Smart label printer with thermal transfer for cable tags and panel Market Insights

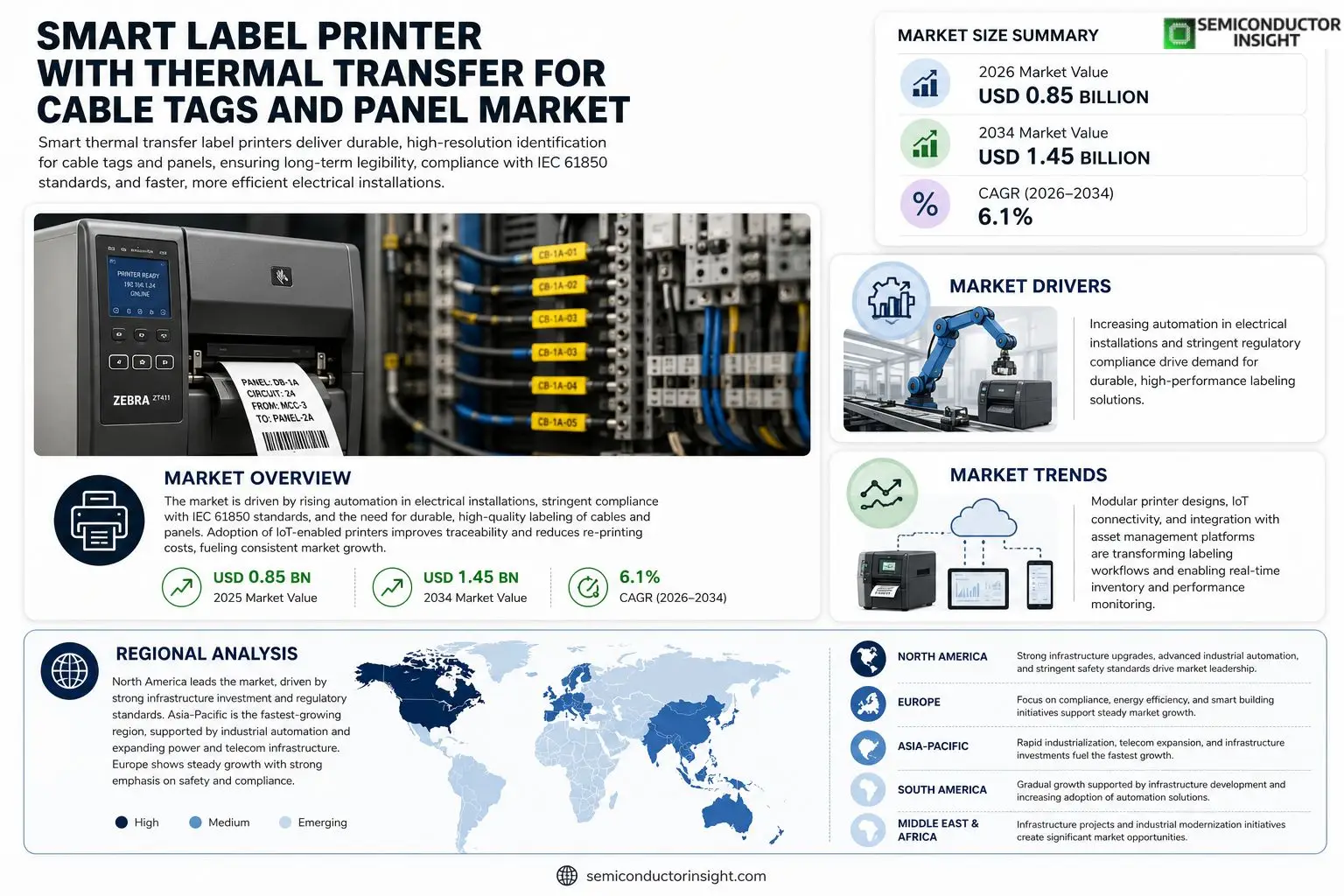

Smart label printer with thermal transfer for cable tags and panel Market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.85 billion in 2025 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period.

A smart label printer equipped with thermal‑transfer technology creates durable, high‑resolution barcodes and alphanumeric data directly on heat‑resistant substrates such as polyester or polyimide films, making it ideal for labeling cable bundles, conduit identifiers, and electrical panels where long‑term legibility is essential.The market is gaining momentum because manufacturers are seeking faster production cycles, while end‑users demand compliance with IEC 61850 standards for power‑grid infrastructure labeling. However, price sensitivity remains a challenge for small‑scale installers, further driving vendors to offer modular solutions that balance cost and performance.

MARKET DRIVERS

Increasing Automation in Electrical Installation

Smart label printer with thermal transfer for cable tags and panel Market is benefiting from a surge in automated wiring processes across industrial facilities. Manufacturers are embracing digital labeling to reduce manual errors and accelerate production cycles.

Regulatory Compliance Demands

Stringent safety standards require durable, legible tags that can withstand harsh environments. Thermal transfer labels provide the necessary resilience, prompting firms to adopt smart printers that comply with IEC and OSHA requirements.

