Smart Home Semiconductor Market Insights

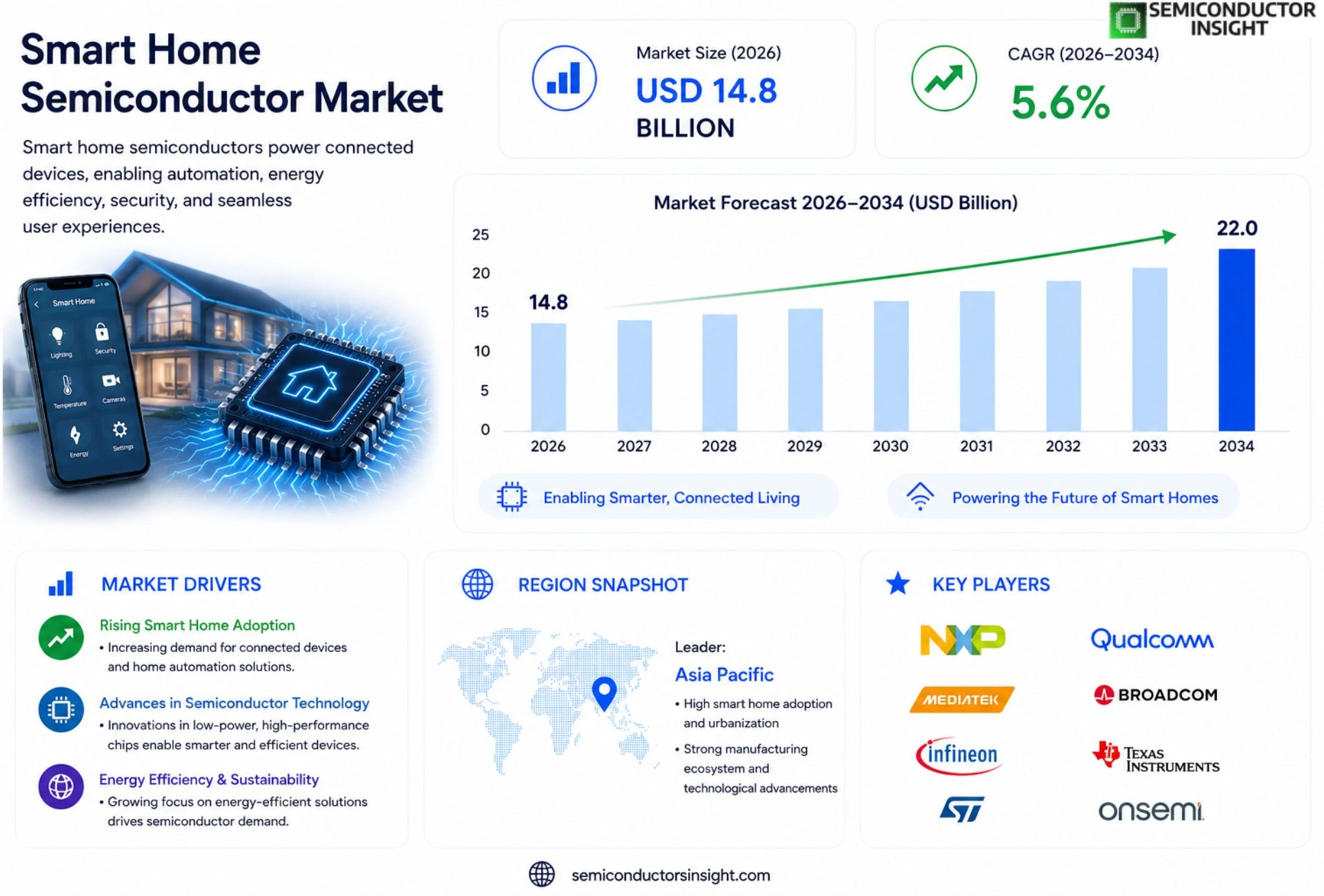

Global Smart Home Semiconductor market size was valued at USD 13.5 billion in 2025. The market is projected to grow from USD 14.8 billion in 2026 to USD 22.0 billion by 2034, exhibiting a CAGR of 5.6% during the forecast period.

Smart home semiconductors are integrated circuits designed to enable connectivity, sensing, processing and power management within residential automation devices such as voice assistants, security cameras, thermostats and lighting controls. These chips typically embed Wi‑Fi/Bluetooth radios, low‑power microcontrollers and AI inference engines that allow edge decision‑making without reliance on cloud latency.

