Silicon Photonics for AI Data Centers Market Insights

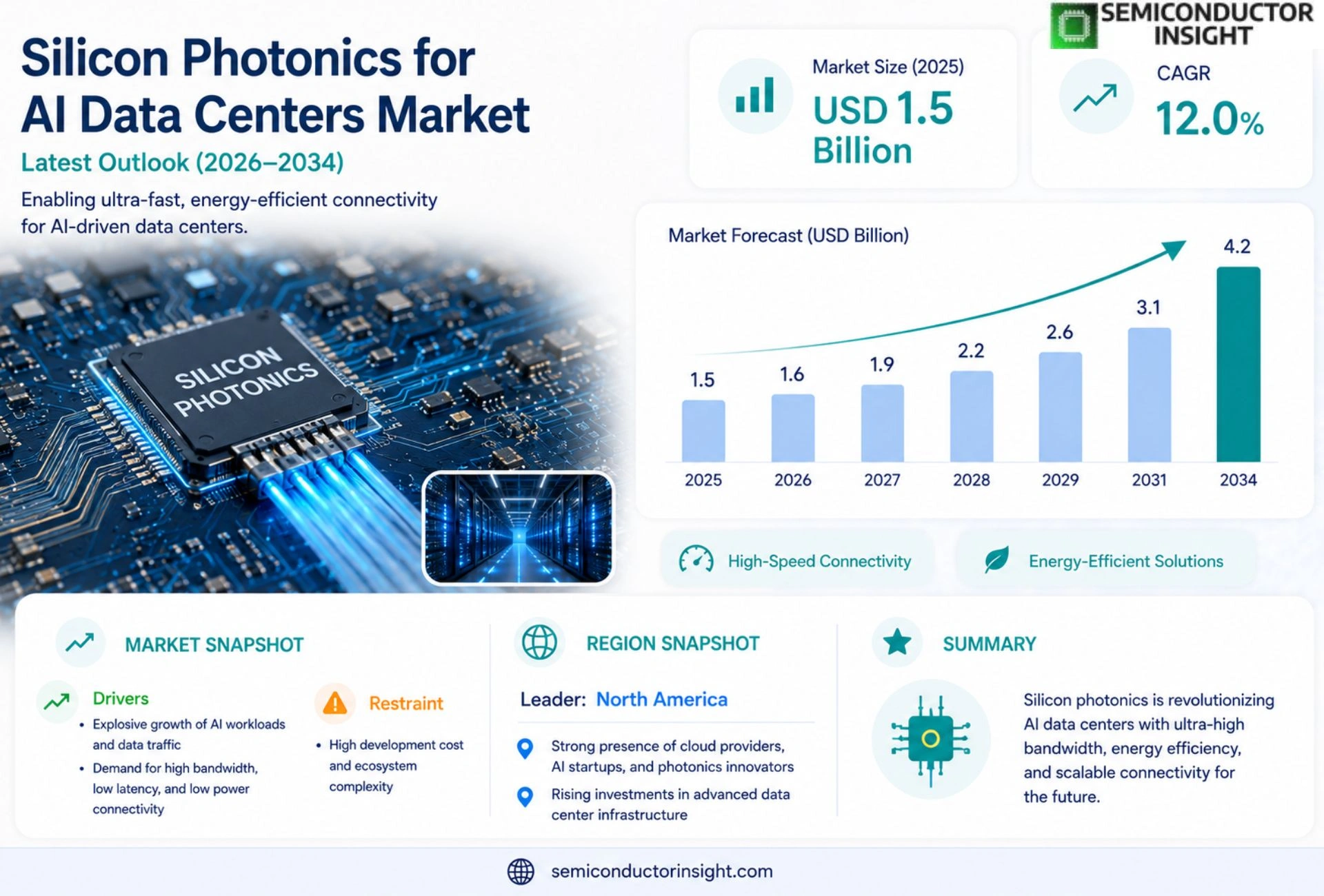

Global Silicon Photonics for AI Data Centers Market size was valued at USD 1.5 billion in 2025. The market is projected to grow from USD 1.6 billion in 2026 to USD 4.2 billion by 2034, exhibiting a CAGR of 12.0% during the forecast period.

