MARKET INSIGHTS

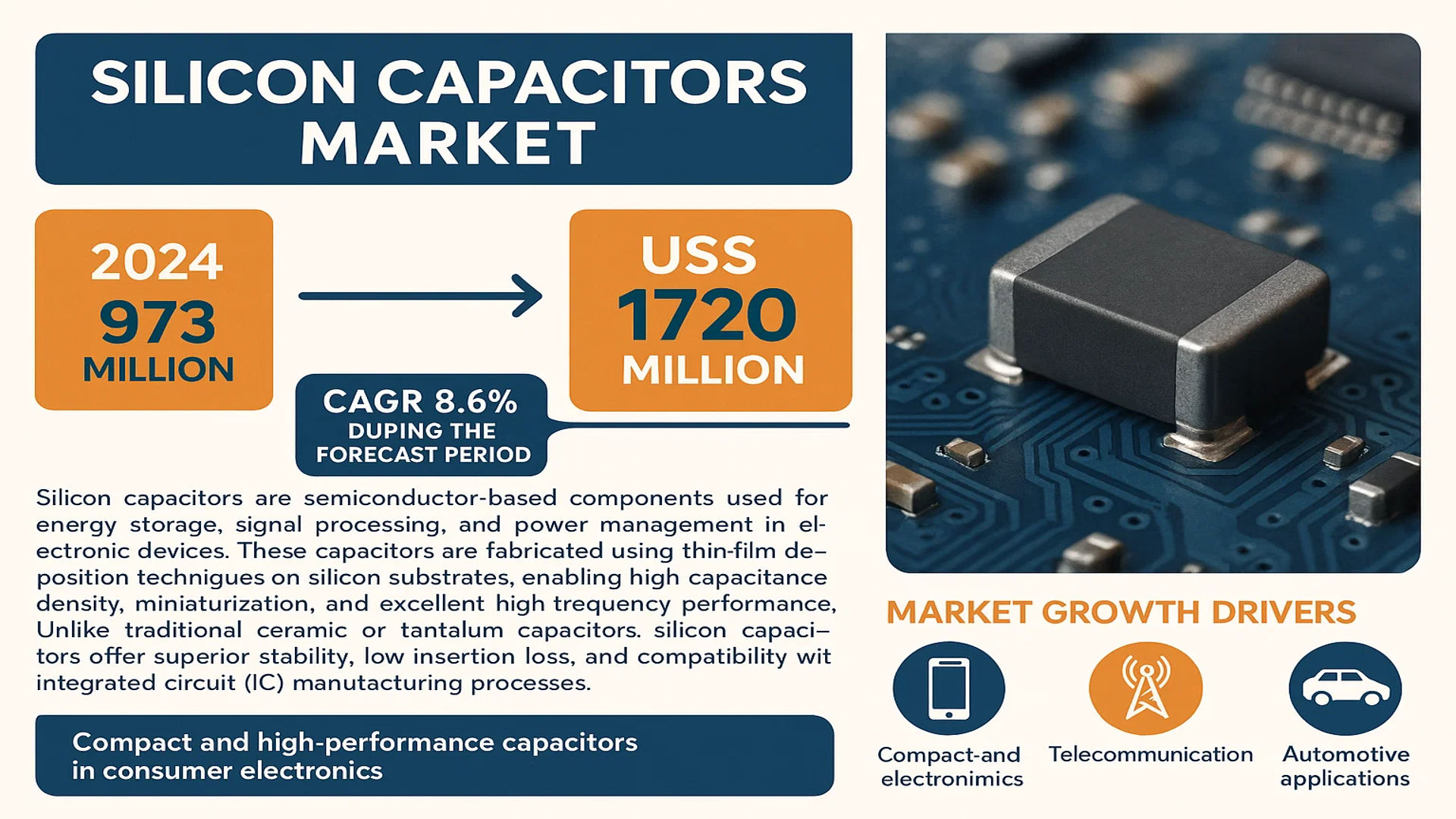

The global Silicon Capacitors Market was valued at 973 million in 2024 and is projected to reach US$ 1720 million by 2032, at a CAGR of 8.6% during the forecast period.

