Smart Vision Chips Market Insights

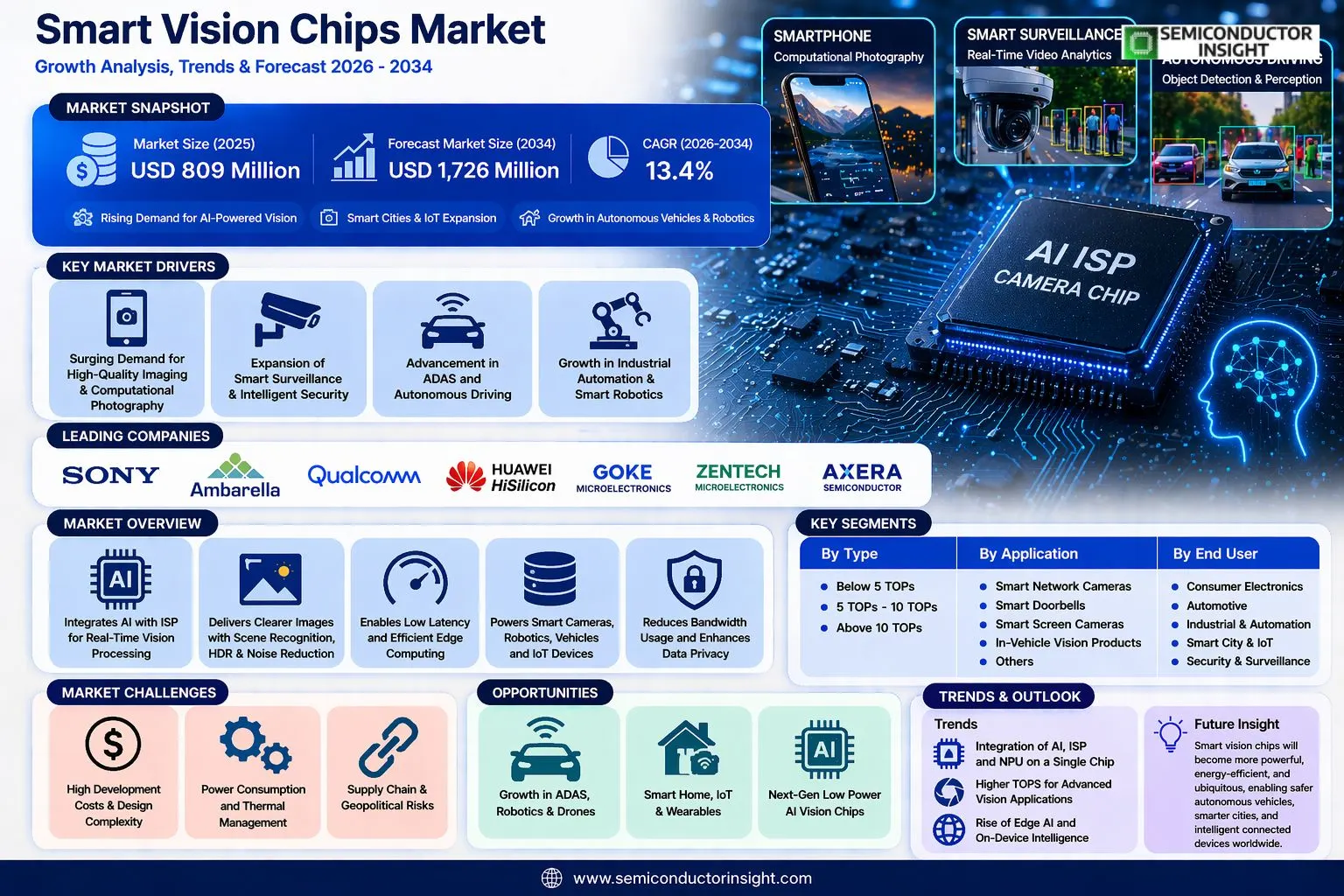

Global Smart Vision Chips market size was valued at USD 809 million in 2025. The market is projected to grow from USD 917 million in 2026 to USD 1,726 million by 2034, exhibiting a CAGR of 13.4% during the forecast period.

