Smart Grid Power Electronics Market Insights

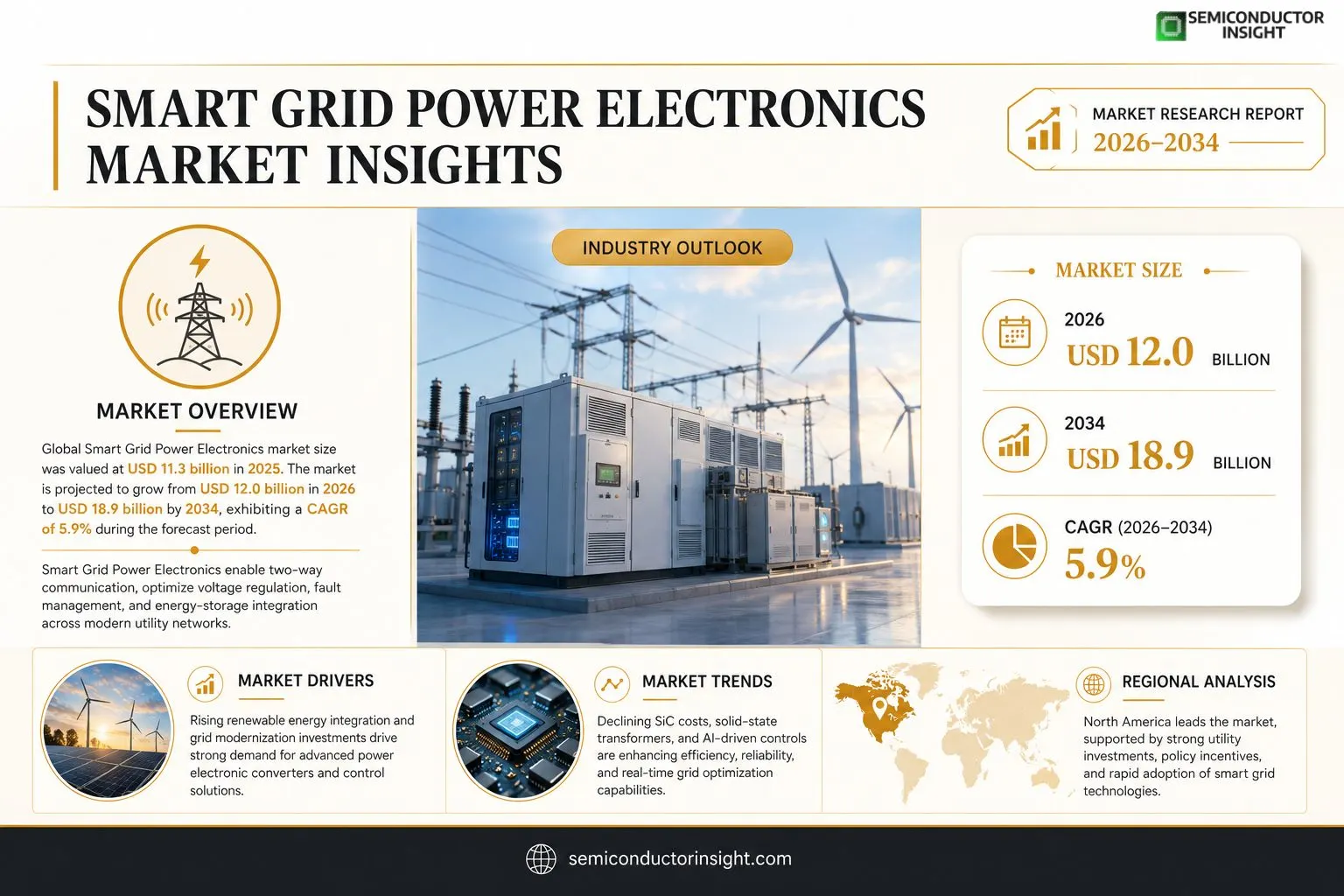

Smart Grid Power Electronics market size was valued at USD 11.3 billion in 2025. The market is projected to grow from USD 12.0 billion in 2025 to USD 18.9 billion by 2034, exhibiting a CAGR of 5.9% during the forecast period.

