MARKET INSIGHTS

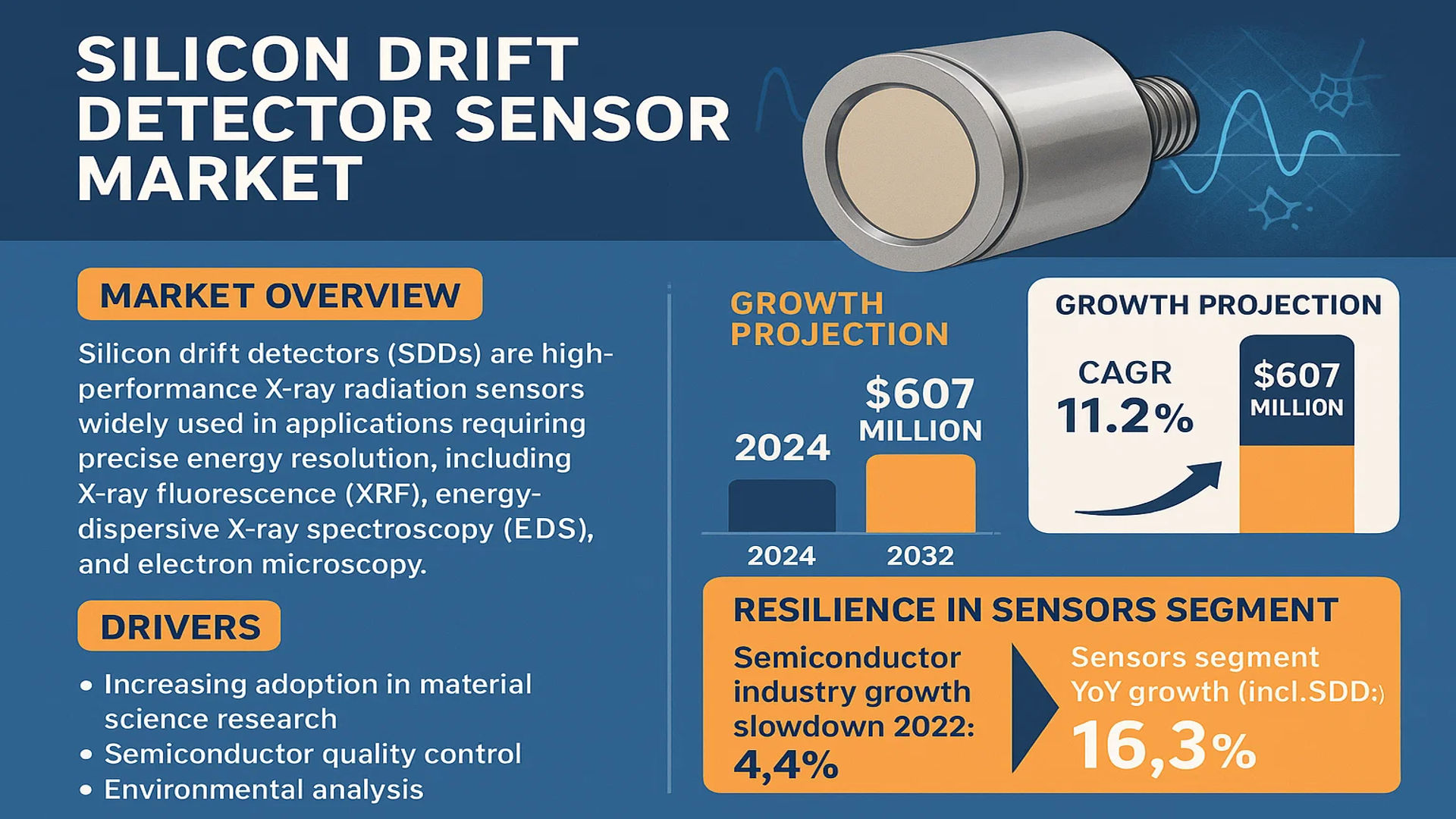

The global Silicon Drift Detector Sensor Market was valued at 294 million in 2024 and is projected to reach US$ 607 million by 2032, at a CAGR of 11.2% during the forecast period.

