MARKET INSIGHTS

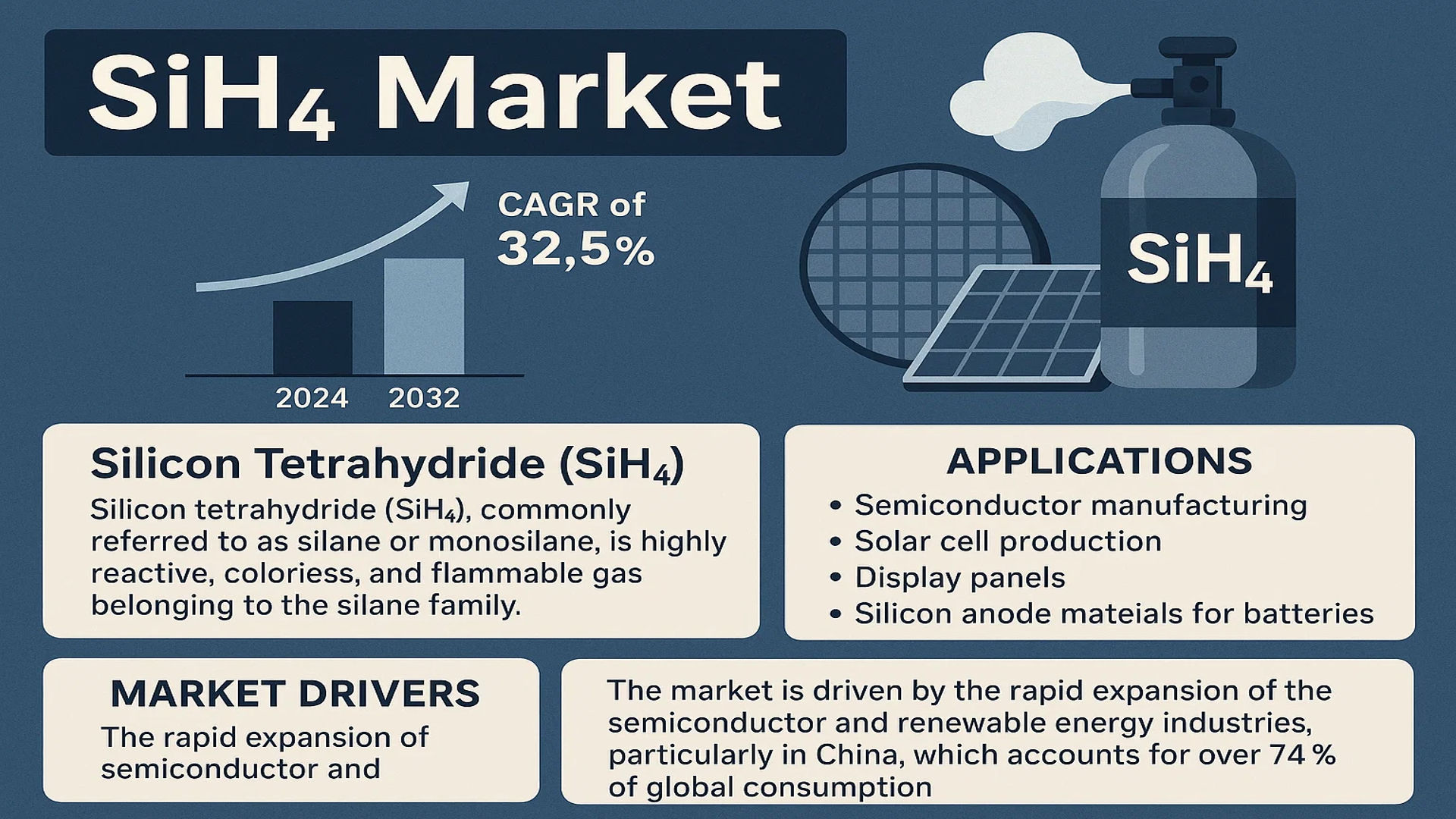

The global SiH4 Market was valued at 871 million in 2024 and is projected to reach US$ 5481 million by 2032, at a CAGR of 32.5% during the forecast period.