Silicon capacitors are semiconductor-based components used for energy storage, signal processing, and power management in electronic devices. These capacitors are fabricated using thin-film deposition techniques on silicon substrates, enabling high capacitance density, miniaturization, and excellent high-frequency performance. Unlike traditional ceramic or tantalum capacitors, silicon capacitors offer superior stability, low insertion loss, and compatibility with integrated circuit (IC) manufacturing processes.

The market growth is driven by increasing demand for compact and high-performance capacitors in consumer electronics, telecommunications, and automotive applications. The proliferation of 5G networks, IoT devices, and electric vehicles further accelerates adoption. Key players such as Murata Manufacturing, KYOCERA AVX, and Vishay Intertechnology are expanding their product portfolios to meet evolving industry needs, leveraging advancements in semiconductor technology.

MARKET DYNAMICS

MARKET DRIVERS

Miniaturization of Electronic Devices to Drive Silicon Capacitor Demand

The relentless trend toward smaller and more powerful electronic devices is a key driver for silicon capacitors. With smartphones, wearables, and IoT devices shrinking in size while increasing in functionality, traditional capacitors struggle to meet space constraints. Silicon capacitors, with their ultra-thin film construction and high capacitance density, provide an ideal solution. Their ability to be directly integrated into semiconductor packages makes them indispensable for modern compact electronics. The smartphone industry alone consumed nearly 1.5 billion silicon capacitor units in 2023, with projections showing a 12% annual growth through 2030.

Electric Vehicle Adoption Accelerating Capacitor Requirements

The global shift toward electric mobility presents substantial opportunities for silicon capacitor manufacturers. Modern EVs require high-reliability capacitors for battery management systems, onboard chargers, and power converters. Silicon capacitors’ ability to operate at extreme temperatures while maintaining performance makes them particularly valuable. With EV production expected to reach 35 million units annually by 2030, their demand for silicon capacitors in voltage regulation and energy storage applications is projected to grow at 20% CAGR.

5G Infrastructure Deployment Creating New Applications

The rollout of 5G networks worldwide is creating strong demand for high-frequency components where silicon capacitors excel. Their low insertion loss at microwave frequencies makes them ideal for RF front-end modules, base stations, and millimeter-wave applications. Telecom infrastructure investments are expected to exceed $300 billion globally between 2024-2030, with a significant portion allocated to components that enable higher bandwidth and lower latency communication.

MARKET RESTRAINTS

High Production Costs Limiting Market Penetration

Despite their advantages, silicon capacitors face cost-related adoption barriers in price-sensitive markets. The semiconductor-grade manufacturing processes required for these components result in prices 3-5 times higher than conventional ceramic capacitors. While the performance benefits justify costs in high-end applications, many consumer electronics manufacturers continue to favor cheaper alternatives where silicon capacitor advantages aren’t critical.

Supply Chain Vulnerabilities Impacting Availability

The specialized fabrication facilities required for silicon capacitor production create potential supply chain risks. With over 70% of global production capacity concentrated in a handful of specialized foundries, any disruptions can quickly lead to shortages. These vulnerabilities became particularly apparent during recent semiconductor supply chain crises, forcing some manufacturers to redesign circuits using alternative components.

Technical Limitations at Extreme Voltages

While silicon capacitors excel in low-voltage applications, their performance becomes less competitive above certain voltage thresholds. Most silicon capacitor products are rated below 100V, limiting their use in high-power industrial and energy applications where film or electrolytic capacitors remain dominant. Developing higher voltage silicon capacitors without compromising size or reliability presents ongoing material science challenges.