Silicon drift detectors (SDDs) are high-performance X-ray radiation sensors widely used in applications requiring precise energy resolution, including X-ray fluorescence (XRF), energy-dispersive X-ray spectroscopy (EDS), and electron microscopy. These detectors operate by collecting charge carriers (electrons) generated by X-ray photons in a silicon crystal structure, offering superior count rate capabilities and energy resolution compared to conventional detectors.

The market growth is driven by increasing adoption in material science research, semiconductor quality control, and environmental analysis. While the semiconductor industry faced a slowdown in 2022 with overall growth of just 4.4%, the sensors segment – including SDDs – demonstrated resilience with 16.3% year-over-year growth. Recent technological advancements in detector miniaturization and cooling systems are further expanding application possibilities. Key players such as Ketek, Mirion Technologies, and Amptek (AMETEK) continue to innovate, developing SDDs with larger active areas (exceeding 100 mm²) to meet growing analytical demands across industries.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Advanced Analytical Techniques in Material Sciences Fuels Market Growth

The global Silicon Drift Detector (SDD) sensor market is experiencing significant growth driven by increasing adoption in material sciences. SDDs offer superior energy resolution and faster processing speeds compared to traditional detectors, enabling more precise elemental analysis. With industries requiring nanoscale material characterization, the demand for high-performance X-ray detectors in electron microscopy and spectroscopy applications has surged. The semiconductor industry alone accounts for over 35% of SDD sensor utilization, with the growing complexity of chip designs necessitating more sophisticated analytical tools. Asia-Pacific has emerged as a key growth region, with semiconductor R&D investments growing at approximately 15% annually since 2020.

Expansion of Pharmaceutical Quality Control Infrastructure Creates New Demand

Pharmaceutical manufacturers are increasingly implementing SDD-based energy dispersive X-ray spectroscopy (EDS) systems for contaminant detection and quality control. The technology’s ability to identify trace metal impurities at parts-per-million levels aligns perfectly with stringent regulatory requirements. With global pharmaceutical quality control equipment spending projected to exceed $9 billion by 2026, SDD sensors are becoming integral components in modern laboratories. Recent advancements in detector cooling systems have extended operational lifetimes by up to 40%, significantly improving cost-efficiency for end users. The market has responded positively, with SDD adoption rates in pharmaceutical applications growing at a compound annual rate of 13.5% since 2021.

Government Investments in Academic Research Accelerate Market Penetration

Academic and government research institutions are driving demand for high-end analytical equipment, with SDD sensors playing a crucial role in cutting-edge physics and materials research. The European Union’s Horizon Europe program has allocated over €700 million for advanced research instrumentation, while the U.S. National Science Foundation’s Major Research Instrumentation program continues to fund university equipment purchases. Such initiatives have created a steady demand stream for SDD-equipped microscopy systems, particularly those with active areas exceeding 100mm². Research-grade SDD implementations now account for nearly 25% of the total market, with double-digit growth projected through 2030.

MARKET CHALLENGES

High Initial Investment and Maintenance Costs Limit Widespread Adoption

While SDD technology offers superior performance, the substantial capital expenditure required for complete systems presents a significant barrier to entry. A fully configured SDD-based analysis system can cost between $150,000 to $500,000, with annual maintenance adding 10-15% to operational budgets. This pricing structure makes the technology inaccessible for smaller laboratories and educational institutions operating under constrained budgets. Manufacturers face the dual challenge of maintaining performance standards while reducing production costs, particularly for emerging markets where price sensitivity is higher. Cryogenic cooling systems, while necessary for optimal performance, contribute significantly to both initial costs and long-term operational expenses.

Other Challenges

Technical Complexity in Integration

The integration of SDD sensors with existing laboratory equipment requires specialized expertise, creating implementation bottlenecks. Unlike conventional detectors, SDD systems demand precise alignment and calibration, often necessitating manufacturer-trained technicians. This requirement extends downtime during maintenance periods and increases total cost of ownership.