Smart Vision Chips are specialized integrated circuits that integrate advanced image processing and artificial intelligence technologies directly onto the hardware. These chips are crucial for enabling real-time visual intelligence in devices, as they combine the functions of traditional image signal processors (ISPs),such as automatic exposure, white balance, and noise reduction,with dedicated neural processing units (NPUs) to execute deep learning algorithms efficiently. This hardware-level integration allows for on-device image recognition and intelligent analysis without constant reliance on cloud connectivity, which is vital for applications requiring low latency and data privacy.

The market is experiencing rapid growth due to several factors, including the explosive demand for AI-powered vision in consumer electronics like smartphones and smart home devices, alongside significant advancements in autonomous vehicles and industrial robotics. Furthermore, the proliferation of IoT devices and smart city infrastructure is creating substantial new demand. Initiatives by key players are also expected to fuel market growth. For instance, companies are continuously launching more powerful and energy-efficient chipsets; a recent development saw Ambarella introduce its new CV5 series AI vision processor for automotive and robotics applications in late 2023. Sony, Ambarella, Huawei HiSilicon, and a range of specialized Chinese firms like Goke Microelectronics and Axera Semiconductor are some of the key players that operate in the market with a wide range of portfolios.

MARKET DRIVERS

Proliferation of AI and Edge Computing

The exponential growth of artificial intelligence applications, particularly computer vision, is the primary catalyst for Smart Vision Chips Market. These specialized processors are designed to perform high-speed, low-power image processing and inferencing at the edge, reducing latency and bandwidth dependency. The rise of Industry 4.0 and smart city infrastructure further pushes the demand for localized, real-time visual data analysis, which these chips efficiently provide.

Demand from Automotive and Surveillance Sectors

The automotive industry’s relentless drive toward Advanced Driver-Assistance Systems (ADAS) and autonomous vehicles creates a massive, high-value segment. Smart vision chips are critical for processing feeds from multiple cameras and sensors for object detection. Simultaneously, the security and surveillance sector constantly seeks more intelligent analytics for facial recognition and behavior monitoring, directly fueling market expansion in Smart Vision Chips Market.

➤ Innovation in chip architecture is accelerating, with a trend toward System-on-Chip (SoC) designs that integrate neural processing units specifically optimized for convolutional neural networks, the backbone of modern computer vision.

Furthermore, consumer electronics like smartphones and AR/VR devices increasingly integrate advanced camera features and immersive experiences, which rely on powerful, yet energy-efficient, visual processing. This diversification of applications ensures robust and sustained demand for smart vision processors.

MARKET CHALLENGES

High Development Complexity and Cost

Designing and manufacturing smart vision chips involves immense technical complexity, requiring expertise in AI algorithms, semiconductor physics, and power optimization. The high non-recurring engineering (NRE) costs and long development cycles, often spanning several years, present significant entry barriers for new players. Additionally, keeping pace with rapidly evolving machine learning models requires continuous and costly architectural revisions.

Other Challenges

High-Power Consumption in Advanced Applications

While optimized for efficiency, the most advanced chips for real-time 4K/8K video analysis or autonomous driving still face significant thermal and power challenges, limiting deployment in certain mobile and embedded form factors.

Ensuring Privacy and Ethical AI Implementation

The deployment of vision AI, particularly in public surveillance, raises major data privacy and ethical concerns. Navigating diverse and evolving global regulations complicates product standardization and market access for vendors.

MARKET RESTRAINTS

Supply Chain Fragility and Geopolitical Tensions

Smart Vision Chips Market remains susceptible to global semiconductor supply chain disruptions. Geopolitical tensions affecting access to advanced fabrication technologies and raw materials can constrain production capacity and lead to volatile pricing. This over-concentration in manufacturing geography poses a persistent risk to steady market growth.

High Threshold for System Integration

The integration of a Smart Vision Chip into a final product is not a simple component swap. It requires significant software development, calibration with camera sensors, and optimization for specific use cases. This complexity raises the total cost of ownership for OEMs and can slow down adoption in cost-sensitive or less technologically mature industries.