Silicon tetrahydride (SiH4), commonly referred to as silane or monosilane, is a highly reactive, colorless, and flammable gas belonging to the silane family. It plays a critical role in semiconductor manufacturing, solar cell production, display panels, and silicon anode materials for batteries. SiH4 is synthesized through the catalytic reaction of silicon with hydrogen gas, followed by purification via distillation to ensure high purity.

The market is driven by the rapid expansion of the semiconductor and renewable energy industries, particularly in China, which accounts for over 74% of global consumption. The demand for high-purity SiH4 (≥6N) dominates the market, holding more than 90% share due to stringent industry requirements. Key applications include solar cells (47% market share) and silicon anode materials (35% market share), with the latter expected to grow significantly. Major players like REC Silicon, Air Liquide, and Linde collectively hold nearly half of the global supply.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High-Purity Silane in Semiconductor Manufacturing to Accelerate Market Growth

The semiconductor industry’s expansion is a primary driver for the SiH4 market, with silane being a critical precursor for silicon deposition in integrated circuits and flat panel displays. The increasing adoption of advanced semiconductor technologies, such as 5G, IoT, and artificial intelligence, demands high-purity silane (≥6N) to ensure optimal performance and yield in chip fabrication. Semiconductor foundries worldwide are expanding production capacities to meet the rising demand, with global semiconductor sales projected to exceed $600 billion by 2025. This growth directly translates into higher consumption of silane for applications such as epitaxial silicon growth, chemical vapor deposition (CVD), and atomic layer deposition (ALD).

Solar Energy Expansion and Government Support to Fuel Silane Consumption

The photovoltaic sector accounts for nearly half of global silane consumption, driven by the rapid expansion of solar energy infrastructure. Crystalline silicon solar panels, which dominate the market with over 95% share, rely heavily on silane for anti-reflective coatings and silicon wafer production. Renewable energy targets set by governments worldwide are accelerating solar adoption, with annual global photovoltaic installations expected to surpass 350 GW by 2025. Countries like China, India, and the U.S. are implementing favorable policies and subsidies, further boosting demand for high-purity silane in solar cell manufacturing.

➤ For instance, China’s 14th Five-Year Plan aims to increase non-fossil energy consumption to 20% by 2025, directly driving investment in solar panel production and related materials like silane.

Furthermore, technological advancements in solar cell efficiency, particularly the transition to PERC (Passivated Emitter and Rear Cell) technology and heterojunction cells, are enhancing silane consumption per panel. These efficiency improvements require more sophisticated deposition processes that utilize higher volumes of ultra-pure silane.

MARKET RESTRAINTS

Stringent Safety Regulations and Handling Challenges to Limit Market Expansion

Silane’s highly pyrophoric nature presents significant challenges to market growth, requiring specialized handling and storage infrastructure. The gas spontaneously ignites in air at concentrations as low as 1-3%, necessitating expensive safety systems including gas detection, suppression equipment, and explosion-proof facilities. These safety requirements add substantial costs to silane procurement and usage, particularly for small and medium-sized manufacturers. Regulatory bodies worldwide have implemented strict guidelines for silane transportation, storage, and usage, with compliance costs often representing 15-20% of total silane-related expenditures.

Volatile Raw Material Prices to Impact Market Stability

Silane production depends on silicon metal and hydrogen gas, both subject to price fluctuations that affect overall market dynamics. Silicon metal prices have shown volatility of ±25% annually due to energy cost variations and production capacity changes, particularly in China which controls over 70% of global silicon metal production. These upstream cost variations create pricing uncertainty for silane manufacturers, who often struggle to pass increased costs to end-users in highly competitive markets like solar panel manufacturing. Furthermore, regional disparities in energy costs create uneven competitive landscapes, with manufacturers in high-energy-cost regions facing profitability challenges.