Supply Chain Vulnerabilities

The semiconductor shortages affecting global markets have indirectly impacted SDD sensor production timelines. With lead times for certain components extending beyond 12 months, manufacturers struggle to meet the increasing demand from research and industrial sectors.

MARKET RESTRAINTS

Performance Limitations in Extreme Conditions Hamper Certain Applications

Despite their advantages, SDD sensors exhibit performance degradation in high-temperature environments and under prolonged exposure to intense radiation. This characteristic restricts their use in certain industrial and aerospace applications where conventional detectors continue to dominate. The maximum operational temperature threshold of ~-30°C to +50°C presents challenges for field applications in harsh environments. While manufacturers have introduced advanced cooling solutions, these add complexity and cost, with performance improvements averaging only 15-20% in extreme conditions. Such limitations have slowed SDD adoption in sectors like oilfield exploration and defense applications, where reliability under adverse conditions is paramount.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy Create New Growth Potential

The rapid expansion of renewable energy technologies is generating novel applications for SDD sensors. In photovoltaic manufacturing, these detectors enable precise compositional analysis of thin-film solar cells, helping optimize conversion efficiencies. Battery research laboratories are increasingly adopting SDD-equipped systems to study next-generation energy storage materials at the atomic level. With global investments in clean energy research exceeding $1 trillion annually, the potential addressable market for specialized analytical equipment continues to expand. Manufacturers who develop application-specific SDD configurations for these emerging sectors stand to capture significant market share in coming years.

Miniaturization Trends Open Doors for Compact SDD Solutions

Advances in semiconductor manufacturing have enabled the development of compact SDD modules suitable for portable analytical instruments. Field-deployable XRF analyzers incorporating these miniaturized detectors are gaining traction in mining, archaeology, and environmental monitoring applications. The portable analyzers market, currently valued at approximately $2.5 billion, is projected to grow at 8% CAGR through 2030, with SDD-based solutions capturing an increasing share. Manufacturers focusing on size reduction without compromising performance metrics can capitalize on this trend, particularly in regions with growing field science requirements.

SILICON DRIFT DETECTOR SENSOR MARKET TRENDS

Growth in Semiconductor Demand Boosts Silicon Drift Detector Sensor Market

The global Silicon Drift Detector (SDD) Sensor market is experiencing robust growth, driven by increasing demand in advanced material analysis and semiconductor manufacturing. SDDs, widely used for X-ray spectrometry (XRF and EDS) and electron microscopy, have gained traction due to their high energy resolution and quicker data acquisition compared to traditional detectors. The market, valued at $294 million in 2024, is projected to surge to $607 million by 2032, expanding at a CAGR of 11.2%. This rapid growth is fueled by the semiconductor industry’s expansion, which saw analog and sensor segments growing by 20.8% and 16.3% respectively in 2022 despite macroeconomic challenges. The integration of SDDs in high-sensitivity applications, such as failure analysis in semiconductor fabrication, is accelerating adoption.

Other Trends

Advancements in Analytical Instrumentation

The increasing complexity of material characterization in industries such as pharmaceuticals, aerospace, and mining is driving innovation in SDD technology. Companies are focusing on developing detectors with larger active areas (e.g., >100 mm²) for enhanced sensitivity in low-concentration sample analysis. For instance, X-ray fluorescence (XRF) applications now demand SDDs capable of detecting trace elements with minimal interference, boosting the segment’s market share. Electron microscopy, another key application, is projected to grow significantly due to rising R&D investments in nanotechnology and life sciences, where SDDs provide superior resolution for microstructural analysis.

