MARKET INSIGHTS

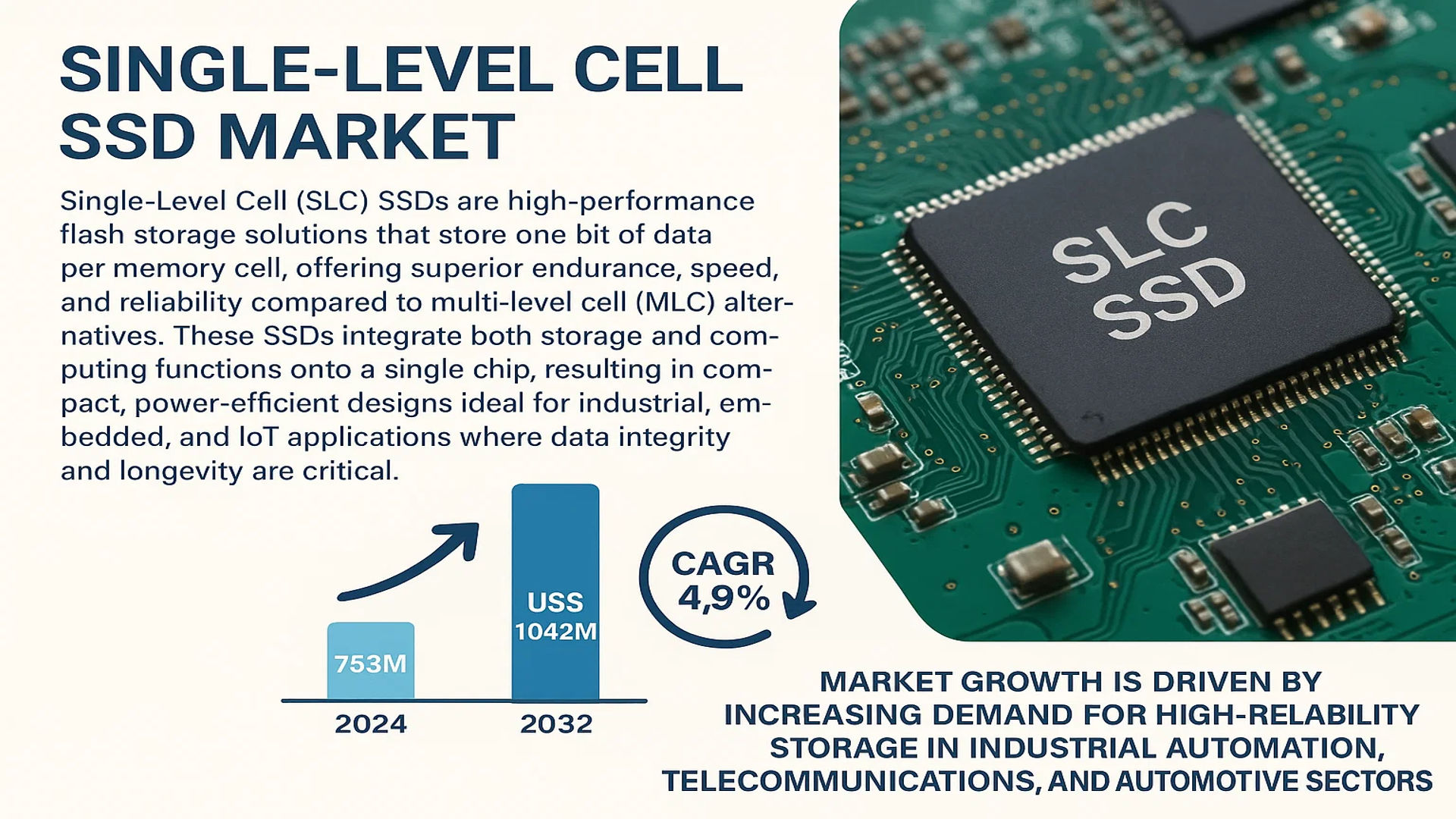

The global Single-Level Cell SSD Market was valued at 753 million in 2024 and is projected to reach US$ 1042 million by 2032, at a CAGR of 4.9% during the forecast period.

