screen in dark environments, extending device usage times and improving the overall user experience.

The Rise of Imaging and Security Features

Advanced imaging and biometric authentication technologies are expanding the role of light sensors. Beyond simple brightness control, they are now critical components for camera systems, enabling better HDR photo capture by fine-tuning exposure. Furthermore, proximity sensing—often paired with infrared light emitters—remains essential for touchscreen deactivation during calls and forms the basis for secure, non-contact gesture controls.

➤ The integration of ambient light sensors in over 1.8 billion smartphones shipped annually underscores their status as an indispensable component.

Manufacturers are increasingly incorporating multi-channel sensors that can distinguish between natural and artificial light, allowing for even more refined auto-white balance in photography and context-aware adjustments for features like reading mode.

MARKET CHALLENGES

Performance and Calibration Complexities

A key challenge in the smartphone light sensors market is achieving consistent and accurate performance. Sensor calibration is complex, as it must account for a wide spectrum of lighting conditions, from direct sunlight to dim indoor settings, across various screen types and sensor placements under the display. Inaccuracies can lead to poor user experience, such as a screen that is too dim or blindingly bright.

Other Challenges

Cost and Integration Pressure

As smartphone BOM costs are scrutinized, the price pressure on sensor components intensifies. Integrating more sophisticated, multi-functional sensors while maintaining slim device profiles presents significant engineering hurdles.

Technological Saturation

The core auto-brightness function is now a mature feature. Convincing OEMs to adopt next-generation sensors with marginal improvements, rather than cost-optimized standard units, is an ongoing commercial challenge for sensor manufacturers.

MARKET RESTRAINTS

Market Maturity and Commoditization

The smartphone market’s transition to a replacement-driven, rather than growth-driven, model acts as a restraint on the smartphone light sensors market. Basic ambient light sensing is a commoditized technology with thin margins. This limits R&D investment for advanced variants in the mid-to-low-tier smartphone segments, which constitute the highest volume sales, thereby slowing overall market innovation and value growth.

Supply Chain and Component Competition

Intense competition for space within the smartphone’s internal architecture restrains sensor development. New components for 5G, larger batteries, and enhanced cooling systems often take priority, limiting the physical real estate for larger or more complex sensor arrays. Furthermore, volatile global semiconductor supply chains can disrupt component availability, impacting production schedules for sensor-dependent devices.

MARKET OPPORTUNITIES

Advanced Under-Display and Health Sensing

The move towards full-screen, bezel-less designs creates a major opportunity for advancements in under-display light sensors. Innovations that allow sensors to function accurately beneath the screen without compromising display quality are in high demand. Furthermore, the convergence with health monitoring presents a transformative opportunity. Integrating spectral sensors capable of measuring light reflectance for heart rate or blood oxygen saturation can turn a standard smartphone into a vital health-tracking tool.

Context-Aware Computing and AR Integration

The expansion of Augmented Reality (AR) applications and context-aware services offers a significant growth vector. Next-generation light sensors that provide precise environmental color temperature and illuminance data can dramatically improve AR realism by allowing virtual objects to cast accurate shadows and blend with real-world lighting. This enables more immersive gaming, shopping, and navigation experiences, driving demand for higher-specification sensors in premium smartphone models.

Smartphone Light Sensors Market Trends

Integration of Multi-Function Sensor Packages

The trend toward integration within the Smartphone Light Sensors Market is accelerating, led by the adoption of multi-function sensor packages. There is a clear shift away from single-purpose light sensors towards 2-in-1 and 3-in-1 combinations that integrate proximity, ambient light, and color detection into a single module. This consolidation reduces component footprint on the smartphone motherboard, lowers power consumption, and simplifies the supply chain for OEMs. The demand for these advanced sensors is particularly strong in premium and mid-range devices aiming to offer sophisticated features like true-tone display adjustment and enhanced power management using less physical space. This integration directly supports the development of sleeker, bezel-less smartphone designs.

Other Trends

Expansion Beyond Display Management

The core application for ambient light sensors remains automatic screen brightness adjustment to optimize visibility and battery life. However, a key trend in the Smartphone Light Sensors Market is their expanding role in imaging and contextual awareness. Advanced sensors are increasingly used to assist with camera auto-white balance and exposure calculations, improving photo quality. Furthermore, these components are enabling new gesture-based and context-aware user interfaces, where the smartphone responds to changes in environmental lighting. This evolution positions the light sensor not just as a utility component but as a key enabler for improved camera performance and intuitive user interaction.

Supply Chain Consolidation and Competitive Landscape

The competitive environment in the Smartphone Light Sensors Market is characterized by significant innovation and consolidation. Leading manufacturers like Sensortek, Broadcom, and STMicroelectronics focus on advancing sensor accuracy and miniaturization while integrating more functions. A notable trend is the strategic acquisition of sensor technology firms by larger semiconductor companies to bolster their portfolios. This competitive pressure and the demand for cost-efficiency are encouraging suppliers to streamline production processes and develop long-term strategic partnerships with major smartphone brands, particularly in high-growth regions such as Asia, which remains Global manufacturing hub for these components.