MARKET OPPORTUNITIES

Expansion into Healthcare and Agricultural Technology

Beyond traditional sectors, Smart Vision Chips Market has vast potential in medical imaging diagnostics and precision agriculture. Chips capable of real-time analysis for disease detection in crops or assisting in surgical procedures represent high-growth, high-impact verticals. These applications demand extreme reliability and accuracy, creating opportunities for specialized, high-value chip solutions.

Advent of Neuromorphic and Event-Based Vision

The next frontier lies in neuromorphic computing, which mimics the human brain’s neural structure for even greater efficiency. Event-based vision sensors, paired with compatible smart vision chips, process only changes in a scene rather than full frames. This emerging paradigm promises revolutionary reductions in power and latency, opening doors to entirely new applications for Smart Vision Chips Market in mobile robotics and always-on wearable devices.

Sustainability and Energy-Efficient AI

Global push for sustainability drives demand for ultra-low-power electronic components. Smart vision chips that enable complex visual AI at the microwatt level can power battery-operated devices for years, unlocking massive deployments in environmental monitoring, smart building management, and large-scale IoT networks, making energy efficiency a key competitive differentiator.

Trends

Convergence of AI and ISP Fuels Edge Intelligence

A dominant trend in Smart Vision Chips Market is the deep hardware integration of neural processing units (NPUs) with traditional image signal processors (ISPs). This convergence enables real-time, on-device intelligent analytics, reducing latency and reliance on cloud connectivity. Chips are increasingly designed to perform complex tasks like object detection, facial recognition, and behavior analysis directly at the edge. This is critical for applications such as autonomous vehicles and industrial robotics where instant decision-making based on visual data is paramount. The advancement is characterized by architectural innovations that optimize power efficiency for always-on vision systems in devices like smart cameras and screen devices, providing more functional and responsive products.

Other Trends

Rising Demand for Lower Compute Tiers

There is significant market growth for chips with computing power below 5 tera-operations per second (TOPs). These cost-effective solutions are well-suited for high-volume consumer Internet of Things (IoT) applications, including smart doorbells and network cameras. Their popularity is driving market expansion as they bring intelligent vision capabilities to mass-market devices, enabling features like package detection or basic person recognition without prohibitive cost. This trend indicates a diversification and maturation of Smart Vision Chips Market, catering to a broader range of price and performance points.

Geographic Shift and Competitive Dynamics

The competitive landscape is evolving, with Asia, particularly China, emerging as a major hub for both consumption and innovation in Smart Vision Chips Market. This is supported by a robust ecosystem of manufacturers serving strong local demand for security and smart home products. Leading global players like Sony and Ambarella are competing with specialized firms such as HiSilicon and Goke Microelectronics. Market competition is intensifying around developing chips that balance performance, power consumption, and system cost. Furthermore, manufacturers are increasingly specializing by application, tailoring their offerings for key segments like automotive vision or smart city infrastructure to capture targeted market share.

COMPETITIVE LANDSCAPE

Key Industry Players

A dynamic field characterized by specialized semiconductor firms, major imaging giants, and strategic AI innovators.

The competitive landscape of Global smart vision chips market is fragmented and highly dynamic, with established semiconductor leaders competing alongside specialized Chinese and international fabless companies. In 2025, Global top five players collectively accounted for a significant revenue share, indicating a concentration of technological and market presence among frontrunners. Sony stands as a dominant force, leveraging its unparalleled strength in image sensor technology to integrate advanced processing at the chip level. Similarly, Ambarella maintains a leading position, particularly in markets such as IP security cameras and automotive, through its high-performance system-on-chips (SoCs) that combine video processing with proprietary AI acceleration. The market structure is further defined by intensive R&D, strategic partnerships across the IoT ecosystem, and a relentless push to improve performance-per-watt and deep learning inference capabilities at the edge.