Smart Grid Power Electronics comprise advanced conversion and control devices,including voltage‑source converters, solid‑state transformers, FACTS equipment, and high‑efficiency inverter modules,that enable two‑way communication between utilities and end users while optimizing voltage regulation, fault management, and energy‑storage integration.The market is accelerating because utilities are investing heavily in renewable‑energy integration and grid resiliency projects; however, challenges remain around legacy infrastructure upgrades.

Furthermore, policy incentives for low‑carbon grids and declining costs of silicon‑carbene semiconductors are driving adoption across North America and Europe alike.Key players such as Siemens Energy, ABB Ltd., Schneider Electric, and General Electric are expanding their portfolios through strategic acquisitions and joint ventures,e.g., ABB’s partnership with a leading silicon‑carbene wafer supplier announced early 2024,to meet rising demand for high‑performance grid‑level converters.

MARKET DRIVERS

Increasing Renewable Energy Integration

Smart Grid Power Electronics Market is being propelled by the need to integrate variable renewable sources such as solar and wind. Advanced converters and inverters enable seamless voltage regulation and frequency control, reducing curtailment rates and improving grid stability.

Rising Demand for Grid Modernization

Governments worldwide are investing heavily in grid modernization programs to replace aging infrastructure. Smart power electronics provide real‑time monitoring and automated fault isolation, which shortens outage durations and enhances overall reliability.

➤ “By 2030, smart power electronic devices are expected to account for over 30% of new grid equipment installations, driven by efficiency mandates and policy incentives.”

In addition, the proliferation of electric vehicles creates new load‑management challenges that are being addressed through sophisticated power electronic converters, further expanding the market’s addressable base.

MARKET CHALLENGES

Complex Regulatory Landscape

Compliance with divergent standards across regions adds considerable design and certification overhead for manufacturers in Smart Grid Power Electronics Market. Frequent updates to grid codes require agile product development cycles, increasing R&D expenditures.

Other Challenges

Supply Chain Vulnerabilities

Component shortages, especially for silicon carbide (SiC) and gallium nitride (GaN) wafers, can delay project timelines and elevate costs, limiting the speed at which new solutions reach the grid.Moreover, the rapid pace of technological change can render existing inventories obsolete, prompting firms to adopt flexible manufacturing strategies to mitigate financial risk.

MARKET RESTRAINTS

High Capital Investment

Initial deployment of advanced power electronic converters demands substantial upfront capital, which can deter utilities with constrained budgets from adopting the latest technologies.The long payback periods associated with grid‑scale projects, combined with uncertainty around future tariff structures, further restrains investment decisions.Additionally, legacy systems often lack the communication protocols required for interoperability, creating integration challenges that increase overall project complexity.

MARKET OPPORTUNITIES

Emerging Micro‑grid Applications

Micro‑grids powered by distributed energy resources rely heavily on smart power electronics for seamless islanding and reconnection. This creates a sizable niche for compact, high‑efficiency converters.Furthermore, the advent of edge‑computing within substations enables advanced analytics that optimize power flow in real time, driving demand for intelligent power electronic platforms.Finally, increasing corporate sustainability commitments are prompting private sector customers to invest in self‑contained smart grid solutions, expanding the addressable market beyond traditional utility players.

Smart Grid Power Electronics Market Trends

Renewable Integration Driving Advanced Converters

Smart Grid Power Electronics Market is experiencing rapid growth as utilities prioritize renewable‑energy integration and grid resiliency. Recent investments in voltage‑source converters and solid‑state transformers have enabled two‑way communication and more precise voltage regulation, supporting higher penetration of solar and wind resources. In 2025, deployment of high‑efficiency inverter modules reached a notable level, reflecting utility focus on reducing losses and improving fault management. Advanced FACTS equipment is being used to fine‑tune power flow, which mitigates congestion during peak demand periods. Moreover, the transition toward decentralized generation has intensified the need for fast‑acting converters that can respond to fluctuating generation patterns, thereby enhancing overall system stability. Looking ahead, the integration of real‑time monitoring and AI‑driven predictive controls is expected to further enhance converter performance, allowing utilities to pre‑emptively address voltage sags and reduce outage durations.