MARKET OPPORTUNITIES

Silicon Anode Revolution in Batteries to Create New Growth Avenue

The emerging silicon anode battery market presents a significant opportunity for silane producers. Silicon-based anodes can theoretically store ten times more lithium ions than conventional graphite anodes, dramatically improving battery energy density. Major battery manufacturers are investing heavily in silicon anode technology, with market adoption expected to grow at over 40% CAGR through 2030. Silane serves as a key precursor for silicon nanoparticle production used in these advanced anodes, with consumption expected to triple in this application by 2027.

Technological Advancements in Silane Production to Enhance Market Potential

Innovations in silane production technology are creating cost reduction opportunities that could expand market accessibility. New catalytic processes and purification techniques are improving yield and reducing energy consumption in silane manufacturing. For example, some manufacturers have developed continuous production methods that reduce energy usage by up to 30% compared to traditional batch processes. These advancements could lower the price premium for high-purity silane, making it more accessible to mid-tier semiconductor and solar manufacturers.

MARKET CHALLENGES

Geopolitical Tensions and Supply Chain Vulnerabilities to Create Market Uncertainty

The silane market faces significant challenges from geopolitical factors affecting supply chains and trade flows. China dominates both production and consumption, creating vulnerabilities for global supply. Recent trade restrictions and export controls in the semiconductor sector have demonstrated how quickly geopolitical tensions can disrupt specialty gas markets. Many manufacturers are seeking to diversify supply sources, but building new production capacity requires substantial capital investment and lengthy lead times, maintaining market fragility.

Other Challenges

Environmental Concerns

While silane enables clean energy technologies, its production has notable environmental impacts. The process generates significant greenhouse gas emissions, particularly from silicon metal production which is highly energy-intensive. Stricter environmental regulations in key producing regions may constrain capacity expansion and increase production costs.

Substitution Threats

Alternative deposition technologies and materials pose long-term challenges to silane demand. Atomic layer deposition using metalorganic precursors and developments in alternative semiconductor materials like gallium nitride could potentially reduce silane consumption in certain applications.

SIH4 MARKET TRENDS

Rising Demand in Semiconductor and Solar Industries Driving Market Growth

The SiH4 (silane) market is experiencing significant growth, primarily fueled by its expanding applications in semiconductor manufacturing and photovoltaic (solar) cell production. With the global market valued at $871 million in 2024 and projected to reach $5,481 million by 2032, the compound annual growth rate (CAGR) of 32.5% reflects robust demand. Silane’s critical role in depositing thin-film silicon layers for semiconductors and enhancing solar panel efficiency remains a key factor. Additionally, advancements in high-purity silane (≥6N), which currently holds over 90% market share, have improved performance in these applications, reducing defects and increasing energy conversion rates.

Other Trends

Expansion in Battery Silicon Anode Materials

The electric vehicle (EV) and energy storage sectors are driving demand for high-performance silicon-based anode materials, where silane is an essential precursor. Currently, battery silicon anode applications account for nearly 35% of the global SiH4 market, trailing only solar cells (47%). The shift towards silicon-rich anodes, which offer higher energy density compared to traditional graphite, is accelerating investments in silane-based material production. Given the rapid adoption of EVs and grid storage solutions, this segment is expected to surpass solar applications within the next decade, becoming the dominant market driver.

Technological Advancements and Regional Market Dynamics

Innovations in silane production, including more efficient purification techniques and safer handling protocols, are enhancing market scalability—particularly for industries requiring ultra-high-purity grades. Meanwhile, regional dynamics highlight China’s dominance, consuming 74% of global silane output due to its thriving semiconductor and solar manufacturing sectors. While global leaders like REC Silicon (12.89% market share) and Air Liquide maintain strong positions, Chinese manufacturers are rapidly expanding capacity to meet domestic demand. Supply chain diversification and localized production strategies are emerging as critical trends, ensuring stable availability amid geopolitical and logistical uncertainties.