The market is experiencing rapid growth because consumer demand for seamless connected experiences is rising sharply, while manufacturers benefit from economies of scale in IoT chip production. Furthermore, expanding broadband penetration and supportive government incentives for energy‑efficient homes are accelerating adoption. Key players,including Qualcomm Technologies Inc., MediaTek Inc., NXP Semiconductors N.V., Texas Instruments Inc., and STMicroelectronics,are actively launching next‑generation solutions that integrate multi‑protocol radios and on‑chip neural processing to capture emerging opportunities.

MARKET DRIVERS

Rising Adoption of Connected Home Devices

The proliferation of voice‑controlled assistants and IoT hubs has accelerated consumer demand for integrated smart‑home solutions. In 2024, more than 65 % of households in North America and Europe owned at least one connected appliance, driving semiconductor suppliers to expand production capacities.

Advancements in Low‑Power Chip Design

Energy‑efficient architectures enable battery‑operated sensors to run for years without replacement. Power‑saving techniques such as sub‑threshold operation and dynamic voltage scaling have lowered the average power draw of smart‑home controllers by 35 % since 2022, making large‑scale deployments financially viable.

➤ Smart Home Semiconductor Market is projected to exceed $30 billion by 2030, reflecting a compound annual growth rate of roughly 12 %.

These drivers collectively reinforce a positive feedback loop: broader device adoption fuels semiconductor innovation, which in turn reduces costs and further stimulates market expansion.

MARKET CHALLENGES

Integration Complexity across Diverse Protocols

Manufacturers must ensure seamless operation among Zigbee, Thread, Wi‑Fi, and emerging Matter standards. Balancing firmware updates while preserving low latency adds significant engineering overhead, slowing time‑to‑market for new chips.

Other Challenges

Supply‑Chain Constraints

Global wafer shortages and geopolitical tensions have raised component lead times by up to 45 % in 2023. This volatility forces OEMs to hold higher inventory, increasing overall system cost.

MARKET RESTRAINTS

Regulatory and Security Concerns

Data‑privacy regulations such as GDPR and emerging IoT‑specific legislation impose strict encryption and logging requirements. Non‑compliant semiconductor designs risk costly redesigns and market exclusion, particularly in the European Union.

MARKET OPPORTUNITIES

Emerging AI‑Edge Integration

Embedding lightweight neural networks directly onto chips enables real‑time voice recognition and predictive automation without cloud reliance. Edge AI reduces latency by up to 70 % and opens premium pricing tiers for privacy‑focused consumers.

5G‑Enabled Home Connectivity

The rollout of 5G broadband expands bandwidth for high‑resolution video streaming and ultra‑responsive control of smart appliances. Semiconductor vendors that incorporate native 5G modems can capture a significant share of the next wave of connected home upgrades.

Overall, Smart Home Semiconductor Market is positioned to benefit from technological convergence, provided that players navigate integration, supply, and regulatory hurdles effectively.

Smart Home Semiconductor Market Trends

Integrated Multi‑Protocol Chips Drive Adoption

Smart Home Semiconductor Market is being reshaped by the convergence of multiple wireless protocols into single‑chip solutions. By embedding Wi‑Fi, Bluetooth Low Energy, Thread and Zigbee on a unified die, manufacturers reduce board space and simplify bill‑of‑materials. This integration directly supports the consumer expectation for seamless, plug‑and‑play connectivity across voice assistants, security cameras and smart thermostats. At the same time, the rise of high‑speed broadband and increasingly affordable routers lowers latency, making local processing more attractive. Leading vendors such as Qualcomm, MediaTek, NXP, Texas Instruments and STMicroelectronics have released families of chips that combine radio transceivers with low‑power microcontrollers, enabling devices to negotiate the optimal protocol without user intervention.

Other Trends

Edge AI Processing

Edge AI processing is emerging as a decisive sub‑trend within the Smart Home Semiconductor landscape. Modern microcontrollers now incorporate dedicated neural‑engine blocks capable of executing inference for voice wake‑up, anomaly detection in security feeds, and adaptive climate control. By performing these tasks locally, devices avoid round‑trip latency to cloud services and reduce data‑transfer costs, which aligns with privacy‑by‑design principles adopted by many manufacturers. The integration of on‑chip AI also permits continuous learning from sensor data, allowing thermostats to refine heating schedules based on occupancy patterns. Recent silicon releases from major players feature quantized 8‑bit operators that deliver sufficient accuracy for typical home applications while maintaining sub‑milliwatt power budgets, making battery‑powered sensors viable for multi‑year deployments.