Expansion of Industrial Automation and Quality Control

Industrial automation is transforming quality control processes, particularly in manufacturing sectors requiring real-time elemental analysis. SDDs are increasingly integrated into automated XRF spectrometers for on-site material testing in metal fabrication, recycling, and environmental monitoring. The Asia-Pacific region, despite a semiconductor market contraction of 2% in 2022, remains a critical growth area due to expanding electronics production in China and South Korea. Moreover, regulatory pressures for stricter material compliance (e.g., RoHS and REACH) are compelling manufacturers to adopt SDD-based solutions for precise contaminant detection in finished products, further propelling market demand.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Drive Innovation in High-Precision Detection Technology

The global silicon drift detector (SDD) sensor market features a competitive yet moderately fragmented landscape, with key players accounting for approximately 65% of market revenue in 2024. Ketek GmbH maintains its leadership position through continuous innovation in radiation detection technology, holding an estimated 18% revenue share. The company’s SDD products are widely adopted in electron microscopy applications, particularly in semiconductor failure analysis laboratories.

Amptek (AMETEK) follows closely with 15% market share, leveraging its expertise in X-ray instrumentation to deliver high-resolution detectors for both industrial and research applications. Their recent product development focuses on improving energy resolution below 125 eV at Mn Kα, which has become an industry benchmark for performance.

Meanwhile, Mirion Technologies has been expanding its presence through strategic acquisitions, including the purchase of a radiation detection division from Thermo Fisher Scientific in 2023. This move strengthened their capability across multiple application segments, from security screening to materials science.

Emerging players like Nuchip Photoelectric are challenging established brands with competitively priced alternatives, particularly in the Asia-Pacific market. Their rapid growth reflects the increasing demand for cost-effective solutions in educational institutions and smaller research facilities.

List of Key Silicon Drift Detector Sensor Manufacturers

- Ketek GmbH (Germany)

- Amptek Inc. (AMETEK) (U.S.)

- Mirion Technologies (U.S.)

- RaySpec Ltd (UK)

- PNDetector GmbH (Germany)

- Nuchip Photoelectric Technology Co., Ltd. (China)

- Bruker Corporation (U.S.)

- Oxford Instruments (UK)

Segment Analysis:

By Type

Active Area ≤ 30 mm² Segment Leads Due to High Precision Requirements in Compact Devices

The market is segmented based on type into:

- Active Area ≤ 30 mm²

- 30 mm² < Active Area ≤ 100 mm²

- Active Area > 100 mm²

By Application

EDS Application Dominates Owing to Widespread Use in Material Science and Semiconductor Analysis

The market is segmented based on application into:

- X-ray Fluorescence (XRF)

- Energy Dispersive Spectroscopy (EDS)

- Electron Microscopy

- Others

By End-Use Industry

Semiconductor Industry Holds Significant Share Due to Increasing Demand for Quality Inspection

The market is segmented based on end-use industry into:

- Semiconductor

- Healthcare and Life Sciences

- Industrial Manufacturing

- Research Institutions

- Others

Regional Analysis: Silicon Drift Detector Sensor Market

Asia-Pacific

The Asia-Pacific region dominates the Silicon Drift Detector (SDD) sensor market with over 42% global market share in 2024. This leadership stems from China’s booming semiconductor industry and Japan’s advanced electronics manufacturing ecosystem. China alone contributes nearly 60% of regional demand, with key applications in metal analysis (XRF) and semiconductor quality control (EDS). While India shows promising growth in analytical instrumentation, price sensitivity remains a challenge. South Korea and Taiwan are adoption hotspots for electron microscopy applications, benefiting from their strong semiconductor fabrication facilities. The region’s lower production costs also attract SDD manufacturers to establish local operations, though technology sophistication still trails Western markets.

North America

North America represents the most technologically advanced SDD sensor market, characterized by high-value applications in research laboratories and defense sectors. The U.S. accounts for 82% of regional demand, driven by robust investments in materials science research (notably at DOE national labs) and shale gas exploration (requiring portable XRF analyzers). Stringent safety regulations in the oil & gas industry are accelerating the replacement of older detectors with SDD technologies. Major manufacturers like Amptek maintain R&D centers in Massachusetts, benefiting from academic partnerships with MIT and Harvard. Canada shows growing adoption in mining sector applications, though market penetration remains below potential.