Beyond the top-tier players, a cohort of significant niche companies is expanding the market’s reach and application diversity. Numerous China-based fabless semiconductor companies are gaining substantial ground, supported by strong domestic demand in security, smart home, and automotive sectors. Key players like Huawei HiSilicon, Goke Microelectronics, and Rockchip Electronics offer competitive System-on-Chip (SoC) solutions that integrate neural processing units (NPUs). Emerging AI-specific chip designers, such as Shanghai TaskOrientedAI, Axera Semiconductor, and Shanghai NextVPU, are focusing on next-generation architectures optimized for computer vision tasks, challenging incumbents with more flexible and efficient designs. This diverse ecosystem drives rapid innovation cycles, price competition, and specialization across key application segments like smart doorbells, in-vehicle vision products, and smart screen cameras.

List of Key Smart Vision Chips Companies Profiled

- Sony

- Ambarella

- Huawei HiSilicon

- Nextchip

- Goke Microelectronics

- Rockchip Electronics

- Axera Semiconductor

- Shanghai TaskOrientedAI

- Vimicro Technology Corporation

- Shanghai Visinex Technology

- Shanghai Timesintelli

- Shanghai NextVPU

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Below 5TOPs chips represent a highly accessible and growth-oriented segment. Their cost-effectiveness and energy efficiency make them the preferred choice for deployment across a vast range of high-volume, mass-market smart IoT devices and consumer electronics. This includes entry-level smart cameras and wearables where ultra-high computational throughput is not the primary requirement, thus enabling widespread integration of basic vision intelligence at a lower system cost. |

| By Application |

|

Smart Network Cameras form a cornerstone application, driving significant demand for vision chips. The continuous global emphasis on security, surveillance, and smart city infrastructure necessitates real-time, intelligent video analytics at the edge. This requires chips capable of on-device processing for functions like facial recognition, object detection, and anomaly monitoring, reducing bandwidth costs and latency while enhancing privacy and system responsiveness. |

| By End User |

|

Consumer Electronics remains the dominant and most dynamic end-user segment, fueled by relentless innovation and high-volume production. The proliferation of smart home devices, from security cameras and video doorbells to intelligent displays and AR/VR equipment, creates a ubiquitous demand for compact, power-efficient vision chips. This segment’s growth is tightly linked to consumer adoption trends and the continuous integration of AI features into everyday gadgets. |

| By Processing Architecture |

|

System-on-Chip (SoC) architectures are leading due to their high integration and design efficiency. By combining the image signal processor, CPU, memory, and dedicated AI acceleration cores on a single chip, SoCs offer optimal performance-per-watt and a smaller footprint. This is critical for space-constrained and battery-powered edge devices, simplifying system design for manufacturers and enabling faster time-to-market for a wide array of vision-enabled products. |

| By Integration Level |

|

Standalone Vision Processors hold a crucial position for applications demanding specialized, high-performance vision computing. They provide dedicated, optimized hardware separate from the main system processor, which is essential for complex, latency-sensitive tasks in automotive ADAS, industrial machine vision, and high-end security systems. This separation allows for parallel processing, ensures deterministic performance, and prevents vision tasks from being interrupted by other system functions, offering reliability and precision. |

Regional Analysis: Smart Vision Chips Market

North America

The region serves as the primary hub for architectural innovation in Smart Vision Chips Market, with companies pioneering specialized neural processing units (NPUs) and edge-AI solutions. Focus is on developing low-power, high-performance chips capable of real-time image analysis, critical for next-generation applications across sectors.

Strong demand stems from the advanced automotive sector’s push towards autonomous driving. North American OEMs and tech firms are major integrators of sophisticated computer vision systems, creating a high-value niche for advanced Smart Vision Chips that meet rigorous safety and reliability standards.

Rapid adoption in smart manufacturing and industrial IoT drives market volume. Vision chips are deployed for quality inspection, predictive maintenance, and logistics automation. The mature industrial base readily integrates these solutions to enhance productivity and operational intelligence.

A favorable environment of significant private equity investment and supportive government initiatives for semiconductor sovereignty and AI research accelerates development. Regulatory standards for data privacy and machine safety also shape chip design priorities within the North American Smart Vision Chips Market.

