Silicon trench capacitor for power supply on chip Market Insights

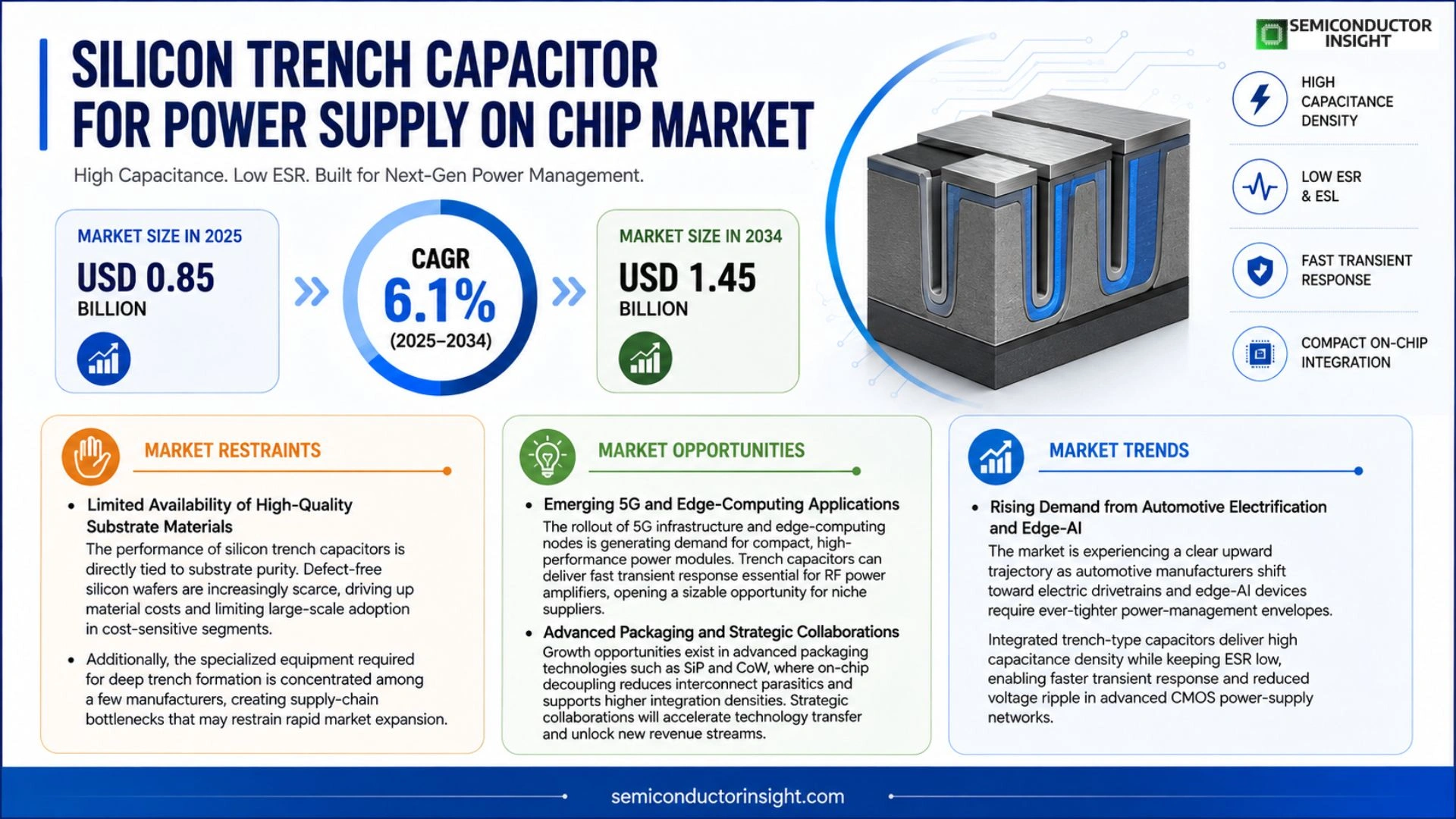

Global Silicon trench capacitor for power supply on chip market size was valued at USD 0.85 billion in 2025 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.1% during the forecast period.

