MARKET INSIGHTS

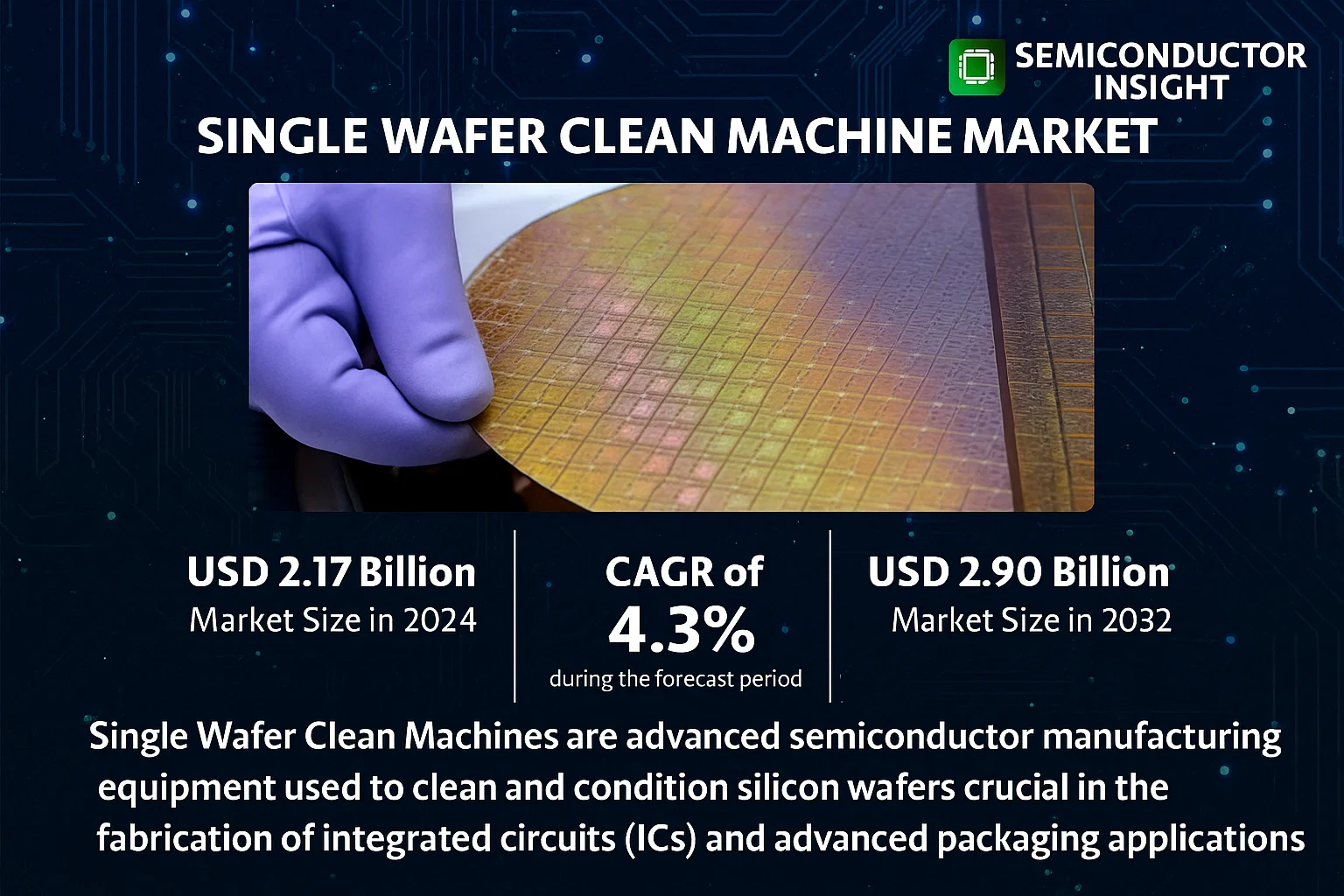

Global Single Wafer Clean Machine Market size was valued at USD 2.17 billion in 2024 and is projected to reach USD 2.90 billion by 2032, exhibiting a CAGR of 4.3% during the forecast period.

Single Wafer Clean Machines are advanced semiconductor manufacturing equipment used to clean and condition silicon wafers with high precision. They are crucial in the fabrication of integrated circuits (ICs) and advanced packaging applications. The machines utilize a combination of chemical, mechanical, and thermal processes to remove contaminants, particles, and residues from the wafer surface, ensuring high yields and device performance.