Silicon photonics integrates optical components onto a silicon substrate to enable high‑bandwidth, low‑latency interconnects that replace traditional copper links in AI‑focused data centers. This technology leverages wavelength‑division multiplexing and energy‑efficient transceivers to support the massive data throughput required by large language models and GPU clusters.

The market is accelerating because hyperscale cloud providers are scaling AI workloads, driving demand for faster interconnects while reducing power consumption. Furthermore, strategic collaborations,such as Intel’s partnership with Nvidia on silicon‑photonic co‑design announced in early 2023,and investments from Cisco, Lumentum, and IBM are expanding product portfolios and driving adoption across global data center operators.

MARKET DRIVERS

Growing Demand for High‑Bandwidth Interconnects

The rapid expansion of AI training workloads is creating an unprecedented need for data‑center interconnects that can sustain multi‑terabit per second throughput. Silicon Photonics for AI Data Centers Market is uniquely positioned to deliver the optical bandwidth required while maintaining a compact footprint.

Energy‑Efficiency Imperatives

Operators are seeking to reduce power consumption per bit transferred. Silicon‑based photonic transceivers consume up to 60% less energy than traditional copper solutions, directly supporting the sustainability goals of hyperscale facilities.

➤ “Deployments of silicon photonic modules have cut intra‑rack latency by 30 % on average.”

These technical advantages are translating into faster time‑to‑market for new AI services, reinforcing the upward trajectory of Silicon Photonics for AI Data Centers Market.

MARKET CHALLENGES

Integration Complexity with Existing Infrastructure

Legacy data‑center architectures rely heavily on established electrical standards. Introducing photonic links requires redesign of rack layouts, firmware updates, and staff training, which can extend deployment timelines.

Other Challenges

Manufacturing Yield and Cost Control

Achieving high‑volume silicon photonic production at competitive cost remains difficult due to stringent lithography tolerances and the need for specialized testing equipment.

MARKET RESTRAINTS

Capital Expenditure Requirements

While operational savings are evident, the upfront capital needed for photonic transceiver procurement and rack redesign can deter mid‑size operators from early adoption, slowing broader market penetration.

Additionally, the perception of higher risk associated with emerging silicon photonic technology can limit financing options for some data‑center projects.

MARKET OPPORTUNITIES

Edge‑AI and 5G Backhaul Expansion

The convergence of AI workloads at the edge and the rollout of 5G networks is driving demand for compact, low‑latency optical solutions. Silicon photonics offers the scalability needed to connect distributed edge nodes to core AI data centers efficiently.

Furthermore, collaborations between semiconductor foundries and cloud providers are accelerating the development of integrated photonic‑electronic chips, opening new revenue streams for vendors Silicon Photonics for AI Data Centers Market.

Silicon Photonics for AI Data Centers Market Trends

Accelerated Adoption Driven by AI Workloads

The rapid expansion of generative AI models and large‑scale GPU clusters is compelling data‑center operators to replace traditional copper interconnects with silicon‑photonic solutions. These optical links deliver significantly higher bandwidth per lane while maintaining low latency, directly addressing the throughput requirements of modern AI inference and training pipelines. Wavelength‑division multiplexing (WDM) enables multiple data streams over a single fiber, further amplifying aggregate capacity without proportionally increasing physical cabling. Operators report measurable reductions in packet loss and jitter, which translate into more predictable model execution times and lower overall infrastructure cost. The shift also simplifies rack design, as fewer copper cables reduce cable‑management complexity and improve airflow in high‑density AI racks.