Silicon trench capacitors are vertically‑structured passive components fabricated within deep trenches etched into a silicon substrate, delivering high capacitance density and low equivalent series resistance (ESR). They serve as decoupling and bulk storage elements in on‑chip power‑supply networks, enabling fast transient response and reduced voltage ripple in advanced CMOS processes.

The market is experiencing rapid growth because automotive electrification, edge‑AI devices, and high‑performance computing demand ever‑greater power‑management efficiency. Furthermore, scaling of CMOS nodes below 10 nm pushes designers toward integrated trench capacitors to save board space and improve reliability. Key players such as Texas Instruments, Infineon Technologies, STMicroelectronics, and NXP Semiconductors are expanding their portfolios through process‑compatible innovations and strategic collaborations with foundries.

MARKET DRIVERS

Increasing Demand for High‑Efficiency Power Management

Silicon trench capacitor for power supply on chip Market is being propelled by the rapid adoption of advanced power‑management ICs in electric vehicles and data‑center servers. Engineers favor trench‑type capacitors because they deliver low equivalent series resistance and high volumetric efficiency, which translate into reduced energy loss and smaller board footprints.

Growth of Renewable Energy Systems

Renewable‑energy inverters and photovoltaic‑converter modules require robust on‑chip decoupling. Trench capacitors meet these needs by providing stable voltage regulation under wide temperature swings, encouraging OEMs to integrate them directly into silicon. This trend is expected to lift market volume by roughly 7% CAGR over the next five years.

➤ Integration of trench capacitors reduces bill of materials by up to 15% while improving overall system reliability.

Manufacturers are also benefitting from mature CMOS‑compatible processes that lower production costs, making the technology attractive for both legacy and next‑generation designs.

MARKET CHALLENGES

Complexity of Advanced Process Integration

While trench capacitors offer performance advantages, their fabrication demands tight control of deep‑reactive ion etching and dielectric deposition. Small variations can lead to yield losses, especially for high‑volume automotive applications where reliability standards are stringent.

Other Challenges

Thermal Management Constraints

The high‑density layout on-chip can exacerbate localized heating, requiring sophisticated thermal‑design solutions that increase design time and validation effort.

Furthermore, the need to co‑optimize capacitor geometry with surrounding circuitry adds design complexity, potentially slowing time‑to‑market for new products.

MARKET RESTRAINTS

Limited Availability of High‑Quality Substrate Materials

The performance of silicon trench capacitors is directly tied to substrate purity. Defect‑free silicon wafers are increasingly scarce, driving up material costs and limiting large‑scale adoption in cost‑sensitive segments.

Additionally, the specialized equipment required for deep trench formation is concentrated among a few manufacturers, creating supply‑chain bottlenecks that may restrain rapid market expansion.

MARKET OPPORTUNITIES

Emerging 5G and Edge‑Computing Applications

The rollout of 5G infrastructure and edge‑computing nodes is generating demand for compact, high‑performance power modules. Trench capacitors can deliver fast transient response essential for RF power amplifiers, opening a sizable opportunity for niche suppliers.

Another growth avenue lies in advanced packaging technologies such as system‑in‑package (SiP) and chip‑on‑wafer (CoW), where on‑chip decoupling reduces interconnect parasitics and supports higher integration densities.

Strategic collaborations between semiconductor foundries and capacitor specialists are expected to accelerate technology transfer, unlocking new revenue streams for early adopters.

Silicon trench capacitor for power supply on chip Market Trends

Rising Demand from Automotive Electrification and Edge‑AI

Silicon trench capacitor for power supply on chip Market is experiencing a clear upward trajectory as automotive manufacturers shift toward electric drivetrains and edge‑AI devices require ever‑tighter power‑management envelopes. Integrated trench‑type capacitors deliver high capacitance density while keeping equivalent series resistance low, enabling faster transient response and reduced voltage ripple in advanced CMOS power‑supply networks. These technical advantages align tightly with the need to shrink board footprints and improve reliability in next‑generation electric vehicles, autonomous systems, and high‑performance compute modules.