The market growth is primarily driven by the increasing demand for semiconductors across various end-use industries, including consumer electronics, automotive, and industrial automation. The ongoing miniaturization of semiconductor devices and the transition to more advanced process nodes, such as those below 10nm, necessitate highly effective cleaning processes, thereby boosting the demand for advanced single wafer cleaning equipment. Additionally, the rise of advanced packaging techniques, including 2.5D and 3D packaging, which require extremely clean surfaces for reliable interconnects, is contributing to market expansion.

Moreover, investments in new semiconductor fabrication plants (fabs), particularly in regions like the United States and Asia-Pacific, are creating new opportunities for equipment suppliers. The CHIPS Act in the United States, for instance, is expected to catalyze significant domestic investment in semiconductor manufacturing, subsequently driving demand for associated equipment, including cleaning systems.

MARKET DRIVERS

Advancements in Semiconductor Technology Nodes

The relentless push towards smaller semiconductor technology nodes below 5nm is a primary driver for the Single Wafer Clean Machine market. As feature sizes shrink, traditional batch cleaning methods become inadequate for removing nanometer-scale contaminants without causing damage or pattern collapse. Single Wafer Clean (SWC) systems offer superior process control and gentler handling, which is critical for high-value advanced logic and memory chips. This trend is accelerating demand as foundries and IDMs ramp up production of cutting-edge devices.

Increasing Demand for 3D NAND and Advanced Packaging

The complexity of 3D NAND flash memory, with its high-aspect-ratio structures, and the proliferation of advanced packaging solutions like chiplets and 3D integration require highly precise and effective cleaning at various stages of fabrication. SWC machines are essential for cleaning deep trenches and delicate interconnect structures without leaving residues or inducing defects, directly supporting the growth of these high-density memory and heterogeneous integration markets.

➤ The global market for Single Wafer Clean equipment is projected to grow at a CAGR of approximately 7-9% over the next five years, fueled by massive investments in new semiconductor fabs worldwide.

Furthermore, the expansion of the Internet of Things (IoT), 5G infrastructure, and artificial intelligence (AI) applications is creating sustained demand for semiconductors, which in turn increases the requirement for sophisticated wafer cleaning solutions. The need for higher yields and lower defect densities in these high-performance chips makes the adoption of SWC technology a strategic imperative for manufacturers.

MARKET CHALLENGES

High Capital Expenditure and Cost of Ownership

Single Wafer Clean machines represent a significant capital investment compared to batch cleaning systems. Their higher throughput per tool and advanced features, including multiple chemical stations and sophisticated drying technologies like Marangoni or IPA vapor drying, contribute to a substantial total cost of ownership. This can be a barrier to adoption for smaller fabrication facilities or those producing less demanding nodes where batch processing remains economically viable.

Other Challenges

Process Complexity and Integration

Integrating SWC tools into existing fabrication lines can be challenging. They require precise coordination with upstream and downstream processes and often need customization for specific fab layouts and process flows. The complexity of managing multiple chemical recipes and ensuring consistent performance across thousands of wafers adds to the operational challenges.

Stringent Chemical and Environmental Regulations

The use of aggressive chemicals, such as SC-1 and SC-2 solutions, along with large volumes of ultra-pure water (UPW), poses environmental and safety challenges. Compliance with increasingly strict regulations regarding chemical handling, waste disposal, and water consumption requires additional investment in abatement systems and sustainable practices, increasing operational costs.

MARKET RESTRAINTS

Maturity of Alternative Cleaning Technologies

While SWC systems are superior for advanced nodes, well-established and cost-effective batch wet bench technology continues to dominate the market for larger technology nodes and certain less critical cleaning steps. The proven reliability and lower initial cost of batch systems act as a significant restraint, limiting the total available market for SWC equipment to primarily the most advanced semiconductor manufacturing segments.

Cyclical Nature of the Semiconductor Industry

The Single Wafer Clean Machine market is highly susceptible to the boom-and-bust cycles of the global semiconductor industry. During periods of downturn or overcapacity, semiconductor manufacturers drastically reduce capital expenditures, delaying or canceling orders for new equipment. This cyclicality creates uncertainty and can lead to volatile revenues for equipment suppliers, restraining steady market growth.