Other Trends

Energy‑Efficient Transceiver Development

Recent silicon‑photonic transceiver designs achieve power consumptions under 5 mW per gigabit, a notable improvement over legacy copper PHYs. The lower power envelope reduces cooling loads in dense AI racks, enabling operators to achieve higher compute density without proportionally increasing facility energy usage. Integrated driver electronics and on‑chip lasers further streamline power distribution, while advanced modulation formats maintain signal integrity across longer reaches. These efficiency gains are especially valuable for hyperscale cloud providers that operate thousands of petabytes of AI‑driven traffic daily, allowing them to meet sustainability targets while scaling performance.

Strategic Partnerships Expanding the Ecosystem

Industry collaborations are accelerating the market. Intel’s co‑design effort with Nvidia, announced in early 2023, integrates silicon‑photonic modules directly onto GPU platforms, shortening the design cycle for AI accelerators. Parallel investments from Cisco, Lumentum and IBM are diversifying the supply chain, introducing modular plug‑and‑play photonic transceivers that can be retrofitted into existing server chassis. These alliances are also fostering standardized programming interfaces, simplifying deployment for hyperscale cloud providers. As a result, adoption cycles have shortened from multi‑year to under a year for many operators, and a growing number of data centers are planning phased migrations from copper to optical interconnects over the next three to five years.

COMPETITIVE LANDSCAPE

Key Industry Players

Silicon Photonics for AI Data Centers: Competitive Landscape Overview

The dominant force in the silicon‑photonic interconnect market is Intel, which leverages its extensive silicon‑foundry capacity and deep relationships with hyperscale cloud providers. Intel’s collaboration with NVIDIA on co‑designing silicon‑photonic transceivers has accelerated the rollout of low‑latency, high‑bandwidth links in AI‑centric data centers, positioning it as the market leader. Cisco’s strategic investments and its broad portfolio of networking hardware further consolidate the top‑tier ecosystem, while the combined market size,projected to reach USD 4.2 billion by 2034,reflects aggressive adoption driven by large‑scale language model training and inference workloads.

Beyond the headline players, a diverse set of niche innovators enriches the competitive tableau. Lumentum supplies high‑performance optical engines, and IBM contributes research‑driven photonic modules that target power‑efficient scaling. Broadcom, Marvell Technology, and Ciena each offer differentiated wavelength‑division multiplexing (WDM) solutions that cater to specific hyperscale configurations. Asian incumbents such as Huawei and Alibaba Cloud are expanding their silicon‑photonic roadmaps to serve regional data‑center clusters, while emerging specialists like Mitsubishi Electric and Juniper Networks focus on integrated transceiver packaging. This fragmented yet collaborative environment fosters rapid technology diffusion and intensifies price‑performance competition.

List of Key Silicon Photonics Companies Profiled

- Intel

- NVIDIA

- Cisco

- Lumentum

- IBM

- Broadcom

- Marvell Technology

- Ciena

- Huawei

- Alibaba Cloud

- Mitsubishi Electric

- Juniper Networks

- Google (Alphabet)

- Microsoft

- Synopsys

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Monolithic Silicon Photonic Modules are favored because they consolidate optical and electronic functions on a single die, delivering compact, high‑density links. Their impact is evident across the AI data‑center ecosystem.

|

| By Application |

|

AI Training Clusters dominate demand as they require massive, synchronized data movement across GPUs. Silicon photonics directly addresses these pressures.

|

| By End User |

|

Hyperscale Cloud Providers act as the primary engine of adoption, driven by the need to accelerate AI services. Their strategic moves shape market direction.

|

| By Integration Strategy |

|

Co‑design with GPU Vendors emerges as a decisive approach, aligning optical and compute roadmaps. This synergy accelerates ecosystem readiness.

|

| By Power Efficiency Focus |

|

Low‑Power Transceivers are a decisive factor for operators seeking to balance performance with sustainability. Their influence cascades through design choices.

|

Regional Analysis: North America

United States

Ongoing investments in data center infrastructure across the US, particularly in major metropolitan areas, are creating a strong demand for advanced interconnect technologies like Silicon Photonics.

The US is a global hub for AI research and development. This strong R&D ecosystem directly fuels the need for next-generation interconnects to support computationally intensive AI workloads.