Other Trends

Technology Scaling and Integration

Device scaling below 10 nm intensifies the pressure on designers to incorporate passive components directly within the silicon substrate. The vertical architecture of trench capacitors allows designers to meet the stringent area constraints imposed by sub‑10 nm nodes, while maintaining the low‑ESR characteristics essential for high‑frequency decoupling. Foundries are therefore expanding their design‑for‑manufacturing (DFM) guidelines to support deeper trench etches and novel dielectric stacks, which in turn accelerates adoption across mixed‑signal SoCs that serve power‑intensive workloads.

Competitive Landscape and Portfolio Expansion

Key players such as Texas Instruments, Infineon Technologies, STMicroelectronics, and NXP Semiconductors are actively broadening their product portfolios through process‑compatible innovations and strategic collaborations with major foundries. These companies are introducing variant families that target specific voltage ratings and temperature ranges, thereby addressing the diverse reliability requirements of automotive, industrial, and consumer segments. The competitive focus on customizable design‑kits and foundry‑friendly validation flows is reshaping the market dynamics, fostering faster time‑to‑market for new on‑chip power‑supply solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

Silicon trench capacitor market overview

Silicon trench capacitor market is dominated by large analog and power‑management powerhouses that leverage deep‑trench processing within advanced CMOS nodes. Texas Instruments leads with a broad portfolio of integrated power‑supply solutions, while Infineon Technologies and STMicroelectronics provide foundry‑compatible trench‑capacitor libraries that address automotive electrification and edge‑AI power budgets. NXP Semiconductors and ON Semiconductor (onsemi) have accelerated development cycles through strategic collaborations with 28 nm and 14 nm process partners, positioning themselves as primary suppliers for high‑density decoupling components in system‑on‑chip designs. These leaders benefit from strong IP protection, extensive design‑enablement ecosystems, and the ability to co‑optimize capacitor structures with process engineers, creating a market structure that favors vertically integrated semiconductor groups.

Beyond the four flagship firms, a cadre of niche players contributes specialized trench‑capacitor expertise. Analog Devices and Maxim Integrated (now part of ADI) focus on precision analog front‑ends that require ultra‑low ESR performance. Renesas Electronics and ROHM Semiconductor supply compact solutions for automotive microcontrollers, while Samsung Electronics and TSMC offer foundry‑level design‑kits that enable custom silicon‑on‑chip capacitor insertion for customers. GlobalFoundries and Intel are investing in process enhancements to support higher capacitance densities, and Micron Technology provides complementary memory‑centric power‑management blocks that pair with trench capacitors for bulk storage.

List of Key Silicon Trench Capacitor Companies Profiled

- Texas Instruments

- Infineon Technologies

- STMicroelectronics

- NXP Semiconductors

- ON Semiconductor (onsemi)

- Analog Devices

- Maxim Integrated

- Renesas Electronics

- ROHM Semiconductor

- Samsung Electronics

- TSMC

- GlobalFoundries

- Intel

- Micron Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

High‑Voltage Trench Capacitors are favored because they enable robust decoupling in automotive power‑train modules; they provide superior voltage handling that aligns with the rising demand for electric‑vehicle power‑electronics. • Designers appreciate the capacity to integrate high voltage tolerance without additional external components, thereby simplifying board layout. • The low‑ESR characteristic of this type ensures rapid transient response, which is critical for maintaining stable supply rails in high‑performance computing chips. |

| By Application |

|

Automotive Power Management drives adoption as vehicle architectures shift toward higher voltage domains and tighter power‑budget constraints. • Trench capacitors provide on‑chip bulk storage that reduces reliance on external bulk capacitors, enhancing reliability under harsh automotive thermal cycles. • Their integration supports compact power‑train modules, essential for modern electric‑vehicle platforms where space is at a premium. |