MARKET OPPORTUNITIES

Expansion into New Application Areas

There is a significant opportunity to expand the application of Single Wafer Clean technology beyond traditional front-end-of-line (FEOL) cleaning. This includes backend-of-line (BEOL) cleaning for advanced packaging, cleaning for compound semiconductors (like GaN and SiC) used in power electronics and RF devices, and applications in the burgeoning MEMS and sensor markets. These segments require the precision and damage-free processing that SWC systems provide.

Development of Sustainable and Efficient Solutions

The growing emphasis on sustainability presents a major opportunity for innovation. Developing SWC systems that significantly reduce chemical consumption, minimize ultra-pure water (UPW) usage through recycling loops, and employ greener chemistry can create a strong competitive advantage. Manufacturers that lead in eco-efficient technology will be well-positioned to meet the industry’s future environmental standards and cost reduction pressures.

Integration with Industry 4.0 and AI

The integration of Industrial Internet of Things (IIoT) sensors, real-time data analytics, and artificial intelligence for predictive maintenance and process optimization is a key future opportunity. Smart SWC machines that can self-monitor, predict failures, and automatically adjust recipes for optimal yield can command a premium and create new service-based revenue models for equipment vendors, moving beyond mere hardware sales.

Single Wafer Clean Machine Market Trends

Sustained Growth Fueled by Semiconductor Demand

The global Single Wafer Clean Machine market is on a trajectory of steady expansion, driven by the incessant demand for advanced semiconductor devices. Valued at US$ 2174 million in 2024, the market is projected to reach US$ 2905 million by 2032, reflecting a Compound Annual Growth Rate (CAGR) of 4.3% during the forecast period. This growth is underpinned by continuous investment in semiconductor fabrication facilities worldwide, particularly for manufacturing logic, memory, and advanced packaging applications where contamination control is critical. The increasing complexity of semiconductor nodes, moving towards 3nm and below, necessitates more precise and efficient cleaning processes, directly benefiting the adoption of single-wafer cleaning technology.

Other Trends

Market Consolidation and Regional Dominance

The competitive landscape of the Single Wafer Clean Machine market is highly concentrated. The global top three companies—SCREEN Semiconductor Solutions, TEL, and Lam Research—collectively hold a market share exceeding 82%. This dominance underscores the high barriers to entry, including significant R&D investment and deep technological expertise required to meet the stringent purity standards of leading foundries. Regionally, China has emerged as the largest market, accounting for approximately 30% of the global share, fueled by massive government and private investment in domestic semiconductor production. It is followed by North America and Japan, with shares of about 18% and 17% respectively, as these regions remain hubs for leading-edge semiconductor research and manufacturing.

Segmentation by Cavity and Application

Market segmentation reveals key trends in product configuration and usage. By the number of cavities, machines are categorized into 8 cavities and below, 8-12 cavities, and more than 12 cavities, each catering to different throughput and process flexibility requirements. In terms of application, the market is divided into Integrated Circuit manufacturing, Advanced Packaging, and Others. The Advanced Packaging segment is experiencing robust growth, driven by the proliferation of heterogeneous integration and chiplets, which require meticulous cleaning processes to ensure package integrity and performance.

Technological Advancements and Future Outlook

The evolution of Single Wafer Clean Machine technology focuses on enhancing performance while reducing chemical and water consumption, aligning with sustainability goals. Innovations include advanced megasonic and cryogenic aerosol cleaning techniques to address nanoscale contamination without damaging delicate device structures. As the semiconductor industry pushes the boundaries of miniaturization, the demand for high-purity, single-wafer processing that minimizes defects and cross-contamination will continue to be a primary driver for this market, ensuring its vital role in the global electronics supply chain.

COMPETITIVE LANDSCAPE

Key Industry Players

An Oligopolistic Market Dominated by a Handful of Global Leaders

The global Single Wafer Clean Machine market is characterized by a high degree of consolidation, with the top three companies—SCREEN Semiconductor Solutions, Tokyo Electron Limited (TEL), and Lam Research—commanding a combined market share exceeding 82%. This concentration of power highlights significant barriers to entry, driven by the intensive R&D required for developing advanced cleaning technologies and the necessity for robust global service and support networks. SCREEN Semiconductor Solutions is often recognized as a leading force, with a strong product portfolio spanning various cavity configurations. The competition is primarily technology-driven, focusing on achieving superior particle removal efficiency, minimizing chemical usage and DI water consumption, and ensuring high throughput for advanced semiconductor nodes in applications like integrated circuit manufacturing and advanced packaging.