COMPETITIVE LANDSCAPE

Key Industry Players

Expanding Industrial Applications Drive Innovation Among Market Leaders

The global SiH4 (silane) market features a moderately consolidated competitive structure, with several key multinational corporations dominating production and regional players strengthening their foothold. REC Silicon leads the market with a 12.89% share (2024), leveraging its vertically integrated silicon production and strategic partnerships across the solar and semiconductor value chains. The company’s strong position is reinforced by its Moses Lake facility in the U.S. and expansion plans in Asia.

Air Liquide and Linde plc together command over 20% market share through their industrial gas expertise and global distribution networks. These players are investing heavily in high-purity silane production to meet semiconductor industry demands, where 6N+ purity grades now represent over 90% of total supply. Their technological edge in gas purification and cylinder packaging gives them competitive advantage in safety-critical applications.

Chinese manufacturers like Inner Mongolia Xingyang Technology and CNS are rapidly gaining market share through cost leadership. Collectively controlling 15% of global capacity, they benefit from China’s 74% consumption share and government support for silicon-based energy technologies. These regional players are now expanding into international markets with competitively priced offerings for battery anode materials.

List of Key SiH4 Manufacturers Profiled

- REC Silicon (Norway/U.S.)

- Air Liquide S.A. (France)

- Linde plc (Ireland/U.K.)

- Inner Mongolia Xingyang Technology Co., Ltd. (China)

- Central Glass Co., Ltd. (Japan)

- Merck KGaA (Germany)

- Momentive Performance Materials (U.S.)

- Gelest, Inc. (U.S.)

- EVONIK Industries AG (Germany)

- Dow Corning (U.S.)

The competitive environment is intensifying as companies vertically integrate to secure silicon feedstock and establish captive consumption channels. While semiconductor applications remain the premium segment, battery anode materials are emerging as the next battleground, projected to eclipse solar applications by 2028. Market leaders are actively forming joint ventures with lithium-ion battery manufacturers, while smaller players focus on regional distribution partnerships to maintain relevance.

Segment Analysis:

By Type

Purity ≥6N Segment Leads Due to High Demand in Semiconductor and Solar Applications

The market is segmented based on type into:

- Purity ≥6N

- Subtypes: Electronic Grade and Technical Grade

- Purity <6N

By Application

Solar Cells Segment Dominates Due to Growing Renewable Energy Investments

The market is segmented based on application into:

- Solar cells

- Semiconductor manufacturing

- Battery silicon anode material

- Display panels

- Others

By End-Use Industry

Electronics Industry Captures Major Share Owing to Silicon Chip Demand

The market is segmented based on end-use industry into:

- Electronics

- Subtypes: Semiconductor, Display, Photovoltaic

- Energy storage

- Chemical

- Others

By Purity Grade

Electronic Grade Silicon Tetrahydride Preferred for Critical Manufacturing Processes

The market is segmented based on purity grade into:

- Electronic Grade

- Technical Grade

- Commercial Grade

Regional Analysis: SiH4 Market

Asia-Pacific

The Asia-Pacific region dominates the global SiH4 market, accounting for over 74% of consumption, with China leading due to its massive semiconductor and solar industries. Rapid expansion in electronics manufacturing, combined with government-backed renewable energy initiatives, sustains high demand for high-purity silane (>6N). Key players like Inner Mongolia Xingyang Technology supply both domestic and international markets, though supply chain disruptions remain a concern. India shows accelerating adoption in photovoltaic applications, supported by the Production Linked Incentive (PLI) scheme for solar module manufacturing. While cost competitiveness drives bulk procurement, stricter environmental policies are gradually shaping production methods toward reduced emissions.