Europe

Europe carves out a significant position in Smart Vision Chips Market, characterized by its strong emphasis on industrial automation, automotive excellence, and stringent data privacy regulations under frameworks like GDPR. The region’s automotive industry, with its focus on premium vehicles and advanced driver-assistance systems (ADAS), is a primary driver, demanding high-reliability vision processing solutions. Furthermore, robust manufacturing sectors in Germany, Italy, and France are actively integrating smart vision for precision engineering and Industry 4.0 initiatives. The European approach often prioritizes specialized, high-performance chips for niche industrial and scientific applications, supported by collaborative R&D projects funded by the EU. This creates a market dynamic focused on quality, security, and application-specific innovation within the broader Smart Vision Chips Market ecosystem.

Asia-Pacific

The Asia-Pacific region is the fastest-evolving and most volume-driven segment of Global Smart Vision Chips Market, fueled by massive electronics manufacturing, rapid urbanization, and substantial government investments in smart city and surveillance infrastructure. China is a central force, with aggressive national strategies in AI and semiconductor self-sufficiency driving both supply and demand. The region excels in cost-competitive manufacturing and scaling vision chips for consumer electronics, smartphones, and expansive public security networks. Countries like Japan, South Korea, and Taiwan contribute advanced manufacturing capabilities and are key players in the supply chain. The diverse application landscape, from automotive production to retail analytics, makes the Asia-Pacific Smart Vision Chips Market a critical hub for mass adoption and manufacturing innovation.

South America

South America represents an emerging and growth-oriented region within Global Smart Vision Chips Market, where adoption is gradually accelerating. Primary growth drivers include the modernization of agricultural technologies, where vision chips are used for monitoring and automation, and investments in urban security and infrastructure projects within major metropolitan areas. The industrial and manufacturing sectors, particularly in Brazil and Argentina, are beginning to explore vision-based automation to enhance competitiveness. While the market is nascent compared to global leaders, increasing awareness of Industry 4.0 benefits and regional economic development initiatives are fostering a slowly expanding base for Smart Vision Chips Market applications, focusing initially on import and integration of established technologies.

Middle East & Africa

The Middle East & Africa region presents a dynamic and investment-led opportunity for Smart Vision Chips Market, characterized by ambitious smart city projects, security-focused expenditures, and infrastructure development. Gulf Cooperation Council (GCC) nations are at the forefront, deploying advanced surveillance and facial recognition systems nationwide and integrating smart vision into transportation and hospitality as part of broader economic diversification plans. In Africa, select urban centers are adopting technology for security and traffic management. The region’s market growth is propelled by government-led technology procurement and partnerships with global tech firms, positioning it as a strategic, high-potential market for security and urban management applications of vision processing technology.

Report Scope

This market research report provides a comprehensive analysis of Smart Vision Chips Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining the current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of smart vision chips in powering advancements across industries such as automotive, security, consumer electronics, and smart IoT devices.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (e.g., Below 5TOPs, 5TOPs-10TOPs, Above 10TOPs), application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI and deep learning algorithms, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Vision Chips Market?

-> Smart Vision Chips Market was valued at USD 809 million in 2025 and is projected to reach USD 1726 million by 2034, growing at a CAGR of 13.4% during the forecast period.

Which key companies operate in Smart Vision Chips Market?

-> Key players include Sony, Ambarella, Huawei HiSilicon, Nextchip, Goke Microelectronics, Rockchip Electronics, Axera Semiconductor, Shanghai TaskOrientedAI, Vimicro Technology Corporation, and Shanghai Visinex Technology, among others.

What are the key growth drivers?

-> Key growth drivers include the rising demand for advanced image processing and AI technologies in smartphones, security monitoring, self-driving cars, robots, and smart IoT devices, enabling efficient image recognition and intelligent analysis at the hardware level.

Which region dominates the market?

-> The market is analyzed across key regions including North America, Europe, Asia, and others. The report provides market size estimations for the U.S. and China, with specific country-level growth analysis in the full report.

What are the key application segments?

-> Key application segments include Smart Network Cameras, Smart Doorbells, Smart Screen Cameras, In-vehicle Vision Products, and others, each analyzed for market size and development potential in the report.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...