COMPETITIVE LANDSCAPE

Key Industry Players

Analyzing market dynamics, innovation, and strategic positioning of key suppliers in the smartphone photonics ecosystem.

Global smartphone light sensor market is characterized by a concentrated yet competitive vendor landscape dominated by established semiconductor and optoelectronics giants. In 2025, the top five players collectively held a significant revenue share, underscoring a high barrier to entry driven by the need for advanced photonics technology, miniaturization expertise, and long-standing relationships with major smartphone OEMs. Market leader Sensortek, along with Broadcom and STMicroelectronics, forms a powerful core group. These companies leverage their extensive R&D capabilities and economies of scale to produce high-precision, low-power ambient light and proximity sensors, including advanced 2-in-1 and 3-in-1 combo modules, which are essential for flagship and mid-tier smartphones across both IOS and Android ecosystems.

Beyond the dominant leaders, numerous specialized and niche players contribute significantly to the market’s technological breadth and regional supply chains. Companies like ams-OSRAM AG and Vishay are notable for their strong portfolios in advanced optical sensing solutions. Meanwhile, firms such as Silicon Labs and Melexis bring expertise in integrated sensor interfaces and automotive-grade reliability to the mobile sector. The competitive intensity is further heightened by agile Asian manufacturers including Lite-On Technology, Everlight, and Sharp Corporation, which compete vigorously on cost-efficiency and volume production. The expanding application scope beyond basic brightness control—into areas like camera auto-focus optimization and gesture-based UI controls—continues to drive innovation and strategic partnerships across the supplier base.

List of Key Smartphone Light Sensors Companies Profiled

- Sensortek

- Broadcom Inc.

- STMicroelectronics

- Silicon Labs

- ams-OSRAM AG

- Vishay Intertechnology, Inc.

- Lite-On Technology Corp.

- Everlight Electronics Co., Ltd.

- Melexis NV

- Sharp Corporation

- Rohm Semiconductor

- Epticore Microelectronics

- HiveMotion

- Sensonia

- Amic Technology

- Dyna Image Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

2-in-1 Light Sensors represent the foundational and widely adopted category, providing core ambient light sensing for automatic brightness adjustment. However, the market is increasingly characterized by a shift toward more sophisticated, integrated solutions. 3-in-1 Light Sensors are emerging as the leading growth segment, driven by the premium smartphone trend for multi-functional, space-saving components. These sensors combine ambient light, proximity, and RGB/gesture sensing into a single package, enabling enhanced user experience features like improved auto-brightness, touchless gesture control, and context-aware power management, which are critical differentiators for high-end devices. |

| By Application |

|

Android Smartphones constitute the dominant application segment due to their vast global volume and extensive product portfolio spanning all price tiers. This segment drives high-volume demand for cost-effective sensor solutions while also pushing innovation as Android OEMs compete on features in the mid-range and premium brackets. The ecosystem’s diversity fosters a broad spectrum of sensor specifications and integration strategies, from basic functionality in budget models to advanced 3-in-1 implementations in flagship devices, making it the primary battleground for sensor suppliers. |

| By End User |

|

Premium/Flagship Smartphone Manufacturers are the key trendsetters and primary drivers for advanced sensor adoption. This segment prioritizes performance, miniaturization, and multi-functionality to enable cutting-edge features like seamless adaptive displays, advanced camera assist functions, and novel human-device interactions. Their demand for high-precision, integrated sensors (like 3-in-1 types) creates a technology pull-through effect, establishes new performance benchmarks, and often leads to tighter, more collaborative supply chain relationships with leading sensor manufacturers to achieve custom integrations and ensure component reliability. |

| By Sensor Capability |

|

Advanced/Context-Aware Sensing is rapidly becoming the focal point for market evolution beyond simple illumination measurement. This capability segment involves sensors that can detect light color temperature (RGB sensing), flicker, and specific spectral components. The leading insight is that this enables smartphones to intelligently adapt screen color balance for eye comfort (e.g., blue light reduction), improve camera white balance in real-time, and better discern between artificial and natural light environments for more accurate and energy-efficient display management, which is a significant value-add for user experience. |

| By Integration Level |

|

Multi-Sensor Hub Integration is a critical strategic segment shaping supplier dynamics and phone design. Here, the light sensor is combined with other sensors (accelerometer, gyroscope) into a central hub managed by a dedicated low-power processor. The leading trend is the movement towards this architecture because it offloads processing from the main application processor, enabling continuous, context-aware functionality like “Always-On Display” and advanced power management without significant battery drain. This integration level demands close collaboration between sensor vendors and platform designers, creating a competitive advantage for suppliers offering robust, interoperable sensor fusion software and hardware. |

Regional Analysis: Smartphone Light Sensors Market

The region’s status as Global electronics manufacturing center creates an integrated supply chain that is indispensable for smartphone light sensor production. Proximity to major assembly plants allows for tighter collaboration on design integration and faster time-to-market for new sensor modules, giving manufacturers a significant logistical and cost advantage.