Energy‑Efficient Power Management

Energy‑efficient power management remains a core driver for Smart Home Semiconductor Market. Advanced power‑gate architectures and dynamic voltage scaling enable chips to transition between active, sleep and deep‑sleep states in microseconds, extending battery life for remote sensors and reducing overall household energy consumption. Integrated power‑distribution modules now combine DC‑DC converters with load‑monitoring circuits, allowing devices such as smart lighting and motorized blinds to regulate current precisely and report real‑time usage to home energy dashboards. Coupled with growing regulatory emphasis on low‑power design, semiconductor manufacturers are prioritizing ultra‑low quiescent current specifications, often below 1 µA, to meet the expectations of eco‑conscious consumers and architects of net‑zero residential projects.

COMPETITIVE LANDSCAPE

Key Industry Players

Intensifying Innovation and Strategic Positioning Define the Smart Home Semiconductor Competitive Arena

The global smart home semiconductor market is characterized by the strong presence of a handful of dominant technology corporations that command significant market share through continuous R&D investment, broad intellectual property portfolios, and deep integration across the smart home device ecosystem. Qualcomm Technologies Inc. leads with its advanced Wi-Fi and Bluetooth SoC platforms tailored for voice assistants and connected home hubs, while MediaTek Inc. leverages its cost-competitive yet high-performance chipsets to serve a broad base of smart display and IoT device manufacturers. NXP Semiconductors N.V. holds a distinguished position in secure connectivity and edge processing, particularly within smart door locks, energy management systems, and automotive-grade home gateway applications. Texas Instruments Inc. remains a critical supplier of low-power microcontrollers and analog semiconductors extensively deployed in smart thermostats and lighting control systems. STMicroelectronics further strengthens the competitive field with its MEMS sensors and STM32 microcontroller families, which are widely adopted across residential automation platforms globally. These leading players are actively investing in multi-protocol radio integration and on-chip AI inference capabilities to address growing demand for edge intelligence in smart home devices.

Beyond the tier-one leaders, several specialized and emerging players are carving out meaningful niches within the smart home semiconductor landscape. Silicon Laboratories Inc. is recognized for its purpose-built, ultra-low-power wireless SoCs optimized for the Matter and Zigbee protocols critical to home automation interoperability. Nordic Semiconductor has gained strong traction in Bluetooth Low Energy solutions powering smart sensors, wearables, and proximity-based home devices. Espressif Systems has established a cost-efficient footprint with its ESP32 series chips, which are widely deployed by smart home device manufacturers in Asia and beyond. Renesas Electronics Corporation and Microchip Technology Inc. offer robust microcontroller and mixed-signal solutions frequently integrated into residential HVAC, security, and energy monitoring systems. Additionally, Infineon Technologies AG contributes power management and security controller ICs that are integral to smart home gateway and IoT endpoint designs, while Marvell Technology and Broadcom Inc. supply high-throughput Wi-Fi and Ethernet semiconductor solutions for home networking infrastructure underpinning smart home ecosystems.

List of Key Smart Home Semiconductor Companies Profiled

- Qualcomm Technologies Inc.

- MediaTek Inc.

- NXP Semiconductors N.V.

- Texas Instruments Inc.

- STMicroelectronics

- Silicon Laboratories Inc.

- Nordic Semiconductor

- Espressif Systems

- Renesas Electronics Corporation

- Microchip Technology Inc.

- Infineon Technologies AG

- Marvell Technology

- Broadcom Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AI Edge Processors are becoming the core engine of smart‑home devices, delivering on‑device decision making and reducing dependence on external clouds. Their influence is evident across multiple product lines.

|

| By Application |

|

Smart Lighting drives much of the market momentum, as consumers seek flexible ambience and energy‑efficient illumination. Its integration with broader ecosystems creates a compelling user experience.

|

| By End User |

|

Homeowners place the greatest emphasis on ease of use and seamless integration across devices, shaping product road‑maps toward intuitive control. Their preferences influence design priorities.

|

| By Connectivity |

|

Matter (Multi‑protocol) is emerging as the unifying standard that simplifies cross‑brand interoperability, a key driver for wider adoption. Its flexibility reshapes how devices communicate.

|

| By Power Management |

|

Battery‑Optimized designs are crucial for wireless devices that must operate for long periods without frequent charging. They influence component selection and architecture.

|

Regional Analysis: North America

North America

Ongoing advancements in semiconductor technology, such as the development of low-power and high-performance chips, are crucial for the growth of the smart home market. Innovations in materials science and manufacturing processes are enabling smaller, more energy-efficient, and cost-effective semiconductors.