➤ Adoption of IoT‑enabled printers allows real‑time inventory tracking and reduces tag re‑printing costs by up to 30%.

Overall, the convergence of digital workflows, tighter compliance, and cost‑saving technologies fuels robust growth in the market.

MARKET CHALLENGES

High Initial Capital Expenditure

Investing in smart label printers equipped with thermal transfer heads requires significant upfront spending, which can deter small‑to‑mid‑size contractors despite long‑term benefits.

Other Challenges

Limited Material Compatibility

The printers are optimized for specific label films; mismatched substrates may lead to poor adhesion or faded printing, restricting broader adoption.

MARKET RESTRAINTS

Supply Chain Volatility

Recent disruptions in polymer resin and ribbon manufacturing have led to intermittent shortages, driving up material costs and delaying equipment rollout for Smart label printer with thermal transfer for cable tags and panel Market.Additionally, the need for trained technicians to calibrate thermal transfer heads imposes a skill gap, especially in regions where digital labeling is emerging.Maintenance cycles for ribbon cartridges and print heads add recurring operational expenses, which can constrain budgeting for firms with tight margins.

MARKET OPPORTUNITIES

Integration with Asset Management Software

Linking smart label printers to cloud‑based asset management platforms creates opportunities for automated data capture, enabling predictive maintenance and reducing downtime in high‑voltage installations.

Expansion into Renewable Energy Projects

Growth in solar and wind farms drives demand for durable cable tags that can survive outdoor exposure; thermal transfer printers equipped with UV‑stable inks are uniquely positioned to capture this niche.Analysts project a compound annual growth rate of approximately 9% through 2032, reflecting expanding infrastructure spend and broader adoption of smart labeling standards.

Smart label printer with thermal transfer for cable tags and panel Market Trends

Accelerating Adoption Driven by Power‑Grid Standards

Smart label printer with thermal transfer for cable tags and panel Market recorded a valuation of USD 0.85 billion in 2025 and is forecast to reach USD 1.45 billion by 2034, reflecting a compound annual growth rate of approximately 6.1 % over the forecast horizon. The growth is anchored in the printer’s ability to create durable, high‑resolution barcodes on heat‑resistant substrates such as polyester and polyimide films. These attributes satisfy the rigorous IEC 61850 labeling requirements that dominate modern power‑grid infrastructure projects. End‑users increasingly prioritize fast production cycles and long‑term legibility, prompting manufacturers to adopt the technology across cable bundles, conduit identifiers, and electrical panels. The market momentum is further reinforced by regulatory pressure to improve traceability and safety in high‑voltage environments.

Other Trends

Cost Sensitivity and Modular Solutions

While large utilities invest heavily in automated labeling systems, price sensitivity remains a notable barrier for small‑scale installers and regional contractors. Vendors are responding with modular printer architectures that separate core thermal‑transfer engines from optional labeling modules, enabling customers to scale functionality in line with budget constraints. This approach reduces upfront capital expenditure while preserving the ability to upgrade to higher throughput models as demand rises. Additionally, consumable cost management—particularly the pricing of polymeric ribbons and engineered label media—has become a decisive factor in purchasing decisions, driving suppliers to negotiate bulk pricing arrangements and to develop recyclable ribbon technologies that lower total cost of ownership.

Integration with Automated Production Lines

Beyond standalone use, Smart label printer with thermal transfer for cable tags and panel Market is being embedded into broader Industry 4.0 ecosystems. Real‑time data exchange between printers and manufacturing execution systems enables dynamic label content updates, ensuring compliance with evolving project specifications without manual re‑programming. Automated line integration also reduces human error, shortens cycle times, and supports predictive maintenance through built‑in sensor diagnostics. As factories adopt higher levels of connectivity, the demand for printers that can seamlessly interface with PLCs and IoT platforms is expected to rise, solidifying the technology’s role as a critical enabler of efficient, compliant cable and panel identification.

COMPETITIVE LANDSCAPE

Key Industry Players

Smart label printer with thermal transfer for cable tags and panel Market Overview

The Smart label printer market for cable tags and panels is anchored by a few leaders whose breadth of thermal‑transfer platforms and extensive service networks set the competitive baseline. Zebra Technologies commands the largest share, leveraging its ZT series of industrial printers that integrate IoT connectivity and IEC 61850‑compliant label templates. Honeywell’s Intermec line and Brother’s QL‑series provide strong alternatives, offering modular print heads that cater to both high‑volume manufacturers and smaller installation firms. Sato (Toshiba) reinforces the tier with its CL4NX series, emphasizing high‑resolution printing on polyimide substrates that meet the durability requirements of power‑grid environments. These incumbents shape pricing dynamics, driving smaller vendors to adopt cost‑effective, plug‑and‑play designs while still delivering the accuracy demanded by regulatory bodies.Beyond the primary tier, a diverse set of niche players enriches the ecosystem with specialized solutions. TSC Auto ID offers the DA series, prized for its low total cost of ownership and open‑source label software. Primera Technology’s PR‑series focuses on compact desktop units for field technicians. Datamax‑O’Neil (Honeywell) supplies mid‑range printers that blend speed with rugged chassis construction. Cabling Technology Ltd. delivers customized label kits for conduit labeling, while OCEAN (Shanghai) targets the Asian OEM market with high‑speed thermal rollers. Pantum and Datacomp round out the landscape, each delivering entry‑level machines that address price‑sensitive segments without sacrificing barcode fidelity.

