Silicon Photonics Market Insights

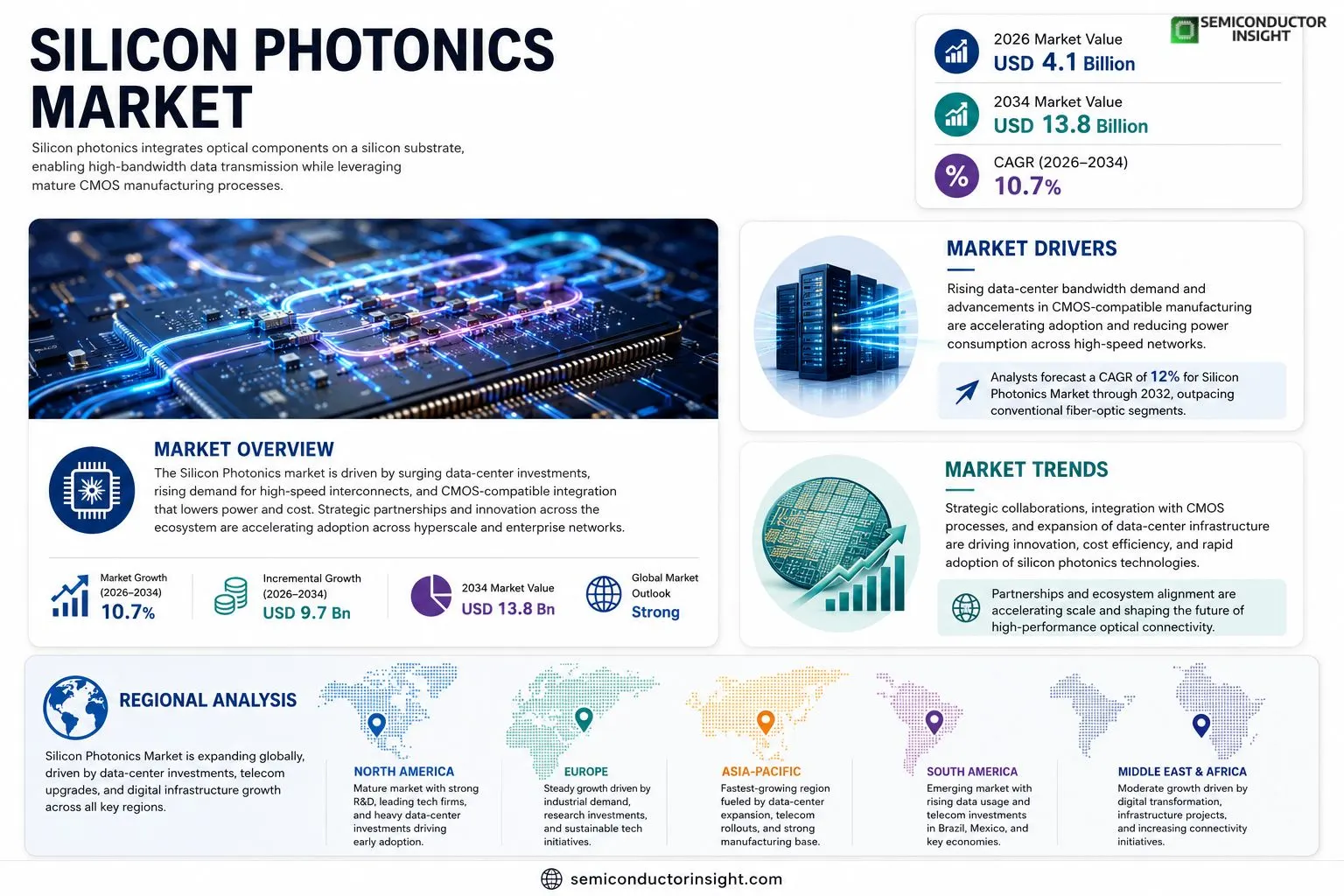

Global Silicon Photonics market size was valued at USD 4.1 billion in 2025. The market is projected to grow from USD 4.1 billion in 2025 to USD 13.8 billion by 2034, exhibiting a CAGR of 10.7% during the forecast period.

Silicon photonics integrates optical components such as waveguides, modulators, detectors and multiplexers onto a silicon substrate, enabling high‑bandwidth data transmission while leveraging mature CMOS manufacturing processes.

The market is experiencing rapid growth due to several factors, including increased investment in data‑center infrastructure, rising demand for high‑speed interconnects in hyperscale computing, and advancements in integrated optics that reduce power consumption. Furthermore, strategic collaborations,such as Intel’s partnership with GlobalFoundries announced in March 2024,to scale production of silicon‑photonic transceivers are accelerating adoption. Key players such as Intel Corporation, IBM Corp., Cisco Systems Inc., Lumentum Holdings Inc., and Acacia Communications are driving innovation across the ecosystem.