| By End User |

|

Chip Designers prioritize trench capacitors for their ability to meet aggressive power‑integrity targets without expanding die size. • The vertical trench architecture aligns with advanced CMOS scaling, allowing seamless incorporation into sub‑10nm process flows. • Designers value the reduced equivalent series resistance that minimizes voltage ripple during high‑frequency switching events, critical for both AI inference engines and automotive ECUs. |

| By Integration Approach |

|

Monolithic Integration is emerging as the preferred route because it embeds the capacitor directly within the silicon substrate, eliminating parasitic interconnects. • This approach yields superior thermal stability, essential for high‑temperature automotive and edge‑computing environments. • It also streamlines the manufacturing flow, enabling designers to achieve tighter power‑rail regulation without additional packaging steps. |

| By Technology Node |

|

Sub‑10nm Nodes stimulate trench capacitor adoption as designers seek to preserve die area while meeting stringent power‑density requirements. • The deep‑trench process is compatible with the aggressive patterning techniques used at these nodes, ensuring seamless integration. • Engineers value the ability to deliver high capacitance density in a footprint that would otherwise be occupied by discrete passives, supporting the miniaturization trends across automotive, AI, and HPC markets. |

Regional Analysis: Silicon trench capacitor for power supply on chip Market

China’s vast electronics manufacturing base fuels demand for compact, high‑performance power capacitors. Government incentives for advanced packaging and energy‑efficient devices encourage local fabs to expand trench capacitor production, while domestic OEMs integrate them into smartphones and electric‑vehicle power modules.

Japan’s focus on precision automotive electronics and industrial automation drives adoption of silicon trench capacitors. Leading chipmakers leverage mature process nodes to deliver capacitors with tighter tolerances, supporting high‑reliability power‑supply architectures in next‑generation vehicles.

South Korea’s strong semiconductor infrastructure and aggressive R&D funding enable rapid iteration of trench‑capacitance designs, targeting high‑speed data‑center and 5G infrastructure where power efficiency is paramount.

Taiwan remains a pivotal foundry hub, offering flexible production capacity for niche power‑management components. Its expertise in advanced lithography supports scaling of trench capacitors for ultra‑compact consumer gadgets.

North America

North America maintains a sophisticated market for Silicon trench capacitor for power supply on chip technologies, largely propelled by the United States’ focus on high‑performance computing and defense applications. Major semiconductor players invest in process optimization to deliver capacitors that meet rigorous reliability standards required for aerospace and critical infrastructure. The region’s emphasis on green‑energy initiatives also pushes integration of efficient power‑management solutions in data‑center hardware, albeit at a slower pace compared with Asia‑Pacific due to higher production costs.

Europe

European demand is shaped by stringent energy‑efficiency directives and a strong automotive sector transitioning to electric drivetrains. Countries such as Germany and France encourage adoption of advanced power‑management components, including trench capacitors, to comply with emissions targets. While local fabs are fewer, strategic partnerships with Asian manufacturers enable European OEMs to source high‑quality capacitors while focusing on system integration and design innovation.

South America

In South America, market growth is modest but steady, driven mainly by telecommunications upgrades and renewable‑energy projects in Brazil and Chile. Limited local semiconductor manufacturing means the region relies heavily on imports, yet rising awareness of power‑efficiency benefits is prompting local distributors to prioritize trench‑capacitor solutions for emerging smart‑grid and IoT deployments.

Middle East & Africa

The Middle East & Africa region experiences nascent adoption, with interest centered on data‑center expansion and renewable‑energy installations in the Gulf Cooperation Council nations. Although local production is minimal, strategic import agreements are being forged to secure Silicon trench capacitor for power supply on chip components that support the region’s ambitious digital‑transformation and sustainability agendas.

Report Scope

This market research report provides a comprehensive analysis of the Silicon trench capacitor for power supply on chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Silicon trench capacitor for power supply on chip Market?

-> Silicon trench capacitor for power supply on chip Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034.

Which key companies operate in Silicon trench capacitor for power supply on chip Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...