Single-Level Cell (SLC) SSDs are high-performance flash storage solutions that store one bit of data per memory cell, offering superior endurance, speed, and reliability compared to multi-level cell (MLC) alternatives. These SSDs integrate both storage and computing functions onto a single chip, resulting in compact, power-efficient designs ideal for industrial, embedded, and IoT applications where data integrity and longevity are critical.

The market growth is driven by increasing demand for high-reliability storage in industrial automation, telecommunications, and automotive sectors. While enterprise storage dominates adoption, emerging applications in edge computing and 5G infrastructure present new opportunities. Leading manufacturers like Samsung, Western Digital, and Micron continue to innovate, with recent developments focusing on enhanced durability and lower power consumption to meet evolving industry demands.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Performance Storage Solutions to Accelerate Market Growth

The global Single-Level Cell (SLC) SSD market is experiencing strong growth driven by the increasing need for high-performance, low-latency storage solutions across industries. SLC NAND flash technology offers superior endurance and faster read/write speeds compared to multi-level cell (MLC) or triple-level cell (TLC) alternatives, making it ideal for mission-critical applications. With enterprises generating approximately 2.5 quintillion bytes of data daily, the demand for reliable storage options that can handle intensive workloads continues to rise. SLC SSDs provide write cycles exceeding 100,000 per cell compared to just 3,000-5,000 for TLC SSDs, offering significantly better performance for industrial, aerospace, and IoT applications where data integrity is paramount.

Explosion of IoT and Edge Computing Applications to Fuel Adoption

The proliferation of IoT devices and edge computing infrastructure represents a major growth driver for SLC SSD technology. With over 30 billion connected IoT devices projected globally by 2025, there is increasing need for rugged, durable storage that can operate in harsh environments while maintaining data integrity. SLC SSDs offer superior endurance in extreme temperatures ranging from -40°C to 85°C, making them ideal for industrial IoT deployments. Their single-bit-per-cell architecture provides more consistent performance under varied workloads compared to multi-bit cells. This reliability advantage is critical for applications like autonomous vehicles, smart manufacturing systems, and remote telemetry installations where data loss can have significant consequences.

Shift Toward Ruggedized Data Storage in Mission-Critical Systems

Defense, aerospace, and medical sectors are increasingly adopting SLC SSDs due to their reliability advantages in extreme operating conditions. The technology’s resistance to electromagnetic interference and vibration makes it suitable for military avionics, where data integrity directly impacts operational safety. In the medical field, SLC SSDs provide the reliability needed for critical patient monitoring systems and imaging equipment. The market is further benefiting from the transition toward higher capacity SLC solutions, with leading manufacturers now offering up to 1TB configurations in industrial-grade form factors. This capacity expansion addresses one of the traditional limitations of SLC technology while maintaining its performance advantages.

MARKET RESTRAINTS

High Costs of SLC Technology to Limit Mass Adoption

Despite its performance advantages, SLC NAND flash remains significantly more expensive than competing technologies, with per-gigabyte costs approximately 3-5 times higher than TLC alternatives. This pricing premium stems from its lower density architecture and more complex manufacturing processes. For consumer applications and general enterprise storage where absolute reliability isn’t critical, many organizations find it difficult to justify the cost differential. The market is further constrained by the ongoing trade-off between capacity and price—while SLC offers superior endurance, comparable MLC solutions often provide 2-4 times the storage capacity at similar price points for many applications.

Emergence of Alternative Storage Technologies to Create Competitive Pressure

The SLC SSD market faces increasing competition from emerging storage technologies offering comparable reliability at lower costs. 3D XPoint memory, for instance, delivers endurance characteristics approaching SLC levels while providing better performance for certain workloads. Additionally, improvements in error correction and wear leveling algorithms have allowed MLC and TLC NAND to achieve reliability levels suitable for many industrial applications that previously required SLC. Enterprise customers are increasingly evaluating these alternatives, particularly when balancing performance requirements against budget constraints. This competitive landscape creates pricing pressure for SLC solutions even in traditional stronghold markets.