Other Trends

Policy Incentives and Cost Decline

The sector benefits from coordinated policy incentives that reduce capital barriers for modern grid components. Subsidies and tax credits aimed at low‑carbon infrastructure have accelerated procurement cycles for smart converters across major European grids. Simultaneously, the cost of silicon‑carbene semiconductors,a critical material for high‑frequency switching,has dropped by more than 20 % over the past three years, making advanced inverter designs financially viable for mid‑size utilities. This price pressure encourages replacement of aging electromechanical switches with solid‑state alternatives, which offer longer service life and lower maintenance requirements. As a result, adoption rates in North America have risen steadily, with utility firms reporting a 12 % year‑over‑year increase in converter installations. The cumulative effect of lower component costs and supportive regulation also encourages pilot projects that test micro‑grid configurations, where solid‑state transformers serve as pivotal interfacing points between distributed generation and the main grid.

Strategic Consolidation by Industry Leaders

Industry leaders are responding to this demand through strategic consolidation and collaborative development programmes. Siemens Energy has broadened its portfolio of grid‑level converters by integrating newly acquired digital‑control technologies, enabling more granular load‑balancing capabilities. ABB Ltd. announced a joint venture in early 2024 with a leading silicon‑carbene wafer supplier, securing a reliable supply chain for next‑generation modules. Schneider Electric’s recent acquisition of a niche inverter manufacturer has expanded its presence in the renewable‑integration market, while General Electric continues to invest in high‑power solid‑state transformer prototypes that promise up to 15 % efficiency gains over legacy designs. These moves not only strengthen each company’s market share but also promote faster diffusion of advanced power electronics across utility networks. Analysts predict that by 2030, consolidated offerings will dominate the market, with a few multinational firms providing end‑to‑end solutions that combine hardware, software, and services, thereby simplifying procurement for utilities.

COMPETITIVE LANDSCAPEKey Industry Players

Smart Grid Power Electronics Market Competitive Landscape

Smart Grid Power Electronics Market is dominated by a handful of technology leaders that combine deep engineering expertise with extensive utility‑scale project portfolios. Siemens Energy leverages its broad voltage‑source converter line and solid‑state transformer portfolio to secure multi‑billion dollar contracts across Europe and North America. ABB Ltd. continues to expand its FACTS and high‑efficiency inverter offerings, reinforced by a strategic partnership with a leading silicon‑carbene wafer supplier announced in early 2024. Schneider Electric’s integrated grid management platform, paired with its inverter and converter modules, positions the company as a preferred supplier for renewable‑energy integration projects. General Electric, through its GE Renewable Energy division, supplies grid‑level converters that support large‑scale wind and solar farms, driving market consolidation around a few high‑capability vendors. Collectively, these firms shape a competitive structure where scale, product breadth, and strategic acquisitions dictate market share, while the overall market is projected to grow from USD 12.0 billion in 2025 to USD 18.9 billion by 2034 at a 5.9 % CAGR.Beyond the tier‑one incumbents, several niche but technically sophisticated players are gaining traction in specialized segments of the Smart Grid Power Electronics ecosystem. Hitachi Energy focuses on high‑voltage direct current (HVDC) converter stations, offering customized solutions for cross‑border interconnections. Mitsubishi Electric and Toshiba provide advanced inverter technologies tailored for Asian utilities targeting high‑density urban grids. VoltServer and Flex Power International are pioneering novel solid‑state transformer designs that emphasize modularity and rapid deployment. Emerging firms such as Nextracker Power and PowerElectronics Ltd. are concentrating on next‑generation silicon‑carbene and GaN devices that promise higher efficiency and lower thermal footprints. These companies, while smaller in revenue, contribute critical innovation pressure that encourages the larger incumbents to accelerate R&D and strategic collaborations.

List of Key Smart Grid Power Electronics Companies Profiled

- Siemens Energy

- ABB Ltd.