The diverse and demanding consumer markets in countries like China and India drive the need for smart features reliant on light sensors. Features such as adaptive display technology for varying light conditions and energy-saving functions are key selling points, pushing OEMs to source the most reliable and responsive ambient light sensing components available.

Leading technology companies and research institutes across South Korea, Japan, and Taiwan are at the forefront of developing advanced light sensing technologies. This includes R&D into sensor fusion, miniaturization, and improved accuracy for applications beyond basic brightness control, such as health monitoring and enhanced augmented reality features on smartphones.

The intensely competitive smartphone landscape in Asia-Pacific forces brands to differentiate through hardware features. This constant pressure results in the early adoption of new light sensor capabilities, creating a dynamic and fast-evolving market for sensor suppliers who must continually innovate to meet the specifications of leading OEMs in the region.

North America

North America represents a high-value market for advanced smartphone light sensors, characterized by a strong consumer preference for premium devices from leading brands. The market dynamics are heavily influenced by innovation in flagship smartphones, where sophisticated ambient light and proximity sensors are standard for enabling premium user experiences like True Tone displays and advanced power management. The region’s robust focus on software-hardware integration pushes sensor performance beyond basic functionality. Furthermore, significant investments in next-generation technologies such as augmented reality and advanced biometrics create early demand for light sensors with higher precision and new capabilities. The presence of major technology firms driving ecosystem development also influences sensor specifications and adoption patterns, ensuring a steady demand for cutting-edge components.

Europe

Europe exhibits a mature and quality-conscious smartphone light sensors market, with strong demand driven by consumer privacy regulations and high device standards. Regional dynamics are shaped by a preference for devices with excellent durability and energy efficiency, where reliable light sensors play a crucial role in optimizing battery life and screen performance. The market sees steady demand from both Western European consumers seeking premium features and Eastern European markets with growing mid-range adoption. European OEMs and brands often emphasize the refined implementation of sensor-driven features, influencing requirements for accuracy and consistency in ambient light sensing. Additionally, the region’s stringent environmental and electronic waste directives encourage the development and integration of longer-lasting, more efficient sensor components in smartphones.

South America

The smartphone light sensors market in South America is primarily volume-driven, with growth centered on expanding affordability and accessibility in the mid- to low-tier smartphone segments. Market dynamics are influenced by economic factors, with a strong focus on cost-competitive devices that still deliver reliable core functionalities. This creates demand for robust, value-oriented light sensor modules that provide essential features like automatic brightness adjustment without significantly increasing the bill of materials. As local manufacturing and assembly gradually increase in countries like Brazil, there is potential for closer integration with supply chains, which could influence regional specification preferences over time. The market’s evolution is tied to broader smartphone adoption rates and replacement cycles.

Middle East & Africa

The Middle East & Africa region presents a diverse and growing market for smartphone light sensors, characterized by a high reliance on imported devices and a rapidly expanding user base. Market dynamics vary significantly between the high-income Gulf states, where demand aligns with global flagship trends requiring advanced sensors, and broader African markets, where affordability and durability in harsh environmental conditions are paramount. This duality drives demand for a wide spectrum of smartphone light sensors, from high-precision components for luxury devices to resilient, cost-effective solutions for entry-level smartphones. The region’s often extreme ambient lighting conditions also place a practical emphasis on the performance and reliability of auto-brightness features, influencing OEM sourcing decisions for this key component.

Report Scope

This market research report provides a comprehensive analysis of the Smartphone Light Sensors Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smartphone Light Sensors Market?

-> Global Smartphone Light Sensors Market was valued at USD 125 million in 2025 and is projected to reach USD 174 million by 2034, growing at a CAGR of 5.0% during the forecast period.

Which key companies operate in Smartphone Light Sensors Market?

-> Key players include Sensortek, Broadcom, STMicroelectronics, SILICON LABS, ams-OSRAM AG, Vishay, Lite-On Technology, Everlight, Melexis, and Sharp Corporation, among others. Global top five players held a significant revenue share in 2025.

What are the key growth drivers?

-> Key growth drivers include the widespread integration of sensors in smartphones for enhancing user experience through features like automatic screen brightness adjustment, auto-focus in cameras, gesture recognition, and power management for battery conservation.

Which region dominates the market?

-> U.S. and China are key country-level markets within Global landscape. Market performance is analyzed across North America, Europe, Asia, South America, and the Middle East & Africa.

What are the emerging trends?

-> Emerging trends include the development and adoption of integrated sensor types like 2-in-1 and 3-in-1 solutions, and their increasing application across various smartphone platforms including IOS and Android smartphones.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...