Government programs and funding initiatives are promoting technological advancements and data center growth, creating a favorable environment for Silicon Photonics adoption.

Increasing emphasis on energy efficiency in data centers is driving the adoption of Silicon Photonics, which offers lower power consumption compared to traditional solutions.

Europe

The European market for Silicon Photonics in AI data centers is experiencing steady growth, driven by increasing investments in AI and high-performance computing across the continent. Several countries, including Germany, the UK, and France, are establishing themselves as key hubs for AI innovation. While the adoption rate is currently lower than in the US, the region is expected to witness substantial growth in the coming years, fueled by initiatives aimed at fostering digital transformation and strengthening data infrastructure. Challenges include navigating complex regulatory landscapes and ensuring interoperability across different European markets. However, the strong focus on sustainability and energy efficiency provides a competitive advantage for Silicon Photonics solutions, aligning with Europe’s commitment to green technology. The development of advanced microchip manufacturing capabilities within Europe is also expected to support domestic Silicon Photonics adoption.

Asia-Pacific

Asia-Pacific represents a high-growth potential market for Silicon Photonics in AI data centers. Countries like China, Japan, and South Korea are investing heavily in AI infrastructure to support their rapidly expanding digital economies. China, in particular, is emerging as a dominant force in AI research and development, creating significant demand for advanced interconnect technologies. The region’s large population and increasing data consumption further contribute to market growth. However, geopolitical factors and trade tensions could pose some challenges to market expansion. The availability of cost-effective manufacturing capabilities in certain parts of Asia-Pacific also offers a competitive advantage to Silicon Photonics suppliers. The focus on edge computing initiatives within the region is also expected to drive demand for high-speed Silicon Photonics solutions.

South America

The Silicon Photonics market for AI Data Centers in South America is nascent but poised for future growth. Countries like Brazil and Chile are beginning to invest in AI infrastructure, driven by the growing digital economy and increasing demand for data processing. The adoption rate is currently limited by infrastructure constraints and the relatively high cost of advanced technologies. However, the region’s increasing focus on technological innovation and the expansion of data centers in major cities are expected to drive market growth in the long term. Government initiatives to promote digitalization and attract foreign investment could also accelerate adoption. The potential for leveraging Silicon Photonics to enhance the efficiency of resource-constrained data centers is a key driver.

Middle East & Africa

The Middle East and Africa represent a promising growth opportunity for Silicon Photonics in AI data centers. Several countries in the region are undertaking ambitious digital transformation initiatives, including investments in AI and data center infrastructure. The increasing demand for high-speed data transmission to support various applications, such as smart cities and industrial automation, is driving market growth. The region’s favourable demographics and increasing disposable incomes further contribute to market potential. However, challenges include limited technological expertise and infrastructure constraints in some areas. Government support for technological development and the expansion of data center facilities are expected to accelerate Silicon Photonics adoption in the region.

Report Scope

This market research report provides a comprehensive analysis of the Silicon Photonics for AI Data Centers Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Silicon Photonics for AI Data Centers Market?

-> Silicon Photonics for AI Data Centers Market size was valued at USD 1.5 billion in 2025. The market is projected to grow from USD 1.6 billion in 2026 to USD 4.2 billion by 2034

Which key companies operate Silicon Photonics for AI Data Centers Market?

-> Key players include Intel, Nvidia, Cisco, Lumentum, and IBM, among others.

What are the key growth drivers?

-> Key growth drivers include the rapid scaling of AI workloads by hyperscale cloud providers, the need for high‑bandwidth low‑latency interconnects, and the industry’s focus on reducing power consumption in data center environments.

Which region dominates the market?

-> North America currently leads adoption due to the concentration of semiconductor innovators and large cloud service providers, while Asia‑Pacific is emerging as a fast‑growing market segment.

What are the emerging trends?

-> Emerging trends include the use of wavelength‑division multiplexing, energy‑efficient silicon‑photonic transceivers, and co‑design collaborations that integrate AI‑specific architectures directly with silicon‑photonic platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...