List of Key Smart Label Printer with Thermal Transfer for Cable Tags and Panel Companies Profiled

- Zebra Technologies

- Honeywell International

- Brother Industries

- Sato (Toshiba) Corporation

- TSC Auto ID

- Primera Technology

- Datamax‑O’Neil

- Cabling Technology Ltd.

- OCEAN (Shanghai) Co., Ltd.

- Pantum

- Datacomp International

- Citizen Systems

- Label Solutions Inc.

- BlueStar Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Thermal‑transfer printers

These devices dominate the market because they combine reliability with the flexibility to print both alphanumeric data and graphic symbols in a single pass, meeting the rigorous documentation requirements of power‑grid and industrial installations. |

| By Application |

|

Cable tagging

The application drives demand for printers that can produce resilient tags quickly, allowing technicians to reduce downtime and maintain accurate asset records throughout a plant’s lifecycle. |

| By End User |

|

Power utilities

Their emphasis on safety, traceability, and standard‑driven documentation positions smart thermal‑transfer printers as a core enabler of reliable grid operation and maintenance efficiency. |

| By Compliance |

|

IEC 61850 compliance

By aligning printer capabilities with these regulatory expectations, vendors create added value for users who must demonstrate adherence during audits and system certifications. |

| By Integration |

|

IoT‑connected printers

Integration depth is becoming a decisive factor as enterprises look to embed labeling into broader digital workflows, ensuring that label generation aligns with predictive maintenance and analytics initiatives. |

Regional Analysis: North America

United States

The telecommunication sector is a major driver, requiring precise labeling for fiber optic cables, network equipment, and conduit systems. The demand for high-resolution printing and durable labels in harsh environments is particularly strong.

Industrial facilities increasingly rely on smart labeling for cable trays, control panels, and machinery. This ensures efficient maintenance, reduces downtime, and enhances operational safety. The need for chemical resistance and high durability is a key consideration.

The rapid expansion of data centers necessitates sophisticated cable management and labeling. Smart label printers facilitate quick and accurate identification of cables within complex data center environments. This is critical for troubleshooting and capacity planning.

Modern commercial buildings require organized and clearly labeled cable systems for various applications, including power distribution, data networks, and security systems. Aesthetic considerations alongside functionality are important in this segment.

Europe

Europe exhibits a steady growth trajectory in the smart label printer market. Stringent regulatory standards related to safety and cable management across various industries are propelling demand. The emphasis on energy efficiency and smart building initiatives is also contributing to market expansion. While the adoption rate might be slightly slower compared to North America, the overall potential remains significant. The focus on sustainable practices is influencing the choice of label materials.

Asia-Pacific

Asia-Pacific represents a dynamic and rapidly expanding market. The region’s robust manufacturing sector, coupled with increasing infrastructure investments, is driving demand for cable labeling solutions. The growing adoption of automation and industrial IoT applications further fuels market growth. Price sensitivity is a key factor in this region, influencing the types of printers and labels adopted. The market is characterized by intense competition from both domestic and international players.

South America

South America presents a moderate growth opportunity. The expansion of telecommunications networks and industrial infrastructure is creating demand for cable management solutions. However, economic fluctuations and varying levels of industrialization pose challenges. The market is expected to witness gradual growth as investments in infrastructure projects increase. The need for durable labels in challenging environmental conditions is a significant consideration.

Middle East & Africa

The Middle East & Africa region offers promising growth potential. Large-scale infrastructure projects, particularly in the oil & gas and construction sectors, are driving demand for cable labeling. Government initiatives focused on smart city development and industrial modernization are further boosting market expansion. The region’s unique environmental conditions require labels with high resistance to extreme temperatures and humidity.

Report Scope

This market research report provides a comprehensive analysis of the Smart label printer with thermal transfer for cable tags and panel Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart label printer with thermal transfer for cable tags and panel Market?

-> Smart label printer with thermal transfer for cable tags and panel Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034 with a CAGR of 6.1 %.

Which key companies operate in Smart label printer with thermal transfer for cable tags and panel Market?

-> Key players are not disclosed in the provided data.

What are the key growth drivers?

-> Key growth drivers include demand for faster production cycles, compliance with IEC 61850 standards, and the need for durable, long‑term legible labeling solutions.

Which region dominates the market?

-> Regional dominance is not specified in the provided information.

What are the emerging trends?

-> Emerging trends include modular printer designs that balance cost and performance, and increased focus on long‑lasting thermal‑transfer labels for power‑grid infrastructure.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...