Beyond the dominant trio, several other significant players compete by carving out specialized niches or focusing on specific geographic markets. Companies such as SEMES and Shibaura Mechatronics hold notable positions, often leveraging strengths in specific cleaning process steps or materials. In the critical China market, which accounts for approximately 30% of global demand, domestic manufacturers like NAURA and Kingsemi are increasingly prominent. These regional champions benefit from local supply chains and supportive government policies aimed at semiconductor self-sufficiency. Other players, including SEMIX Semiconductor and MTK Co., Ltd., compete by offering cost-effective solutions, targeting mature process technologies, or serving the market for machines with lower cavity counts.

List of Key Single Wafer Clean Machine Companies Profiled

- SCREEN Semiconductor Solutions

- Tokyo Electron Limited (TEL)

- Lam Research

- SEMES

- Semix Semiconductor

- Shibaura Mechatronics

- NAURA

- KINGSEMI

- MTK Co., Ltd

- DNS (Dainippon Screen Manufacturing Co., Ltd.)

- Applied Materials, Inc.

- KLA Corporation

- Akrion Systems

- Modutek Corporation

- PSK Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

More Than 12 Cavities is recognized as the leading segment, primarily due to its superior throughput capabilities which are essential for high-volume semiconductor manufacturing fabs seeking to maximize production efficiency. This segment’s dominance is driven by the industry’s relentless pursuit of economies of scale, where processing multiple wafers simultaneously significantly reduces the cost per wafer. The technological sophistication required for these multi-cavity systems also allows for highly uniform cleaning processes, a critical factor for advanced node fabrication where even minor inconsistencies can lead to yield loss. |

| By Application |

|

Integrated Circuit fabrication stands as the dominant application segment, constituting the primary demand driver for single wafer clean machines. This leadership is anchored in the extreme precision and particle control required at numerous stages of IC manufacturing, from front-end to back-end processes. The perpetual miniaturization of semiconductor devices, moving towards 3nm nodes and beyond, demands cleaning technologies that can remove contaminants at an atomic level without damaging intricate nanostructures. The growth in demand for logic, memory, and microprocessor chips directly fuels the adoption of advanced cleaning systems to ensure high yields and device reliability. |

| By End User |

|

Foundries represent the leading end-user segment, driven by their central role in the global semiconductor supply chain and their massive capital expenditure on cutting-edge fabrication facilities. Major foundries are in a constant race to adopt next-generation process technologies, which necessitates the deployment of the most advanced single wafer clean equipment to maintain competitive yields and process integrity. The pure-play foundry model, serving a diverse clientele with stringent quality requirements, creates a consistent and high-volume demand for reliable and precise cleaning solutions to handle a wide variety of chip designs and process flows. |

| By Cleaning Technology |

|

Wet Chemical Cleaning remains the foundational and leading technology segment due to its proven effectiveness, versatility, and maturity in removing a wide range of contaminants, including particles, organic residues, and metallic ions. Its dominance is sustained by continuous innovation in chemical formulations that enhance selectivity and reduce environmental impact, such as the development of dilute chemistries. While newer technologies are emerging for specific challenging applications, wet chemical cleaning’s ability to be seamlessly integrated into complex process flows and its cost-effectiveness for many standard cleaning steps ensure its continued preeminence in semiconductor fabs worldwide. |

| By Wafer Size |

|

300mm wafers constitute the unequivocal leading segment, representing the current industry standard for high-volume manufacturing of advanced semiconductors. The transition to 300mm was driven by substantial gains in productivity and cost reduction per die, making it the backbone of modern logic and memory chip production. The vast majority of new fab investments and capacity expansions are focused on 300mm technology, creating sustained demand for compatible single wafer clean machines. While 200mm equipment remains vital for legacy and specialized applications, the technological roadmap and economic drivers firmly anchor the 300mm segment as the dominant force in the market. |

Regional Analysis: Single Wafer Clean Machine Market

Taiwan and South Korea represent the epicenter of demand, driven by their world-leading pure-play foundries and dominant memory manufacturers. The transition to sub-5nm logic nodes and advanced DRAM/NAND structures creates a continuous need for highly precise single wafer cleaning tools that can handle complex geometries and delicate structures without damage, making technological adoption here exceptionally high.