MARKET CHALLENGES

Supply Chain Constraints to Impact Manufacturing Capacity

The semiconductor industry’s ongoing supply chain challenges present significant obstacles for SLC SSD production. SLC NAND requires specialized fabrication processes that are increasingly difficult to maintain as manufacturers prioritize high-density TLC and QLC production for mainstream markets. Allocating sufficient wafer capacity for SLC production has become more challenging, particularly as demand grows for industrial and embedded applications. This constrained supply situation is exacerbated by long lead times for specialized components used in industrial-grade SSDs, including extended temperature-range controllers and ruggedized packaging materials.

Technical Hurdles in Scaling SLC NAND Density

While SLC SSDs offer clear reliability advantages, the technology faces inherent scaling challenges that limit its competitiveness in capacity-driven applications. The single-bit-per-cell architecture means capacity improvements require significant advancements in lithography and cell shrinking techniques. Current fabrication nodes for SLC NAND have largely stabilized at 15-19nm processes, while multi-bit cells continue advancing to smaller nodes. This technical limitation makes it difficult for SLC technology to keep pace with the exponential growth in data storage requirements for many modern applications, forcing users to consider alternative architectures where absolute data integrity isn’t mission-critical.

MARKET OPPORTUNITIES

Expansion of Industrial Automation to Create New Growth Avenues

The rapid growth of Industry 4.0 and industrial automation presents significant opportunities for SLC SSD adoption. Modern smart factories require storage solutions that can withstand harsh operating environments while ensuring continuous operation. SLC technology is particularly well-suited for programmable logic controllers, industrial PCs, and robotics systems where downtime is extremely costly. Market research indicates that manufacturing facilities implementing automation solutions are willing to pay premium prices for components with proven reliability. This positions SLC SSDs as attractive solutions despite their higher costs compared to commercial-grade alternatives.

Development of Specialized Form Factors for Emerging Applications

Manufacturers are exploring opportunities in developing specialized SLC SSD solutions tailored for next-generation applications. Ruggedized modules for automotive systems, ultra-compact designs for UAVs, and radiation-hardened variants for space applications represent promising growth segments. The ability to customize controllers and firmware for specific industry requirements allows SLC technology to maintain competitiveness despite pricing pressures. Recent product launches include SLC SSDs with specialized encryption for defense applications and models featuring extended retention periods for archival storage—both areas where multi-bit cells struggle to meet reliability requirements.

Advancements in Controller Technology to Enhance Value Proposition

Innovations in SSD controller technology are helping overcome some traditional limitations of SLC SSDs. Next-generation controllers with enhanced error correction capabilities and improved wear leveling algorithms are extending product lifetimes while maintaining the inherent reliability advantages of SLC architecture. These technological improvements are particularly valuable in applications requiring long product lifecycles, such as avionics and critical infrastructure. Manufacturers that can successfully integrate these advancements while controlling costs are positioned to expand their market share in specialized industrial and enterprise applications where absolute data integrity remains non-negotiable.

SINGLE-LEVEL CELL SSD MARKET TRENDS

Demand for High-Performance Storage Solutions Drives SLC SSD Adoption

The global Single-Level Cell (SLC) SSD market is experiencing significant growth due to the rising demand for high-performance, low-latency storage solutions in industrial, enterprise, and IoT applications. Unlike Multi-Level Cell (MLC) or Triple-Level Cell (TLC) SSDs, SLC NAND flash offers superior endurance, faster write speeds, and greater reliability, making it ideal for mission-critical environments. Recent data indicates that the market was valued at $753 million in 2024, with projections suggesting it will reach $1,042 million by 2032, growing at a CAGR of 4.9%. This growth trajectory is largely fueled by sectors such as data centers, embedded systems, and industrial automation, where data integrity and longevity are non-negotiable.