MARKET OPPORTUNITIES

Medical Electronics Creating New High-Value Applications

The medical device industry presents significant growth opportunities for silicon capacitors, driven by increasing demand for implantable and wearable medical technologies. Their biocompatibility, reliability, and small form factor make them ideal for devices like pacemakers, hearing aids, and continuous glucose monitors. The global market for implantable medical electronics is projected to exceed $80 billion by 2028, creating substantial demand for miniaturized passive components that meet stringent medical standards.

Automotive Electrification Expanding Component Requirements

Beyond EVs, broader automotive electrification trends are creating new capacitor applications. Advanced driver assistance systems (ADAS), in-vehicle networking, and autonomous driving technologies all require reliable energy storage solutions. Silicon capacitors are particularly well-suited for these applications due to their vibration resistance and stable performance across automotive temperature ranges. The ADAS market alone is expected to grow at 15% annually through 2030, driving corresponding demand for supporting components.

Emerging AI Hardware Driving Component Innovation

The rapid development of artificial intelligence accelerators and edge computing devices is creating demand for specialized capacitors that can support high-performance computing. Silicon capacitors with their ability to handle high-frequency switching and provide localized decoupling are becoming increasingly important in AI chip packages. With AI hardware investments expected to grow at 30% CAGR over the next five years, this represents a major growth avenue for capacitor manufacturers.

MARKET CHALLENGES

Technical Complexity in High-Volume Manufacturing

The semiconductor processing required for silicon capacitors presents significant manufacturing challenges. Yield optimization becomes increasingly difficult as feature sizes shrink, with defects potentially affecting entire production batches. Maintaining over 95% yields on complex multi-layer capacitor structures requires substantial process control investments that can deter new market entrants.

Competition from Emerging Capacitor Technologies

While silicon capacitors currently lead in miniaturization, emerging technologies like ultra-thin ceramic capacitors and advanced polymer-based solutions present growing competition. Some new materials offer comparable performance characteristics at potentially lower costs, forcing silicon capacitor manufacturers to continually innovate to maintain their competitive edge.

Design Integration Complexities

The integration of silicon capacitors into modern electronic designs presents complex engineering challenges. Unlike discrete components, many silicon capacitor applications require close collaboration with semiconductor designers and process engineers early in the development cycle. This design complexity can extend product development timelines and increase engineering costs, particularly for companies new to silicon capacitor implementation.

SILICON CAPACITORS MARKET TRENDS

Miniaturization and High-Performance Demands Drive Silicon Capacitor Adoption

The growing demand for smaller, high-performance electronic components is accelerating the adoption of silicon capacitors, particularly in consumer electronics and IoT devices. These capacitors offer advantages such as low insertion loss at high frequencies and compact form factors, making them ideal for use in smartphones, wearables, and 5G modules. Innovations in thin-film deposition and semiconductor fabrication techniques have further enhanced their capacitance density, enabling manufacturers to meet the increasing need for power efficiency in next-generation devices. With the global silicon capacitors market projected to grow at a CAGR of 8.6%, advancements in these technologies are expected to continue shaping industry trends.

System-on-Chip (SoC) Integration

The integration of silicon capacitors into SoCs is emerging as a significant trend, particularly in applications requiring space optimization and improved energy efficiency. In the smartphone sector, manufacturers are embedding silicon capacitors directly into chipsets to reduce power consumption while enhancing signal integrity. This trend extends to AI processors and high-performance computing (HPC) applications, where silicon capacitors provide stable voltage regulation and noise suppression. By minimizing the need for discrete components, this integration is expected to streamline production processes while reducing overall system costs in sectors like telecommunications and data centers.

Growing Demand in Automotive and Renewable Energy Applications

Silicon capacitors are increasingly being utilized in electric vehicles (EVs) and power electronics, where their ability to handle high-voltage environments proves advantageous. In EVs, they are employed in battery management systems, onboard chargers, and inverters to ensure consistent energy delivery and fast-charging capabilities. Meanwhile, the shift toward renewable energy sources has amplified the need for reliable capacitors in grid stabilization and power conversion systems. As solar and wind energy infrastructure expands, silicon capacitors play a crucial role in managing fluctuations and improving power quality, making them indispensable in the transition to sustainable energy solutions.