MARKET DRIVERS

Rising Data Center Bandwidth Demand

Silicon Photonics Market is being propelled by exponential growth in data traffic, with global data center bandwidth expected to exceed 300 Tbps by 2027. Cloud service providers are adopting silicon‑based optical transceivers to achieve lower power consumption and higher port densities, driving immediate procurement cycles.

Advancements in CMOS Compatibility

Recent breakthroughs in CMOS‑compatible manufacturing enable silicon photonic chips to be fabricated alongside traditional microprocessors, cutting production costs by up to 30 %. This integration reduces packaging complexity and accelerates time‑to‑market for high‑performance networking solutions.

➤ Analysts forecast a compound annual growth rate (CAGR) of 12 % for Silicon Photonics Market through 2032, outpacing conventional fiber‑optic segments.

Combined, these drivers create a robust ecosystem where equipment vendors, foundries, and end‑users collaborate to expand Silicon Photonics Market footprint across hyperscale and enterprise environments.

MARKET CHALLENGES

High Capital Expenditure for Fab Facilities

Establishing a silicon photonics fabrication line demands multi‑hundred‑million‑dollar investments, deterring new entrants and limiting capacity expansion. Many incumbents must balance these outlays against slower adoption rates in legacy telecom segments.

Other Challenges

Manufacturing Yield Variability

Yield rates for high‑density photonic arrays currently hover around 70‑80 %, creating cost pressures for volume buyers and slowing broader market diffusion.

MARKET RESTRAINTS

Limited Availability of Skilled Workforce

The specialized knowledge required for silicon photonic design and testing is scarce, with fewer than 5 % of semiconductor engineers possessing requisite optical expertise. This talent gap constrains R&D pipelines and prolongs timeframes for new product launches.

MARKET OPPORTUNITIES

Emerging Applications in 5G and Edge Computing

5G densification and edge‑computing deployments demand ultra‑low‑latency interconnects. Silicon photonics offers sub‑nanosecond signaling with negligible loss, positioning Silicon Photonics Market to capture a sizeable share of next‑generation telecom infrastructure spending.

Silicon Photonics Market Trends

Data‑Center Infrastructure Investment Driving Adoption

The rapid expansion of hyperscale data‑centers is creating a sustained demand for high‑speed, low‑power interconnects. Silicon photonics enables dense wavelength‑division multiplexing on a single silicon die, allowing carriers to move terabits of data per second while consuming less energy than traditional copper solutions. Mature CMOS manufacturing reduces production cost and shortens time‑to‑market, making the technology attractive to operators seeking to upgrade legacy architectures. As enterprises migrate workloads to cloud platforms, the pressure to sustain bandwidth growth without proportional power draw reinforces the strategic importance of Silicon Photonics Market within data‑center roadmaps.

Other Trends

Integration with CMOS Processes

Recent advancements have streamlined the co‑fabrication of optical waveguides, modulators, and detectors alongside electronic circuits on standard silicon wafers. This integration eliminates the need for discrete optical packages, improving signal integrity and reducing assembly complexity. Early adopters report measurable gains in module reliability and a 20‑30% reduction in overall system power consumption. The seamless alignment of photonic and electronic design flows also accelerates iterative development, allowing vendors to respond quickly to emerging standards for 400 Gb/s and beyond.

Strategic Partnerships Accelerating Scale

Collaboration between leading fabless designers and foundries is reshaping the supply chain. Intel’s March 2024 agreement with GlobalFoundries to co‑develop high‑volume silicon‑photonic transceivers exemplifies how joint R&D reduces risk and leverages shared tooling. Parallel initiatives by IBM, Cisco, Lumentum, and Acacia Communications focus on jointly certifying components, standardizing interface specifications, and expanding the ecosystem of compatible modules. These alliances shorten commercialization timelines and broaden customer access, reinforcing the overall momentum of Silicon Photonics Market across networking, telecom, and emerging AI accelerator segments.