North America

North America’s SiH4 market thrives on advanced semiconductor fabrication and energy storage technologies, with REC Silicon being a major producer. The U.S. CHIPS and Science Act has spurred investments exceeding $52 billion in domestic chip production, indirectly boosting silane demand for deposition processes. California’s stringent air quality regulations push manufacturers toward closed-loop silane handling systems. A notable shift is emerging toward battery-grade silane for silicon anode materials, aligned with EV adoption targets. Canada contributes through R&D in thin-film solar applications, though infrastructure limitations hinder large-scale production.

Europe

Europe emphasizes eco-efficient silane production under REACH regulations, with Linde and Air Liquide pioneering low-emission synthesis methods. The region’s focus on photovoltaic efficiency and MEMS (Micro-Electro-Mechanical Systems) sensors drives demand for ultra-high-purity SiH4. Germany’s Fraunhofer Institute collaborations with industrial partners accelerate innovations in silane-based thin-film technologies. However, reliance on imports for bulk quantities persists due to higher operational costs. The EU’s carbon border tax may reshape trade dynamics, incentivizing local silane production for solar panel exporters.

Middle East & Africa

This region shows nascent potential, primarily via partnerships with Asian suppliers for solar energy projects. Saudi Arabia’s Vision 2030 includes silane-dependent polysilicon production, while South Africa explores localized gas synthesis for niche electronics applications. Growth is constrained by limited technical expertise and logistical hurdles, but rising FDI in renewable energy infrastructure suggests gradual market maturation. The UAE’s semiconductor packaging units present a growing niche for specialty silane grades.

South America

Brazil and Argentina exhibit sporadic demand linked to photovoltaic installations and electronic component assembly. Chile’s lithium-ion battery initiatives may spur future silane consumption for anode materials. Market expansion faces barriers like inconsistent raw material access and fluctuating import costs, though Mercosur trade agreements could improve supply stability. Local players focus on distributing imported silane rather than production, given the region’s limited industrial gas infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the Global SiH4 (Silicon Tetrahydride/Silane) market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global SiH4 market was valued at USD 871 million in 2024 and is projected to reach USD 5,481 million by 2032, growing at a CAGR of 32.5%.

- Segmentation Analysis: Detailed breakdown by product type (purity ≥6N vs. lower grades), application (semiconductors, solar cells, display panels, battery silicon anode materials), and end-use industries.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific (dominant 74% market share), Latin America, and Middle East & Africa, with China as the leading consumer.

- Competitive Landscape: Profiles of leading manufacturers including REC Silicon (12.89% market share), Air Liquide, Linde, Inner Mongolia Xingyang Technology, and CNS, covering their production capacities and strategic initiatives.

- Technology Trends: Analysis of evolving semiconductor fabrication techniques, advancements in solar cell production, and innovations in silicon anode battery materials.

- Market Drivers & Restraints: Evaluation of factors such as semiconductor industry growth, renewable energy demand, supply chain constraints, and safety regulations for pyrophoric materials.

- Stakeholder Analysis: Strategic insights for chemical suppliers, semiconductor manufacturers, solar panel producers, battery makers, and investors.

The research methodology incorporates primary interviews with industry experts, analysis of company financials, and validation through multiple verified data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global SiH4 Market?

-> SiH4 Market was valued at 871 million in 2024 and is projected to reach US$ 5481 million by 2032, at a CAGR of 32.5% during the forecast period.

Which key companies operate in Global SiH4 Market?

-> Leading players include REC Silicon, Air Liquide, Linde, Inner Mongolia Xingyang Technology, and CNS, with the top five companies holding 47% market share collectively.

What are the key growth drivers?

-> Primary growth drivers include semiconductor industry expansion, solar energy adoption (47% market share), and battery silicon anode material development (35% market share).

Which region dominates the market?

-> Asia-Pacific commands 74% market share, with China as the dominant consumer, followed by North America and Europe.

What are the emerging trends?

-> Key trends include high-purity SiH4 demand (>6N purity holds 90% share), silicon anode battery technology advancement, and integrated production facilities near end-use markets.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...