Telecommunications and Medical Devices Fueling Growth

The expansion of 5G networks and the increasing deployment of IoT devices are driving demand for silicon capacitors in the telecommunications sector. These components are vital in RF signal processing and filtering, ensuring optimal performance in high-frequency applications such as base stations and satellite communications. Concurrently, the medical device industry is leveraging silicon capacitors in implantable and diagnostic equipment due to their reliability and longevity. From pacemakers to wearable health monitors, the ability to maintain consistent performance in compact form factors makes these capacitors essential for next-generation medical technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Competition in Silicon Capacitors Market

The global silicon capacitors market exhibits a competitive yet dynamic landscape, characterized by the presence of both established semiconductor giants and emerging innovators. As demand surges across applications like 5G infrastructure, automotive electronics, and IoT devices, companies are actively expanding their portfolios through advanced thin-film technologies and system integration capabilities. The market’s projected 8.6% CAGR until 2032 is fueling aggressive R&D investments among key players.

Murata Manufacturing leads the silicon capacitor segment with its proprietary multi-layer silicon capacitor technology, holding approximately 22% market share in 2024. The company’s recent $200 million investment in Kyoto semiconductor fabrication facilities reinforces its dominance in high-frequency RF applications. Similarly, KYOCERA AVX’s breakthrough in ultra-low ESR silicon capacitors has positioned it as a preferred supplier for electric vehicle power management systems.

Mid-tier competitors are gaining traction through specialization—Empower Semiconductor has captured significant market share in data center applications with its integrated voltage regulator silicon capacitors, while ELSPES focuses on medical-grade capacitors meeting stringent ISO 13485 standards. This diversification creates a multi-layered competitive environment where technological edge often outweighs company size.

Strategic partnerships are reshaping market dynamics. Vishay Intertechnology’s 2023 collaboration with a major automotive Tier 1 supplier accelerated its penetration into EV markets, demonstrating how alliances can disrupt traditional market share distributions. Meanwhile, ROHM Semiconductor leverages its vertical integration model to offer cost-competitive solutions for consumer electronics.

List of Key Silicon Capacitor Companies Profiled

- Murata Manufacturing Co., Ltd. (Japan)

- ROHM Semiconductor (Japan)

- KYOCERA AVX (U.S.)

- Vishay Intertechnology (U.S.)

- MACOM Technology Solutions (U.S.)

- Microchip Technology (U.S.)

- Skyworks Solutions (U.S.)

- Empower Semiconductor (U.S.)

- ELSPES (France)

Segment Analysis:

By Type

MOS Capacitors Lead the Market Due to Superior High-Frequency Performance

The market is segmented based on type into:

- MOS Capacitors

- Subtypes: Thin-film, Thick-film, and others

- MIS Capacitors

- Trench Silicon Capacitors

- Subtypes: Deep trench, Shallow trench, and others

- Silicon-on-Insulator (SOI) Capacitors

- Others

By Application

Telecommunication Dominates with High Demand for 5G Infrastructure

The market is segmented based on application into:

- Telecommunication

- Automotive

- Medical Devices

- Industrial

- Consumer Electronics

By End-User

Semiconductor Industry Accounts for Largest Adoption

The market is segmented based on end-user into:

- Semiconductor Manufacturers

- Electronic Component Suppliers

- Research Institutions

- System Integrators

- Others

Regional Analysis: Silicon Capacitors Market

Asia-Pacific

The Asia-Pacific region dominates the silicon capacitors market, accounting for over 45% of global demand, driven by robust electronics manufacturing in China, Japan, South Korea, and India. China’s semiconductor industry expansion, coupled with increasing investments in 5G infrastructure (projected to reach $180 billion by 2025), fuels demand for high-frequency silicon capacitors. Japan remains a key innovator, with companies like Murata Manufacturing and ROHM Semiconductor leading in thin-film capacitor development for consumer electronics. While cost sensitivity favors traditional capacitors in some applications, the region’s growing EV market and IoT adoption are accelerating the shift toward advanced silicon-based solutions.