COMPETITIVE LANDSCAPEKey Industry Players

Silicon Photonics Market: Competitive Overview

Silicon Photonics Market is anchored by a handful of technology giants that control the majority of silicon‑based transceiver volume. Intel Corporation leads the ecosystem, leveraging its deep CMOS expertise and a strategic partnership with GlobalFoundries announced in March 2024 to scale high‑volume silicon‑photonic transceivers for hyperscale data centers. IBM Corp. complements Intel by focusing on advanced modulators and detector architectures for cloud‑scale interconnects, while Cisco Systems Inc. drives adoption through aggressive OEM integration in its networking portfolio. Lumentum Holdings Inc., having acquired Luxtera, provides a broad wafer‑scale photonic component catalog, and Acacia Communications supplies high‑performance coherent optical engines that are increasingly being re‑engineered on silicon platforms. These firms dominate design, IP licensing, and large‑scale manufacturing, creating a market structure where economies of scale and deep fab relationships are decisive competitive advantages.Beyond the core tier, a diverse set of niche and regionally strong players enriches the landscape with specialized solutions and emerging technologies. Infinera Corp. focuses on integrated photonic modules for long‑haul transport, while Ayar Labs delivers silicon‑based electro‑optical transceivers targeting low‑power compute racks. Broadcom Inc. and Ciena Corp. contribute ASIC‑compatible photonic interfaces for carrier‑grade equipment, and Fujitsu Ltd. pursues silicon‑photonic sensor arrays for data‑center monitoring. These companies, often operating in focused market segments or geographic niches, foster innovation through agile R&D, strategic alliances, and targeted IP portfolios, ensuring a vibrant competitive environment that supports the market’s projected rise to $13.8 billion by 2034.

List of Key Silicon Photonics Companies Profiled

- Intel Corporation

- Intel Corporation

- IBM Corp.

- IBM Corp.

- Cisco Systems Inc.

- Cisco Systems Inc.

- Lumentum Holdings Inc.

- Lumentum Holdings Inc.

- Acacia Communications

- Acacia Communications

- GlobalFoundries

- GlobalFoundries

- Infinera Corp.

- Ayar Labs

- Broadcom Inc.

- Ciena Corp.

- Fujitsu Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Passive Components

|

| By Application |

|

Data Center Interconnects

|

| By End User |

|

Hyperscale Cloud Providers

|

| By Technology |

|

CMOS‑Compatible Integration

|

| By Market Driver |

|

Data Center Bandwidth Demand

|

Regional Analysis: North America

North America

The data center segment in North America is a primary driver for Silicon Photonics adoption, with increasing demands for faster data transmission and energy efficiency.

The telecommunications sector’s rollout of 5G networks and expansion of fiber optic infrastructure significantly contributes to the demand for advanced optical solutions.

Enterprise networks are increasingly adopting Silicon Photonics for high-speed connections within data centers and between buildings.

Emerging applications in automotive, particularly for advanced driver-assistance systems (ADAS) and autonomous driving, are creating new opportunities for Silicon Photonics in connectivity.

Europe

Europe exhibits a steady growth trajectory in Silicon Photonics Market, driven by strong industrial sectors, increasing investments in research, and a growing focus on sustainable technologies. The region’s key markets include Germany, the UK, France, and the Netherlands, each with unique strengths and opportunities. The automotive and industrial sectors are significant users, while the telecommunications infrastructure upgrades are also contributing to demand.

Asia-Pacific

Asia-Pacific is poised to be the fastest-growing market for Silicon Photonics globally. Countries like China, Japan, South Korea, and Taiwan are experiencing rapid expansion in data centers, telecommunications, and manufacturing, fueling significant demand. Government initiatives promoting technological innovation and infrastructure development further contribute to this growth. The region is also a major manufacturing hub for Silicon Photonics components.

South America

Silicon Photonics Market in South America is still in its nascent stages but showing promising potential. Brazil and Mexico are the primary markets, driven by increasing internet penetration, growing data consumption, and investments in telecommunications infrastructure. The demand is primarily focused on data centers and enterprise networking.

Middle East & Africa

The Middle East & Africa region presents a moderate growth opportunity for Silicon Photonics. Investments in digital transformation, infrastructure development, and increasing data traffic are driving demand. The telecommunications sector and government initiatives to enhance connectivity are key growth drivers. The region is witnessing a growing adoption of advanced networking technologies.

Report Scope

This market research report provides a comprehensive analysis of the Silicon Photonics Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Silicon Photonics Market?

-> Silicon Photonics Market was valued at USD 4.1 billion in 2025 and is expected to reach USD 13.8 billion by 2034, exhibiting a CAGR of 10.7 % during the forecast period.

Which key companies operate in Silicon Photonics Market?

-> Key players include Intel Corporation, IBM Corp., Cisco Systems Inc., Lumentum Holdings Inc., and Acacia Communications.

What are the key growth drivers?

-> Key growth drivers include increased investment in data‑center infrastructure, rising demand for high‑speed interconnects in hyperscale computing, and advancements in integrated optics that reduce power consumption.

Which region dominates the market?

-> The reference does not specify a dominant region for Silicon Photonics Market.

What are the emerging trends?

-> Emerging trends include strategic collaborations to scale production (e.g., Intel‑GlobalFoundries partnership), integration of silicon photonics with mature CMOS processes, and a focus on power‑efficient high‑bandwidth data transmission.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...