Europe

Europe’s SDD market thrives on precision-focused applications, with Germany, France, and the UK leading adoption. The region holds particular strength in electron microscopy systems, where Zeiss and Thermo Fisher Scientific integrate SDDs into advanced materials characterization tools. EU-funded research initiatives for nanotechnology and clean energy solutions are creating sustained demand. Scandinavian countries demonstrate above-average growth, especially in environmental monitoring applications. However, complex certification processes under CE marking regulations occasionally slow product launches. Eastern Europe shows untapped potential, currently limited by budget constraints in academic and industrial research sectors.

South America

The South American SDD sensor market remains in development stage, concentrated primarily in Brazil’s mining and oil industries. Portable XRF guns for ore analysis represent the largest application segment. Argentina shows growing activity in agricultural soil testing, though economic volatility frequently disrupts capital equipment investments. Regional demand suffers from limited local technical support and high import duties on analytical instruments. Nevertheless, copper mining expansions in Chile and Peru forecast promising medium-term growth, particularly for field-deployable SDD solutions that reduce laboratory dependence.

Middle East & Africa

This emerging market shows concentrated demand in Gulf Cooperation Council (GCC) countries, particularly for petroleum and precious metal analysis. The UAE leads in adoption, with Dubai’s gold trade driving XRF analyzer requirements. Saudi Arabia’s Vision 2030 industrialization plans are beginning to generate demand for quality control instrumentation. Africa’s market remains largely untapped, though South Africa demonstrates steady growth in mining applications. Israel presents a unique case with strong capabilities in detector technology development, though primarily for defense applications rather than commercial SDD systems. Infrastructure limitations and intermittent power supply constrain broader African adoption.

Report Scope

This market research report provides a comprehensive analysis of the Global Silicon Drift Detector Sensor market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 294 million in 2024 and is projected to reach USD 607 million by 2032, growing at a CAGR of 11.2%.

- Segmentation Analysis: Detailed breakdown by product type (Active Area ≤ 30 mm², 30 mm² ≤ Active Area ≤ 100 mm², Active Area ≥ 100 mm²), application (XRF, EDS, Electron Microscopy, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. In 2024, Asia-Pacific accounted for the largest share, while Europe showed significant growth potential.

- Competitive Landscape: Profiles of leading market participants including Ketek, RaySpec, Mirion Technologies, PNDetector, Amptek (AMETEK), and Nuchip Photoelectric, with analysis of their market share, product portfolios, and recent developments.

- Technology Trends & Innovation: Assessment of emerging semiconductor fabrication techniques, integration with AI/ML for enhanced X-ray detection, and improvements in detector resolution and efficiency.

- Market Drivers & Restraints: Evaluation of factors such as increasing demand for material analysis in semiconductor manufacturing, growth in electron microscopy applications, along with challenges like high production costs and supply chain constraints.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, analytical instrument OEMs, research institutions, and investors regarding market opportunities and competitive positioning.

Primary and secondary research methods were employed, including interviews with industry experts and analysis of verified market data, to ensure the accuracy and reliability of the findings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Silicon Drift Detector Sensor Market?

-> Silicon Drift Detector Sensor market was valued at 294 million in 2024 and is projected to reach US$ 607 million by 2032, at a CAGR of 11.2% during the forecast period.

Which key companies operate in Global Silicon Drift Detector Sensor Market?

-> Key players include Ketek, RaySpec, Mirion Technologies, PNDetector, Amptek (AMETEK), and Nuchip Photoelectric.

What are the key growth drivers?

-> Growth is driven by increasing demand for material analysis in semiconductor manufacturing, advancements in electron microscopy, and expanding applications in XRF and EDS technologies.

Which region dominates the market?

-> Asia-Pacific holds the largest market share, while North America shows strong growth due to technological advancements and R&D investments.

What are the emerging trends?

-> Emerging trends include integration of AI for improved detection accuracy, development of higher resolution detectors, and increasing adoption in semiconductor quality control applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...