China’s aggressive investments in building a self-sufficient semiconductor supply chain are a major growth driver. Numerous new fabs are being equipped with advanced manufacturing tools, including single wafer cleaners, to support both mature and leading-edge node production. This significant capacity expansion, supported by national policies, ensures sustained demand growth for cleaning equipment within the region.

Japan maintains a strong presence with its focus on specialty semiconductors, image sensors, and power devices, which require tailored cleaning processes. Southeast Asian nations are growing as important sites for assembly, testing, and packaging, creating demand for cleaning equipment used in these back-end processes, complementing the front-end demand from other parts of the region.

The concentration of semiconductor manufacturing in Asia-Pacific has fostered a robust local ecosystem of equipment suppliers, service providers, and R&D centers. This proximity allows for closer collaboration between equipment makers and chip manufacturers, accelerating the development and optimization of single wafer cleaning processes tailored to specific regional production challenges and technological roadmaps.

North America

North America holds a significant position in the Single Wafer Clean Machine market, primarily driven by the presence of major fabless semiconductor companies and Integrated Device Manufacturers (IDMs) that demand cutting-edge fabrication technology. While a large portion of high-volume manufacturing occurs overseas, leading-edge R&D and pilot production lines in the US require the most advanced single wafer cleaning solutions. Furthermore, substantial government initiatives, such as the CHIPS Act, are incentivizing the onshoring of advanced semiconductor manufacturing, which is expected to create new, sustained demand for these precision cleaning tools. The market is characterized by a focus on innovation, with equipment suppliers working closely with research institutions and leading chip designers to develop next-generation cleaning technologies for future node requirements.

Europe

The European market for Single Wafer Clean Machines is anchored by a strong presence of automotive, industrial, and research-oriented semiconductor manufacturers. The region specializes in producing chips for demanding applications like automotive power electronics, sensors, and microcontrollers, which require highly reliable and contamination-free manufacturing processes. This drives demand for robust single wafer cleaning equipment. Significant public and private investments, such as the European Chips Act, aim to bolster the region’s semiconductor sovereignty, which includes supporting advanced manufacturing capabilities. The market growth is further supported by leading research organizations that push the boundaries of semiconductor technology, creating a need for specialized cleaning processes for novel materials and device architectures.

South America

The South American market for Single Wafer Clean Machines is currently a smaller, niche segment compared to other regions. Demand is primarily linked to academic and research institutions, as well as a limited number of facilities focused on analog and discrete semiconductors. There is minimal large-scale, leading-edge semiconductor fabrication in the region. However, growing technological adoption across various industries and gradual investments in local electronics manufacturing could potentially create future opportunities for market expansion. The focus for equipment suppliers in this region is often on supporting specialized applications and providing service for existing installed bases rather than high-volume sales.

Middle East & Africa

The Middle East & Africa region represents an emerging and strategically developing market. While traditionally not a major hub for semiconductor fabrication, there are growing initiatives, particularly in the Middle East, to diversify economies and invest in high-technology sectors. This includes plans for establishing semiconductor manufacturing capabilities. Such long-term strategic investments could eventually generate demand for supporting equipment like single wafer cleaners. Currently, the market is very limited, with demand concentrated in research and small-scale specialty production. The region’s potential lies in future greenfield projects aiming to create a local technology ecosystem.

Report Scope

This market research report provides a comprehensive analysis of the Single Wafer Clean Machine Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Single Wafer Clean Machine Market?

-> Single Wafer Clean Machine Market size was valued at USD 2.17 billion in 2024 and is projected to reach USD 2.90 billion by 2032, exhibiting a CAGR of 4.3% during the forecast period.

Which key companies operate in Single Wafer Clean Machine Market?

-> Key players include SCREEN Semiconductor Solutions, TEL, Lam Research, SEMES, Semix Semiconductor, Shibaura Mechatronics, NAURA, KINGSEMI, and MTK Co., Ltd, among others. The global top three companies hold a market share of over 82%.

What are the key growth drivers?

-> Key growth drivers include advancements in semiconductor manufacturing, increasing demand for integrated circuits and advanced packaging, and technological innovation in wafer cleaning processes.

Which region dominates the market?

-> China is the largest market, with a share of about 30%, followed by North America (18%) and Japan (17%).

What are the emerging trends?

-> Emerging trends include the development of higher cavity machines, precision cleaning for advanced nodes, and integration with other fabrication tools for improved yield and efficiency.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...