Rising consumer awareness of the benefits of smart home technology, including enhanced convenience, energy savings, and security, is driving demand. Preferences are evolving towards user-friendly interfaces, seamless integration, and robust data privacy features.

The North American smart home semiconductor market is highly competitive, with established players and emerging companies vying for market share. Strategic partnerships and collaborations are becoming increasingly important for companies to gain a competitive edge.

Government regulations related to data privacy, security, and energy efficiency are influencing the development and deployment of smart home semiconductor technologies. Compliance with these regulations is essential for market participants.

Europe

Europe represents a significant and growing market for the Smart Home Semiconductor Market. The region’s emphasis on energy efficiency and sustainable living is a major catalyst for the adoption of smart home devices. Stringent environmental regulations and government incentives are further promoting the growth of this market segment. Key applications include smart thermostats, lighting controls, and energy management systems. The European smart home market is characterized by a diverse range of players, including both established technology companies and innovative startups. Collaboration between industry, academia, and research institutions is fostering technological advancements. The trend towards open standards and interoperability is gaining momentum, enabling seamless integration of devices from different manufacturers. The focus is on creating user-centric solutions that enhance comfort, security, and sustainability.

Asia-Pacific

The Asia-Pacific region is poised for rapid growth in the Smart Home Semiconductor Market. Driven by increasing urbanization, rising disposable incomes, and a growing middle class, the demand for smart home devices is surging. Countries like China, Japan, and South Korea are leading the way in adopting smart home technologies. The region’s robust manufacturing capabilities and strong supply chains are also contributing to market expansion. Key applications include smart appliances, security systems, and voice assistants. The Asia-Pacific smart home market is highly competitive, with a large number of domestic and international players. The focus is on offering affordable and feature-rich solutions to cater to the diverse needs of consumers. The integration of AI and IoT technologies is driving innovation and enhancing the functionality of smart home devices.

South America

South America presents a promising, albeit developing, market for the Smart Home Semiconductor Market. Increasing internet penetration and a growing interest in technology are driving adoption of smart home devices. Urbanization and rising disposable incomes in countries like Brazil and Chile are further fueling market growth. Key applications include smart security systems, lighting controls, and energy management solutions. The South American smart home market is relatively nascent but offers significant growth potential. The focus is on providing affordable and accessible smart home solutions to a wider consumer base. The development of local manufacturing capabilities and the establishment of strong distribution networks are crucial for market expansion.

Middle East & Africa

The Middle East & Africa region represents an emerging market for the Smart Home Semiconductor Market. Rapid urbanization, increasing disposable incomes, and a growing emphasis on smart infrastructure are driving adoption of smart home devices. Countries like the UAE, Saudi Arabia, and South Africa are witnessing significant growth in this segment. Key applications include smart home automation systems, energy management solutions, and security systems. The Middle East & Africa smart home market is characterized by a young and tech-savvy population. The focus is on providing innovative and aesthetically pleasing smart home solutions. Government initiatives promoting smart cities and digital transformation are further contributing to market growth.

Report Scope

This market research report provides a comprehensive analysis of the Smart Home Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Home Semiconductor Market?

-> Smart Home Semiconductor Market was valued at USD 13.5 billion in 2025 and is expected to reach USD 22.0 billion by 2034.

Which key companies operate in Smart Home Semiconductor Market?

-> Key players include Qualcomm Technologies Inc., MediaTek Inc., NXP Semiconductors N.V., Texas Instruments Inc., and STMicroelectronics.

What are the key growth drivers?

-> Key growth drivers include rising consumer demand for seamless connected experiences, economies of scale in IoT chip production, expanding broadband penetration, and supportive government incentives for energy‑efficient homes.

Which region dominates the market?

-> The reference material does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include integration of multi‑protocol radios, on‑chip neural processing, AI inference at the edge, and increasingly power‑efficient semiconductor designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...