North America

North America’s silicon capacitor market is propelled by cutting-edge R&D in power electronics and telecommunications. The U.S. accounts for nearly 75% of regional demand, with companies like Microchip Technology and Skyworks Solutions focusing on SoC-integrated capacitors for aerospace and data centers. Strict Federal Communications Commission (FCC) regulations on signal integrity and the push for renewable energy storage systems further drive innovation. Canada’s growing EV sector also presents opportunities, though higher production costs compared to Asia remain a challenge for widespread adoption.

Europe

Europe’s market emphasizes precision and sustainability, with Germany and France leading in automotive and industrial applications. The EU’s focus on energy-efficient electronics under the Ecodesign Directive supports demand for silicon capacitors in smart grids and medical devices. While the region trails Asia in production volume, its strength lies in specialized high-reliability capacitors for aerospace and healthcare. However, dependence on Asian suppliers for raw materials creates supply chain vulnerabilities, prompting recent investments in local semiconductor fabs under the EU Chips Act.

South America

The South American market shows emerging potential, particularly in Brazil’s automotive and telecom sectors. Limited local manufacturing capabilities result in heavy reliance on imports, primarily from the U.S. and Asia. Brazil’s National IoT Plan and Argentina’s renewable energy projects are driving gradual adoption, though economic instability and underdeveloped semiconductor infrastructure hinder faster growth. The region remains price-sensitive, with most demand concentrated in basic MOS capacitors for consumer electronics.

Middle East & Africa

This region represents a nascent but growing market, with the UAE, Israel, and Saudi Arabia investing in 5G networks and smart city initiatives. Israel’s strong tech sector utilizes silicon capacitors for military and medical applications, while Gulf countries increasingly adopt them for oil/gas monitoring systems. Africa’s market remains constrained by limited electronics manufacturing, though rising smartphone penetration in Nigeria and Kenya signals future opportunities. The lack of local production facilities keeps prices elevated compared to other regions.

Report Scope

This market research report provides a comprehensive analysis of the global Silicon Capacitors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Silicon Capacitors market was valued at USD 973 million in 2024 and is projected to reach USD 1720 million by 2032, growing at a CAGR of 8.6% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (MOS Capacitors, MIS Capacitors), application (Automotive, Medical, Telecommunication, Industrial, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific leads in market share due to high electronics manufacturing activity, while North America shows strong growth in advanced semiconductor applications.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Murata Manufacturing, ROHM Semiconductor, KYOCERA AVX, and Vishay Intertechnology.

- Technology Trends & Innovation: Assessment of emerging technologies including System-on-Chip (SoC) integration, high-density capacitors for mobile devices, and applications in electric vehicles and renewable energy systems.

- Market Drivers & Restraints: Evaluation of factors driving market growth (miniaturization of electronics, EV adoption, 5G expansion) along with challenges (supply chain constraints, high fabrication costs).

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in silicon capacitor technologies.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Silicon Capacitors Market?

-> Silicon Capacitors Market was valued at 973 million in 2024 and is projected to reach US$ 1720 million by 2032, at a CAGR of 8.6% during the forecast period.

Which key companies operate in Global Silicon Capacitors Market?

-> Key players include Murata Manufacturing, ROHM Semiconductor, KYOCERA AVX, Vishay Intertechnology, MACOM, and Microchip Technology, among others.

What are the key growth drivers?

-> Key growth drivers include demand for miniaturized electronics, expansion of 5G networks, electric vehicle adoption, and renewable energy applications.

Which region dominates the market?

-> Asia-Pacific dominates the market due to high electronics manufacturing activity, while North America shows strong growth in advanced applications.

What are the emerging trends?

-> Emerging trends include System-on-Chip integration, high-density capacitors for mobile devices, and applications in EV power management systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...