Other Trends

Expansion of Edge Computing and IoT Applications

The proliferation of edge computing and IoT devices is accelerating the adoption of SLC SSDs, as these solutions require robust, low-power storage capable of withstanding extreme conditions. Manufacturers are increasingly embedding SLC SSDs in industrial sensors, networking equipment, and autonomous systems, where consistent performance is essential. The integration of SLC SSDs in smart infrastructure projects—such as smart grids and autonomous vehicles—further strengthens market demand due to their ability to handle frequent read-write operations without degradation.

Technological Innovations and Cost Optimization

While SLC NAND has historically been more expensive than MLC or TLC alternatives, advancements in manufacturing processes are gradually reducing costs, making SLC SSDs more accessible for mid-range applications. Additionally, leading manufacturers are developing hybrid solutions that combine SLC caching with high-density NAND to balance performance and cost efficiency. PCIe Gen4 and upcoming Gen5 SSDs are also pushing the boundaries of speed, with some enterprise-grade SSDs now achieving sequential read speeds exceeding 7,000 MB/s. These innovations are reshaping the landscape, allowing SLC SSDs to maintain their dominance in high-stakes industries.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Leaders Accelerate Innovation to Capture Market Share in High-Growth SLC SSD Segment

The global Single-Level Cell (SLC) SSD market features a dynamic competitive environment dominated by established memory manufacturers and emerging specialists. Samsung maintains its leadership position, leveraging its vertically integrated NAND production and economies of scale to deliver high-performance SLC solutions. The company commanded approximately 18% of the global SLC SSD revenue share in 2024, benefiting from strong demand in industrial applications and enterprise storage.

Western Digital and Toshiba closely follow as key competitors, particularly in the PCIe SSD segment where reliability and endurance are critical. Their strength lies in proprietary controller technologies that optimize SLC NAND performance, with both companies investing heavily in R&D to maintain technological superiority. Recent product launches featuring 3D SLC NAND technology demonstrate the intensifying innovation race in this space.

Chinese manufacturers such as Shanghai Weigu Information Technology are gaining traction by offering cost-competitive alternatives for IoT and embedded applications. While their market share remains relatively small globally, regional policies supporting domestic semiconductor production are enabling faster growth in Asia-Pacific markets.

List of Key SLC SSD Manufacturers Profiled

- Samsung Electronics (South Korea)

- Western Digital Corporation (U.S.)

- Toshiba Memory Corporation (Japan)

- Micron Technology, Inc. (U.S.)

- Intel Corporation (U.S.)

- SiliconMotion Technology Corporation (Taiwan)

- Kingston Technology Company, Inc. (U.S.)

- Shanghai Weigu Information Technology (China)

- Innodisk Corporation (Taiwan)

- ADLINK Technology Inc. (Taiwan)

Segment Analysis:

By Type

PCIe SSD Segment Leads Due to Higher Performance and Scalability in Data-Intensive Applications

The market is segmented based on type into:

- PCIe SSD

- Subtypes: NVMe and AHCI

- SATA SSD

- eMMC

- Others

By Application

Embedded Systems Segment Dominates Owing to Increasing Demand for Compact and Efficient Storage Solutions

The market is segmented based on application into:

- Embedded Systems

- Industrial Control

- Internet of Things

- Others

By End User

Enterprise Segment Gains Traction Fueled by Data Center Expansion and Cloud Adoption

The market is segmented based on end user into:

- Enterprise

- Consumer Electronics

- Automotive

- Healthcare

- Others

Regional Analysis: Single-Level Cell SSD Market

Asia-Pacific

The Asia-Pacific region dominates the global Single-Level Cell (SLC) SSD market, accounting for the largest revenue share due to rapid technological adoption and manufacturing capabilities. Countries like China, Japan, and South Korea lead in semiconductor production, with key players such as Samsung, Toshiba, and SiliconMotion driving innovation. The growing demand for high-performance storage in consumer electronics, industrial automation, and IoT applications fuels market expansion. Additionally, government initiatives supporting local semiconductor manufacturing, such as China’s “Made in China 2025” policy, further accelerate regional growth. While PCIe SSDs gain traction in data centers, cost-sensitive sectors still favor SATA SSDs for embedded systems.