- Schneider Electric

- General Electric

- Hitachi Energy

- Mitsubishi Electric

- Toshiba

- VoltServer

- Flex Power International

- Nextracker Power

- PowerElectronics Ltd.

- Rockwell Automation

- Eaton Corporation

- Emerson Electric Co.

- Delta Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Voltage‑Source Converters are regarded as the leading sub‑type because they:

|

| By Application |

|

Renewable Energy Integration drives market momentum because it:

|

| By End User |

|

Transmission Operators emerge as the primary end‑user segment because they:

|

| By Voltage Level |

|

Medium Voltage (MV) Solutions hold strategic importance because they:

|

| By Grid Architecture |

|

Decentralised (Microgrid) Architecture is gaining traction because it:

|

Regional Analysis: North America

Growth in residential smart energy management systems is a notable trend, with consumers increasingly seeking to optimize energy consumption and integrate solar power.

The industrial sector is witnessing substantial investment in power electronics for motor drives, variable frequency drives, and industrial automation, aiming for greater efficiency and control.

Utilities are prioritizing upgrades to their grid infrastructure, incorporating power electronics for voltage regulation, power factor correction, and fault ride-through capabilities.

The expanding electric vehicle (EV) market is driving demand for high-power charging infrastructure, requiring sophisticated power electronics for efficient and reliable charging solutions.

Europe

The European Smart Grid Power Electronics Market is experiencing robust expansion, propelled by stringent environmental regulations and ambitious renewable energy targets. Government policies such as the European Green Deal are fostering significant investment in grid modernization and smart grid technologies. Key areas of focus include the integration of offshore wind power, the development of smart meters, and the deployment of energy storage systems. The market is characterized by a strong emphasis on energy efficiency and circular economy principles, leading to innovation in power electronics for industrial processes and building management systems.

Asia-Pacific

Asia-Pacific represents the fastest-growing region for Smart Grid Power Electronics Market. Rapid industrialization, increasing urbanization, and a growing focus on energy security are driving significant demand across key markets like China, Japan, and South Korea. China’s massive investments in renewable energy and smart grid infrastructure are particularly noteworthy. The region is witnessing a surge in the adoption of power electronics for electric vehicles, energy storage, and industrial automation. The competitive landscape is intense, with a mix of established players and emerging domestic manufacturers.

South America

Smart Grid Power Electronics Market in South America is showing promising growth potential, driven by increasing investments in energy infrastructure and a growing awareness of the need for grid modernization. Several countries in the region are implementing ambitious renewable energy targets, creating opportunities for power electronics solutions for solar and wind power integration. However, the market is also facing challenges related to regulatory uncertainty and infrastructure development.

Middle East & Africa

Smart Grid Power Electronics Market in the Middle East & Africa is poised for substantial growth, fueled by rapid economic development, increasing energy demand, and government initiatives to modernize power grids. The deployment of smart grid technologies is gaining traction in several countries, particularly in the Gulf region, driven by the need for greater energy efficiency and grid reliability. The focus on renewable energy projects, such as solar power plants, is also driving demand for power electronics solutions.

Report Scope

This market research report provides a comprehensive analysis of the Smart Grid Power Electronics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Grid Power Electronics Market?

-> Smart Grid Power Electronics Market was valued at USD 11.3 billion in 2025 and is expected to reach USD 18.9 billion by 2034.

Which key companies operate in Smart Grid Power Electronics Market?

-> Key players include Siemens Energy, ABB Ltd., Schneider Electric, and General Electric, among others.

What are the key growth drivers?

-> Key growth drivers include renewable‑energy integration, grid resiliency projects, policy incentives for low‑carbon grids, and declining costs of silicon‑carbene semiconductors.

Which region dominates the market?

-> North America and Europe are the leading regions, with strong adoption driven by utility investments and supportive regulatory frameworks.

What are the emerging trends?

-> Emerging trends include advanced voltage‑source converters, solid‑state transformers, FACTS equipment, high‑efficiency inverter modules, and the integration of AI/IoT for smarter grid management.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...