North America

North America is a significant market for SLC SSDs, propelled by advanced data center infrastructure and high adoption of enterprise storage solutions. The U.S. holds the majority share, with companies like Intel, Micron, and Western Digital investing in high-endurance SSDs for cloud computing and AI workloads. The region benefits from strong R&D investments and collaborations between tech firms and universities. However, pricing pressures from Asian manufacturers and slower growth in traditional server markets pose challenges. PCIe SSD adoption is notably high, driven by demand for low-latency storage in financial services and healthcare sectors.

Europe

Europe’s SLC SSD market is characterized by stringent data security regulations (e.g., GDPR) and a focus on industrial automation. Germany and the U.K. are key markets, with automotive and manufacturing sectors utilizing SLC SSDs for robust, high-reliability storage in harsh environments. The shift toward Industry 4.0 and edge computing further boosts demand, particularly for embedded and industrial control applications. European firms like Phoenix Contact and Innodisk emphasize energy-efficient designs, aligning with EU sustainability goals. However, the market faces competition from cheaper MLC/TLC alternatives in consumer segments.

South America

South America exhibits gradual growth, with Brazil and Argentina emerging as focal points for SLC SSD adoption in telecommunications and automotive industries. Economic instability and currency fluctuations hinder large-scale investments, but local governments are incentivizing tech infrastructure upgrades. The market remains price-sensitive, with SATA SSDs preferred over PCIe variants. Limited local manufacturing capabilities result in dependence on imports, though partnerships with global suppliers are slowly improving accessibility.

Middle East & Africa

The MEA region shows nascent but promising growth, driven by smart city projects in the UAE and Saudi Arabia. Demand stems from oil & gas, defense, and telecommunications sectors requiring durable storage solutions. While the market is constrained by budget limitations and low awareness of SLC SSD advantages, partnerships with multinational suppliers like Samsung and Kingston are expanding distribution networks. South Africa and Turkey are key growth markets, albeit with slower adoption rates due to competing priorities in basic infrastructure development.

Report Scope

This market research report provides a comprehensive analysis of the global Single-Level Cell SSD market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Single-Level Cell SSD market was valued at USD 753 million in 2024 and is projected to reach USD 1042 million by 2032, growing at a CAGR of 4.9%.

- Segmentation Analysis: Detailed breakdown by product type (PCIe SSD, SATA SSD, Emmc, Others), application (Embedded Systems, Industrial Control, IoT, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis. The U.S. and China represent key growth markets.

- Competitive Landscape: Profiles of leading market participants including Samsung, Intel, Toshiba, Micron Technology, Western Digital, Kingston, and emerging players like Shanghai Weigu Information Technology and Innodisk.

- Technology Trends & Innovation: Assessment of emerging storage technologies, integration of AI/ML in storage solutions, and evolving industry standards for single-chip SSDs.

- Market Drivers & Restraints: Evaluation of factors including growing demand for high-performance storage, IoT expansion, and challenges like supply chain constraints and price volatility.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

The research employs primary and secondary methodologies, including interviews with industry experts, manufacturer data, and verified market intelligence to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Single-Level Cell SSD Market?

-> Single-Level Cell SSD Market was valued at 753 million in 2024 and is projected to reach US$ 1042 million by 2032, at a CAGR of 4.9% during the forecast period.

Which key companies operate in Global Single-Level Cell SSD Market?

-> Key players include Samsung, Intel, Toshiba, Micron Technology, Western Digital, Kingston, Shanghai Weigu Information Technology, SiliconMotion, and Innodisk, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-performance storage solutions, growth in IoT applications, and increasing adoption in embedded systems and industrial controls.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America currently holds the largest market share.

What are the emerging trends?

-> Emerging trends include development of single-chip solutions with integrated computing capabilities, AI-optimized SSDs, and energy-efficient storage technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...